Closing a Capital One credit card sounds simple. But a lot of cardholders run into problems they didn’t expect. They lose rewards they could have kept. They forget about subscriptions tied to the card. They don’t know what to do about a remaining balance.

If you’re trying to figure out how to close a Capital One credit card the right way, you’ve come to the right place. The process takes just a few minutes once you know the steps.

Below, we’ll walk you through everything, from what to do before you close to verifying the account is truly gone from your credit report.

Key Takeaways

This guide explains how to close a Capital One credit card, including preparing your account, redeeming rewards, handling balances and subscriptions, choosing a closure method, and understanding potential credit report and credit score effects.

Core Facts:

- Redeem all Capital One rewards before closing because closed, restricted, or delinquent accounts may lose access to unredeemed cash back, points, or miles.

- Closing a Capital One card does not eliminate debt; minimum payments remain due, interest continues accruing, and missed payments can still be reported to credit bureaus.

- Before closing your account, update recurring payments and subscriptions because merchants cannot automatically transfer charges to a different payment method.

- Capital One allows account closure online, by phone, by mail, or at a branch, with online closure available through the website rather than the mobile app.

- Closing a credit card reduces available credit, which can increase credit utilization and potentially affect your credit score depending on your overall credit profile.

- A Capital One account closed in good standing can remain on your credit report for up to 10 years, allowing positive payment history to continue contributing to your credit record.

Best for:

- Cardholders who want a step-by-step process for closing a Capital One credit card while avoiding lost rewards, missed subscriptions, or account-related issues.

- Consumers evaluating whether to close a credit card or use alternatives such as a product change, retention offer, or card lock feature.

- Anyone who wants to understand how closing a Capital One account may affect credit utilization, account history, and credit report reporting after closure.

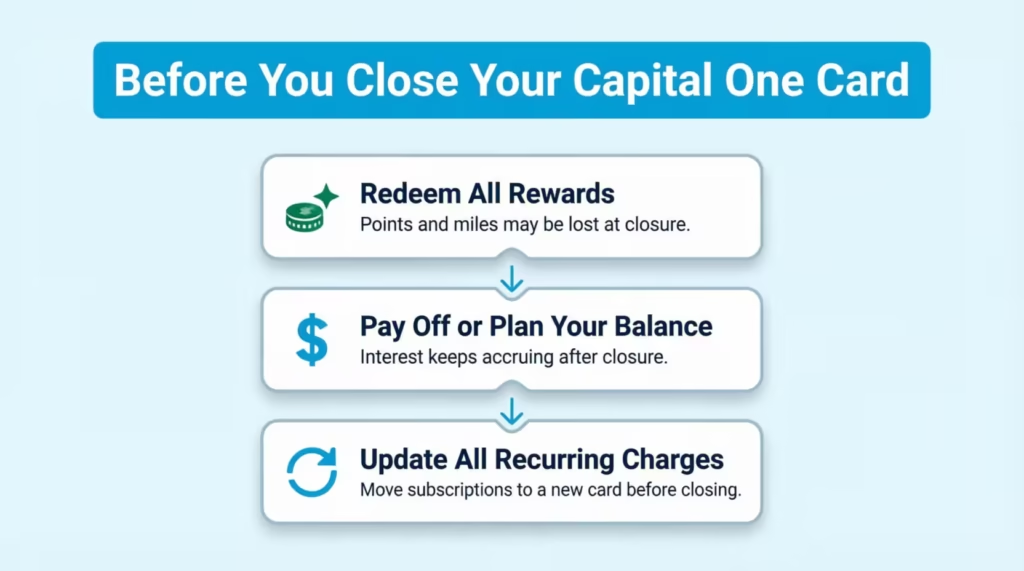

Steps to Take Before You Close Your Capital One Credit Card

Most people jump straight to canceling and figure out the rest later. That’s where things go wrong. Rewards disappear. Subscriptions get declined. Balances keep growing with interest on an account you thought was gone.

