I know the frustration. You’ve had your Capital One card for a while, you pay on time, and yet you still feel boxed in by a limit that’s too low for your real spending needs. Maybe a big purchase is coming up, or your credit utilization is creeping too high and pulling your score down. The good news? Getting a Capital One credit limit increase is often easier than people think, and it usually won’t hurt your credit score.

Here’s the short answer: log in, find the credit line increase option, submit accurate income and housing details, and ask for a realistic bump.

Below, I’ll walk you through every step, the rules Capital One uses, what to do if you’re denied, and how to time your request for the best shot at approval.

Key Takeaways

This guide explains how to request a Capital One credit limit increase through the website, mobile app, or phone, covering eligibility rules, the six-month waiting period, and how to respond if your request is denied.

Core Facts:

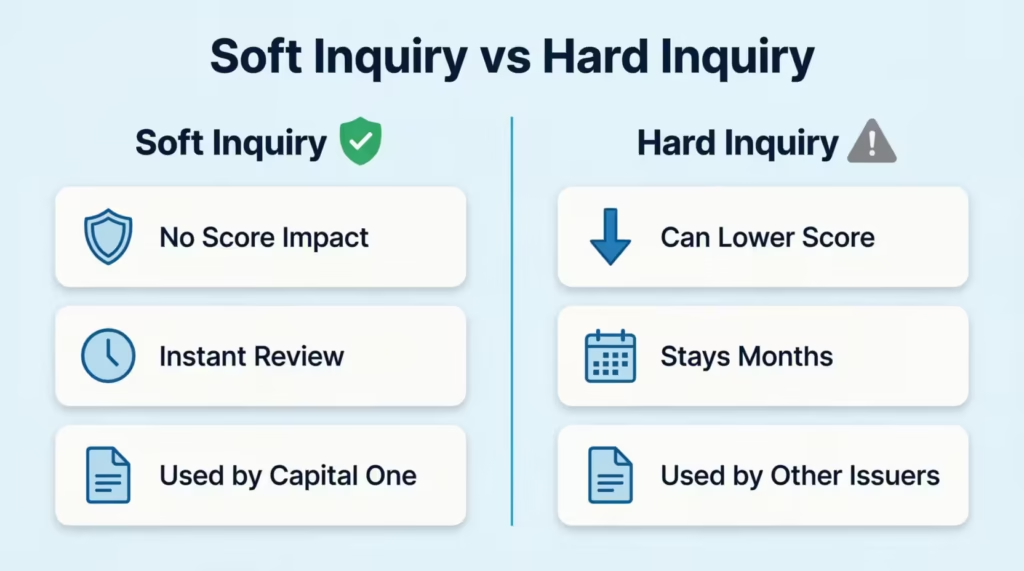

- Capital One uses a soft credit inquiry to review credit line increase requests, which does not impact your credit score, unlike hard inquiries used by some other issuers.

- Most manual requests receive a decision within seconds, though some require additional review that can take up to 30 days, with most resolved in two to three business days.

- Capital One generally recommends waiting at least six months between manual credit line increase requests on the same card, with the clock starting from the date of the last decision.

- Required information for a request includes total annual income, employment status, monthly housing payment, and desired credit limit.

- Secured cards do not use the standard increase request form since the limit is tied to the security deposit, though the deposit itself can be increased up to a set cap.

- The Consumer Financial Protection Bureau notes that keeping credit utilization under 30% shows lenders responsible credit management.

Best for:

- Current Capital One cardholders who want a higher credit limit and are unsure how to submit a request or what information is required.

- Cardholders who were previously denied an increase and want to understand common denial reasons before reapplying.

- Cardholders deciding between requesting a manual increase or waiting for an automatic credit line review.

How to Request a Capital One Credit Limit Increase

There are three ways to ask Capital One for more spending room: the website, the mobile app, and the phone. All three lead to the same review system, so pick whichever feels easiest. The key is knowing exactly where to click, because the option is buried inside a menu that many cardholders miss on their first try.

Before you start, log in from a quiet place where you can think clearly. You’ll be asked for personal financial details, and rushing through them can hurt your approval odds. Have your income figure ready, your monthly rent or mortgage payment, and the new limit you want in mind.

