If you’re packing for a trip and wondering whether your Capital One credit card will actually work once you land, you’re not alone. Many travelers aren’t sure what fees to expect, whether their card needs a PIN, or what happens if something goes wrong abroad.

The good news is that Capital One credit cards are built for international use and work in countries around the world with no foreign transaction fees.

In this guide, we’ll walk you through everything, from fees and chip technology to what to do if your card is declined or lost overseas.

Key Takeaways

This guide explains how Capital One credit cards work internationally, including card acceptance, foreign transaction fees, currency conversion, ATM usage, PIN limitations, security features, and practical steps to avoid unnecessary travel costs abroad.

Core Facts:

- Capital One credit cards work internationally through the Visa or Mastercard network and are accepted at millions of merchants, hotels, restaurants, and ATMs worldwide.

- Capital One charges no foreign transaction fees on any credit card, including travel, cash back, student, and business cards.

- International purchases are converted using the Visa or Mastercard exchange rate, and Capital One does not add its own currency conversion markup.

- Dynamic currency conversion can increase costs because merchants use their own exchange rates; choosing local currency helps avoid these extra charges.

- Capital One credit cards use chip-and-signature technology, which works at most staffed merchants but may encounter issues at some automated kiosks and transit terminals.

- ATM withdrawals with a Capital One credit card are treated as cash advances and may trigger cash advance fees, immediate interest charges, and ATM operator fees.

Best for:

- Travelers who want to understand whether a Capital One credit card will work internationally and what fees or limitations to expect.

- Cardholders preparing for international travel who want to avoid unnecessary currency conversion costs and payment issues abroad.

- People who plan to use their Capital One card for purchases overseas and need guidance on ATM withdrawals, security tools, and backup payment strategies.

Yes, Your Capital One Credit Card Works Internationally — Here’s What to Know

Here’s the short answer: your Capital One credit card is accepted in countries all around the world. Capital One has designed all of its credit cards to work internationally. The cards use the Visa or Mastercard network. Both are accepted at millions of shops, hotels, restaurants, and ATMs around the world.

There are a few important things to know before you go, though. Capital One charges no foreign transaction fees on any of its credit cards. That includes travel cards, cash back cards, student cards, and business cards. You won’t see a 1% to 3% surcharge added to your international purchases the way you might with other banks.

Capital One also does not require you to set a travel notice before your trip. Their fraud detection system monitors your account automatically. So there’s no phone call to make, no form to fill out, and no box to check before boarding your flight.

That said, there are a few situations where things can get more complicated. Certain automated kiosks may prompt for a PIN that your card doesn’t use for purchases. Dynamic currency conversion can add hidden costs if you’re not careful. And ATM withdrawals are handled differently from regular card purchases. The sections below break all of this down so you know exactly what to expect.

Which Networks Are Capital One Credit Cards On?

Capital One issues its credit cards on both the Visa and Mastercard networks. Which one you have is printed on the front or back of your card. Both networks are accepted in nearly every country in the world. They are two of the four major global payment networks, and they have by far the widest international reach.

To check which network your card uses, look at the lower-right corner of your card for the Visa or Mastercard logo. You can also check the Capital One Mobile app or your online account.

One important note: acceptance happens at the merchant level. Most large merchants, hotels, airports, and restaurants worldwide accept both networks without issue. In very rural areas or at very small local shops, some vendors may only accept cash or local payment methods. It’s good to have a bit of local cash for emergencies. But for most international purchases, your Capital One card will work well.

Capital One Charges No Foreign Transaction Fees — On Any of Its Cards

One of the biggest worries travelers have is the foreign transaction fee. Many banks charge a fee for purchases made outside the U.S. This surcharge typically ranges from 1% to 3% of each transaction. You’ll see it listed as a separate line item on your monthly statement.

Capital One does not charge this fee. And this isn’t just for their travel-focused products. Capital One confirmed that the no-foreign-transaction-fee policy applies to every credit card they issue, including cash back cards, student cards, and business cards. You don’t need a Venture card to benefit from this.

WalletHub data shows that Capital One cardholders save an average of 1.58% on every international purchase compared to the average credit card offer. On a $5,000 international trip, that’s roughly $79 in savings just from avoiding the fee. It’s not a huge number on a single trip, but it adds up across extended travel or frequent international use.