Completing these three steps first, in order, protects you from all of that. Think of them as your pre-flight checklist before the account goes dark.

How to Redeem Your Capital One Rewards Before Closing

Your rewards don’t automatically survive account closure. Capital One states that rewards don’t expire for the life of the account, but accounts that are closed, restricted, or delinquent may have different redemption options, or may lose unredeemed rewards entirely.

That means you need to redeem before you close, not after.

How you redeem depends on which card you have:

- Cash back cards (like Quicksilver or SavorOne): Redeem as a statement credit, check, or gift card directly from your online account.

- Miles cards (like Venture or Venture X): Transfer miles to a Capital One travel partner’s loyalty program, or redeem through Capital One Travel.

- If you hold multiple Capital One cards, you may be able to pool rewards from the card you’re closing into another active Capital One account, so they aren’t lost.

Log in to your account, go to the rewards section, and redeem or transfer every last point or mile before you take any steps toward closing. Once the account closes, what’s left is likely gone for good.

How to Handle Your Remaining Balance Before Closing

The ideal situation is a $0 balance before you close. Capital One will process a closure even if you still owe money, but that doesn’t mean the debt disappears. You’re still legally responsible for every dollar.

Here’s what happens if you close with a balance:

- Minimum payments are still due each month, on schedule.

- Interest keeps accruing on the unpaid balance.

- Late or missed payments still get reported to the credit bureaus.

If paying the full balance before closing isn’t possible right now, that’s okay, but go into the closure knowing you’ll need to keep making payments until it hits zero.

Also, don’t rely on just your most recent statement balance as your payoff number. Call Capital One or check your account for the exact payoff amount, because accrued interest can push the real total slightly higher than what your last statement showed.

How to Update Recurring Charges and Subscriptions

This is the step most people forget, and it’s the one that causes the most headaches afterward.

When your Capital One account closes, any merchant set to charge that card will get a decline. Capital One can’t forward those charges to a new card for you. The merchant won’t know why the payment failed. You’ll find out when a subscription gets cancelled or a utility sends a late notice.

Here’s how to handle it:

- Pull up your last two or three statements and look for any charge that repeats monthly or annually. Common ones include streaming services, gym memberships, insurance premiums, utility autopay, and phone plans.

- Log in to the Capital One mobile app and check the “expected transactions” feature, which flags recurring charges on your account.

- Go to each merchant’s website or app and update the payment method to a different card or bank account before you close.

Complete this step before you initiate closure. Once the account is closed, you won’t have easy access to transaction history, and some merchants may not notify you of a failed charge until the damage is already done.

⚠️ Mistake to Avoid: Don’t assume merchants will automatically update to a new card number. Capital One’s recurring transaction system can help you identify subscriptions, but it’s your responsibility to update each one directly with the merchant. Blocking a charge through Capital One’s app prevents it from going through but does not cancel the underlying subscription.

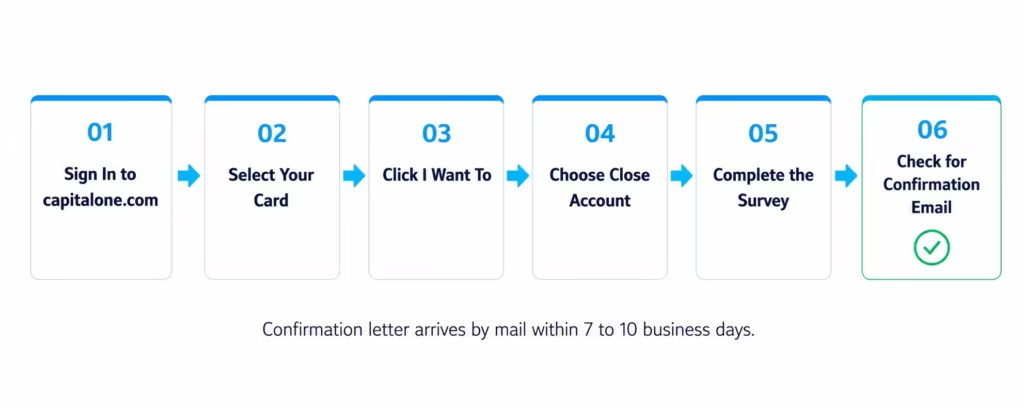

How to Close Your Capital One Card Online

Closing online is the fastest and most straightforward method Capital One offers. You can do it any time, without waiting on hold.

