I’ve been there too. You’re standing near an ATM, and you only have your Capital One credit card in your wallet. The contractor wants cash. The bill needs to be split. The taxi only takes paper money. And you have no idea if your credit card will even work, or what it might cost if it does.

Yes, you can withdraw cash from an ATM with a Capital One credit card by using a cash advance, but it comes with a fee, a higher interest rate, and no grace period.

Below, you’ll get the exact steps, real-dollar cost math on a $200 withdrawal, PIN setup help, and cheaper backup options before you tap that screen.

Key Takeaways

This guide explains how to withdraw cash from an ATM using a Capital One credit card, covering the cash advance process, PIN setup, real fee and interest costs, and cheaper alternatives.

Core Facts:

- A Capital One credit card cash withdrawal at an ATM is processed as a cash advance, which carries its own fee, a higher APR, and no grace period.

- Capital One’s cash advance fee is $5 or 5% of the withdrawal amount, whichever is higher, charged the moment the cash leaves the ATM.

- The cash advance APR on most Capital One cards ranges from about 28.49% to 29.99% variable, and interest starts accruing the same day, even if the balance is paid in full.

- A cash advance PIN must be set up separately through the Capital One app, website, or by phone, since it is not mailed automatically with a new card.

- The cash advance limit is a smaller portion of the total credit limit, typically 20% to 50%, so it is possible to be declined even with available credit remaining.

- Carrying a $200 cash advance balance for one billing cycle costs around $218.33 once the cash advance fee, a typical ATM operator surcharge, and 30 days of interest are included.

Best for:

- Readers who already have a Capital One credit card and need to know the exact steps, fees, and PIN requirements before using it at an ATM.

- People weighing whether a cash advance is worth it for an urgent, short-term cash need versus a debit card or peer-to-peer payment app.

- Travelers wanting to understand how Capital One credit card ATM withdrawals work internationally, including foreign transaction fee policy.

Can You Use a Capital One Credit Card at an ATM?

Yes. You can use a Capital One credit card at most ATMs in the United States and around the world. If the ATM accepts Visa or Mastercard, it will almost always accept your card. Capital One issues cards on both networks, so coverage is wide.

But there’s a catch. Pulling cash from an ATM with a credit card is not the same as using a debit card. The bank treats it as a cash advance. That changes the fees, the interest, and the rules. So while the answer to “can you use a Capital One card at an ATM” is yes, the real question is whether you should.

A Capital One credit card cash withdrawal is allowed on every standard Capital One consumer credit card, including Quicksilver, Venture, SavorOne, and Platinum. The mechanics are the same across products. Only the limits and rates differ.

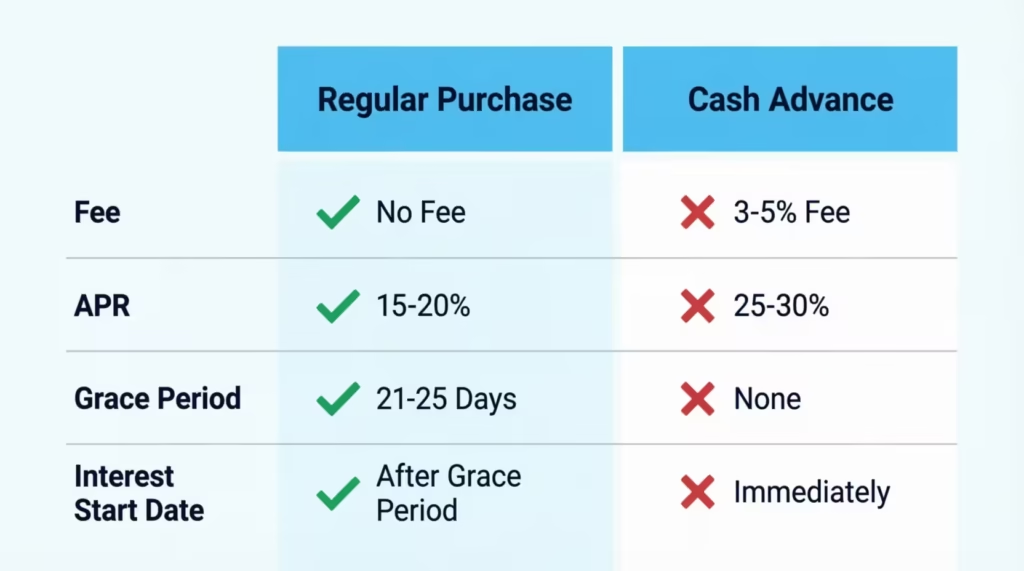

What a Cash Advance Is (and Why It’s Different From a Purchase)

A cash advance is short-term cash you borrow against your credit card. Instead of swiping at a store, you take dollars out of the credit line itself. You can get this cash from an ATM, a bank teller, or a convenience check the card issuer mailed you.

