I get why you’re here. You’ve had your Capital One Venture card for a while, and you want more room to spend or a better credit utilization ratio. But you’re worried that asking for a Capital One Venture credit limit increase could ding your score or end in a denial. That’s a fair concern, and it’s a question I’ve helped many cardholders think through.

The good news is simple: Capital One uses a soft inquiry to review most credit limit increase requests, so asking does not hurt your credit score.

Below, we’ll walk through the exact steps, the eligibility rules, what income to report, and what to do if you get turned down.

Key Takeaways

This guide explains how to request a credit limit increase on a Capital One Venture card, including the soft-pull policy, eligibility timing, income reporting rules, and what to do after a denial.

Core Facts:

- Capital One uses a soft inquiry for Venture credit limit increase requests, so asking does not affect your credit score, except in rare cases requiring deeper account review.

- You can request a credit limit increase once every six months, counted from your account opening date or your most recent increase.

- Secured Venture-related accounts and authorized users or co-applicants are not eligible to request a credit limit increase.

- Report your gross annual income before taxes, not take-home pay, and you may include household income if you are 21 or older with reasonable access to it.

- Online and phone requests often receive a decision immediately, though some requests go to manual review and take a few business days.

- Common denial reasons include low card usage, a recent late payment, an account under six months old, or income too low for the requested limit.

Best for:

- Capital One Venture cardholders who want a higher limit but are unsure if requesting one will hurt their credit score.

- Cardholders who have held the Venture card for at least six months with a clean payment history and want to time their request strategically.

- Anyone whose recent credit limit increase request was denied and wants to understand the next steps.

Does Requesting a Credit Limit Increase Hurt Your Credit Score?

This is the first worry most cardholders have, and the answer is clear. Capital One uses a soft inquiry when reviewing credit limit increase requests on the Venture card. A soft pull does not affect your credit score in any way. It only shows on your personal credit report, and lenders cannot see it.

That’s different from a hard pull, which is what happens when you apply for a new card or a loan. A hard inquiry can shave a few points off your FICO score and stay on your report for two years. With a Capital One credit line increase request, that does not happen.

It’s also worth noting that this is a Capital One policy, not a universal rule. Other card issuers, like some banks, still use a hard pull when you ask for more credit. So a tip that works for one card may not work for another. As Capital One’s official help center states, “Requesting a credit increase won’t impact your credit score because we use soft inquiries for credit limit increase requests.”

There is one rare exception to keep in mind. If your account needs a deeper review for some reason, Capital One may need to look more closely at your file. In a very small number of cases, that could trigger a hard pull. This is not the norm, but it’s honest to mention it so you know what to expect.

💡 Pro Tip: Even though the request itself is a soft pull, do not apply for a new credit card the same week. A new card application is a hard pull, and it can lower your odds of approval for the limit increase.

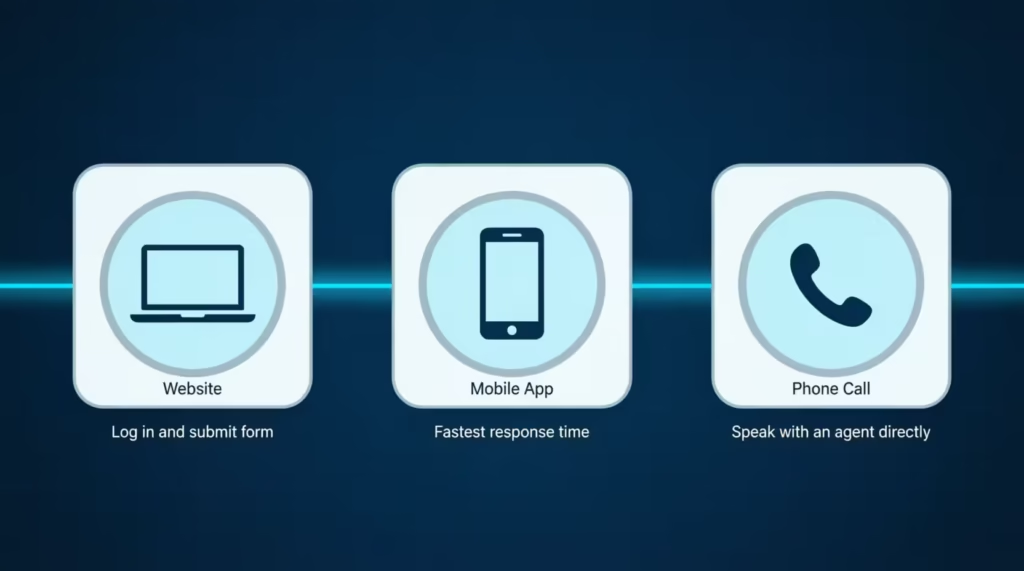

How to Request a Credit Limit Increase on Your Venture Card

You have three ways to ask for more credit on your Venture card: the Capital One website, the Capital One mobile app, and a phone call. All three lead to the same review process. Pick the one that feels easiest for you.