One important note first: online closure is available through the Capital One website, not through the mobile app. If you’ve been trying to find it in the app and can’t, that’s why. You’ll need to use a browser on your phone or computer.

Here’s the full process:

- Go to capitalone.com and sign in to your account.

- From your dashboard, find and select the card account you want to close.

- Click the “I want to…” button. It’s usually displayed next to a small gear icon.

- In the dropdown menu that appears, look under the “Control Your Card” section.

- Select “Close Account.”

- Follow the on-screen prompts. Capital One will typically walk you through a short survey asking why you’re closing, and may show you information through their CreditWise tool about how the closure could affect your credit score.

- Confirm your decision at the final step.

The account closes immediately once you complete the prompts. Look for a confirmation email from Capital One within a few minutes. Capital One also sends a written confirmation letter by mail, typically within 7 to 10 business days. Hold onto that letter. You’ll want it if you ever need to dispute anything on your credit report later.

💡 Pro Tip: Before you close, download your account statements from the past 12 to 24 months. Once the account closes, access to older statements may become limited or require a call to customer service.

How to Close Your Capital One Card by Phone

Calling is the right choice if you want real-time confirmation, have questions about your account, or simply prefer to speak with someone. It’s also the method where you’re most likely to receive a retention offer.

Capital One’s customer service number is 1-800-227-4825.

Before you call, have these ready:

- Your full credit card number

- Your account number (found in your online account or on a statement)

- The last four digits of your Social Security number for identity verification

Once you’re connected, a representative will verify your identity and then ask why you’re calling. When you say you want to close the account, expect a retention conversation. The rep will likely offer you something to keep the account open, such as a statement credit, a temporary annual fee waiver, or bonus points.

You don’t have to accept. A clear, polite statement works well here: something like, “I appreciate the offer, but I’ve made my decision to close the account. Can you please process the closure?” Stay consistent if they come back with a second offer. Most reps will move forward once you’ve declined twice.

Before you hang up, ask for two things:

- A confirmation number for the closure request.

- A written confirmation will be sent to your email or through Capital One’s secure message center.

Write down the confirmation number and the name of the representative you spoke with. If anything comes up later, these details will help you resolve it faster.

Other Ways to Close a Capital One Card

Online and phone are the two main closure methods. But if neither works for your situation, Capital One does offer two additional options.

Closing by Mail

A written request is the slowest method, but it does create a paper trail from your end.

Write a letter that includes:

- Your full credit card number

- Your account number

- Your signature

- A date by which you’d like the account closed

Mail it to:

Capital One Attn: General Correspondence PO Box 30285 Salt Lake City, UT 84130-0287

Allow extra processing time compared to online or phone. Once you’ve sent the letter, follow up by calling 1-800-227-4825 or checking your online account to confirm the closure was processed. Don’t assume the account is closed until you have confirmation.

Closing in Person at a Capital One Branch

If you’d rather handle this face-to-face, you can visit a Capital One branch and request closure at the counter. Bring a valid photo ID and the card you want to close. A branch representative can process the request directly and confirm the closure before you leave.

Use the branch locator on capitalone.com to find the nearest location.

What Happens If You Close Your Capital One Card with a Balance

Some cardholders need to close their account before they’ve paid it off. That’s understandable. But it’s important to know exactly what you’re agreeing to when you do.

Capital One will close the account even with an outstanding balance. The account stops accepting new charges. But the debt doesn’t go away.