Requesting Online Through the Website

To request a credit line increase on the Capital One website, sign in to your account on a desktop or mobile browser. Once you’re in, look for the card you want to upgrade. Click on it to open the account dashboard.

From there, find the “I Want To” menu. This is the drop-down that holds most of your account tools. Inside it, you’ll see an option called “Request Credit Line Increase”. Click it to start the form.

The form is short. You’ll fill in your current income, employment status, monthly housing payment, and the new credit limit you want. Double-check your numbers before you submit. Once you click send, Capital One reviews the request right away in most cases.

Requesting Through the Capital One Mobile App

The Capital One Mobile app uses a slightly different path, but it’s just as fast. Open the app and tap the card you want to grow. This brings up the account screen for that specific card.

Scroll down and tap “Account & Feature Settings” or look for the option labeled “Request Credit Line Increase”. On some app versions, it sits inside an “Services” or “Account Services” group. If you can’t find it, use the search bar at the top of the app and type credit line increase. The app will pull up the right link.

The form on the app mirrors the website. Same fields, same review system. The app sometimes pre-fills your last reported income, but always update it if your earnings have changed.

Requesting by Phone

Some people prefer talking to a real person. You can call Capital One’s customer service line at 1-800-227-4825, which is printed on the back of every Capital One card. Ask the agent for a credit line increase request.

The agent will ask the same questions you’d answer in the form: income, housing cost, employment, and the limit you want. They submit the request on your behalf. This route works well if you have a special situation, like a recent raise or a denied request you want to discuss before reapplying.

How Long Does the Decision Take

Most requests get an answer within seconds. Capital One’s system reviews your account, your payment history, and your latest financial details right away. If you’re approved, the new limit usually shows up on your account the same day.

Some requests need a deeper look. These can take up to 30 days, though most are settled in two to three business days. If you don’t get an instant answer, Capital One will send a decision by mail or email. You don’t need to call to follow up unless 30 days have passed with no response.

💡 Pro Tip: Submit your request right after a paycheck hits your bank account. Your income field can include all household income you have reasonable access to, which often pushes your reported number higher than just your base salary.

Will Requesting a Credit Limit Increase Hurt Your Credit Score?

This is the number one worry, and the answer brings real relief. Capital One uses a soft credit inquiry to review credit line increase requests, not a hard pull. Soft inquiries do not show up on your credit report in a way that affects your score. As Capital One confirms on its help center, “Requesting a credit increase won’t impact your credit score because we use soft inquiries for credit limit increase requests.”

That makes Capital One different from some other card issuers, who run a hard inquiry that can drop your score by a few points for several months. With Capital One, you can ask freely without that worry.

There’s an indirect benefit, too. If your limit goes up and your spending stays the same, your credit utilization ratio drops. A lower ratio often lifts your FICO score over the next billing cycle. So a successful request can actually help your credit, not hurt it.

The only catch is if you’re approved and then run the new limit up. High balances on a higher line still hurt your score. The boost only helps if you keep your spending steady.

What Information You’ll Need to Provide

Capital One asks for a small set of details before reviewing your request. Having these ready makes the form take less than two minutes.

Below is what you’ll need:

- Total annual income. Include your salary, side income, freelance pay, and any household income you have reasonable access to. Be honest, but don’t underreport.

- Employment status. Full-time, part-time, self-employed, retired, student, or unemployed. Pick the one that fits best.

- Monthly housing payment. Your rent or mortgage. If you live with family and pay nothing, you can enter zero.

- Desired credit limit. The new total limit you want, not the amount of the increase. For example, if your limit is $2,000 and you want $1,000 more, type $3,000.

Capital One uses these numbers to judge your ability to handle a higher line. The income and housing fields together give the bank a sense of your free cash flow each month. The desired limit shows them what you’re aiming for, which helps them decide if your request is realistic.

Update your income before you ask. Many people leave their old starting salary in the system for years. A simple refresh can be the difference between approval and denial.

⚠️ Mistake to Avoid: Don’t inflate your income to boost your odds. Capital One can ask for proof, and false income on a credit application is fraud. Stick to numbers you can back up with pay stubs or tax returns.

Eligibility Requirements for a Capital One Credit Limit Increase

Not every cardholder can ask for a higher limit right away. Capital One has a few basic rules to make sure the request makes sense for both sides.