The fastest channel for most people is the app or website. You log in, find the right menu, and answer a short set of questions. Many decisions come back right away. The phone option is helpful if you’d rather speak to a person or if you can’t access your account online.

Requesting Online or Through the Mobile App

The web and app paths are nearly the same, so the steps below work for both. To submit a Capital One Venture CLI request:

- Log in to your Capital One account on the website or open the Capital One mobile app.

- If you have more than one card, pick your Venture card from the list.

- Look for the “I Want To” menu on your account page.

- Tap or click “Request Credit Line Increase.”

- Fill in the short form with your current income, employment, monthly card spend, rent or mortgage, and the new limit you want.

- Submit the request.

Most online requests get an answer right away. If Capital One needs more time to review, you may see a message saying a decision will come in a few days.

Requesting by Phone

If you’d rather talk to someone, call the customer service number on the back of your Venture card. When the representative answers, say clearly: “I’d like to request a credit limit increase on my Venture card.”

The agent will ask the same questions as the online form: your annual income, employment status, monthly spend, rent or mortgage, and the limit you’d like. Be ready with these numbers before you call, so the call goes smoothly.

A decision over the phone may come right away, or the agent may tell you the request needs more review. Either outcome is normal. If it goes to review, you’ll usually hear back within a few business days.

Eligibility Requirements Before You Request

Before you submit, check a few quick rules. This helps you avoid wasting a request when you’re not yet eligible.

How Often You Can Request an Increase

Capital One generally lets you request a credit limit increase once every six months. The clock starts from the date you opened the account or the date of your last increase, whichever is more recent. This rule applies to both customer-initiated requests and automatic increases.

So if you opened your Venture card four months ago, wait a couple more months before asking. The same is true if you just got an increase three months back. Asking too soon will usually lead to a quick denial.

Accounts That Aren’t Eligible

Not every account can get a credit line increase (CLI). Secured Venture-related accounts often cannot be increased the same way an unsecured card can. The deposit on a secured card sets the limit, so the path to more credit is different.

Authorized users and co-applicants also cannot ask for an increase. Only the primary account holder can submit the request. If you share the card with a partner, family member, or business co-owner, the person whose name is on the main account needs to be the one to ask.

What Information You’ll Need to Provide

The form is short, but having your numbers ready makes the request faster and more accurate. Capital One will ask you for:

- Your total annual income (more on how to report this in the next section)

- Your employment status and occupation

- An estimate of your monthly spend on the Venture card

- Your monthly mortgage or rent payment

- The new credit limit you’d like

You don’t need pay stubs or tax forms to submit the form. Capital One trusts the numbers you enter, but they should match what’s already on file as closely as possible.

Checking Your Current Limit Before You Start

Before you submit, take a moment to look up your current credit limit. You can find it on your account home page online or near the top of your card screen in the app. It also shows on your monthly statement.

Knowing your current limit helps you set a realistic target. Asking for a jump that’s too large, like going from $5,000 to $25,000, often leads to a denial. A request for 25% to 50% more than your current limit is usually more reasonable. If your limit is $10,000, asking for $13,000 to $15,000 tends to land better than asking for $30,000.

How to Report Your Income Accurately

The income field trips up a lot of people, especially freelancers, gig workers, and folks who just got a raise. Here’s how to handle it.

Capital One asks for your total annual income, which is your gross yearly income before taxes. Use the gross figure, not your take-home pay. If you earn $5,000 a month before taxes, report $60,000 a year, not the lower number that lands in your bank account.

If your income changes from month to month, like for freelancers or commission-based workers, add up your earnings from the last 12 months and use that total. If you’ve had a recent raise or a new job, use your new annual salary rather than last year’s lower number. An annual income update in your favor is one of the strongest signals for approval.

You can also include household income if you’re 21 or older and have reasonable access to a partner’s or spouse’s income to pay for the card. This rule comes from the Credit CARD Act of 2009 and is allowed by Capital One. Reporting household income legally can push your numbers higher and improve your odds.

⚠️ Mistake to Avoid: Do not inflate your income beyond what you can prove. Capital One may pull tax data or verify income later, and false information can lead to account closure or worse.

Keep your reported income in line with what banks already have on file. If you’ve reported $55,000 to other lenders recently and you suddenly enter $120,000 here, that gap can raise flags. Honest, consistent numbers build trust over time.

How long does the Decision Take

In most cases, you’ll see a decision right after you submit. Capital One states that “in most cases, credit limit increase decisions are available immediately after the request is submitted.”

