You just reviewed your Discover account, and something is wrong. A charge you don’t recognize. A duplicate billing. A payment for something you never received. It can feel frustrating, especially when you’re not sure how the process works or whether you’ll get your money back.

The good news: you have real legal rights here. To dispute a Discover credit card charge, you can file online, by phone, or by mail, and federal law requires Discover to complete the investigation within 90 days.

In this guide, we’ll walk you through every step. We’ll cover what types of charges you can dispute, what documentation to gather, how to file, what happens to your account during the review, and exactly what to do if Discover rules against you.

Key Takeaways

This guide explains how to dispute a Discover credit card charge, including valid dispute reasons, FCBA deadlines, filing methods, investigation timelines, appeal options, and the steps required to protect your rights throughout the process.

Core Facts:

- The Fair Credit Billing Act (FCBA) requires Discover to acknowledge a dispute within 30 days and complete the investigation within two billing cycles, not exceeding 90 days.

- Valid Discover disputes include unauthorized charges, billing errors, goods or services not received, and items that were significantly different from what was promised.

- FCBA protections apply when disputes are filed within 60 days of the statement date, while Discover generally allows most disputes up to 120 days from the transaction date.

- Pending charges cannot be disputed through Discover’s system; cardholders must wait for the transaction to post or contact the fraud department immediately if fraud is suspected.

- Discover may issue provisional credit during an investigation, but the credit can be reversed if the final decision favors the merchant.

- If Discover denies a dispute, cardholders have 10 days to appeal with new evidence and may escalate unresolved cases through the CFPB complaint process.

Best for:

- Discover cardholders who need to challenge unauthorized transactions, billing errors, duplicate charges, or merchant-related purchase problems.

- Consumers who want to understand FCBA dispute deadlines, documentation requirements, and their legal protections during an investigation.

- Cardholders whose disputes were denied and need guidance on appeals, evidence submission, or escalation through the CFPB.

Your Rights Under the Fair Credit Billing Act

Before you file a single dispute, it helps to know the law that protects you. The Fair Credit Billing Act (FCBA) is a federal law that governs billing disputes on open-end credit accounts, including credit cards. It gives you a clear set of rights and places firm obligations on issuers like Discover.

Under the FCBA, Discover must:

- Acknowledge your dispute within 30 days of receiving it.

- Resolve the dispute within two billing cycles. That window cannot exceed 90 days from the date Discover receives your complaint.

- Refrain from taking any negative credit action against you while the investigation is ongoing.

The FCBA covers three main dispute categories:

- Unauthorized charges: purchases you didn’t make or approve

- Billing errors: wrong amounts, duplicate charges, or math mistakes on your statement

- Goods or services not received as agreed: items that never arrived or didn’t match what was promised

On top of FCBA protections, Discover offers its own $0 Fraud Liability Guarantee. This means that if someone makes unauthorized purchases on your Discover card, you’re not responsible for those charges at all. The FCBA’s standard cap limits your liability to $50 for unauthorized charges, but Discover reduces that to zero.

These protections give you real leverage. When you file a dispute, you’re not asking for a favor. You’re exercising a right backed by federal law.

Which Discover Charges Can and Cannot Be Disputed

Not every charge you disagree with qualifies for a formal dispute. Filing an invalid claim wastes time and can result in a quick denial that leaves you without a path to recovery. Before you file anything, confirm your situation fits one of the four valid categories.

Unauthorized or fraudulent charges: Someone used your card without your knowledge or permission. For example, you check your statement and find a $340 charge at a retailer in a city you’ve never visited.

Billing errors: The charge was authorized, but the amount is wrong or the same charge appeared twice. For example, a restaurant charged you $89 instead of the $69 on your receipt, or a streaming service billed you twice in the same month.

Non-receipt of goods or services: You paid for something that was never delivered, or a service that was never provided. For example, you ordered a desk online, paid $420, and it never arrived despite multiple follow-up emails.

Goods or services significantly not as described: You got the item, but it was not what was advertised. It was damaged, defective, or the wrong product. The merchant also refused your return.

The following situations are not valid grounds for a chargeback:

- A subscription you forgot to cancel, but technically authorized

- A purchase made by a family member using your card without your specific knowledge. This is not third-party fraud under FCBA rules.

- Buyer’s remorse or dissatisfaction with a legitimate product that arrived as described

- Pending charges that have not yet been posted to your account

⚠️ Mistake to Avoid: The merchant name on your statement often looks different from the actual business name. A charge reading ‘AMZN Mktp US’ is Amazon. Before disputing on the basis that you don’t recognize a merchant, search the name online first. Filing an invalid dispute won’t hurt your credit score, but it will delay recovery if the real issue is something else.

