Spotting a charge on your Capital One statement that you didn’t make, didn’t approve, or didn’t receive can feel stressful. The clock starts ticking the moment that charge posts, and many cardholders worry they’ll lose their money if they pick the wrong path or wait too long. If you’ve been searching for a clear way to dispute a charge with Capital One, you’re not alone, and the process is more time-sensitive than most people think.

The short answer: file your claim within 60 days of the statement date through the Capital One app, online account, phone, or certified mail, and back it up with strong evidence.

Below, we’ll walk you through every step, from spotting the right type of claim to escalating a denial, so you can act fast and protect your money.

At a Glance

This guide explains how to dispute a Capital One credit card charge, covering the difference between fraud and dispute claims, the 60-day federal filing deadline, required documentation, available filing methods, and steps to take if Capital One denies your claim.

Core Facts:

- Capital One handles two separate claim types: fraud claims (unauthorized charges you never approved) close your card and trigger an investigation, while dispute claims (merchant errors, non-delivery, wrong amounts) keep your card open and involve the merchant directly.

- The federal filing deadline under the Fair Credit Billing Act is 60 days from the statement date the charge appeared, not the date you noticed it.

- Filing methods include the Capital One mobile app, the website at capitalone.com, phone at 1-800-227-4825 (staffed 24/7), or certified mail with return receipt.

- Capital One must acknowledge your claim within 30 days of receiving it and resolve the dispute within two billing cycles, with a maximum of 90 days from the filing date.

- A provisional credit may be placed in your account during the investigation, but it can be reversed if the decision favors the merchant.

- If Capital One denies your dispute, escalation options include a written appeal, a complaint with the CFPB at consumerfinance.gov/complaint, a Better Business Bureau complaint, or small claims court for eligible amounts.

Best for:

- Cardholders who spotted an unfamiliar, duplicate, or incorrect charge on a Capital One statement and are unsure whether to file a fraud claim or a standard dispute.

- Anyone who contacted the merchant without resolution and is ready to escalate to Capital One with documented evidence.

- People whose Capital One dispute was denied and who need a clear path to appeal or escalate through federal consumer protection channels.

What Qualifies as a Disputable Charge on Your Capital One Card

Not every charge you dislike is one you can fight. Capital One follows federal billing rules, which means only certain types of charges qualify for a formal claim. Knowing the difference saves you time and keeps you from filing a claim that gets shut down right away.

A charge usually qualifies as a billing error or unauthorized charge if it falls into one of these groups:

- Unauthorized use: someone used your card or card number without your permission.

- Billing errors: you were charged the wrong amount, charged twice, or charged for something you returned.

- Goods or services problems: the item never arrived, arrived broken, or was not what the merchant promised.

- Math or posting mistakes: the math is wrong, a payment isn’t showing, or a credit is missing.

- Missing paperwork: You asked the merchant for proof of the charge and never got it.

A pending charge is trickier. Pending means the transaction has not fully posted yet. Capital One typically asks you to wait until the charge posts before filing a formal claim, because pending amounts can still drop off, change, or be canceled by the merchant. If a pending charge looks fake or you don’t know the merchant, call Capital One right away so they can flag the account.

What does not qualify:

- Buyer’s remorse: you changed your mind after buying.

- Family or friend use: someone you gave the card to used it in a way you didn’t like.

- Service fees you agreed to: annual fees, late fees, or interest you accepted in the cardholder terms.

💡 Pro Tip: Before you file, screenshot the charge from your account and note the exact post date. Capital One’s clock runs from the statement date, not the day you noticed the charge, so quick records protect your timeline.

