I’ve been there myself, sitting with my Quicksilver card in hand, wondering if Capital One would say yes to a second card. Most people get stuck on the same worry: will the bank actually approve me, or will I just waste a hard inquiry? The rules feel hidden, and one wrong move can ding your credit. The good news? Capital One follows a clear, pattern-based system that you can learn.

The simplest answer is yes, you can hold two personal Capital One cards if you meet the timing, credit, and bureau rules.

Below, I’ll walk you through every rule, the best card pairings, and the smart steps to apply with confidence.

Key Takeaways

This guide explains how to get approved for a second Capital One credit card, including the bank’s informal two-card limit, six-month application rule, three-bureau credit checks, approval factors, and strategies for choosing the best card combination.

Core Facts:

- Capital One generally allows cardholders to hold two personal credit cards at the same time, although this limit is based on observed approval patterns rather than a published policy.

- Capital One typically approves only one new card every six months, and applying before the waiting period ends often results in a denial.

- Capital One pulls credit reports from Equifax, Experian, and TransUnion during the application process, resulting in hard inquiries across all three bureaus.

- Approval for a second Capital One card depends on factors including credit score, payment history, credit utilization, income, account age, and recent credit activity.

- Capital One business cards generally do not count toward the informal two-personal-card limit, but the six-month approval rule still applies.

- Using Capital One’s pre-approval tool provides card recommendations through a soft credit check and can help reduce unnecessary hard inquiries.

Best for:

- Current Capital One cardholders considering a second card and wanting to understand approval requirements before applying.

- Consumers deciding between travel rewards and cash-back card combinations to maximize ongoing spending rewards.

- Applicants who want to protect their credit score by understanding Capital One’s timing rules, credit bureau pulls, and pre-approval process.

Can You Have Two Capital One Credit Cards?

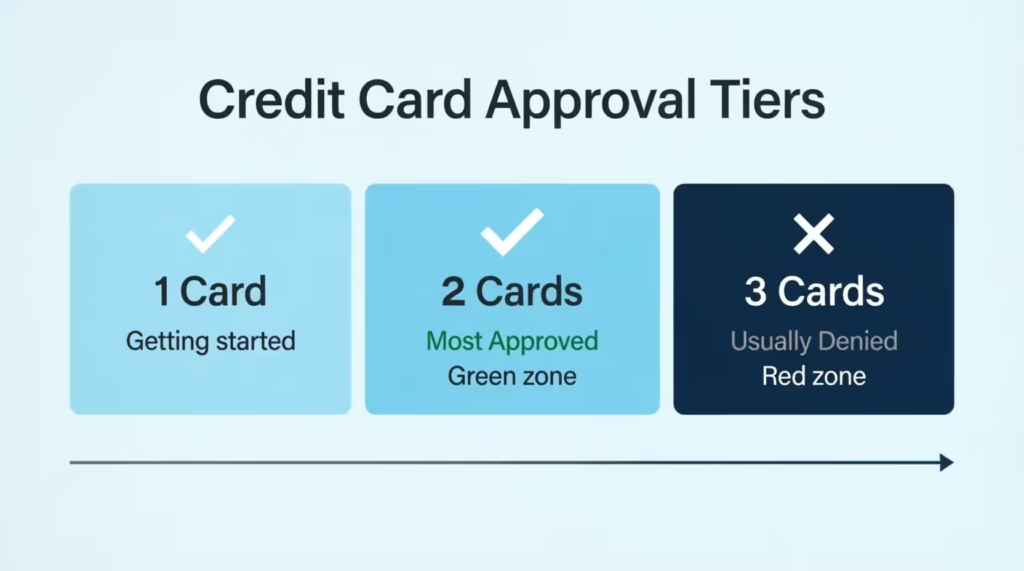

Yes, you can hold two personal Capital One credit cards at the same time. The bank does not post an official cap. But in practice, most cardholders see a soft limit of two personal branded cards on their account. This is not written into Capital One’s terms. It is a pattern people see again and again when they apply for a third card and get denied.

