If you’re wondering how to increase the credit limit on your Capital One secured card, you’re not alone. A $200 starting limit can feel tight fast. It can block everyday purchases, push your utilization too high, and slow down the credit-building progress you’re working toward. Many cardholders search for a “request credit limit increase” button online and come up empty, which only adds to the confusion.

The good news: there are real paths to a higher limit. They just work differently from a standard credit card.

In this guide, we’ll explore all your options. We’ll cover the 35-day deposit window after approval, the automatic 6-month review, and more. We’ll also discuss what disqualifies you, how to graduate to an unsecured card, and what you should do now to prepare for success.

Key Takeaways

This guide covers two paths to increasing your Capital One secured card limit: depositing extra funds during the 35-day pre-activation window and qualifying for the automatic 6-month credit review.

Core Facts:

- Capital One does not offer a manual credit limit increase request for secured cards. The option does not exist in the app or online portal for either the Platinum Secured or the Quicksilver Secured.

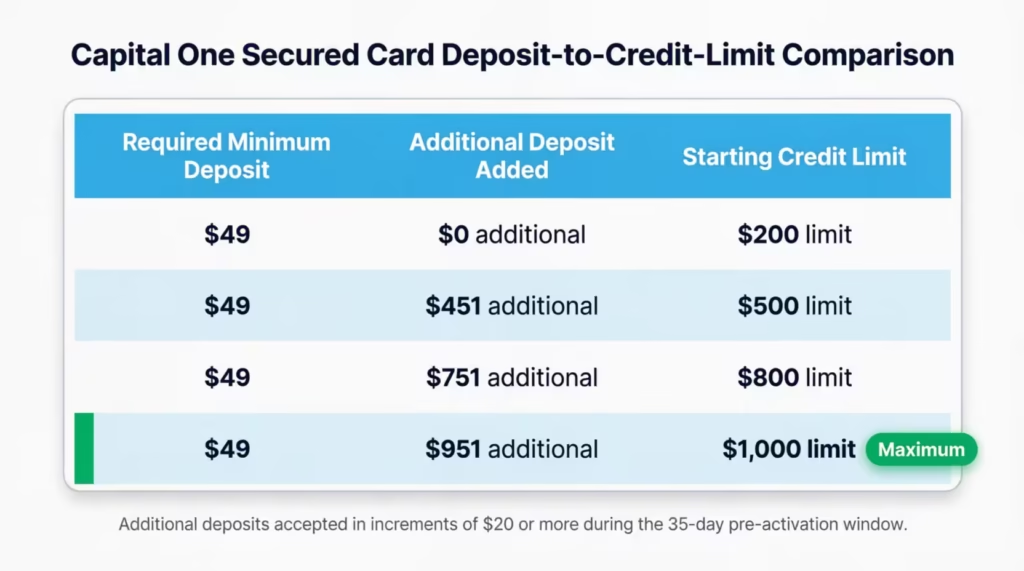

- Before activating the card, cardholders have up to 35 days from their approval date to deposit additional funds and raise their starting credit line up to the $1,000 maximum. The 35-day clock starts on approval, not card arrival.

- After 6 months, Capital One automatically reviews the account for a potential credit line increase using a soft credit pull, which does not affect the cardholder’s credit score.

- Capital One reviews the full credit report at the 6-month mark, so a late payment on any other account during that period can block an increase even with a perfect secured card payment record.

- A credit limit increase raises the spending limit while keeping the deposit with Capital One. Card graduation converts the account to unsecured and returns the full security deposit.

- Reviews run no more than once every 6 months. If Capital One reviewed the account recently with no increase granted, the next cycle will not begin for another 6 months.

Best for:

- New cardholders still within the 35-day pre-activation window who want to start with the highest possible credit line before the funding window closes permanently.

- Cardholders at or past the 6-month mark who want to understand why an automatic increase did not arrive and what to address before the next review cycle.

- Anyone building credit who wants to understand how their secured card limit directly affects their credit utilization ratio and monthly score reporting.

Can You Request a Credit Limit Increase on a Capital One Secured Card?

The short answer is no. Capital One does not offer a manual credit limit increase request for secured credit cards. If you go looking for that option in the app or online portal, you won’t find it. That’s not a glitch. That’s by design.