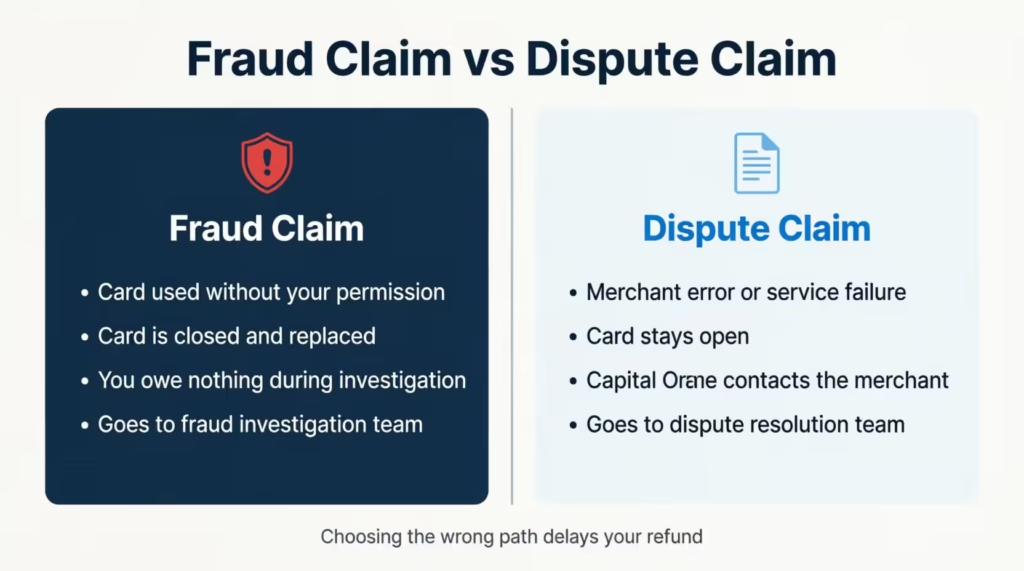

Fraud Claim vs. Dispute Claim: Which Path Applies to You

These two paths look similar, but they go to different teams inside Capital One, and picking the wrong one can slow down your refund.

A fraud claim is for charges you did not make and did not allow anyone else to make. Think of a stolen card, a leaked card number, or a charge from a country you’ve never visited. Capital One will close your card, send a new one, and start a fraud investigation. You are not responsible for paying these charges while they look into it.

A dispute claim is for charges you did make, or that a merchant you trusted made, but something went wrong. Maybe the item never showed up, the service was not as promised, or you were charged twice. Your card stays open, and Capital One contacts the merchant on your behalf.

Picking the right path matters. If you file a fraud claim for what is really a dispute, Capital One will close your card for no reason. If you file a dispute when it is really fraud, the thief may keep using your number.

Know Your Deadline Before You Do Anything Else

Time is the most important part of this whole process. Under the Fair Credit Billing Act (FCBA), you have 60 days from the date the statement with the charge was mailed or made available to file a written billing error claim. Miss that window, and you lose your federal protection.

A few things to know about the 60-day deadline:

- The clock starts on the statement date, not the day you noticed the charge.

- For paperless accounts, it starts the day Capital One posts your e-statement.

- For fraud, Capital One often allows claims past 60 days, but you should still report it as soon as you spot it.

- For non-delivery, the clock can shift to start when the goods were supposed to arrive, not when you paid.

If you are close to the cutoff, file the claim now and add documents later. A late, complete file is worse than an early, light one. Once you are inside the 60-day window, Capital One must follow strict federal rules about how they handle your claim. This is laid out in the Consumer Financial Protection Bureau’s billing error guidance, which explains how the FCBA protects cardholders.

For longer disputes, like a service that was never finished or goods that arrived weeks later, the 60-day rule can feel tight. In those cases, file your claim the moment the problem is clear, even if you are still hoping the merchant will fix it.

What to Do Before You File Your Dispute

Filing too fast can hurt your case. Capital One often asks if you tried to fix the issue with the merchant first, and many disputes are denied just because that step was skipped.

Here’s what to do before you submit anything:

- Wait for the charge to post. Pending charges can change or drop off on their own. A posted transaction has a clear date, amount, and merchant name you can point to.

- Contact the merchant first. Call, email, or message them. Ask for a refund, a replacement, or a written reason for the charge. Keep notes with the date, time, name of the rep, and what they said.

- Give the merchant a fair window. Most merchants need 7 to 14 days to respond. If they refuse, ignore you, or promise a refund that never comes, you’ve earned the right to escalate.

- Check your card terms. Some perks, like purchase protection or extended warranty, may cover your problem faster than a dispute.

- Confirm the merchant name on your statement. A charge from “SP* JANES BAKERY” may be a real bakery you paid for using a payment processor. A quick search can save you from filing a claim against a real business.

Skipping the merchant step is the most common reason a dispute fails. Capital One needs to see that you tried to fix it the easy way first.

Documentation to Gather Before You Submit

Before you click submit or pick up the phone, gather everything in one folder, digital or paper. Capital One’s investigators move fast, and a complete file beats a messy one.