Now here’s why it’s not like a normal purchase. Three things change at once.

First, there’s a cash advance fee added the moment the money leaves the ATM. It’s a percentage of what you take out.

Second, the cash advance APR is higher than your normal purchase APR. Often much higher.

Third, there’s no grace period. With a regular purchase, you can pay off the statement by the due date and owe zero interest. Capital One confirms in its cash advance help center that interest begins to add up the same day you take the cash. Paying it back fast helps, but it never costs zero.

Your credit card agreement spells all of this out in the Schumer box on the first page. If you ever want to double-check your exact rate, that’s where to look.

How to Withdraw Cash With Your Capital One Card at an ATM

The process itself is simple. The hard part is having a PIN ready. To complete a Capital One cash advance at ATMs, follow these steps:

- Find an ATM. Any machine with the Visa or Mastercard logo will accept your card. A Capital One-branded ATM is fine. So is a bank ATM, a CVS ATM, or one in a gas station.

- Insert your card. Or tap if the ATM supports contactless.

- Enter your Capital One credit card PIN. This is not the same PIN you may use for a debit card. Without it, you can’t complete the transaction.

- Select “Credit” or “Cash Advance” from the on-screen menu. Do not pick “Checking” or “Savings.” Your credit card isn’t tied to those.

- Pick the amount. Stay inside your cash advance limit, which is usually lower than your full credit line.

- Accept any operator fee. The screen will show the ATM’s own surcharge before you confirm. If it looks too high, cancel and try a different machine.

- Take the cash, the card, and the receipt. Keep the receipt. You’ll want it to match your statement.

That’s the whole flow. Now the part that trips most people up is the PIN.

Setting Up or Retrieving Your Cash Advance PIN

If you’ve never set up a PIN, your card won’t pull cash, no matter how nice the ATM looks. Capital One does not auto-mail a PIN with a new credit card. You have to ask for one.

Below are the two fastest ways to get one:

- Online: Sign in at capitalone.com or open the Capital One mobile app. Go to your card, then select “I Want To,” then “Get a Cash Advance PIN.” Capital One’s PIN help page walks through the screens. Some cardholders can view or set a PIN instantly. Others will have one mailed in about 7 to 10 business days.

- By phone: Call the number on the back of your card. A rep can verify you and set or reset the PIN. Mail delivery still applies for some accounts.

What if you’re standing at the ATM right now with no PIN? You won’t be able to do the cash advance tonight. Two options are still open. You can visit a bank branch that accepts Visa or Mastercard for over-the-counter cash advances and show photo ID. Or you can switch to a cheaper option from the alternatives section below.

💡 Pro Tip: Set up your cash advance PIN the day you activate the card, even if you never plan to use it. Future-you in an emergency will thank you.

Using a Capital One Card at an International ATM

Capital One does not charge foreign transaction fees on its credit cards. That’s a real advantage when you travel. But cash advance fees still apply. So does the cash advance APR.

The local ATM operator may also tack on its own fee in the local currency. The ATM’s conversion screen might offer “dynamic currency conversion.” Decline it. Always choose to be charged in the local currency. The Visa or Mastercard exchange rate is almost always better than the rate the local machine offers.

Capital One Cash Advance Fees and Interest Costs

This is the part most articles gloss over. Real numbers matter when you’re deciding whether to pull $200 or find another way.

Capital One’s standard cash advance fee is either $5 or 5% of the amount you withdraw, whichever is higher. On a $40 ATM trip, that’s still $5. On a $400 trip, it’s $20.