If the system needs to look at your file more closely, the request goes to a manual review. That usually takes a few business days, and you’ll get a letter or email with the result. Phone requests follow the same pattern: some are answered on the call, and others take a few days.

If you don’t hear back within about 10 business days, log in to your account or call customer service to check the status.

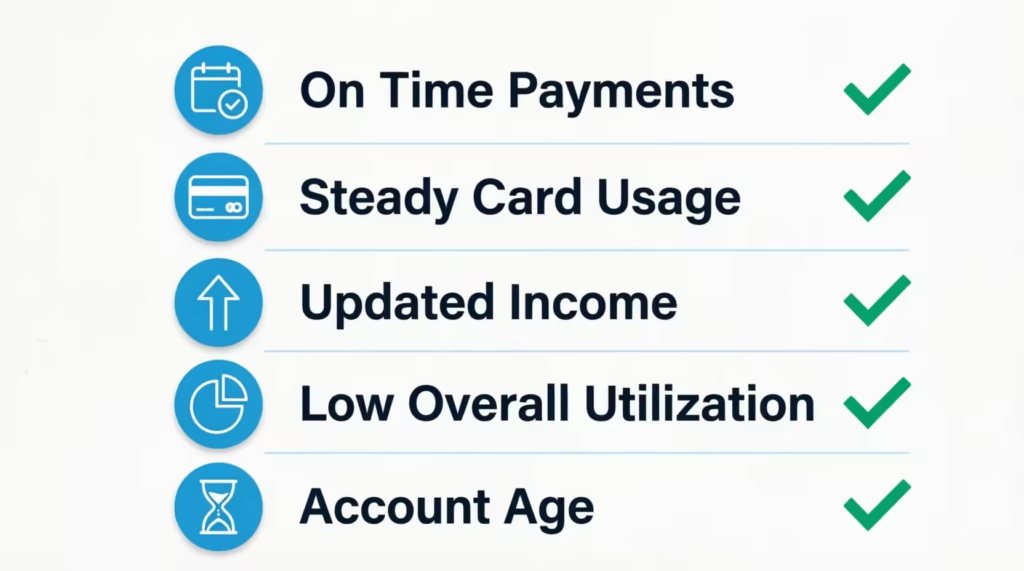

Factors That Improve Your Approval Odds

This is where small actions before you ask can make a real difference. Capital One looks at your full account behavior, not just your credit score, when deciding on a credit line increase (CLI). Focus on these areas before you submit a request.

Pay on time, every time. A run of six straight months of on-time payments is one of the strongest signals you can send. Even one late payment in the last six months can hurt your approval odds. If you’ve missed a due date recently, wait until you have a clean six-month stretch before asking.

Use the card, but don’t max it out. A card that sits unused gives Capital One no reason to extend more credit. On the other hand, a card that’s always at 90% of its limit looks risky. Aim for steady, active use where your statement balance stays under 30% of your limit. That ratio is called your credit utilization ratio, and it’s a key signal both to Capital One and to your overall FICO score.

Update your income if it has grown. A higher reported income tells the bank you can handle a higher limit. If you got a raise, switched to a better-paying job, or picked up steady side income, update your profile before you request the increase.

Keep overall utilization low across all your cards. Even if your Venture card looks fine, high balances on other cards can drag down your approval. Pay down other balances in the weeks before you ask, so your full credit picture looks healthy.

Let the account age. Capital One tends to give bigger increases to accounts that have been open longer with a strong history. After 12 months of responsible use, your odds go up. After 24 months, they go up again.

📌 Did You Know: Capital One automatically reviews many Venture accounts for a higher credit limit after about six months of on-time payments. You may get an increase without ever asking.

Common Reasons a Capital One Credit Limit Increase Is Denied

If your request gets denied, it usually traces back to one of a handful of common reasons. Knowing them helps you fix the issue and try again later.

- Low or inconsistent card usage. If you barely use the Venture card, Capital One has no recent activity to judge. Putting at least a few purchases per month on the card before you ask helps.

- Recent late or missed payments. A past-due status in the last six months is one of the most common denial reasons. Even one slip can pause your eligibility.

- The account is too new or too recently increased. Capital One usually wants at least six months of history since account opening or since your last credit line increase before granting another.

- Income too low for the requested limit. If you ask for a $20,000 limit but report a $30,000 income, the math doesn’t work for the bank. Ask for a smaller jump or update your income first.

- Low credit score. A FICO score in the low 600s or below makes any Capital One Venture credit limit increase harder to get. Work on your score first.

- You’re not the primary account holder. Authorized users and co-applicants cannot get an increase. The denial letter often spells this out.