So while you can have multiple Capital One credit cards, the issuer tends to draw the line at two personal accounts. Business cards and cobranded cards work a bit differently, and we’ll cover those in a later section.

If you already have one card, like a Quicksilver or a Venture, you are in a strong spot to add a second. You need to follow the bank’s other rules around timing, credit checks, and your profile.

The Informal Two-Card Cap Explained

The two-card cap is called “informal” for a reason. It is not in any printed policy. But Capital One’s underwriting team uses it as a guideline. If you try to open a third personal card, the system often flags it. You may get an instant denial, even with a strong FICO score.

Here is what this means for you:

- Two personal cards = green zone. Most users with good credit can hold this combo with no issue.

- Three personal cards = red zone. Approvals here are rare, and the denial letter often cites “too many Capital One accounts.”

- Business cards do not always count. More on this below.

Think of it like a soft fence. You can lean on it, but you can’t jump over it. The bank wants to spread risk across many customers, not stack too much credit with one person.

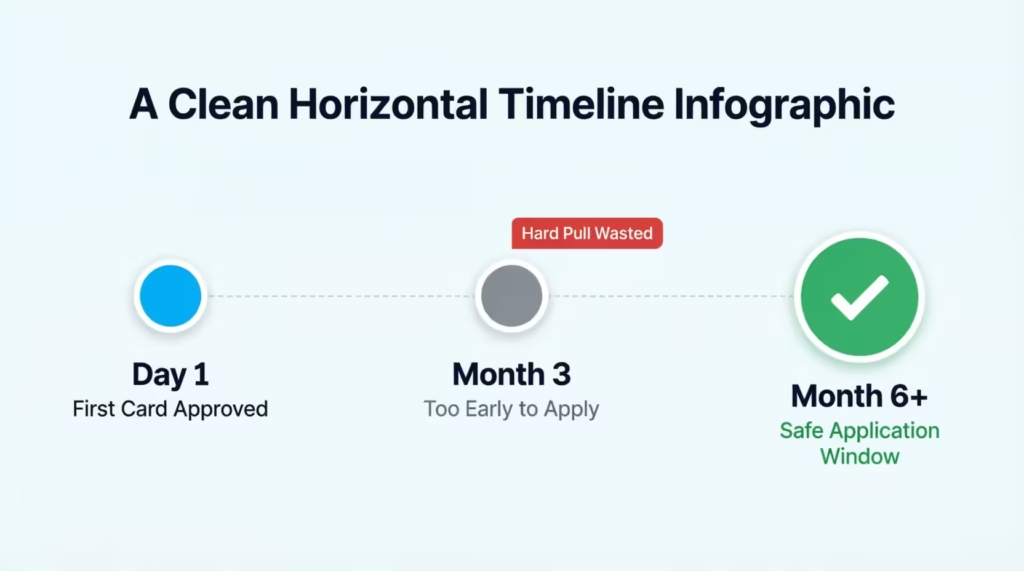

How Long You Have to Wait Between Capital One Applications

Capital One uses a clear timing rule. You can only get one new card approved every six months across the bank. This is true even if you apply for two different cards. The system will approve the first and deny the second if both fall in the same six-month window.

So if your Quicksilver was approved on January 1, your next approval window opens on July 1. Applying on June 15 will almost always result in denial, no matter how strong your credit looks.

Here are a few key points to keep in mind:

- The clock starts on the approval date, not the date you got the card in the mail.

- Denials still trigger a hard pull. So a rushed second application can hurt your score for no gain.

- The rule applies bank-wide. A personal card and a small business card both fall under this six-month window in most cases.

💡 Pro Tip: Set a calendar reminder for the exact day six months after your last Capital One approval. Apply the next day, not before, to avoid an auto-denial that still costs you a hard inquiry.

This rule helps the bank manage risk. It also protects you from stacking too much new credit too fast, which is a known FICO score risk.

Capital One Pulls All Three Credit Bureaus: What That Means

Here is one of the most missed facts about applying. Capital One pulls your credit file from all three major bureaus: Equifax, Experian, and TransUnion. Most banks pull from just one. Capital One pulls from all three at once.

This matters for two reasons.