The cash advance APR sits well above the regular purchase rate. Most Capital One consumer credit cards list a cash advance APR in the range of about 28.49% to 29.99% variable, depending on the card and your credit profile. Check the rate card mailed with your account or the agreement in your online profile for the exact number.

Why There’s No Grace Period on a Cash Advance

A grace period is the gap between your purchase date and your statement due date. During that time, regular purchases don’t accrue interest if you pay in full.

Cash advances skip that gift. Interest accrual starts the day the cash leaves the machine. Even if you pay your bill in full on the due date, you’ll still owe interest for the days the money was out.

📌 Did You Know: Card issuers also apply your monthly payment to the lower-APR balance first, by federal rule, unless you pay more than the minimum. That means cash advance balances can sit on your account, racking up interest, while your payment chips at purchases. The Consumer Financial Protection Bureau outlines this payment allocation rule under the CARD Act.

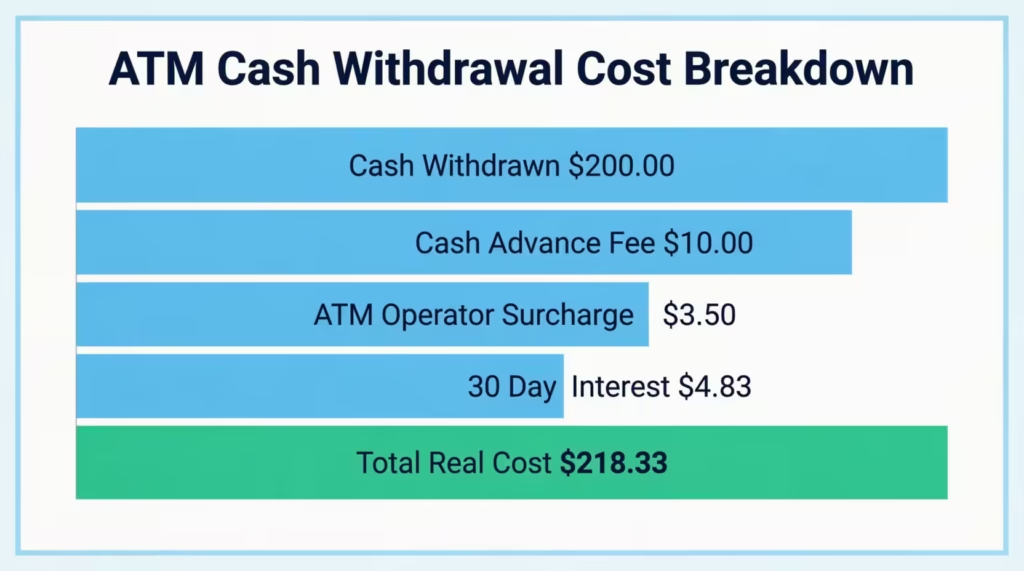

Real-Cost Example: What a $200 ATM Withdrawal Actually Costs

Let’s walk through one realistic withdrawal. Numbers below assume an out-of-network ATM and one billing cycle of carrying the balance.

| Cost Piece | Amount |

|---|---|

| Cash withdrawn | $200.00 |

| Capital One cash advance fee (5% or $5, whichever is greater) | $10.00 |

| ATM operator surcharge (typical range $2 to $5) | $3.50 |

| Cash advance APR interest for 30 days at 28.99% | about $4.83 |

| Total real cost to access $200 in cash | about $218.33 |

So that $200 actually costs you around $218.33 if you pay it off after one cycle. The longer you carry it, the worse the math gets. At 60 days, you’d owe roughly another $4.83 in interest. At 90 days, more again.

That extra $18 is the true price of convenience. It’s not crushing, but it’s also not free. And it stacks fast if you do it more than once.

