Planning a trip abroad or shopping from a foreign online store can feel exciting, until the worry kicks in. Will my card hit me with surprise fees? Many Capital One cardholders ask the same thing before booking flights, paying for hotels, or buying something in another currency. The truth about Capital One foreign transaction fees is simpler than most people expect, but the details still matter.

The quick answer: Capital One does not charge any foreign transaction fees on any of its U.S. credit cards or its 360 Checking debit card.

In this guide, we’ll cover each card type, hidden costs, exchange rate facts, and smart travel tips. This way, you can use your card abroad with confidence.

Key Takeaways

This guide covers Capital One’s foreign transaction fee policy across every card type, explains how the Visa and Mastercard exchange rate system works, and identifies hidden costs like Dynamic Currency Conversion and ATM operator fees that can still add up abroad.

Core Facts:

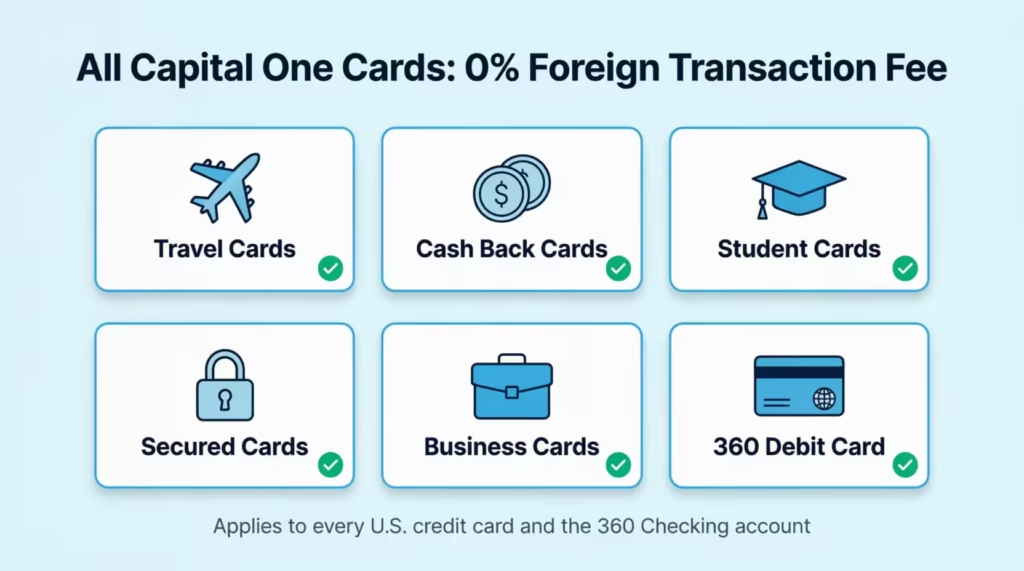

- Capital One charges 0% foreign transaction fees on every U.S. credit card it issues, including travel cards, cash back cards, student cards, secured cards, and business cards.

- The Capital One 360 Checking debit card also carries no foreign transaction fee on purchases or ATM withdrawals made outside the United States.

- Dynamic Currency Conversion (DCC) lets merchants apply their own exchange rate, which can add 3% to 12% on top of the real rate. Always choose local currency at the payment terminal to avoid this.

- ATM operator fees of roughly $2 to $10 per withdrawal may apply abroad. These come from the machine owner, not from Capital One.

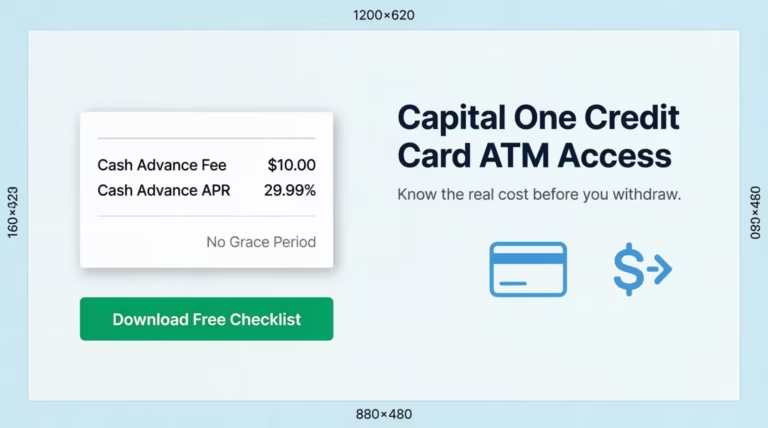

- Using a Capital One credit card at a foreign ATM counts as a cash advance, which carries a fee of around 5% plus immediate interest with no grace period.