This applies to both the Capital One Platinum Secured and the Capital One Quicksilver Secured. Neither card supports the kind of request you can make on an unsecured Capital One card, where you fill out a short form, provide income details, and get a decision.

That said, you’re not stuck at $200. There are two ways to get a higher limit. The first is available only before your card is activated. The second kicks in after six months of account use. Both are covered in detail in the sections below.

Why Secured Cards Work Differently Than Unsecured Cards

With a secured card, your security deposit is what sets your credit limit. Capital One holds that deposit as collateral against what you spend. On the Capital One Platinum Secured, a $49, $99, or $200 deposit gives you a $200 credit line. On the Quicksilver Secured, your deposit equals your limit dollar for dollar.

Since the deposit and limit are linked, Capital One can’t raise your limit without changes on their side or yours. You either put in more money, or you demonstrate enough responsible behavior that they’re willing to extend more credit beyond your deposit. That second path takes time. But it’s real, and it’s the foundation of how this card is designed to work.

How to Increase Your Limit Before the Card Is Activated: The 35-Day Deposit Window

This is the one option most new cardholders don’t know about, and it’s also the most powerful. Right after you’re approved, Capital One gives you a 35-day window to fund your account. During that window, you can deposit more than your required minimum to lock in a higher starting credit line immediately.

The 35-day clock starts on your approval date, not the date your card arrives in the mail. That distinction matters. Cards sometimes take 7 to 10 days to arrive, which means your window may be partly used before you even open the envelope.

To make it concrete: say Capital One assigned you a required minimum deposit of $49. If you deposit $449 more during the funding window, your starting credit line becomes $498. If you put in the full $951 beyond your minimum, your limit reaches the maximum of $1,000. The additional deposit raises your limit by exactly the amount you put in.

Deposits can be made online through your Capital One account, by phone, or in installments of at least $20. Capital One notes it can take up to 7 to 10 business days for the additional deposit to clear and for the higher credit limit to be established.

Once you activate the card, this window closes permanently. There is no way to reopen it or make a late additional deposit after activation.

⚠️ Mistake to Avoid: Don’t activate your card the same day it arrives if you haven’t yet decided whether to put in extra funds. Review your finances first, then fund the account to the level that fits your goals, and activate afterward. Once the card is active, the deposit window is gone.

What Happens to the Extra Deposit You Put In

Any deposit you make, whether it’s the required minimum or an amount above it, is held as collateral while your account is open. It’s not spent or applied toward purchases. Capital One holds it in full.

When your account is eventually closed in good standing or when the card graduates to an unsecured card, the entire deposit is returned to you. No portion is forfeited for depositing more than the minimum. There are also no extra fees for putting in a larger amount.

How Capital One’s Automatic Credit Limit Review Works After 6 Months

After your account has been open for six months, Capital One begins reviewing it for a potential credit line increase. This review is automatic. You don’t have to request it, call in, or fill out a form. Capital One runs it on its own schedule.

If the review results in an increase, something important happens: you don’t need to put in more deposit money to get it. Capital One extends the additional credit beyond your deposit amount, which means your card becomes partially unsecured for that incremental amount. It’s a meaningful shift, even if the limit increase itself is modest.

Capital One does not publish the exact increase amount in advance. It varies by account and is determined by their internal review criteria. Some cardholders see an increase from $200 to $500. Others see smaller bumps. The amount is entirely at Capital One’s discretion.

Reviews happen no more than once every six months. If you receive an increase at the six-month mark, the next potential review won’t begin until at least six months after that.

Capital One uses a soft credit inquiry during these automatic reviews. A soft pull does not affect your credit score. If an increase is granted, you’ll be notified in the app or by mail. No action is required on your end to receive it.

What Capital One Evaluates During the Automatic Review

Capital One doesn’t publish a full checklist, but based on their stated policies and how credit reviews typically work at major issuers, the review looks at several factors.

- Payment history on the secured card: Even one late payment within the first six months can disqualify you for that review cycle.

- Late payments on any other credit account: Capital One checks your full credit report, not just your activity on this card. A missed payment to another issuer during the review period is a red flag.

- Credit utilization ratio: Consistently carrying a balance close to your $200 limit signals financial stress. Keeping utilization low shows restraint.