Here’s what continues after closure:

- You still owe the full remaining balance. Closing the account is not a debt settlement or forgiveness. The obligation is unchanged.

- Minimum monthly payments are still due. Capital One will still send statements, and payments must be made on schedule.

- Interest keeps accruing. The card’s APR still applies to whatever you owe until the balance reaches zero.

- Late payments still get reported to the credit bureaus. A closed account has no special protection. If you miss a payment, it shows up on your Equifax, Experian, and TransUnion reports just like it would on an open account.

The stakes escalate if payments stop entirely. After roughly 120 to 180 days of non-payment, Capital One may charge off the account. A charge-off is reported to all three credit bureaus and causes serious, lasting damage to your credit score. The debt may also be sold to a collections agency at that point, which creates a separate negative entry on your report.

The practical recommendation: If you can’t pay the balance to zero right now, stay current on minimum payments after closure until the account is fully paid. Treat it like any other debt obligation. The account being closed doesn’t change your repayment responsibility.

How Closing a Capital One Card Affects Your Credit Score

This is the section most readers want to skip to first. The honest answer is that closing a card can lower your credit score, but the impact depends on your specific situation, and it’s rarely permanent.

There are two main credit score factors affected by closure. Understanding each one helps you prepare and minimize the damage.

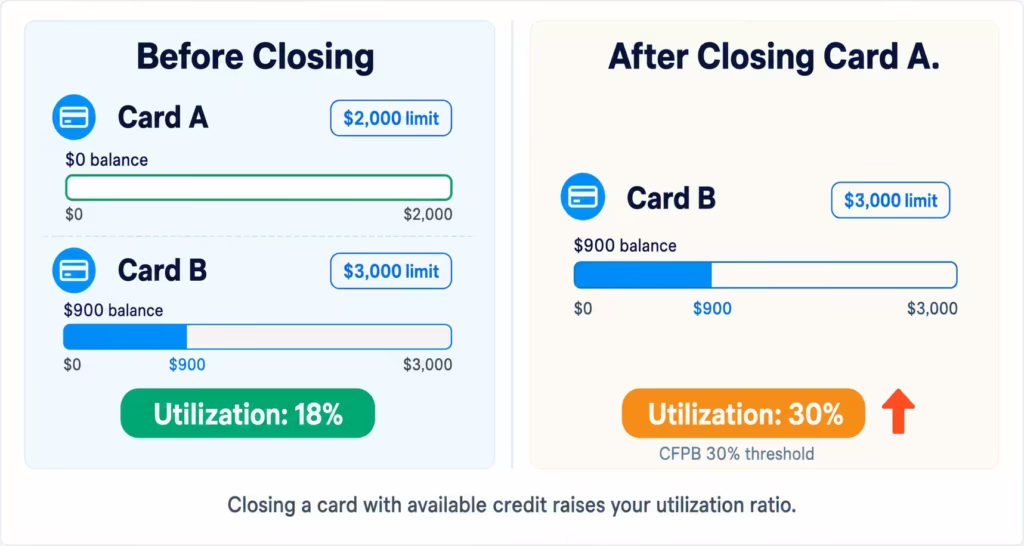

How Closure Affects Your Credit Utilization Ratio

Credit utilization is the ratio of your total credit card balances to your total available credit, expressed as a percentage. The Consumer Financial Protection Bureau recommends keeping utilization below 30% of your available credit to avoid a negative impact on your scores.

When you close a card, you lose that card’s credit limit. Your available credit goes down. If your balances elsewhere stay the same, your utilization ratio goes up.

Here’s a concrete example:

- Before closure: You have two cards. Card A has a $2,000 limit with a $0 balance. Card B has a $3,000 limit with a $900 balance. Total available credit: $5,000. Total balance: $900. Utilization: 18%.

- After closing Card A, the total available credit drops to $3,000. Total balance is still $900. Utilization rises to 30%, right at the CFPB threshold.

- If Card A had a $1,000 limit instead, Utilization would jump to 45%, well above the recommended level.