The denial letter Capital One sends will list the specific reason. Read it carefully, since it points you straight to the fix.

What to Do If Your Request Is Denied

A denial is not the end of the road. It’s information you can act on.

Start by reading the denial letter or notice. Capital One is required by law to tell you why your request was turned down. The reason will fall into one of the categories above. Match the reason to a clear next step:

- If usage was too low, use the card more for daily spending over the next few months.

- If you had a late payment, build a clean six-month streak of on-time payments before asking again.

- If the account was too new, simply wait. Time is the only fix here.

- If income was the issue, wait for a raise or a new income stream, then update your profile before reapplying.

- If your credit score was the issue, work on paying down other balances and keeping older accounts open.

Some readers ask if a reconsideration request works after a denial. With Capital One, reconsideration calls are less common than with some other issuers. The cleaner path is to wait at least six months, fix the root cause, and submit a fresh request.

In the meantime, keep using the card responsibly. Charge what you can pay off in full each month. Keep your statement balance below 30% of your limit. Avoid new credit applications during this stretch. These steps protect your file and set you up for a stronger second request.

Automatic Increases vs. Requesting One Yourself

Capital One offers two paths to a higher limit: an automatic increase the bank gives you on its own, and one you ask for. Understanding both helps you decide whether to wait or take action.

Automatic credit limit increases happen quietly in the background. Capital One reviews accounts about every six months. If your account shows steady on-time payments, healthy usage, and a good credit profile overall, you may get a higher limit with no request from you. You’ll see it as a message in your account or a letter in the mail. The review uses a soft pull, so it never hurts your score.

The upside of waiting is that it costs you nothing. There’s no form, no question about whether you’ll be approved, and zero impact to your file. The downside is that the increase, when it comes, may be smaller than what you’d ask for, and you have no control over the timing.

Asking for an increase yourself gives you control. You pick the timing, you pick the amount, and you can update your income to support a larger jump. The trade-off is that you may get denied, which doesn’t hurt your score but does start the six-month clock over for another request.

Asking does not block you from a future automatic increase. The two paths run side by side. A reasonable strategy is to wait six months after opening the account, make sure your income and on-time payment history are strong, and then submit a request for the limit you actually want. If it’s approved, great. If not, the automatic review is still on the table for later.

For most cardholders who’ve held the Venture card for at least a year with a clean payment history, asking is the better move. You’ll likely get a bigger jump than the bank would give on its own, and the soft-pull policy means there’s no real downside to trying.

Frequently Asked Questions (FAQs)

Does Capital One Venture automatically increase the credit limit?

Yes. Capital One reviews accounts roughly every six months and may raise your limit on its own if you have on-time payments and healthy card usage. This automatic review uses a soft pull, so it never affects your credit score.

How often does Capital One Venture increase credit limits?

You can request an increase once every six months, counted from your account opening date or your last increase. Automatic reviews from Capital One also happen on roughly the same six-month cycle.

What is the Capital One 6-month rule?

Capital One requires your Venture account to be at least six months old since opening, or six months since your last credit limit increase, before you can request another one. This applies to both self-requested and automatic increases.

Why is it so hard to get a credit limit increase with Capital One?

Common denial reasons include low card usage, a late payment in the last six months, an account that’s too new, or income too low to support the requested limit. A low FICO score, typically in the low 600s or below, also makes approval harder.

Will Capital One give me a second chance after a denial?

Yes, but reconsideration calls are uncommon with Capital One compared to other issuers. The better path is to wait at least six months, fix the specific reason listed in your denial letter, then submit a fresh request.

Does a denied credit limit increase request hurt your credit score?

No. Capital One uses a soft inquiry for credit limit increase requests, including ones that end in denial, so a turned-down request leaves your credit score untouched.

Can I request a credit limit increase on a secured Capital One Venture card?

No. Secured Venture-related accounts can’t be increased the same way as unsecured cards, since the limit is set by your security deposit amount rather than a credit review.

Do I need a joint account to report my spouse’s income on the request?

No. If you’re 21 or older and have reasonable access to a partner’s or spouse’s income to help pay the card, you can legally report that household income under the Credit CARD Act of 2009, even without a joint account.

Bottom Line

Getting a higher limit on your Venture card comes down to timing, preparation, and honest numbers. The request itself uses a soft inquiry, so it does not hurt your score. Eligibility hinges on a six-month account age, clean payment history, and active card use. The form is short, but accurate income reporting and a realistic target amount make a real difference.

Wait for six clean months based on Capital One’s soft-pull policy. Then, update your income. After that, request a limit increase of 25% to 50% over your current limit.

If you know someone else with a Capital One Venture card who’s nervous about asking for more credit, share this guide with them. It could save them from sitting on a low limit far longer than they need to.