You must be the primary account holder. Authorized users cannot request increases. Only the person whose name and Social Security number are tied to the account can submit a request.

Your account should be open for at least a few months. Capital One wants to see how you handle the card before giving you more rope. Most users find that three to six months of activity is the sweet spot, though some can ask sooner.

Your recent payment record should be clean. Late payments, returned payments, or going over your current limit can all block an increase. Capital One looks at the last six months of activity most closely.

You also should not have asked for an increase in the last few months. As Capital One notes in its credit line increase FAQ, “if you’ve recently received an increase on the same card, we recommend waiting several months before applying again.” Most users wait six months between requests to be safe.

Other quiet rules apply too. Your account should not be frozen, under review, or in any kind of collections status. If you’ve had a recent change to your address or name that hasn’t been verified, finish that first.

Why Secured Cards Work Differently

Secured cards play by a different set of rules. If you have a Platinum Secured or Quicksilver Secured card from Capital One, your credit limit is tied directly to the security deposit you paid when you opened the account.

That means you can’t simply ask for a higher line through the normal form. The standard “I Want To” menu often won’t even show the request option for secured accounts. Instead, you can raise your limit by adding more money to your security deposit. Capital One lets secured cardholders boost their deposit up to a set cap, and the new deposit amount becomes the new credit limit.

There’s a second path, too. After several months of on-time payments, Capital One may offer to release your deposit and upgrade your secured card to an unsecured one. When that happens, you keep your same account and your credit history, but the bank now sets your limit based on your credit profile, not your deposit. From that point on, you can use the normal credit line increase request process.

If you’re not sure which card type you have, check the welcome materials or look at your account details online. Secured cards are clearly labeled.

How Automatic Credit Limit Increases Work

Capital One reviews many accounts on its own and offers higher limits without you asking. This is called an automatic credit line review, and it runs in the background based on how you use the card.

The system looks for steady, healthy use. That means making on-time payments, keeping balances reasonable, and using the card often enough to show a real pattern. After about six months of this kind of activity, your account may get flagged for a possible increase.

If the system likes what it sees, you’ll get a message in your online account, your app, your email, or by mail. The new limit may be applied right away, or you may need to click a button to accept it. There’s no form to fill out and no soft pull worry, since Capital One already has all the data it needs.

Not every cardholder gets an automatic bump. Secured cards rarely qualify for automatic increases in the same way unsecured cards do, and accounts with any negative marks usually get skipped. The bank’s system also pauses these reviews if you’ve had a recent manual increase.

Should You Request One or Wait for an Automatic Increase?

This depends on how soon you need the extra room. If you have a planned expense in the next month or two, a manual request makes sense. You’ll get an answer fast, and if approved, the limit jumps right away.

If you’re not in a hurry, waiting for an automatic review has perks. You skip the form, you avoid any risk of denial ding your record, and the bank often offers a bigger jump than you might have asked for yourself.

A smart middle path: keep using your card well for six months, then submit a manual request. If you’re already on track for an automatic review, your odds of approval on the manual request are very high. You essentially trigger the same review your card was heading toward anyway.