First, you get three hard inquiries on your record, not one. Each inquiry can shave a few points off your score. As FICO notes, one new hard inquiry usually drops a FICO score by less than five points. With three inquiries, you may see a dip of 5 to 10 points across your reports.

Second, you can’t hide a weak bureau. Some people have a strong Experian file but a weaker TransUnion file. Other banks let you slip by on the strong one. Capital One sees all three. So your weakest credit report sets the floor for your approval.

To prepare, pull your free reports from AnnualCreditReport.com before you apply. Look at all three. Fix errors first. Pay down high balances on any card to lower your utilization ratio across each bureau.

This three-bureau pull is one reason the six-month rule exists. The bank wants to keep your file clean and avoid stacking inquiries.

What Capital One Evaluates When Approving a Second Card

When you apply for a second Capital One card, the bank looks at a short list of key factors. These tie back to standard underwriting, but Capital One puts extra weight on a few of them.

The main factors include:

- FICO Score. A score of 700 or higher lines up well with most Capital One cards. For premium cards like the Venture X, aim for 740 or above.

- Payment history. This is the biggest piece of your FICO Score, worth about 35% of the total. One late payment in the past two years can sink your odds.

- Credit utilization. Keep your balances below 30% of your limits. Below 10% is even better.

- Income. Capital One wants to see steady income that supports the new credit line.

- Length of time with your first card. Six to eighteen months of good use is the sweet spot.

- Recent credit applications. Too many new accounts in the last 12 months can hurt your odds.

The bank also reviews your full credit mix. A clean file with a mortgage, an auto loan, or another card you pay on time signals you can handle more credit.

| Factor | Target Range | Why It Matters |

|---|---|---|

| FICO Score | 700+ (740+ for premium) | Sets your approval tier |

| Utilization | Below 30% | Shows healthy credit use |

| First card age | 6 to 18 months | Proves you can manage the card |

| Late payments | Zero in last 24 months | Confirms reliability |

| Recent inquiries | Fewer than 3 in 12 months | Avoids “credit hungry” flag |

Does a Capital One Business Card Count Toward the Limit?

Here is the short answer: a Capital One business card usually does not count against your two-personal-card cap. Business cards live on a separate ledger in Capital One’s system. So you may be able to hold two personal cards and one or two small business cards at the same time.

But there are a few catches:

- The six-month rule still applies. A business card approval starts the clock just like a personal card.

- The business card will likely report to your personal credit report, since most small business cards do. That means it can still affect your utilization and FICO Score.

- You need a real business, even a side hustle, to apply. The application asks for a business name and an income source.

So if you run a small consulting firm or sell items online, a business card can be a smart way to add credit without using a personal card slot.

Do Cobranded Cards Count?

Cobranded cards, like a Capital One-backed airline or hotel card, sit in a gray zone. The two-card cap mostly tracks Capital One-branded personal cards, the ones with names like Quicksilver, Savor, and Venture. Cobranded cards may not count against the two-card cap in the same strict way.

Still, the bank pulls all three bureaus and applies the six-month rule no matter what type of card you apply for. So treat a cobranded card the same as a regular Capital One card when you plan your timing.

Check Pre-Approval Before You Apply

The single best step you can take is to use Capital One’s free pre-approval tool on its website. This is a soft pull. It does not show up on your credit report. It does not drop your score. It just tells you which Capital One cards you may qualify for based on a soft check of your file.

To use the tool:

- Go to the Capital One pre-approval page.

- Enter your name, address, date of birth, and the last four digits of your Social Security number.

- Wait a few seconds for a list of cards you may qualify for.

If your target card shows up in your pre-approval list, your odds of full approval go up by a lot. If it does not show up, you can hold off and work on your credit first. This single step can save you from a needless hard inquiry and the three-bureau hit that comes with it.

What Pre-Approval Does and Does Not Tell You

Pre-approval is a useful tool, but it is not a promise. Here is what it covers and where it falls short.

What pre-approval tells you:

- Which Capital One cards do your file currently line up with?

- A rough hint that you are in the bank’s target zone for that card.

- A safe way to test the waters without any credit impact.