- Capital One cards run on Visa or Mastercard networks, accepted in over 200 countries, and apply the network’s wholesale exchange rate with no markup added by Capital One.

Best for:

- Travelers planning international trips who want to confirm their Capital One card will work abroad without surprise fees.

- Online shoppers purchasing from foreign websites or merchants that bill in non-U.S. currencies.

- Capital One 360 Checking account holders who plan to use their debit card for purchases or ATM withdrawals outside the United States.

Capital One’s Foreign Transaction Fee Policy

Capital One stands out in the U.S. credit card market because it charges a flat 0% foreign transaction fee on every credit card it issues. This applies whether you tap your card in a café in Rome, swipe it at a hotel in Tokyo, or type your card number into a website based in London.

A foreign transaction fee is a surcharge added by a card issuer when a purchase is processed outside the United States or in a currency other than U.S. dollars. Most banks tack on 1% to 3% per transaction. On a $2,000 hotel stay, that could mean an extra $60 you didn’t plan for.

Capital One removed this charge across its entire credit card lineup years ago. So whether you carry a basic cash back card or a premium travel card, the international transaction fee is always zero. That’s a real perk, especially compared to issuers like Chase, Bank of America, or Citi, which still charge fees on many of their everyday cards.

💡 Pro Tip: The “no foreign transaction fee” benefit covers the fee itself, not every cost tied to spending abroad. ATM operator charges and merchant currency tricks can still sneak in if you’re not paying attention.

Which Capital One Cards Have No Foreign Transaction Fees

Every single Capital One credit card issued in the United States skips the foreign transaction fee. That includes travel rewards cards, cash back cards, student cards, secured cards, and business cards. You don’t need to pick a premium product to get this benefit, which makes Capital One one of the most traveler-friendly issuers in the country.

Travel Cards

The travel lineup is built for people who fly often and spend time abroad. The Capital One Venture X Rewards card, the Venture Rewards card, and the VentureOne Rewards card all come with no fees on international purchases. You earn miles for every dollar spent abroad. So, a $500 dinner in Paris not only skips extra fees but also boosts your travel rewards.

Cash Back Cards

The Quicksilver and Savor lines, including the Quicksilver Cash Rewards and the Savor Cash Rewards card, also waive the fee. So if you’re using a cash back card abroad, your rewards rate still applies. A 1.5% flat cash back on a Quicksilver purchase abroad means real money back, with no fee eating into your earnings.

Student Cards

Students studying abroad or backpacking through Europe can use the Quicksilver Student card or the Savor Student card without worrying about the surcharge. This is a strong feature, since many student cards from other banks charge international fees and limit travel benefits.

Secured Cards

Even if you’re using a Capital One secured card to rebuild credit, like the Platinum Secured, you’ll still get the 0% fee on foreign purchases. This is rare in the secured card market, where most issuers add a 3% fee.

Business Cards

Small business owners traveling for work get the same deal. The Spark Miles, Spark Cash Plus, and Venture X Business cards have no foreign transaction fees. This helps owners save on travel costs while earning rewards.

International Fees That Can Still Appear With a Capital One Card

While Capital One itself doesn’t charge foreign transaction fees, other charges can pop up during international use. These don’t come from Capital One. They come from ATMs, merchants, or other third parties. Knowing where they hide helps you avoid them.

ATM Operator Fees When Withdrawing Cash Abroad

If you pull cash from an ATM outside the U.S., the local ATM owner may add a fixed fee for using their machine. This can range from $2 to $10 per withdrawal. Capital One doesn’t add an international ATM fee for its 360 Checking debit card, but the local bank that owns the machine still might. To lower this cost, withdraw larger amounts less often and stick to ATMs run by major banks instead of standalone kiosks.