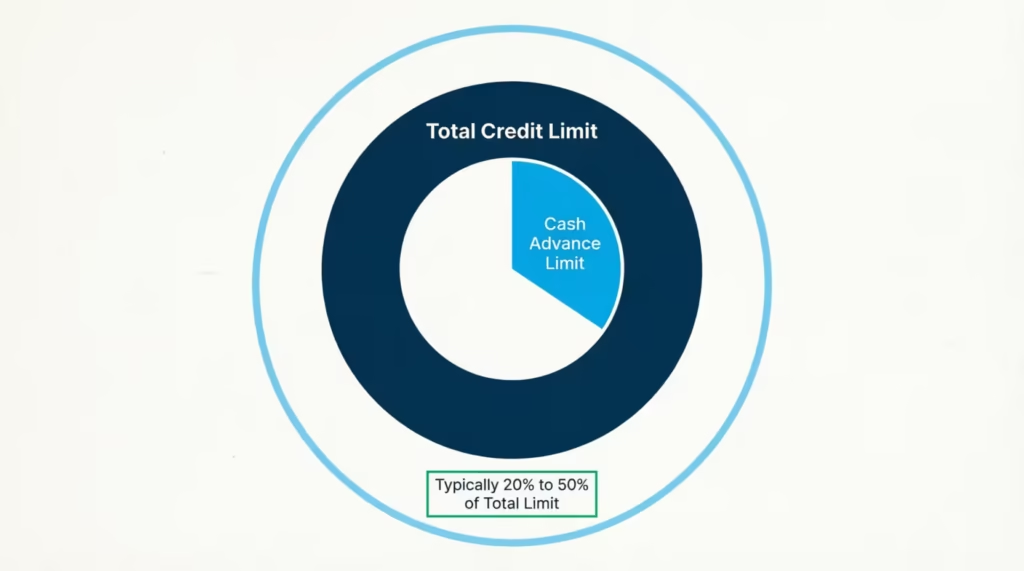

Cash Advance Limit vs. Total Credit Limit

Your credit limit is the full amount you can spend on the card. Your cash advance limit is a smaller pool inside that limit. It’s usually 20% to 50% of the total.

Why does this matter? Because if your card has a $5,000 credit limit, you may only be able to pull about $1,000 to $2,000 as cash. The ATM won’t tell you why if you go over. It will just decline.

To find your exact cash advance limit:

- In the Capital One mobile app: Tap your card, then “Account & Feature Settings,” then look under “Available Credit.” Your cash advance line is listed separately from your purchase limit.

- On capitalone.com: Sign in, click on the card, and open “Account Services” or “Card Details.” The cash advance limit shows alongside total credit and available credit.

- On your paper statement: It’s listed near the top, next to your total credit line.

If you’ve used cash advances before, the available cash credit will be lower than the listed limit. Recent purchases also reduce what’s available.

How to Avoid Extra ATM Operator Fees

Here’s a piece of fine print most blogs miss. Capital One has a fee-free ATM network for its checking account customers using a debit card. That network includes Capital One ATMs, the Allpoint network, and the MoneyPass network, with over 70,000 machines combined.

But that network only waives fees on debit card withdrawals tied to a Capital One bank account. For credit card cash advances, the ATM operator is free to charge their own surcharge, no matter which network you use. So the $2 to $5 ATM operator fee is hard to dodge completely.

Still, you can keep that fee small or skip it:

- Use a Capital One-branded ATM if one is nearby. Surcharges here are usually $0, even for a credit card cash advance.

- Pick a bank ATM tied to a major bank. Their machines often charge less than freestanding ATMs in convenience stores. Out-of-network ATM fees inside gas stations and bars are the highest.

- Withdraw one larger amount instead of two smaller ones. Two trips mean two operator fees and two Capital One cash advance fees. One bigger trip costs less in total.

- Check the screen before you confirm. Every ATM is legally required to show its surcharge before the transaction completes. If it feels too high, hit cancel and walk away. You won’t be charged.

⚠️ Mistake to Avoid: Splitting a $400 need into two $200 withdrawals. You pay the $5/5% Capital One fee twice and the ATM surcharge twice. That can double your cost for the same cash.

Other Transactions Capital One Treats as Cash Advances

ATM withdrawals aren’t the only thing that triggers the same fee structure. Capital One classifies several other moves as a cash advance, even if you didn’t think of them that way.

These include:

- Bank teller cash withdrawals using your credit card and ID.

- Convenience checks that the issuer may mail you.

- Wire transfers funded by your credit card.

- Money orders purchased with the card.

- Casino chips, betting, and lottery tickets.

- Cryptocurrency purchases on most exchanges.

- Some third-party bill pay apps that route a credit card payment as cash, including certain transfers on Venmo and PayPal when funded directly by a credit card.