What pre-approval does not tell you:

- Your final credit limit.

- Whether you’ll clear the six-month rule.

- Whether income, debt, or recent inquiries might trip up the full review.

In other words, pre-approval is a green light to try, not a guaranteed yes. The full application still does a three-bureau hard pull, and the bank reviews your file in more detail before making a final call.

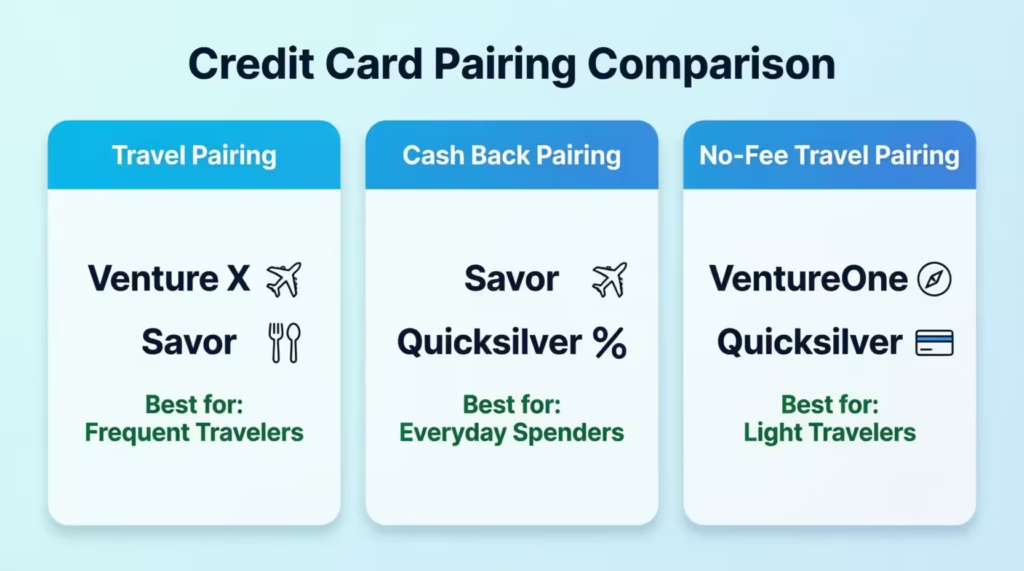

The Best Two-Card Combinations With Capital One

Picking the right second card is just as important as getting approved. The best pairings let you stack rewards in two key spots, often travel and everyday spending. Here are three smart combos to think about.

Travel-Focused Pairing: Venture X + Savor

If you travel a few times a year and dine out often, this pairing is hard to beat.

- Venture X earns 2 miles per dollar on every purchase, plus higher rates on travel booked through Capital One Travel. It also gives a yearly travel credit and lounge access.

- Savor earns higher cash back on dining, entertainment, and streaming. You can then transfer that cash back into miles through the Venture X account.

This is where the magic happens. The Savor’s strong dining rewards turn into flexible travel miles when paired with the Venture X. Together, you have a high-earning everyday card and a strong dining card that share one rewards pool.

Cash-Back-Focused Pairing: Savor + Quicksilver

If you don’t travel much but want strong cash back, pair the Savor with the Quicksilver.

- Savor gives boosted cash back on dining, entertainment, and streaming.

- Quicksilver earns a flat 1.5% cash back on everything else.

Use the Savor at restaurants, concerts, and on Netflix. Use Quicksilver for gas, groceries, and bills. Together, they cover almost every spend type with no overlap.

📌 Did You Know: Capital One lets you pool cash back between some cards in your account. That means a $200 reward on the Quicksilver can sit next to a $300 reward on the Savor, ready to use as one balance.

No-Annual-Fee Pairing With Travel Access

If you want travel perks without a yearly fee, look at this combo.

- VentureOne earns 1.25 miles per dollar on every purchase with no annual fee.

- Quicksilver adds the flat 1.5% cash back for non-travel spend.

This combo works well for light travelers. You can still book flights and hotels with miles, but you don’t pay the higher Venture X fee. It is a strong starter pair for anyone new to travel rewards.