Cash Advance Fees on Credit Cards

Using a Capital One credit card to take out cash from an ATM counts as a cash advance, not a normal purchase. Cash advances usually carry a fee of around 5% of the amount, plus a higher interest rate that starts right away with no grace period. This applies whether you’re at an ATM in Chicago or in Bangkok. So if you need cash abroad, use your 360 debit card, not your credit card.

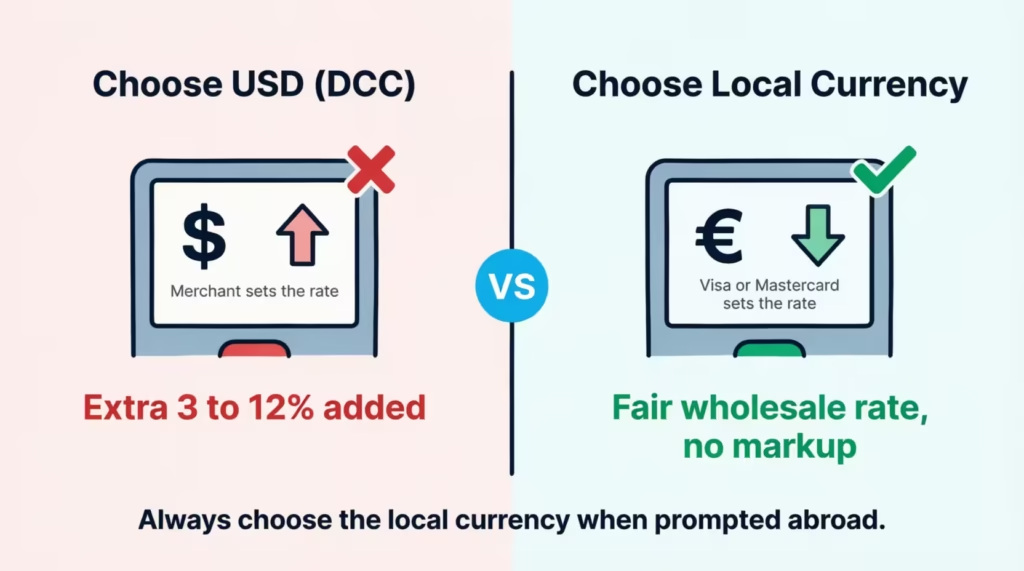

Dynamic Currency Conversion

When you pay with your card overseas, the cashier or payment terminal may ask if you’d like to be charged in U.S. dollars or the local currency. Picking U.S. dollars triggers Dynamic Currency Conversion.

The merchant or terminal provider sets their own exchange rate. This rate is usually worse than the network rate. This shows up as a higher final price, even though Capital One isn’t charging you anything extra.

Dynamic Currency Conversion: What It Is and Why You Should Always Decline It

Dynamic Currency Conversion, often shortened to DCC, is one of the most common ways travelers lose money abroad without realizing it. The pitch sounds helpful. The terminal offers to show you the price in dollars so you know exactly what you’ll pay. But the rate they use is set by the merchant or the payment processor, not by Visa or Mastercard.

These rates can add anywhere from 3% to 12% on top of the real exchange rate. Here’s a simple example. Imagine your dinner in Paris costs €100. The fair Visa rate might convert that to about $108. If you accept DCC, the terminal might show $118 instead. That extra $10 goes to the merchant’s currency conversion partner, not to Capital One.

The fix is easy. When the card reader asks which currency you want, always pick the local currency. So in Spain, choose euros. In Japan, choose yen. In Mexico, choose pesos. This lets Visa or Mastercard manage the conversion at the wholesale rate. This is the rate Capital One gives you without any markup.

⚠️ Mistake to Avoid: Many travelers say yes to DCC because the dollar amount feels easier to understand. That choice can cost more than the foreign transaction fees you were trying to avoid in the first place.