Each of these gets the same cash advance fee, the same higher APR, and the same lack of a grace period. So if you’ve ever loaded a Venmo balance with your Capital One card, you may have already paid the fee without realizing it.

Does a Cash Advance Affect Your Credit Score?

A cash advance doesn’t show up as its own line on your credit report. The three bureaus see one balance on your card, not “this was a purchase” or “this was cash.”

But the balance still counts toward your credit utilization ratio. That ratio is the percentage of your total credit limit you’re using, and it’s a major factor in your FICO score.

So pulling $1,000 in cash on a card with a $2,000 limit pushes utilization to 50%. Even if you pay it off the next month, the balance reported on the statement date is what the bureaus see. High utilization can ding your score for a cycle or two until it’s paid down.

The act of taking the advance doesn’t lower your score. The high balance might. Pay it down before the statement closes if you can.

When a Cash Advance Makes Sense, And When to Avoid One

Cash advances get a bad reputation, and most of it is deserved. The fee, the cash advance APR, plus the lack of a grace period, stack up fast. But there are narrow cases where it really is the right move.

A cash advance can make sense when:

- You need physical cash right now, you’re far from a bank, and the alternative is missing a flight, missing rent, or paying late.

- The fee is smaller than the cost of the problem. A $15 cash advance fee beats a $200 service call cancellation.

- You can pay the balance back within a few days, keeping interest charges tiny.

Skip the cash advance when:

- You’d be carrying the balance for weeks or months. The 28% plus APR compounds.

- Your cash advance limit is already close to maxed. Adding to it spikes credit utilization.

- You have a debit card or P2P app available with the same cash in 30 seconds.

- You’re using it to pay off another credit card. That move shifts debt to a higher-rate balance.

The rule of thumb is simple. Cash advances are an emergency tool, not a regular cash source. Used once, paid off fast, they’re an expensive but workable option. Used often, they’re one of the most costly ways to borrow money short of a payday loan.

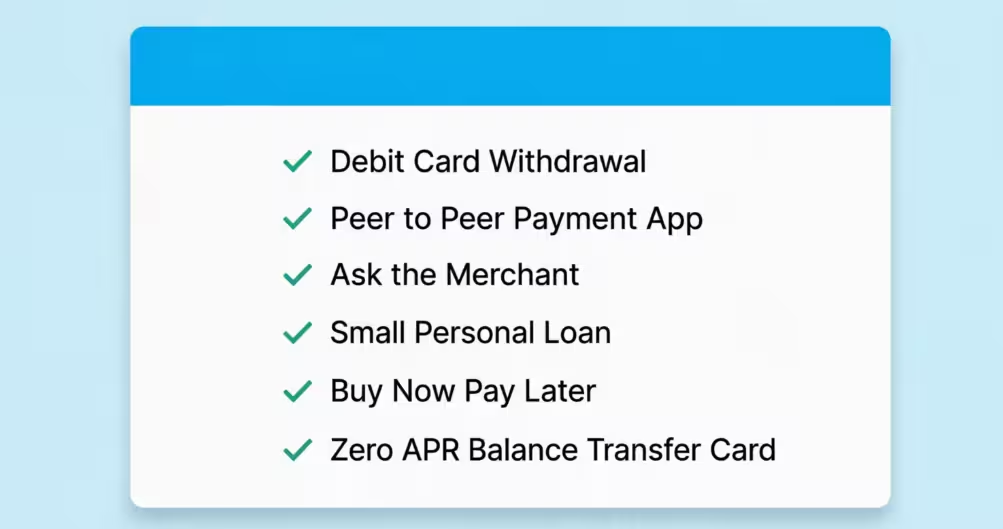

Alternatives to a Capital One Cash Advance

Before tapping the ATM screen, check these cheaper options. Often, one of them solves the same problem for far less money.

1. A debit card from your checking account.

No fee on most debit withdrawals at your bank’s ATM. No interest, because it’s your own money. This is the first thing to try if you have a bank account at all.

2. Peer-to-peer payment apps funded by a bank account.

Venmo, Cash App, Zelle, and PayPal can send cash to a person in seconds. If the recipient has the same app, they can withdraw the money themselves later. Just be sure you fund the transfer with a linked bank account, not a credit card, or Capital One will treat it as a cash advance.