Gather these items:

- The exact transaction details: date, amount, merchant name, and the last four digits of the card used.

- Receipts and order confirmations: from email, the merchant’s app, or your account.

- Proof you contacted the merchant: emails, chat logs, screenshots, and call notes with dates.

- Shipping or tracking records: if the item never arrived or was returned.

- Photos: of damaged, wrong, or counterfeit items.

- A short written summary: 3 to 5 sentences explaining what happened, what you want fixed, and what the merchant said.

Save copies of everything for yourself. If your dispute is denied, you’ll need this same file to appeal or escalate.

How to Dispute a Capital One Charge Online or Through the App

For most cardholders, the fastest path is digital. Capital One built the dispute flow right into the app and the website, and it usually takes less than ten minutes.

To file through the Capital One website:

- Sign in at capitalone.com.

- Open the account with a charge.

- Find the transaction in your recent activity.

- Click the charge, then choose “Report a problem” or “Dispute this transaction.”

- Pick the reason that matches your case: not received, wrong amount, duplicate, canceled service, and so on.

- Add your written summary and upload any proof.

- Submit and save the confirmation number.

To file through the Capital One mobile app:

- Open the app and sign in.

- Tap the card account.

- Scroll to the transaction.

- Tap it, then choose “Report a problem with this transaction.”

- Walk through the same prompts as on the website.

The app saves your spot if you need to come back. You can upload photos straight from your phone, which is helpful for damaged goods or shipping labels.

After you submit, watch your email and your secure message center. Capital One often asks follow-up questions, and a slow reply can stall your case.

How to Dispute a Capital One Charge by Phone

If your charge is older than 90 days, hard to explain in a form, or tied to a closed account, calling is often smarter. Phone calls also help when you are racing the 60-day clock.

Call the number on the back of your card, or use Capital One’s customer service line at 1-800-227-4825, which is staffed 24/7. Tell the agent you want to dispute a transaction. Be ready to share:

- The transaction date, amount, and merchant.

- The reason for the dispute.

- What you’ve already tried with the merchant.

- A short, clear summary of what you want.

Ask for a case number before you hang up. Write down the agent’s name, the time, and what they said you should do next. If you are told to send paperwork, ask for the exact address and what to label the envelope.

How to Dispute a Capital One Charge by Mail

A written letter is your strongest move under federal billing rules. It creates a paper trail, locks in your filing date, and is the official method named in the FCBA.

Send your letter to the billing inquiries address listed on the back of your statement. Use certified mail with a return receipt so you can prove the date Capital One got your claim.

Your letter should include:

- Your full name, address, and account number.

- The transaction date, amount, and merchant name.

- A short, clear reason for the dispute.

- Copies (never originals) of supporting papers.

- A request for a written response and provisional credit if it applies.

Mail the letter so it reaches Capital One within 60 days of the statement date. Keep your certified mail receipt and a copy of the full packet. If you ever escalate to a regulator, this paperwork is gold.

What Documentation Strengthens Your Dispute

Strong evidence does the heavy lifting in any claim. A clear file can turn a 50/50 case into a clear win. A weak file can sink even an obvious one.

Different problems call for different proof:

For merchant disputes (wrong item, wrong amount, canceled service):

- The original receipt or order confirmation.

- A copy of the merchant’s refund or return policy.

- Emails or chats showing the merchant agreed to refund or cancel.

- Screenshots of any account or subscription page showing the cancel date.

For non-delivery claims:

- The tracking number and the carrier’s “no delivery” notes.

- Any message from the merchant about shipping delays.

- A photo of an empty package, if it arrived empty.

- A copy of the address the merchant shipped to, if it was wrong.

For quality or “not as described” claims:

- Clear photos of the item next to the listing or ad.

- The product description from the merchant’s site at the time of sale.

- A repair estimate, if one applies.

- A written statement from a third party, like a mechanic or technician.

Label every file with the date and a short note, like “2026-05-12_email_from_seller.pdf.” A clean stack of chargeback evidence makes the investigator’s job easy, and that usually helps you.

⚠️ Mistake to Avoid: Don’t send long, emotional letters. Investigators skim. A short summary plus dated, labeled proof beats a five-page story every time.