One thing to understand clearly: “no foreign transaction fee” does not mean “no possible international costs.” Capital One removes the fee that its own institution would charge for processing a foreign purchase. But two other potential costs can still apply: currency conversion and ATM-related fees. Both of those are covered in the sections below.

How Capital One Converts Foreign Currency

When you use your Capital One card abroad, the price is charged in the local currency and then converted to U.S. dollars. The conversion rate used is the Visa or Mastercard network exchange rate on the date the transaction is processed. Since Visa and Mastercard update their rates every day based on market conditions, the rate you get is competitive. In most cases, it’s better than what you’d find at an airport currency exchange counter.

Airport kiosks and currency exchange booths typically charge markups of 5% to 10% above the market rate. Using your Capital One card at a merchant is usually a better deal than converting cash before your trip or at the exchange counter.

One thing to be aware of: the processing date may not be the same as your transaction date. A purchase on a Monday might not go through until Tuesday or Wednesday. The exchange rate shown on your statement will be the one from the processing date. This is normal. It’s not an error. The difference is usually very small, but it’s worth knowing so you’re not surprised when you review your statement at home.

📌 Did You Know: The exchange rate on your Capital One statement comes directly from Visa or Mastercard, not from Capital One itself. Capital One applies no additional markup on top of the network rate, which is why using the card directly tends to beat airport currency exchange counters by a significant margin.

Always Pay in Local Currency — How to Avoid Dynamic Currency Conversion

Dynamic currency conversion, often called DCC, is one of the most common and costly traps for international travelers. Here’s exactly how it works.

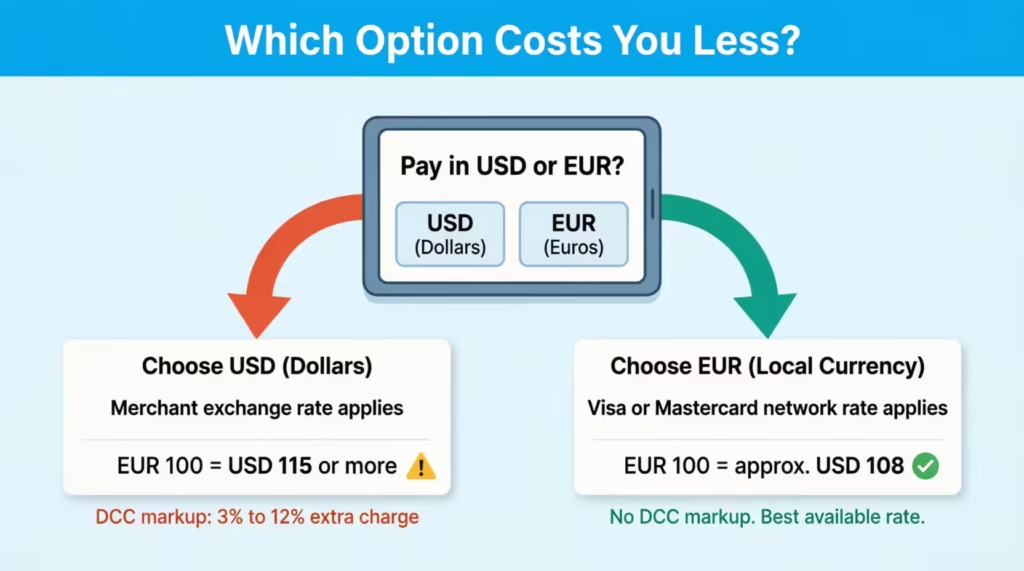

You’re at a restaurant in Paris. The bill arrives in euros. When you hand over your card, the terminal asks: “Would you like to pay in euros or U.S. dollars?” It sounds helpful. You can see exactly how much you’re spending in your home currency. But there’s a significant cost hiding in that convenience.

When a merchant converts the charge to U.S. dollars at the point of sale, they use their own exchange rate, not Visa’s or Mastercard’s. That merchant rate is almost always worse. Dynamic currency conversion fees usually range from 3% to 12% of the purchase amount, as stated by Capital One. That’s money you pay in addition to whatever the normal exchange rate would have cost you.

Here’s a concrete example. Say you’re buying a €100 jacket in Rome. At the standard Visa network rate, that might convert to roughly $108. If you accept DCC, that same jacket could show up as $115 or more on your statement. That’s an extra $7 on one purchase. On a two-week trip with dozens of transactions, accepting DCC every time could easily cost you $150 to $200 more than necessary.