3. Asking the merchant if they accept cards.

Many contractors, landlords, and small vendors say “cash only” by habit, but accept Zelle, Venmo, or even a card on request. A 30-second ask can save the entire fee.

4. A small personal loan.

For larger needs, say $1,000 or more, a personal loan from a bank or credit union usually carries a rate around 8% to 15%, far below the cash advance APR. Approval takes a day or two, so this isn’t great for tonight, but it’s worth knowing about for planned expenses.

5. Buy Now, Pay Later or split-pay services.

Some retailers let you split a charge into four interest-free payments. For one-time purchases, this beats a cash advance hands down.

6. A 0% APR balance transfer or purchase card.

If your need is to free up cash flow rather than get physical bills, opening a 0% intro APR card can shift the cost without any interest for 12 to 18 months. Capital One and other issuers offer these. They take a week or more to arrive, so they’re a planning tool, not an emergency one.

For Sarah, an operations manager at a Boston consulting firm who needed $400 to pay her mover in cash, the cheapest answer wasn’t an ATM at all. She paid the mover $400 by Zelle from her checking app. Cost: $0. The same $400 as a cash advance would have run about $25 to $35 once fees and one month of interest were added in.

The point is to think for two minutes before pulling the trigger on a cash advance. The cheaper path is often hiding in your other apps.

Frequently Asked Questions (FAQs)

Can I use my Capital One credit card at an ATM?

Yes, most ATMs that accept Visa or Mastercard will take your Capital One credit card. The withdrawal counts as a cash advance, which carries a fee and starts accruing interest immediately.

Why can’t I withdraw money from my Capital One credit card?

The most common reason is a missing PIN, since Capital One doesn’t automatically mail one with a new card. You could also be over your cash advance limit, which is typically only 20% to 50% of your total credit line.

How do I get a PIN for my Capital One credit card?

Sign in to the Capital One app or website, go to your card, then select “I Want To” followed by “Get a Cash Advance PIN.” Some accounts get instant access while others wait 7 to 10 business days for a mailed PIN.

What happens if I withdraw cash with my Capital One credit card?

You’ll pay a cash advance fee of $5 or 5% of the amount, whichever is higher, plus a cash advance APR of around 28.49% to 29.99% that starts charging interest the same day. There’s no grace period like with regular purchases.

How much can I withdraw from my Capital One credit card per day?

Your daily withdrawal is capped by your cash advance limit, not your full credit line. On a $5,000 credit limit, that cash advance limit is often only $1,000 to $2,000.

Which ATMs can I use my Capital One credit card at?

Any ATM displaying the Visa or Mastercard logo will accept it, including Capital One-branded machines, bank ATMs, and ATMs at stores like CVS or gas stations. Capital One-branded ATMs usually skip the operator surcharge even for cash advances.

Can I withdraw money from my Capital One credit card without the physical card?

No, a standard ATM cash advance requires the physical card and PIN to complete the transaction. If you don’t have the card, a bank teller cash advance with photo ID is the only listed alternative.

Does a Capital One cash advance hurt your credit score?

The cash advance itself doesn’t appear separately on your credit report, but the balance counts toward your credit utilization ratio. Pulling $1,000 on a $2,000 limit pushes utilization to 50%, which can lower your score until it’s paid down.

What’s a cheaper alternative to a Capital One cash advance?

A debit card withdrawal from your own bank account has no fee and no interest since it’s your own money. Peer-to-peer apps like Zelle or Venmo, funded by a bank account rather than a credit card, also move cash for free.

Bottom Line

A Capital One credit card can get you cash at almost any ATM, but the trip costs more than most people expect. A 5% or $5 fee, a higher APR with no grace period, and a possible operator surcharge can turn a $200 withdrawal into about $218 or more.

Based on the cost math above, the most effective approach for most readers is to treat a credit card cash advance as a true emergency tool, not a routine one. Use a debit card, a P2P app, or a quick ask to the merchant first. Save the cash advance for the moment when nothing else will work, and pay it back as fast as you can.

If you know someone who travels often or runs into cash-only situations, share this guide with them. It could save them $20 to $50 the next time they’re stuck near an ATM with only a credit card.