How a Second Capital One Card Affects Your Credit

Adding a second card can help or hurt your score, based on how you use it. The key is to weigh two big factors: utilization and hard inquiries.

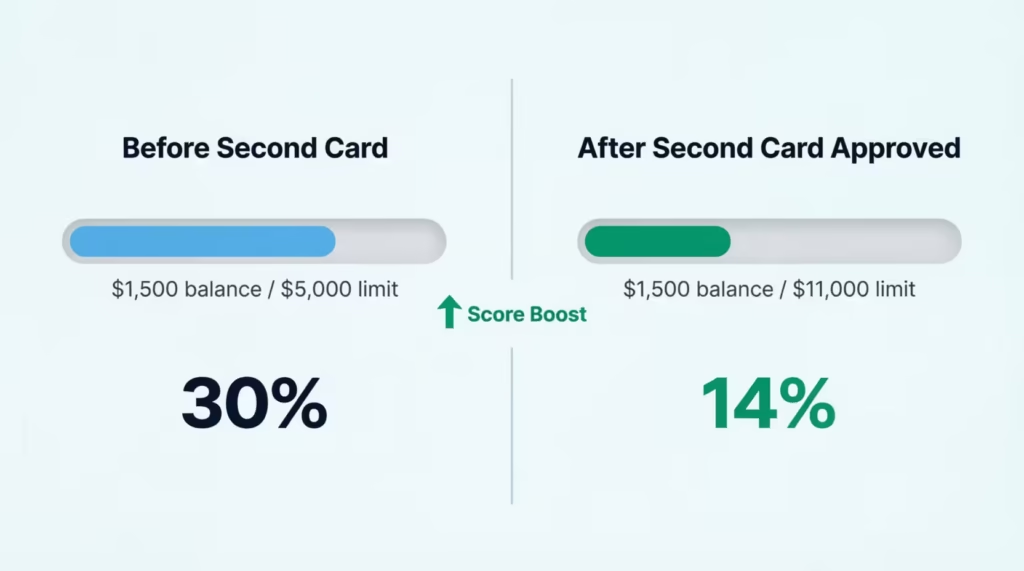

The Credit Utilization Benefit

Here is the upside. A new card raises your total credit limit. If you don’t add new spending, your overall utilization ratio drops.

Let’s run a quick example. Sarah, a marketing manager at a mid-sized consulting firm, has a Quicksilver with a $5,000 limit and a $1,500 balance. Her utilization is 30%. She gets approved for a Savor with a $6,000 limit. Now her total limit is $11,000 with the same $1,500 balance. Her utilization drops to about 14%.

That drop alone can lift her FICO Score by 10 to 20 points over the next two billing cycles. As Experian explains, credit utilization is the second biggest factor in your FICO Score, just after payment history. Keeping it low across your billing cycle is one of the fastest ways to lift your score.

The Hard Inquiry Impact in Real Numbers

Now the downside. Capital One’s three-bureau pull means three hard inquiries. Each one can knock off a few points. The real-world drop tends to be:

- 5 to 10 points total in the first month.

- The points usually return within 6 to 12 months as long as you pay on time.

- Hard inquiries fully drop off your credit report after two years.

So you may take a short dip of about 10 points. But the utilization benefit often more than makes up for it within a few months. The net effect is usually a higher score, not a lower one, if you handle the new card well.

Managing Two Capital One Cards Without Hurting Your Credit

Once you have two cards, the goal is to keep your file strong. The biggest factor is on-time payment history, which makes up 35% of your FICO Score. One late payment can undo months of good work.

Here is a simple plan to follow:

- Set up autopay on both cards for at least the minimum due. This stops missed payments cold.

- Pay the full statement balance each month if you can. This skips all interest charges.

- Use the Capital One mobile app to track both cards in one place. Push alerts for due dates, big charges, and rewards.

- Keep each card active. Run a small charge on the second card every few months. Banks may close inactive cards, which hurts your utilization.

- Watch your utilization per card. Try to keep each card below 30%, not just your total.

⚠️ Mistake to Avoid: Closing your first card after you get a second one. Closing it drops your total credit limit and can spike your utilization ratio overnight. It also lowers the average age of your accounts.