- Card usage frequency: A dormant card gives Capital One less evidence to evaluate. Regular, low-balance usage is the signal they’re looking for.

- Income and employment status: The information you provided when you applied is still on file. If your income has increased, updating it can help.

Why You Might Not Get an Automatic Increase Even After Paying on Time

This is the part that frustrates a lot of cardholders. Six months go by. Every payment is on time. Then nothing happens.

Paying on time on this card is necessary. But it’s not enough on its own. Capital One reviews your entire credit profile, not just what’s happened on this one card. Any of the following can result in a denial, even with a clean payment record on the secured card:

- A late payment on another account: If your car payment, student loan, or another credit card shows a delinquency during the review period, Capital One will see it. That’s often enough to hold the increase.

- High credit utilization on this card: Carrying a balance consistently above $60 to $70 on a $200 limit, which puts utilization at 30 to 35 percent or more, sends a risk signal. Issuers want to see that you don’t rely heavily on the credit you already have.

- Minimal card activity: If you’ve barely used the card, Capital One has little evidence to support extending more credit. Zero-balance months don’t necessarily help. Using the card regularly and paying it off does.

- The account hasn’t reached six months yet: Accounts under six months old simply aren’t eligible, regardless of how well they’ve been managed.

- Too many recent hard inquiries: Applying for several new credit accounts in the months before the review adds risk signals to your credit profile.

- A review happened in the past six months: If Capital One already reviewed your account, even if no increase was granted, the next review cycle won’t begin until another six months have passed.

📌 Did You Know? Capital One looks at your full credit report during the automatic review, not just your activity on the secured card. A single missed payment on an unrelated account, like a phone bill or auto loan, can be enough to pause an otherwise clean review.

What to Do If 6 Months Have Passed With No Increase

If your six-month mark has come and gone without any change to your credit limit, don’t close the account. That would hurt your credit score by removing available credit and shortening your credit history. Instead, take a few focused steps.

Start by checking your credit report for derogatory marks on other accounts. If there’s a late payment or collection account on your report that appeared during the past six months, that’s likely what blocked the increase. You can challenge errors with the credit bureau directly. Also, paying down or settling overdue accounts can boost your standing for the next review.

Next, look at how you’ve been using the secured card itself. If your balance has been consistently high relative to the $200 limit, work on keeping it below 30 percent, ideally below 10 percent in the month before a review. If you hardly use the card, start with small, regular purchases. Try a monthly streaming service or a utility bill. Then, pay the balance in full each month.

You can call Capital One’s customer service number to ask whether your account was reviewed and what the outcome was. They won’t always share specific reasons, but some representatives will confirm whether a review occurred and whether anything in your file is flagged for attention. This can help you identify what to fix.

Finally, avoid applying for new credit in the months leading up to your next expected review window. Hard inquiries from new applications signal credit-seeking behavior, which can work against you during the evaluation.

The Difference Between a Credit Limit Increase and Card Gradation

These two outcomes are often used interchangeably online, but they’re not the same thing. Understanding the distinction matters because they have different implications for your deposit and your account.

A credit limit increase means Capital One raises your spending limit on the existing secured card. Your deposit stays with Capital One. Your card remains a secured card. Your account number doesn’t change. Nothing is returned to you. You simply have more room to spend and a lower utilization ratio.

Graduation is different. It’s when Capital One converts your secured account into a traditional unsecured credit card. Your security deposit is returned. The card is no longer collateralized. You may or may not receive a higher limit at the time of graduation, but the card now functions like a standard unsecured card going forward.

These events can happen independently. You might receive a credit limit increase at the six-month mark without graduating. Graduation might happen a year or more later. Some accounts receive graduation without ever having received an intermediate limit increase.

Capital One makes both decisions through its own internal review process. Neither can be triggered or requested by the cardholder. Graduation notifications are sent by mail. According to Capital One’s own help center, upgrades happen automatically when your account becomes eligible, and your card can’t be upgraded by request.

How Capital One Decides When to Graduate Your Account

Capital One periodically reviews secured card accounts for graduation eligibility. There is no fixed published timeline for when this happens. Some cardholders report graduation after 12 to 18 months. Others wait longer. The timing depends on your overall credit profile, not just your behavior on this one card.