The size of the impact depends entirely on how much of your total available credit the closed card represents. If the card you’re closing has a high credit limit and you carry balances on other cards, the utilization spike can be significant.

One way to soften this: Pay down balances on your other cards before closing. Reducing what you owe elsewhere keeps your utilization lower even after you lose the closed card’s available credit.

How Closure Affects Your Length of Credit History

Both FICO and VantageScore consider two age-related factors: the age of your oldest account and the average age of all your accounts. Older is better on both measures.

Here’s the nuance that most articles get wrong: closing an account doesn’t instantly erase its history. A Capital One account closed in good standing can remain on your credit report for up to 10 years. During that entire period, it continues to contribute to your credit history length. The hit to your average account age comes from losing an active account from the calculation, but the closed account’s positive payment record doesn’t vanish overnight.

The situation that causes the most damage is closing your oldest active account. If that Capital One card is the most senior card in your wallet, think carefully before closing it.

Once the closed account eventually drops off your report after 10 years, your average account age may decrease again. That’s a downstream effect worth knowing about, even if it’s years away.

📌 Did You Know: A closed account in good standing can stay on your credit report for up to 10 years. That means its positive payment history keeps working in your favor long after you’ve closed it.

Alternatives to Closing Your Capital One Card

Closing isn’t always the right move. In many cases, the problem the reader wants to solve, usually an annual fee that’s hard to justify or a card they’re no longer using, has a better solution that doesn’t involve the credit score consequences of full closure.

Consider these three options before you make the final call.

Request a Product Change (Downgrade to a No-Fee Card)

A product change is Capital One’s term for switching your existing card to a different card in their lineup, without opening a new account or closing the old one. It’s also sometimes called an upgrade or downgrade, depending on the direction.

Here’s why this matters: when you do a product change, your account number, credit limit, and account history all stay exactly the same. There’s no hard inquiry on your credit. Your average account age is unaffected. You keep your available credit. The only thing that changes is the card’s benefits and annual fee.

For most people who want to eliminate an annual fee, this is the superior option.

For example, if you have the Capital One Savor card with a $95 annual fee and you’re not using the dining rewards enough to justify it, you may be able to downgrade to the SavorOne, which has no annual fee and a similar rewards structure. The account stays open. Your credit score is protected.

How to request a product change:

- Log in to your Capital One account and look under “More Account Services,” then “View Offers and Upgrades.” If Capital One has pre-approved you for a different card, you’ll see the offer here.

- If no offer appears, call the number on the back of your card and ask the representative to speak with the retention or product change team. Tell them you’re considering closing due to the annual fee and ask what downgrade options are available.

One important trade-off: a product change typically doesn’t qualify you for a new cardholder bonus. If you want to earn the welcome offer on a different card, you’d need to apply separately. But if your goal is simply to keep the account open without paying the annual fee, a product change does exactly that.

Lock Your Card Instead of Closing It

If the card you’re thinking about closing has no annual fee, closing it may not be necessary at all.

Capital One allows you to lock your card directly from the mobile app. A locked card can’t be used for new purchases. It still shows up as an open account on your credit report. It still contributes to your available credit and account age. You just can’t spend on it.

This works well if you’re worried about accidental spending or simply don’t want to use the card anymore. You can unlock it at any time with the same few taps.

One thing to keep in mind: if you lock a card and never use it, Capital One may eventually close it for inactivity. To prevent that, consider setting up one small recurring charge, like a $5 or $10 monthly subscription, on the locked card and then unlocking it briefly each month to confirm the charge went through. This keeps the account active without requiring much attention.

Ask for a Retention Offer Before You Decide

Before you close, it costs nothing to ask whether Capital One will offer you something to stay. Retention offers are real, and they can sometimes change the math enough to make keeping the card worthwhile.

Call the number on the back of your card and tell the representative that you’re thinking about closing because the annual fee doesn’t feel worth it anymore. From there, you may receive an offer for a statement credit, a temporary fee waiver, or bonus points.