A simple monthly check, ten minutes in the app, is all you need to keep both cards working for you.

When a Second Capital One Card May Not Be the Right Move

A second card is not for everyone. There are clear signs that you should hold off and try another path.

You may want to wait if:

- You plan to apply for a mortgage, auto loan, or student loan in the next 6 to 12 months. New inquiries and a fresh account can lower your score right when you need it high.

- You already applied for another credit card in the last six months. The six-month rule will likely lead to a denial.

- Your utilization is above 50% on your first card. Pay it down first. A new card right now signals you may be chasing credit to cover debt.

- You have a late payment in the last 12 months. Build a clean payment record first.

- Your income just dropped, or you changed jobs in the last 90 days. The bank may see this as a risk.

If any of these match your case, a second Capital One card can wait. Your goal is to apply when your file is at its strongest, not when you are stretched thin.

Consider a Credit Limit Increase Instead

If you want more credit but the timing isn’t right, ask for a credit limit increase on your current card. Capital One often allows these every six months. Many requests are soft pulls, which means no hit to your credit score.

To ask for one:

- Log in to your Capital One account, online or in the app.

- Find the “Request a credit line increase” link under your card’s services menu.

- Enter your current income, rent or mortgage, and the new limit you want.

- Wait a few seconds for a decision, or expect a letter within seven to ten days.

A higher limit gives you the same utilization benefit as a new card, without the hard inquiry hit. It is the smart middle step for many people who are not ready for a second account.

Frequently Asked Questions

Can I have more than two Capital One credit cards?

Capital One has no official written limit, but in practice, the bank applies an informal cap of two personal branded cards per customer. Attempting a third personal card typically results in a denial, even with a strong credit score.

Can I get 3 Capital One cards?

Getting three personal Capital One cards is possible but rare. Most applicants who try for a third receive a denial letter citing too many Capital One accounts, even when their credit profile is otherwise strong.

Is it worth having two Capital One credit cards?

Yes, if you pick cards that cover different spending categories. Pairing a dining-focused card like the Savor with a flat-rate card like the Quicksilver lets you earn higher rewards across most purchases without overlap.

What credit score do I need for a Capital One card?

A score of 700 or higher qualifies for most Capital One cards. For premium options like the Venture X, aim for 740 or above, since those cards have stricter approval thresholds.

Will Capital One give me a second chance?

Yes, if you use the free pre-approval tool on Capital One’s website before applying. It runs a soft pull that won’t affect your score and shows which cards you currently qualify for, so you can rebuild your profile and apply when the odds are in your favor.

How quickly will Capital One increase my credit limit?

Capital One typically allows a credit limit increase request every six months. Many requests are processed as soft pulls, so there’s no impact to your credit score when you ask through your online account or the mobile app.

What is considered the best Capital One credit card combination?

For travelers, the Venture X paired with the Savor is the strongest combo, combining flat-rate miles on all purchases with boosted rewards on dining and entertainment. For cash-back users, the Savor and Quicksilver together cover nearly every spending category.

Does a Capital One business card count toward the two-card limit?

Business cards generally do not count against the two-personal-card cap since they sit on a separate ledger in Capital One’s system. However, the six-month rule between approvals still applies to business cards, just as it does to personal ones.

Do cobranded Capital One cards follow the same rules as personal cards?

Cobranded cards may not count against the two-personal-card cap in the same strict way as branded cards like the Quicksilver or Venture. That said, Capital One still pulls all three credit bureaus and enforces the six-month rule regardless of card type.

Bottom Line

Adding a second Capital One card can boost your rewards and lower your utilization, but only if you follow the bank’s rules. Based on the data in this guide, the best path is to check pre-approval first, wait the full six months between applications, and pick a card pair that matches how you actually spend.

The most effective approach for most readers is the Venture X plus Savor combo if you travel, or the Savor plus Quicksilver combo if you don’t. Smart pairing turns a second card into a real win for your wallet.

If you know someone planning to apply for a new Capital One card, share this guide. It could save them from a needless denial and protect their credit score in the process.