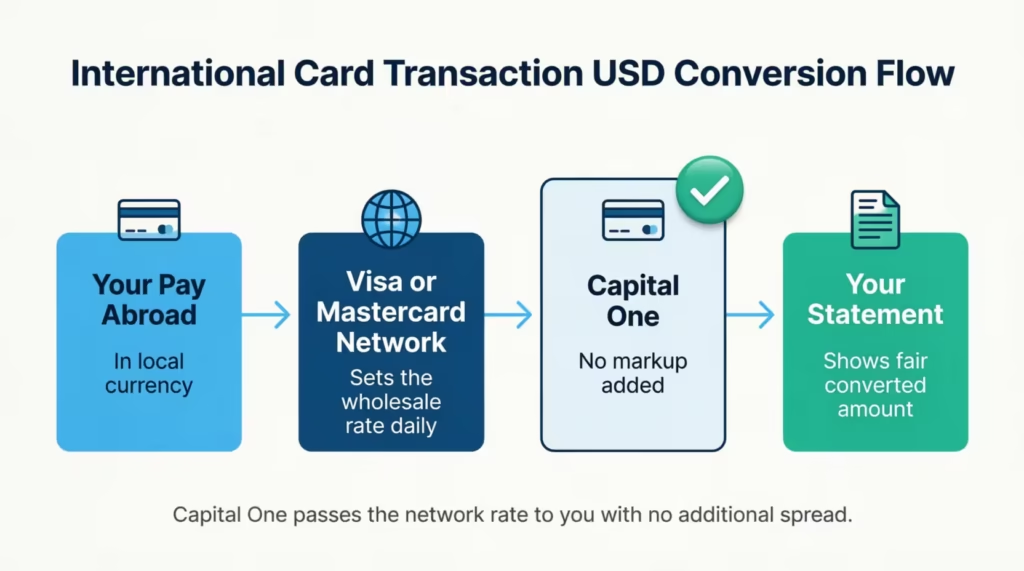

What Exchange Rate Does Capital One Use on International Purchases

When you make a purchase abroad with a Capital One card, the exchange rate comes from the card’s payment network, either Visa or Mastercard, depending on which logo is on your card. These networks set wholesale conversion rates every day. They are usually near the mid-market exchange rate you find on Google or in financial news.

Capital One does not add a markup to this rate. So if Visa converts €100 at a rate of 1.08, your statement shows roughly $108. There’s no hidden spread on top. This is a key reason why Capital One cards are so popular for international travel. The combined effect of no foreign transaction fee and no exchange rate markup keeps your overseas spending close to the real cost.

For comparison, some banks add their own 1% network surcharge or use a less favorable rate. That kind of stack can add up fast. With Capital One, the price you see on the menu is very close to the price that hits your statement, after the simple currency conversion.

Capital One 360 Debit Card and Foreign Transaction Fees

The Capital One 360 Checking debit card is one of the best travel-friendly debit cards out there. It charges no foreign transaction fee on purchases or withdrawals. So if you pay for a taxi in Berlin or buy groceries in Lisbon with your 360 debit card, Capital One won’t add a fee on top.

It also doesn’t add a fee for using out-of-network ATMs internationally. That said, the ATM owner may still charge you their own operator fee, which is separate from anything Capital One controls. To save money, you can use ATMs at Allpoint network locations, which are fee-free even in some international destinations.

Non-360 Capital One Checking Accounts

If you have an older Capital One checking account, like the Essential Checking product from the legacy Capital One Bank branch network, the rules are different. Some of these older accounts do charge foreign transaction fees and international ATM fees.

Before traveling, check your specific account terms or call Capital One to confirm. If you’re a frequent traveler, switching to a 360 Checking account is often worth it.

Do You Need to Notify Capital One Before Traveling Internationally

You do not need to notify Capital One before you travel. The bank dropped its travel notification feature years ago. Instead, it uses real-time fraud detection systems that look at your spending patterns, device data, and merchant location to decide if a charge is normal or risky.

This automatic system works in most cases. If something does look unusual, Capital One may send you a text or push notification asking you to confirm a transaction. As long as you reply quickly, your card keeps working. It’s still smart to make sure your phone number and email in your Capital One account are up to date before your trip, so you don’t miss those alerts.