The factors for graduation are like those in the credit limit review. They include consistent on-time payments, low utilization, regular card use, and a credit report without new delinquencies.

If Capital One determines your account qualifies, the upgrade happens automatically. You’ll receive a notification by mail, and your account will be converted with no action required on your end.

What Happens to Your Security Deposit After Graduation

When your account graduates to unsecured status, Capital One returns your full security deposit. This typically appears as a statement credit on your next bill, though it can also come as a check or electronic refund depending on how you originally funded the deposit.

The return can take a few weeks to process. You can check whether it’s been applied by logging into your account online or looking at your next statement. If your account is ever closed in good standing before graduation, the deposit is also returned at that time, minus any outstanding balance you owe.

How a Higher Credit Limit Helps Your Credit Score

Getting a higher limit on a secured card isn’t just about having more room to spend. It has a direct effect on your credit score through something called your credit utilization ratio.

Credit utilization is the second most important factor in the FICO scoring model, accounting for roughly 30 percent of your score. It’s the percentage of your available credit that you’re currently using. FICO’s own credit education materials indicate that keeping utilization below 30 percent is generally recommended, with lower being better for score optimization.

On a $200 credit limit, the math works against you fast. A $70 purchase puts you at 35 percent utilization. A $100 balance puts you at 50 percent. Both are in ranges that can pull your score down, even if you pay the full balance every month. The problem isn’t the spending. It’s the limit being too low to make the ratio look healthy.

Now consider the same $70 purchase on a $500 limit. That’s 14 percent utilization. On a $1,000 limit, it drops to 7 percent. The spending hasn’t changed. But the signal your score receives is dramatically different.

Capital One reports your payment activity and balance to all three major credit bureaus: Equifax, Experian, and TransUnion. This happens every month. Every on-time payment builds your payment history, which carries 35 percent of your FICO score. And every month your utilization sits low, your score gets the benefit of both factors working in your favor at once.

Using Capital One CreditWise to Track Your Progress

Capital One offers a free credit monitoring tool called CreditWise. It’s available through the Capital One mobile app and at creditwise.capitalone.com. What makes it worth using is that it’s open to anyone, including non-Capital One customers, and it doesn’t require a credit card to access.

CreditWise shows your current credit score, the key factors affecting it, and how changes to your behavior might impact your score over time. It also alerts you to significant changes on your credit report, which is useful for spotting potential issues that could affect your next automatic review.

If you’ve been wondering why your score isn’t climbing despite paying on time, CreditWise can often surface the reason, whether it’s high utilization, a derogatory mark on another account, or a thin credit history. Checking it monthly takes two minutes and gives you an early signal before Capital One runs its next review.

The Behaviors That Position You for a Credit Limit Increase

Getting a higher limit on a Capital One secured card is less about doing one big thing right and more about consistently doing several small things right, over time. The habits below matter across every stage of your account lifecycle.

- Pay on time, every month. This is the single most important habit. Even one late payment can reset your eligibility for the automatic review cycle. Set up autopay for at least the minimum payment as a safety net, even if you plan to pay in full each month.

- Keep utilization low on this card. Try to keep your balance below 30 percent of your credit limit. Below 10 percent is better for FICO score purposes. On a $200 limit, that means keeping your statement balance under $20 to $40 ideally. Pay the card off fully each month if you can.

- Use the card regularly. A dormant card gives Capital One nothing to evaluate. Small, recurring purchases that you pay off each month are the ideal usage pattern. Think subscription services, a gas fill-up, or groceries once a week.

- Keep your other accounts current. Capital One reviews your full credit report, not just this card. Pay every other bill on time, too. A missed car payment or a collection account on a medical bill can stall your review outcome, even if this card is perfect.

- Avoid applying for new credit before a review. Each new credit application generates a hard inquiry. Multiple hard inquiries in a short window can signal financial instability. Hold off on new applications for two to three months before you expect your six-month review.

- Update your income with Capital One if it has increased. Income is a factor in credit decisions. If you’ve gotten a raise or changed jobs since you applied, updating your profile can improve the picture Capital One sees.