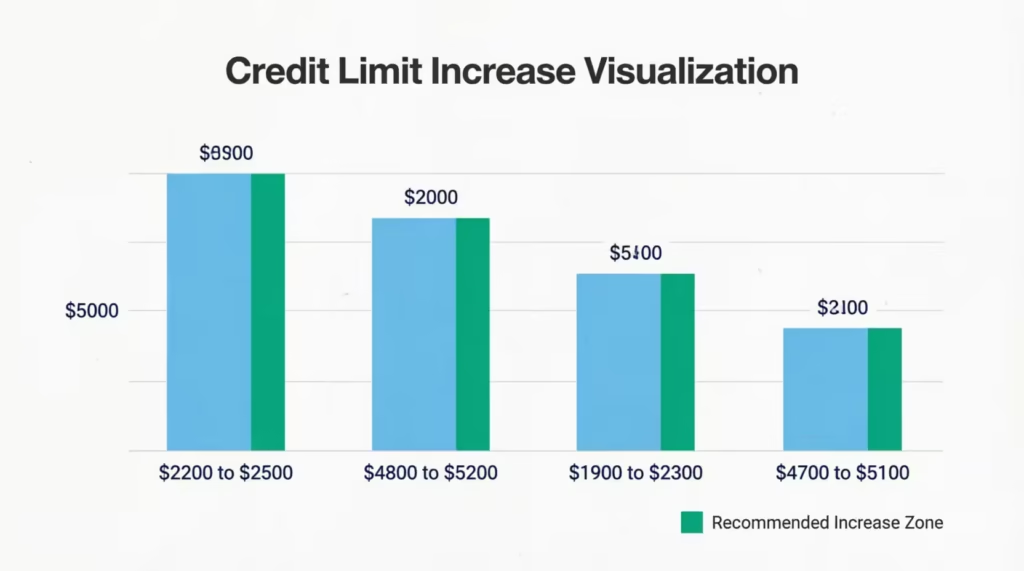

How Much of an Increase to Request

This is where many people slip up. They aim too high and get denied, or aim too low and waste the request. The sweet spot for most Capital One cardholders is an increase of 10% to 25% above their current limit.

So if your current limit is $2,000, ask for $2,200 to $2,500. If it’s $5,000, aim for $5,500 to $6,250. This range matches what Capital One’s review system tends to approve for users in good standing.

Why this range? Capital One looks at your spending pattern, your income, and your payment history. A small to mid-size jump fits the math the bank already trusts. Asking for double or triple your current limit often gets flagged as a risk, even if you could handle it.

A few cases let you ask for more. If your income has gone up by a large amount since you opened the card, you can push toward the upper end or even past it. If you’ve had the card for years and never had an increase, the system has more room to grow your line. And if your credit score has jumped 50 points or more, a bigger ask becomes more reasonable.

Round numbers work well, too. Asking for $3,000, $5,000, or $10,000 reads cleaner to the system than odd amounts like $2,847. Pick a target that fits the 10% to 25% rule, then round to the nearest hundred or thousand.

📌 Did You Know: Capital One sometimes approves a smaller increase than you asked for. If you request $5,000 and get $4,200, that’s still a win. You can keep the new limit and try for more in six months.

What Capital One Considers When Reviewing Your Request

The bank’s review system weighs several factors at once. Knowing them helps you time your request when your profile looks its best.

Payment history on the card. This is the biggest factor. Capital One wants to see at least six months of on-time payments with no missed dates, no returned payments, and no over-limit hits. One late payment in the last six months can sink your odds.

Current credit utilization. If you’re using a high share of your current limit each month, the system may worry that more credit will lead to more debt. Try to keep your utilization under 30% in the month before you ask. The Consumer Financial Protection Bureau notes that keeping a low credit utilization ratio under 30 percent shows lenders you’re responsible and have available credit.

Income compared to housing and debt. Capital One looks at how much free cash flow you have after rent and other bills. A higher income with steady housing costs gives more room for a bigger line.

Length of time the account has been open. Newer accounts get smaller bumps. Accounts open for a year or more tend to get larger.

Overall credit profile. The bank also checks your wider credit report through a soft pull. New accounts, recent hard inquiries from other lenders, and any negative marks can hold you back.

Account use pattern. Cards used regularly tend to grow faster. A card sitting in a drawer rarely gets a higher line, since the bank has no fresh data to judge.

What to Do If Your Request Is Denied

A denial stings, but it’s not the end of the road. Capital One sends a denial letter by email or mail within a few days that lists the main reasons. Read this letter carefully. It’s your road map to a successful next attempt.

Common reasons include short account history, recent late payments, high utilization, low reported income, or a recent increase that’s still in the cool-down window. Each one has a fix.

Start by checking your free CreditWise account, which Capital One offers to all cardholders. CreditWise shows your TransUnion credit report and a VantageScore based on TransUnion data. Look for anything that surprises you, like an old missed payment or an error in your account list. Dispute any mistakes through TransUnion.

Then work on the weak spot, the letter named. If utilization was too high, pay your balance down to below 30% of your limit. If income is an issue, update your reported income once it grows. If your account is too new, simply wait the right amount of time.

Pay your bill on time, every time, in the meantime. Set up auto-pay for at least the minimum, so a busy week never costs you a late mark. Use the card regularly, but keep your balance well below the limit.

How Often You Can Request an Increase

Capital One asks users to wait at least six months between manual requests on the same card. If you ask sooner, the system often turns you down without a real review.