Managing Your Account While Traveling With the Capital One App

The Capital One mobile app gives you full control while you’re overseas. You can lock or unlock your card with one tap if it gets lost, set travel-friendly alerts, check your balance in real time, and even chat with support through the app.

If you ever spot a charge you don’t recognize, you can dispute it right from your phone without calling a hotline. This kind of in-app control is one of the easiest ways to stay safe and aware on the road.

Where Is a Capital One Card Accepted Internationally

Capital One credit cards run on either the Visa or Mastercard network, both of which are accepted in over 200 countries and territories around the world. That means your card works in most places where card payments are taken, from major cities to small towns.

Almost all Capital One cards now come with chip-and-PIN or chip-and-signature support. This matters because many merchants in Europe, Australia, and parts of Asia use chip-based terminals as their main payment method.

If a terminal asks for a PIN and your card was set up with one, you can use it like a local card. If it only supports a signature, the terminal will usually print a slip for you to sign.

Some specific places may still have limits. For example, automated kiosks at train stations or unattended fuel pumps in Europe sometimes require a chip-and-PIN setup, so it’s wise to carry a backup payment method like cash or a second card.

Outside of those edge cases, your Capital One card should work smoothly anywhere Visa or Mastercard is displayed.

Frequently Asked Questions (FAQs)

Can I use my Capital One card in Europe?

Yes. Capital One cards run on the Visa or Mastercard network, both accepted in over 200 countries, and all U.S. Capital One credit cards charge no foreign transaction fee. Most cards also support chip-and-PIN, which is the standard payment method at European merchants and transit kiosks.

Do I need to tell Capital One I’m traveling internationally?

No. Capital One dropped its travel notification requirement years ago and now uses automated fraud detection that monitors your spending patterns and merchant location in real time. Just make sure your phone number is current in your account so you can confirm any flagged transactions quickly.

What is the best way to pay when traveling in Europe?

Use a no-foreign-transaction-fee credit card and always choose to pay in the local currency when prompted at the terminal. Accepting the dollar option triggers Dynamic Currency Conversion, where the merchant sets their own exchange rate, which can add 3% to 12% on top of the real rate.

How do I avoid a 3% foreign transaction fee?

Use a Capital One credit card, which charges 0% foreign transaction fees on every card in its lineup. Also, decline Dynamic Currency Conversion at payment terminals abroad, since that merchant-controlled currency swap can cost more than the fees you were trying to avoid.

What does a 3% international transaction fee cost on a $1,000 purchase?

A 3% foreign transaction fee on a $1,000 purchase adds $30 to your bill. On a $2,000 hotel stay, that climbs to $60 in charges you did not plan for. Capital One charges 0% on all its U.S. credit cards, so that extra cost disappears entirely.

Can I use my Capital One debit card internationally without fees?

The Capital One 360 Checking debit card charges no foreign transaction fees on purchases or ATM withdrawals abroad. The local ATM operator may still add their own flat fee, typically $2 to $10, but that charge comes from the machine owner, not from Capital One.

Is it better to use cash or a card abroad?

A no-foreign-transaction-fee card, like a Capital One credit card, is usually the better choice because it uses the Visa or Mastercard wholesale exchange rate with no markup added. Cash from a foreign ATM can work for small vendors, but withdrawing with a credit card triggers a cash advance fee of around 5% plus immediate interest.

Does using a Capital One credit card at a foreign ATM trigger extra fees?

Yes. Pulling cash from any ATM with a Capital One credit card counts as a cash advance, which carries a fee of roughly 5% of the amount plus a higher interest rate that starts immediately with no grace period. For ATM cash abroad, use the Capital One 360 debit card instead.

Bottom Line

Choosing the right card for international spending matters a lot, and Capital One makes it easy. Every U.S. credit card and the 360 Checking debit card waive foreign transaction fees, while Visa and Mastercard handle currency conversion at fair wholesale rates. Watch out for DCC traps, cash advance costs, and ATM operator fees, since those still apply.

Based on the evidence in this guide, a Capital One card is one of the most cost-friendly options for travel abroad.

If you know a friend planning a big trip or studying overseas, share this guide so they can save real money on every purchase.