A 3-Stage Action Timeline From Approval to Graduation

Where you are in your account lifecycle determines what actions are available to you right now. Use this timeline to find your current stage and focus on what matters most.

- Days 1 to 35: Before Activation

- Decide whether to deposit more than your required minimum. Up to $1,000 total is allowed.

- Fund the account at your chosen level before activating the card.

- Allow 7 to 10 business days for additional deposits to clear.

- Activate the card only after your funding is complete.

- Months 1 to 6: Building Your Review Profile

- Pay your bill on time every month. Even one late payment can affect the six-month review.

- Use the card regularly at low balances. Keep utilization under 30 percent.

- Pay off the balance in full when possible to avoid interest charges.

- Keep all other credit accounts current. Capital One will check the full report.

- Monitor your credit score monthly using CreditWise or another free service.

- Month 6 and Beyond: Review Window and Graduation Path

- Continue all the habits from Stage 2. They don’t stop at month six.

- Capital One’s automatic review runs on its schedule. You won’t be notified that it’s happening.

- If no increase arrives, review your credit report for issues and maintain the habits above for the next six-month cycle.

- Graduation to an unsecured card may come at any point. You’ll receive a mail notification when it does.

💡 Pro Tip: If you’re in Stage 2, consider setting your card’s autopay to the full statement balance each month. This ensures you never miss a payment, you never carry interest charges on a 29.99% APR card, and your utilization shows up near zero to the bureaus. It’s the single habit that does the most work for your review eligibility.

Frequently Asked Questions (FAQs)

Can I increase my Capital One secured card limit?

You cannot request a limit increase directly. Your only two options are depositing extra funds during the 35-day window before you activate the card or waiting for Capital One’s automatic review at the 6-month mark.

How do I get a $1,000 credit limit on a Capital One secured card?

Within 35 days of approval and before activating your card, deposit up to $1,000 total into your account. The additional deposit raises your starting credit line dollar for dollar up to the $1,000 maximum.

Will paying on time for 6 months guarantee a credit limit increase on a Capital One secured card?

No. On-time payments are required but not sufficient on their own. Capital One reviews your full credit report, so a late payment on any other account, such as a car loan or utility bill, can block the increase even if this card is perfect.

What’s the highest credit limit Capital One will give on a secured card?

The maximum credit limit on a Capital One secured card is $1,000. You reach it by depositing that full amount during the 35-day pre-activation funding window.

Can I put $10,000 on a Capital One secured credit card?

No. The Capital One Platinum Secured and Quicksilver Secured both cap the total deposit at $1,000, which is also the maximum credit line. Any deposit above that amount is not accepted.

How many times will Capital One increase your credit limit on a secured card?

Capital One reviews your account for a potential increase no more than once every 6 months. There is no stated cap on the total number of increases, but each review cycle requires another 6-month wait regardless of the outcome.

What is the difference between a credit limit increase and card graduation on a Capital One secured card?

A credit limit increase raises your spending limit while your card stays secured and your deposit stays with Capital One. Graduation converts your account to an unsecured card and returns your full security deposit, which can happen independently of any prior limit increase.

Does Capital One notify you before running the automatic 6-month review?

No. Capital One runs the review on its own schedule without notifying you in advance. If an increase is approved, you will receive a notification in the mobile app or by mail after the decision is made.

What happens to my security deposit if Capital One increases my credit limit?

Your deposit stays with Capital One and is not returned. A credit limit increase extends additional credit beyond your deposit amount, making part of the card unsecured, but the deposit itself is only returned when the account graduates to an unsecured card or is closed in good standing.

Bottom Line

Increasing your credit limit on a Capital One secured card takes patience, but the path is clear. If you’re still within the 35-day funding window, depositing more before you activate the card is the fastest way to start with a higher limit. After activation, the automatic six-month review is the primary path, and it rewards consistent on-time payments, low utilization, and regular card use across all your accounts.

Based on how Capital One structures these reviews, the most effective approach is to treat every billing cycle as a building block. Your deposit comes back at graduation. Your credit score improves with every low-utilization, on-time month. Both outcomes are within reach if you stay consistent.

If you know someone who just got approved for a Capital One secured card, share this guide with them. The 35-day deposit window is the most time-sensitive thing most new cardholders never find out about in time.