If the offer covers a meaningful portion of the annual fee, or adds value that makes the card worth keeping for another year, that’s a legitimate reason to hold off on closing. If the offer doesn’t move the needle, you can decline and proceed with whatever you’ve decided.

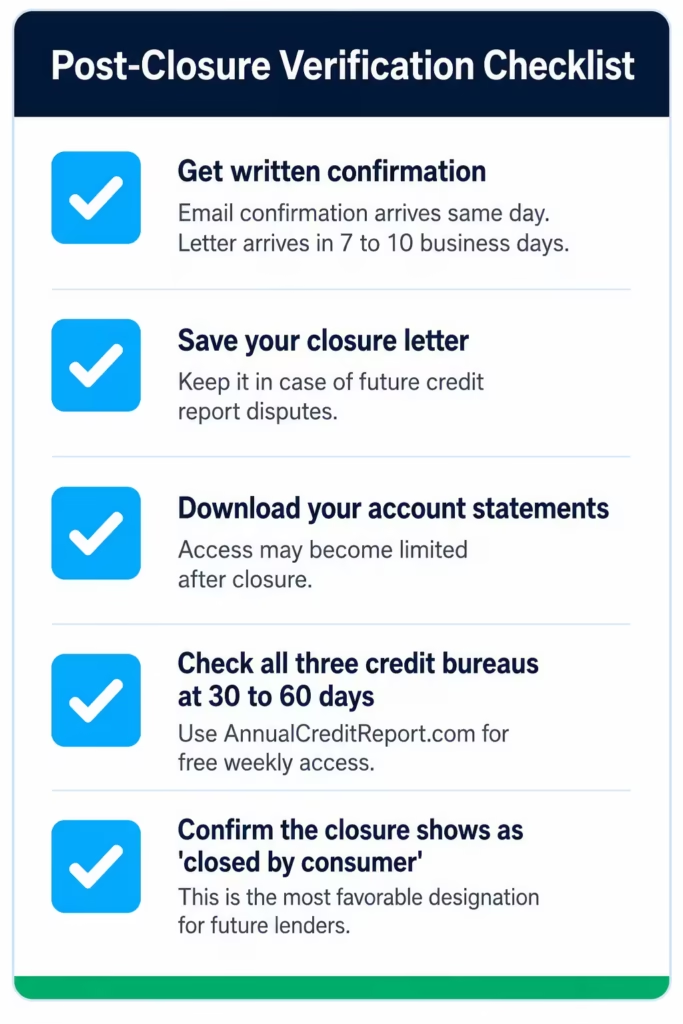

How to Confirm Your Capital One Account Is Closed

Closing the account is step one. Confirming it actually closed, and that it’s reported correctly on your credit file, is step two. Most people skip this part. That’s a mistake.

Start with the confirmation you receive during the closure process itself. If you closed online, check your email for a confirmation message from Capital One. If you closed by phone, you should have a confirmation number and a rep’s name. Capital One also sends a written confirmation letter by mail within 7 to 10 business days. Keep that letter somewhere safe.

If you don’t receive an email confirmation within a few hours or the letter doesn’t arrive within two weeks, call Capital One to verify the account status. Don’t assume the closure has been processed just because the online steps have been completed.

Checking Your Credit Report After Closure

Around 30 to 60 days after closing, pull your credit reports from all three bureaus: Equifax, Experian, and TransUnion. The most convenient way to do this for free is through AnnualCreditReport.com, which provides free weekly access to all three reports.

When you find the Capital One account on each report, check for three things:

- Account status: It should show as closed.

- Balance: It should show $0 if you paid it off, or the remaining balance you still owe.

- Closure designation: Look for language like “closed by consumer” or “account closed at consumer’s request.” This is the most favorable designation.

If the report shows “closed by issuer” and you initiated the closure yourself, that’s worth disputing. A closure marked by the issuer can signal to future lenders that Capital One chose to close the account, which looks different from a voluntary consumer closure.