The solution is simple. Always choose to pay in the local currency. When a terminal or ATM asks if you want to pay in dollars or local currency, always choose local currency. Your Capital One card will handle the conversion using the Visa or Mastercard network rate, which is the better deal.

This applies at ATMs too. Some international ATMs will ask if you want to withdraw in U.S. dollars. Say no. Take the local currency and let your card do the conversion.

You are never required to accept dynamic currency conversion. It’s optional at every terminal. If a merchant tries to complete the transaction in dollars without giving you a choice, you can ask them to redo it in local currency.

⚠️ Mistake to Avoid: Accepting “pay in dollars” at a foreign terminal is one of the most common and expensive mistakes international travelers make. Even experienced travelers sometimes click through it without thinking. Get in the habit of looking for the currency option before confirming any payment abroad.

Does Your Capital One Card Need a PIN to Work Abroad?

Capital One credit cards use chip-and-signature technology. The chip in your card makes a unique code for each transaction. You verify purchases by signing, not by entering a PIN. This is the standard for U.S.-issued credit cards.

For the vast majority of international travel, this is not a problem. Most merchant terminals in Europe, Asia, Latin America, and beyond accept chip-and-signature cards without issue. Restaurants, hotels, shops, and most transit hubs with staffed counters handle these cards the same way they handle any credit card.

Capital One’s help centre states clearly: your card doesn’t need a PIN for purchases outside the U.S. If a terminal asks for a PIN, just talk to the merchant. In most cases, they can process the transaction another way, either by switching to a signature-based mode or running it as a contactless payment.

Contactless tap-to-pay is a practical workaround in many situations. For smaller purchases, tapping your card at an NFC-enabled terminal skips the PIN prompt entirely. This is used in more and more transit systems, coffee shops, convenience stores, and supermarkets around the world.

Where Chip-and-Signature Cards Can Fail: Automated Kiosks and Transit Terminals

The real limitation of chip-and-signature cards shows up at self-service, automated terminals. These include:

- Train and subway ticket machines in many European countries

- Parking garage pay stations

- Toll booth kiosks

- Self-service fuel pumps at gas stations in some countries

- Some museum or attraction ticketing kiosks

These machines are often designed to work with chip-and-PIN cards only. They can’t process a signature. So, if your card’s chip is read, the machine might decline it or get stuck asking for a PIN that you haven’t set up for purchases.

This is a known limitation, not a card malfunction. It affects nearly all U.S.-issued credit cards, not just Capital One.

The practical solutions are straightforward. First, look for a staffed window or counter nearby. A human cashier can usually process your chip-and-signature card without issue. Second, try contactless tap-to-pay if the machine supports it, since this often bypasses the PIN prompt. Third, keep a debit card with a PIN as a backup for exactly these situations. Many travelers find that a debit card handles transit kiosks and parking machines more reliably than a credit card abroad.

How to Get a Cash Advance PIN from Capital One Before You Travel

Capital One does offer a Cash Advance PIN, and you can request one before your trip. Here’s how to get it:

- Log in to your Capital One account online

- Select the credit card you want the PIN for

- Click “I Want To…” and look for “Get a Cash Advance PIN.”

- Choose to receive it in the mail or instantly using a security code sent to your phone

If you request it by mail, allow several days for delivery. Don’t wait until the day before you leave.

One important clarification: this PIN is designed for ATM cash advance withdrawals, not for purchase authorization at merchant terminals. Getting a Cash Advance PIN does not turn your Capital One card into a chip-and-PIN card for store or kiosk purchases. It gives you the ability to withdraw cash at an ATM abroad in case of an emergency.

Knowing this PIN before you leave is useful. Trying to request one while you’re already in another country is inconvenient, and by mail, it won’t arrive in time.

Do You Need to Notify Capital One Before Traveling Internationally?

No. Capital One does not require a travel notice, and as of 2026, there is no travel notice feature to set for Capital One credit cards.

Many banks still require cardholders to call ahead or log into their account to flag upcoming international travel. This helps their fraud systems recognize that a charge from Tokyo or London is legitimate. Capital One took a different approach. Their automated fraud detection watches your account all the time. It looks for patterns that seem truly suspicious, not just any purchase from a foreign country.