What Happens After You File Your Capital One Dispute

Once your claim is in, Capital One has set steps to follow. Knowing what to expect keeps you calm and ready to respond if they ask for more.

Here is the general flow of a Capital One dispute investigation:

- You get an acknowledgment. Capital One must let you know they got your claim, usually within 30 days.

- The charge is flagged. While they look into it, the disputed amount is set aside, and interest on that amount is paused.

- Capital One contacts the merchant. The merchant gets a chance to respond with their own proof.

- You may get follow-up questions. Watch your messages and reply fast. A missed reply can close your case.

- A decision is made. Capital One either sides with you, sides with the merchant, or splits the result.

During the investigation, you do not have to pay the disputed amount or any interest tied to it. You still have to pay the rest of your bill on time. Skipping the full payment can hurt your credit and give the merchant a reason to push back.

Understanding Your Provisional Credit

A provisional credit is a temporary refund. Capital One puts the disputed amount back into your account while they look into your claim, so you are not out the money during the wait.

It is not a final win. Keep these points in mind:

- The credit can be reversed if the investigation sides with the merchant.

- The credit usually shows up within 1 to 2 statement cycles.

- It may show as a separate line item, not a refund from the merchant.

- Don’t spend the credit if your case is shaky. If it gets reversed, your balance jumps back up.

Treat a provisional credit like a held bond. It’s yours for now, but it can move either way once the case closes.

How Long Does Capital One Take to Resolve a Dispute

Under federal rules, Capital One must follow these timelines:

- Acknowledge your claim within 30 days of getting it.

- Resolve the dispute within two billing cycles, and no more than 90 days from the day you filed.

In real life, simple cases close in 30 to 45 days. Complex cases, like international charges, large amounts, or service disputes, can use the full 90 days. If your case crosses the 90-day mark with no answer, call Capital One and ask for an update in writing.

📌 Did You Know: While your dispute is open, the merchant cannot send your account to collections for that exact amount, and Capital One cannot report it as late. This is a strong federal protection most cardholders never use.

What to Do If Capital One Denies Your Dispute

A denial is not the end. Capital One must send you a written explanation that says why they sided with the merchant, what proof they relied on, and what you can do next.

Read the letter carefully. Look for:

- The exact reason for the denial.

- What proof did the merchant send

- Any deadline to send new evidence

- The case number, which you’ll need for any appeal.

Common reasons for denial include:

- The merchant showed proof of delivery or service.

- You filed past the 60-day window.

- You did not try the merchant first.

- The reason you picked did not match the facts.

If the denial is based on missing proof, you can usually reopen the case by sending the new documents within a set window, often 10 to 30 days. Be specific. Address each point in the denial letter, one by one.

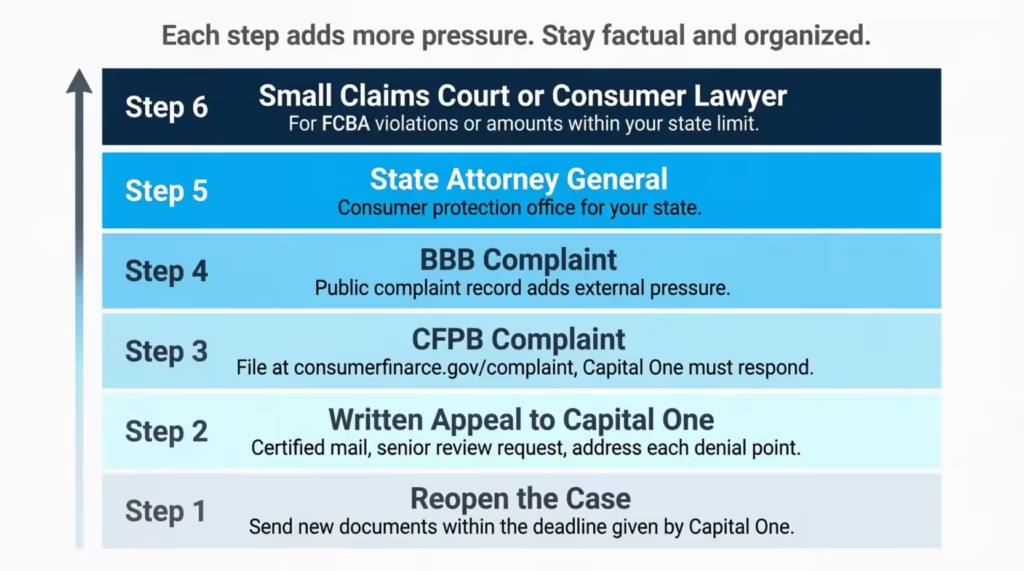

How to Escalate After a Denial

If reopening the case does not work, you still have options. Each step takes more time, but each one adds more pressure on the bank.