To dispute an error, contact the relevant credit bureau directly with your written closure confirmation from Capital One as supporting documentation. Each bureau, Equifax, Experian, and TransUnion, has its own online dispute process.

You can also use CreditWise from Capital One to monitor your score and credit report changes after closure. The tool is free and doesn’t require a Capital One card to use.

How Long the Closed Account Stays on Your Credit Report

A Capital One account closed in good standing typically stays on your credit report for up to 10 years. During that entire window, the positive payment history attached to the account continues to factor into your credit score calculations.

That’s actually good news. It means the years of on-time payments you built up don’t vanish the moment you close the card.

After 10 years, the account drops off entirely. At that point, the average age of your remaining accounts may decrease, which could nudge your score down slightly. It’s a downstream effect and not something to stress about now, but it’s worth knowing so it doesn’t catch you off guard later.

One caveat: Capital One has the discretion to stop reporting a closed account earlier than 10 years. This is uncommon, but it does happen. If that account is important to your credit history length, keep an eye on it through your annual credit report pulls.

Frequently Asked Questions (FAQs)

What is the highest balance I should have on a $3,000 credit card?

Keep your balance at or below $900 on a $3,000 limit card. That keeps your credit utilization at 30%, which is the threshold the Consumer Financial Protection Bureau recommends to avoid a negative impact on your credit score.

What happens when you close a credit card with a $0 balance?

Closing a card with no balance still reduces your total available credit, which raises your credit utilization ratio on other cards. It can also lower the average age of your accounts, so a zero balance doesn’t protect your credit score from the effects of closure.

Will Capital One close my account if I don’t use it?

Yes, Capital One can close a card due to inactivity, though they typically contact the cardholder first. To prevent this, set up a small recurring charge on the card, like a low-cost subscription, to keep the account active.

How much will my credit score drop if I close a credit card?

There’s no fixed number because the impact depends on your total available credit, the balances you carry on other cards, and the age of the account you’re closing. A card with a high limit or a long history will generally cause a larger drop than a newer, lower-limit card.

Is it better to close a credit card or leave it open with a zero balance?

Leaving it open is usually better for your credit, because an open card with a $0 balance lowers your utilization ratio and keeps your account age intact. If the card has an annual fee you can’t justify, downgrading to a no-fee version preserves both benefits without the cost.

Why is it not a good idea to close a credit card?

Closing a card reduces your total available credit and raises your utilization ratio, both of which can lower your credit score. If the card has no annual fee, keeping it open costs nothing and continues to support your credit history.

Can you turn off your Capital One credit card without closing it?

Yes. Capital One’s card lock feature lets you block all new purchases with a few taps in the mobile app, while keeping the account open and active on your credit report. You can unlock it just as easily whenever you want to use it again.

What is worse, closing a credit card or not using it?

Not using it is generally better than closing it, because an open, unused card still contributes to your available credit and account age. Closing it removes both, which can raise your utilization ratio and shorten your credit history.

Can I reopen a Capital One credit card after I close it?

No. Capital One account closures are final, and accounts cannot be reopened, regardless of how recently they were closed. If you want access to a Capital One card again, you would need to submit a new application.

What happens to authorized users when I close my Capital One card?

Authorized users lose access to the card immediately when the account closes. The account’s payment history may no longer appear on their credit reports, so if the card was helping build an authorized user’s credit, closure removes that benefit.

Bottom Line

Closing a Capital One credit card the right way takes more than a single click or phone call. It means redeeming your rewards first, handling your balance, updating every subscription, and then verifying the closure actually shows up correctly on all three credit reports.

Based on the credit score mechanics covered here, the most effective approach for anyone whose main concern is the annual fee is to request a product change first. It eliminates the fee without touching your credit history or utilization.

If closing is the right call for you, this guide gives you everything you need to do it cleanly. Share this with anyone juggling multiple credit cards who might be weighing the same decision.