This means you can board your flight without making any calls to Capital One, and your card should work as expected on the other side.

A key point to note: if you have a Capital One checking or savings account with a debit card, the rules for ATM withdrawals in high-risk countries are slightly different. Capital One’s identity protection policy says that if you notify them about international ATM use, it can stop blocks on your account. If you’re bringing a Capital One debit card in addition to a credit card, it’s worth checking your specific account terms before traveling.

For credit cards specifically, no travel notice is needed or available. The fraud detection system handles it.

What to Do Before Your International Trip Instead

Even though you don’t need to set a travel notice, there are a few specific steps that will make your trip much smoother.

Update your contact information. Log in to your Capital One account and confirm that your phone number and email address are current. Capital One sends real-time fraud alerts to your phone and email. If your contact details are outdated, those alerts won’t reach you, and you may not know if something suspicious happens on your account.

Download the Capital One Mobile app and enable push notifications. The app lets you view transactions in real time, lock your card instantly, and manage your account from anywhere with a data connection. Set up push notifications before you leave so you get instant alerts for every purchase.

Save Capital One’s international customer service number. The number to call from abroad is +1-804-934-2001, and Capital One accepts collect calls. Save this in your phone before you travel. If something goes wrong and you don’t have data access, you can call from any landline.

Check your available credit. Know your current credit limit and available balance before you leave. Large hotel pre-authorizations and rental car holds can temporarily reduce your available credit. If you’re planning high-spend travel, it’s worth knowing where you stand.

Request a Cash Advance PIN if you think you’ll need ATM access. See the section above for how to do this. It takes a few days if done by mail, so request it early.

Using Your Capital One Card at ATMs Abroad

Your Capital One credit card can be used at any ATM internationally that displays the Visa or Mastercard logo. Both networks have global ATM systems, so you can find compatible machines at most airports, banks, and commercial areas worldwide.

However, there is a critical distinction between using your card at an ATM and using it at a merchant terminal for a regular purchase. Using a credit card at an ATM is a cash advance, not a standard purchase. The two are treated very differently, and the costs are meaningfully different.

Capital One does not charge a foreign transaction fee on ATM withdrawals with its credit cards. That part is consistent with the general no-foreign-transaction-fee policy. But the cash advance fees and the ATM operator’s own charges still apply.

For most international travelers, using a debit card tied to a checking account is a better option for ATM withdrawals. Debit card withdrawals don’t trigger cash advance fees or immediate interest. If you have a Capital One checking account or a debit card with low international ATM fees, that’s the better tool for pulling local cash. Save the credit card for purchases at merchants.

Cash Advance Fees and Interest on International ATM Withdrawals

When you use your Capital One credit card at an ATM abroad, three separate costs can apply:

1. Capital One’s cash advance fee. This is a front-end transaction fee charged as a percentage of the amount you withdraw. The exact rate varies by card. Check your specific card’s terms for the current figure. This fee posts to your account on the day of the transaction.

2. Interest, starting immediately. Unlike regular credit card purchases, cash advances do not have a grace period. Interest begins accruing on the day you withdraw the cash. The cash advance APR is typically higher than your regular purchase APR.

3. The ATM operator’s fee. The bank or company that owns the ATM may charge its own separate fee for using its machine. This is charged by the ATM itself, not by Capital One, and it’s common at international ATMs. Some ATMs will disclose this fee before you confirm the withdrawal.

Using a credit card for ATM withdrawals costs much more than using a debit card. This is due to the combination of three fees. Use the credit card at ATMs only if you have no other option.

Do You Still Earn Rewards on International Purchases?

Yes. Capital One’s rewards programs apply fully to international purchases. You earn the same rewards on every purchase, whether it’s abroad or at home. There are no reduced earn rates, no penalties, and no exclusions for spending outside the U.S.

This is worth knowing because international trips tend to involve higher-than-usual spending. Hotels, meals, transportation, and activities can add up quickly. That spending can translate into a meaningful amount of miles or cash back if you’re using the right card.