The six-month clock starts on the date of your last decision, not the date you applied. So if you asked on January 10 and got an answer on January 12, your next eligible date is roughly July 12.

If your last request was approved, the same six-month rule applies before you ask again. Some users have luck stretching to nine or twelve months between requests, since longer waits give your file more time to show new positive activity.

You can still get an automatic increase during this six-month window. The wait only blocks new manual requests, not the bank’s own reviews.

Weighing the Tradeoffs of a Higher Credit Limit

A bigger credit line brings real perks, but it isn’t all upside. Think through both sides before you push for a major jump.

The wins:

- Your credit utilization ratio drops if your spending stays the same, which often lifts your score.

- You have more room for big purchases without maxing out the card.

- You earn more rewards if you put more spending on the card and pay it off each month.

- You build a stronger credit profile, which helps when you apply for loans, mortgages, or new cards later.

The risks:

- A higher limit can tempt you to spend more. If you do, your utilization climbs back up and your balance grows.

- Carrying a balance on a bigger line means more interest paid each month. Capital One’s standard APRs are not low.

- If you ever apply for a mortgage, lenders look at your total available credit. Very high limits across many cards can sometimes work against you, since they signal more borrowing power than the lender wants to see.

- A higher line means more loss if your card is stolen or used by fraud, though Capital One’s zero liability policy protects you in most cases.

The best users treat a higher limit as a safety buffer, not as more money to spend. They keep their normal spending the same, enjoy the lower utilization ratio, and let their credit score grow. That’s how a credit line increase pays off in the long run.

Frequently Asked Questions (FAQs)

Why is it so hard to get a credit limit increase with Capital One?

Capital One denies requests mainly for short account history, recent late payments, utilization over 30%, or outdated income on file. Asking too soon after a previous increase, before the six-month cooldown ends, is another common cause of denial.

Will Capital One give me a second chance?

Yes, you can reapply after fixing the issue named in your denial letter, typically after waiting six months. Paying down your balance, updating your income, or building more on-time payment history usually improves your next attempt.

What is the 6-month rule for Capital One?

Capital One generally requires at least six months between manual credit limit increase requests on the same card. The clock starts from the date of your last decision, not the date you applied.

How do I get Capital One to raise my credit limit?

Log into your account, open the “I Want To” menu, and select “Request Credit Line Increase,” then enter your income, housing payment, and desired limit. You can also request by phone at 1-800-227-4825 or wait for an automatic increase offer.

How often does Capital One automatically increase credit limits?

Capital One reviews eligible accounts automatically, often after about six months of on-time payments and steady card use. Not every account qualifies, and secured cards rarely receive automatic increases.

Should I increase my credit limit every 6 months?

You can request an increase as often as every six months, but it’s only worth it if your payment history is clean and utilization is under 30%. Requesting too aggressively without improved finances raises your denial risk.

Can I request a credit limit increase on a Capital One secured card?

No, secured cards don’t use the standard increase request form since your limit is tied to your security deposit. You can raise it by adding more to your deposit, or qualify for an unsecured upgrade after months of on-time payments.

What happens if Capital One denies my credit limit increase request twice?

Each denial letter lists specific reasons, so review both letters and fix every issue mentioned, such as high utilization or outdated income, before reapplying. Waiting the full six months between attempts and building a longer clean payment history improves your odds on a third try.

How do I get a $10,000 credit limit with Capital One?

Reaching $10,000 typically requires multiple increases over time, since Capital One favors requests of 10% to 25% above your current limit rather than large jumps. Building a year or more of on-time payments and rising income makes larger increases, including past the 25% range, more realistic.

Bottom Line

Getting a higher line on your Capital One card comes down to timing, clean payment history, and asking for a realistic amount. The bank uses soft inquiries, so the request itself is safe to make. The most effective approach is to wait at least six months after opening the account or your last increase, keep your utilization under 30%, update your income, and ask for 10% to 25% above your current limit.

If you’re denied, the letter tells you what to fix before you try again. For most cardholders, using the new limit as a buffer instead of a spending boost can really improve their credit score.

If you know someone stuck with a low credit limit who’s afraid to ask for more, share this guide with them on social media. It could be the push that finally lifts their score and gives them the breathing room they’ve been missing.