1. Send a final written appeal to Capital One.

Mail a clear letter, certified, that lists each point in the denial and your fresh proof for each one. Ask for a senior review.

2. File a complaint with the Consumer Financial Protection Bureau (CFPB).

The CFPB is a federal agency that handles consumer finance complaints. You can file at consumerfinance.gov/complaint. Capital One must respond, usually within 15 days, and the CFPB tracks the case.

3. File a complaint with the Better Business Bureau (BBB).

BBB complaints are public and can pressure the bank to take a second look. Be factual, not emotional, and attach your file.

4. Contact your state attorney general’s consumer protection office.

Each state has one. They handle bank and merchant complaints and can sometimes step in.

5. Take the merchant or the bank to small claims court.

For amounts under your state’s limit, usually $5,000 to $10,000, small claims is fast and does not need a lawyer. Bring your full file and your timeline.

6. Ask a consumer lawyer about FCBA violations.

If Capital One missed a federal step, like the 30-day acknowledgement or the 90-day resolution rule, you may have a separate legal claim. Many consumer lawyers offer free first meetings.

Escalation works best when you stay calm, stick to the facts, and keep every paper trail. The more organized your file, the harder it is for any party to brush you off.

Frequently Asked Questions (FAQs)

Can I dispute a charge that I willingly paid for?

Not usually. Buyer’s remorse, gifts made to family or friends, and fees you agreed to in your cardholder terms all fall outside Capital One’s disputable charge categories. A charge only qualifies if there was a billing error, an unauthorized use, or a failure to deliver goods or services as promised.

How late is too late to dispute a Capital One charge?

The federal deadline under the Fair Credit Billing Act is 60 days from the statement date the charge appeared on, not the date you noticed it. Filing even one day past that window forfeits your federal protection, though Capital One may extend the window for confirmed fraud cases.

Do credit card disputes hurt your credit?

No. While a dispute is open, Capital One cannot report the contested amount as a late payment, and the account itself stays open in most dispute cases. Your credit score is not affected by the act of filing a dispute.

Will Capital One refund me if I get scammed?

Yes, if the charge was made without your permission, Capital One treats it as a fraud claim, not a standard dispute. You are not responsible for unauthorized charges while the investigation is open, and the bank will close your compromised card and issue a new one.

How do you win a credit card dispute with Capital One?

The strongest cases combine an early filing, a documented attempt to resolve the issue with the merchant first, and clearly labeled evidence such as receipts, shipping records, and written communication. Investigators skim files, so a summary with dated proof outperforms long explanations every time.

Is it easy to dispute a Capital One credit card charge?

The process itself is straightforward through the Capital One app or website and typically takes under ten minutes to file. What determines success is acting within the 60-day window and submitting solid documentation, not the complexity of the filing steps.

What is a provisional credit from Capital One, and will I keep it?

A provisional credit is a temporary refund Capital One places in your account while the dispute investigation is ongoing, usually appearing within one to two statement cycles. It is not a final decision and can be reversed if the investigation ultimately sides with the merchant.

What number is 800-227-4825?

That is Capital One’s main customer service number for credit card disputes and general account questions. It is staffed around the clock, every day of the week.

Does Capital One have 24/7 customer service?

Yes. Capital One’s dispute and account service line at 1-800-227-4825 is available 24 hours a day, seven days a week. Calling is recommended when a dispute is complex, time-sensitive, or tied to a closed account.

Bottom Line

Disputing a wrong, unauthorized, or bad transaction with Capital One comes down to three things: act inside the 60-day window, pick the right path between fraud and dispute, and back your claim with clean, dated proof. From your first call to the merchant, through the app or mailed letter, all the way to a CFPB complaint if needed, each step builds on the last.

Based on the federal protections in the FCBA, the most effective approach is to file early, in writing, with a clear summary and labeled evidence.

If you know a friend or family member juggling a wrong charge right now, share this guide. It could save them weeks of stress and real money.