Here’s a quick breakdown of what different Capital One cards earn on international purchases:

| Card | Earn Rate on International Purchases |

|---|---|

| Capital One Venture X | 2X miles on all purchases; 5X on flights/vacation rentals/activities via Capital One Travel; 10X on hotels and rental cars via Capital One Travel |

| Capital One Venture | 2X miles on all purchases; 5X on hotels, vacation rentals, and rental cars via Capital One Travel |

| Capital One VentureOne | 1.25X miles on all purchases |

| Capital One Quicksilver | 1.5% cash back on all purchases |

| Capital One Savor | Category-based cash back (dining, entertainment, groceries) applies to eligible international transactions in those categories |

The miles you earn apply to the total charged in local currency, converted to U.S. dollars at the network rate. There’s no adjustment or reduction because the purchase happened overseas.

If you’re planning a big international trip, now’s a great time to check which Capital One card you have. Cardholders with a Venture or Venture X card earn 2X miles on every international restaurant, hotel, and purchase not booked through the Capital One Travel portal. This adds up fast on a multi-week trip.

What to Do If Your Capital One Card Is Declined Abroad

A declined transaction abroad is frustrating, but it’s usually fixable. Here are the most common reasons it happens and what to do about each one.

Insufficient available credit. Hotels and car rental companies often place large pre-authorization holds on cards when you check in. These holds reduce your available credit even though the money isn’t actually charged yet. If you’re close to your credit limit, a subsequent purchase might be declined. Check your available balance in the Capital One Mobile app before making a large purchase.

Daily transaction or spending caps. Some Capital One cards have daily spending limits. A busy travel day with multiple large purchases can sometimes bump against those limits. If a card is declined and you have plenty of available credit, a call to Capital One’s customer service can often resolve this quickly.

Terminal incompatibility. As covered above, certain self-service terminals require a PIN your card isn’t set up to use for purchases. If an automated terminal declines your card, look for a staffed alternative or try contactless tap-to-pay.

Fraud hold. Even with Capital One’s automated detection, an unusual transaction can sometimes trigger a temporary hold. This is more likely on a first-time large purchase at an unfamiliar merchant in a new country. Capital One will typically send a text alert and may temporarily block the card pending verification.

What to do when a card is declined:

- Check the Capital One Mobile app immediately. It often shows the reason for a decline.

- Try a different payment method at the moment (cash, a debit card, or a second credit card) to complete your purchase.

- Call Capital One’s international customer service at +1-804-934-2001. They can lift a fraud hold, confirm your identity, and restore access in most cases within minutes.

💡 Pro Tip: Always travel with at least two payment methods. A Capital One card as your primary, plus a debit card or a second credit card from a different network, gives you a reliable backup for the rare moments when one card doesn’t work.

How Capital One Protects Your Card When You Travel

Capital One builds several security tools directly into every credit card account. These tools are especially useful when you’re traveling internationally, far from home, and potentially more vulnerable to fraud.

$0 fraud liability. If your card is used for unauthorized purchases, Capital One holds you responsible for none of it. Under federal law, issuers can hold cardholders liable for up to $50 in unauthorized charges made before reporting the card lost or stolen. Capital One waives that entirely. You pay nothing for charges you didn’t make, as long as you report them promptly.

Real-time fraud alerts. If Capital One’s systems detect a suspicious charge, they send an immediate text alert. You can respond to confirm or deny the transaction without having to call in. Make sure your phone number is up to date in your account before you travel so these alerts reach you.

Card lock. If your card is lost or misplaced, you can lock it instantly from the Capital One Mobile app. Locking the card prevents any new purchases or cash advances from going through. If you find the card, you can unlock it just as quickly from the same app. This is one of the most useful tools for international travelers.

Virtual card numbers via Eno. Capital One’s Eno assistant can generate virtual card numbers for online bookings. When booking hotels, activities, or rentals online abroad, use a virtual card number. It keeps your real card number private. If a merchant’s system is ever compromised, your real card number stays protected.

If your card is lost or stolen while traveling:

- Open the Capital One Mobile app and lock the card immediately.

- Call +1-804-934-2001 (collect calls accepted) to report the card stolen.

- Request an emergency card replacement. Capital One can often send a replacement card to your location within a few business days.

- Use your backup payment method while you wait.

Physical security habits to practice abroad:

- Shield your PIN at ATMs and terminals

- Keep your card in sight during restaurant and bar transactions

- Use RFID-blocking sleeves or a wallet to reduce digital skimming risk

- Carry only the cards you need that day; leave others in the hotel safe

Using the Capital One Mobile App to Monitor Your Card Abroad

The Capital One Mobile app is your best tool for managing your account while you’re overseas. Think of it as your card’s control panel, accessible from anywhere with a data connection.

Here’s what the app lets you do while traveling:

- View transactions in real time. Every approved purchase appears in the app within seconds. If you see something you didn’t make, you can act immediately.

- Lock and unlock the card. A few taps and the card is locked. Find it again, and a few more taps unlock it.

- Receive purchase notifications. Enable push notifications to get an alert every time your card is charged. This is the fastest way to spot unauthorized activity.

- Request a Cash Advance PIN. You can do this through the app if you didn’t request one before leaving.

- Access account details. View your available credit, payment due date, and account settings from anywhere.

The app works on Wi-Fi, so even if you don’t have an international data plan, you can use it from your hotel or any Wi-Fi-connected location. Download it and set up your preferred notification settings before you leave home, not after you land.

If you don’t have app access and need to reach Capital One, call +1-804-934-2001. Landline collect calls are accepted, so you don’t need a working international phone plan to reach them.

Frequently Asked Questions (FAQs)

Do I need to do anything before using my Capital One card internationally?

Capital One doesn’t require a travel notice, but a few prep steps will protect you. Update your contact information in your account, enable push notifications in the Capital One Mobile app, and save the international support number (+1-804-934-2001) before you leave.

Which Capital One card doesn’t charge international fees?

Every Capital One credit card, including travel, cash back, student, and business cards, has no foreign transaction fees. There is no specific card you need to qualify for this benefit.

Is a 3% foreign transaction fee high?

Yes, it adds up quickly. On a $3,000 international trip, a 3% fee costs $90 in charges that appear on top of your actual purchases, with no benefit to you in return. Capital One cardholders avoid this fee entirely on every card they offer.

What does a 3% foreign transaction fee cost on $1,000 in spending?

A 3% fee on $1,000 in international purchases adds $30 in extra charges. Capital One doesn’t charge this fee, so that $30 stays in your pocket on every $1,000 you spend abroad.

Is it better to exchange money before traveling or use your credit card?

Using your Capital One card directly at merchants is almost always the better deal. Airport currency exchange counters and kiosks typically charge markups of 5% to 10% above the market rate, while your Capital One card converts at the Visa or Mastercard network rate with no added markup.

What countries accept Capital One credit cards?

Capital One cards run on the Visa and Mastercard networks, which are accepted in nearly every country worldwide. Before traveling to a remote or cash-heavy destination, check whether local merchants in that area accept card payments, since acceptance varies at the merchant level.

Is Capital One good to use in Europe?

Capital One cards work well across Europe for most merchant purchases. One limitation to know: self-service kiosks at train stations and parking garages often require chip-and-PIN, which U.S.-issued Capital One cards don’t support for purchases. A staffed window or contactless tap-to-pay is usually the fix.

What is the downside of Capital One credit cards internationally?

The main limitation is the chip-and-signature technology. Automated kiosks at transit stations, parking garages, and toll booths in some countries require chip-and-PIN, which Capital One credit cards don’t support for purchases. ATM withdrawals also trigger cash advance fees and immediate interest, which makes them more expensive than using a debit card for cash.

Does Capital One charge any fees when using a credit card at a foreign ATM?

Capital One waives the foreign transaction fee on ATM withdrawals, but cash advance fees and immediate interest still apply since credit card ATM use is treated as a cash advance. The ATM operator may also add its own separate fee on top.

Can I use Apple Pay or Google Pay with my Capital One card internationally?

Yes. Capital One cards are compatible with Apple Pay, Google Pay, and Samsung Pay. Using a digital wallet for contactless payments abroad can also serve as a useful workaround at terminals that prompt for a PIN, since tap-to-pay often bypasses that requirement for low-value purchases

Bottom Line

Using your Capital One credit card internationally is straightforward. Capital One cards have no foreign transaction fees. You don’t need to set a travel notice, and there are no penalties for earning rewards on international purchases.

The key is to know the details that matter:

- Always choose local currency at terminals to avoid extra charges.

- Remember that ATM withdrawals count as cash advances and have their own fees.

- Be prepared for what to do if a chip-and-signature card can’t finish a kiosk transaction.

When traveling internationally, use your Capital One card for purchases. Keep a debit card for ATM cash withdrawals. Set up the Capital One Mobile app before your flight.

If you’re heading abroad soon and found this helpful, share it with a fellow traveler who might be asking the same questions.