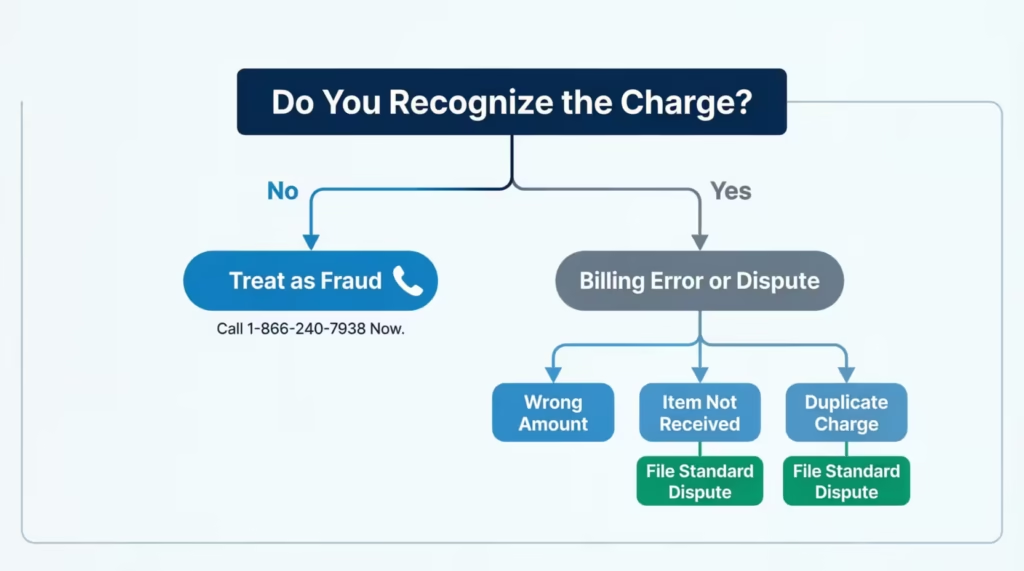

Fraud vs. Billing Error: Which Dispute Path Applies to You

This distinction matters because the two situations require different first steps.

If the charge was made by a third party without your knowledge or consent, treat it as fraud. Don’t start with an online dispute form. Call Discover’s dedicated fraud line at 1-866-240-7938 right away. Fraud specialists can quickly lock your account, cancel the compromised card, and start an investigation. This is much faster than the usual dispute process.

If the charge was approved but is incorrect in amount, a duplicate, linked to a canceled subscription, or for an item you didn’t receive, it’s a billing error or cardholder dispute. In those cases, the standard filing process (online, phone, or mail) is the right path.

A simple rule: if you don’t recognise the merchant at all and have no reason to believe that you or anyone you allowed made the purchase, treat it as fraud first.

The Deadline You Cannot Miss

The timeline for filing a dispute is one of the most misunderstood parts of the process. Missing it can mean losing your right to challenge the charge permanently.

The FCBA sets a 60-day minimum window for disputes. That clock starts from the date your billing statement was mailed or made available online. This is a critical detail: the clock does not start when you notice the charge. It starts the day the statement containing the charge was issued.

Here’s what makes this confusing: Discover’s operational window is longer. The network allows up to 120 days from the transaction date for most dispute types. So in practice, you likely have more time than the FCBA minimum. Your strongest legal protections under federal law, however, apply only within that first 60-day window.

All Discover dispute deadlines are measured in calendar days, not business days. Weekends and holidays count.

| Deadline Type | Time Window |

|---|---|

| FCBA legal protection window | 60 days from statement date |

| Discover’s operational dispute window | 120 days from transaction date |

| Days counted as | Calendar days (weekends included) |

If you’re near either deadline, don’t wait to gather perfect documentation. File the dispute now with what you have, then submit additional evidence once the case is open. A timely but incomplete filing is recoverable. A missed deadline is not.

Can You Dispute a Pending Charge?

No. Pending charges aren’t on your account yet, so you can’t dispute them through Discover’s system.

If you see a pending charge that looks fraudulent, don’t wait for it to post. Call Discover’s fraud line at 1-866-240-7938 right away. A fraud specialist can freeze your account or cancel the card before the charge finalizes. This stops the problem at the source.

If the pending charge appears to be a billing error, allow it to post first. Most pending transactions clear within 3 to 5 business days. Once it posts, you can file your dispute through any standard channel.

What to Gather Before You Contact Discover

The single biggest factor in whether a dispute succeeds is documentation. Cardholders who provide clear, organised evidence do much better than those who just claim a charge is wrong. Gather what you need before making contact. It strengthens your initial claim and reduces the chance of follow-up requests that delay resolution.

For every type of dispute, collect these first:

- A screenshot or PDF of your statement or account activity page showing the charge

- The exact merchant name as it appears on your statement, not the store’s actual name, but the billing descriptor

- The transaction date and exact dollar amount

For fraud and unauthorized charges, also gather:

- Any police report number, if you’ve filed one

- Prior statements confirming this merchant or charge type has not appeared before

- Documentation of any account alerts you received around the time of the charge

For billing errors (wrong amount or duplicate charge), also gather:

- The original receipt, invoice, or order confirmation showing the correct amount

- Any written or email correspondence with the merchant about the error

For non-receipt or items not as described, also gather:

- Order confirmation and tracking information

- Proof of attempted contact with the merchant: emails, chat logs, or call records with dates

- Photos of defective or incorrect items received

- Written denial of your return or refund request from the merchant

For a canceled subscription that kept billing:

- Cancellation confirmation email or screenshot

- The date of cancellation vs. the date of the charge, to show the billing came after cancellation

💡 Pro Tip: Always keep copies of everything you submit. When uploading documents to Discover’s portal, save local copies too. If the dispute escalates to an appeal or a CFPB complaint, you’ll need a complete record of exactly what evidence you provided and when.

Should You Contact the Merchant First?

For billing errors, non-receipt disputes, and canceled subscription issues, yes. Try to resolve the situation with the merchant before contacting Discover. Both the FCBA framework and Discover’s own guidelines expect cardholders to make a good-faith effort to resolve disputes directly with the seller first.

There’s also a practical reason: merchants typically prefer to handle these situations themselves. A chargeback costs them time and fees. A direct resolution costs them only the refund. Many companies will issue a credit quickly once you present the evidence clearly.

Skip the merchant contact entirely if the charge is fraudulent. Don’t call the merchant about a charge you didn’t make. Contact Discover’s fraud line immediately.

Whatever the outcome of your merchant contact, document it. Save every email, note every call with a date and representative name, and screenshot any live chat exchanges. If the merchant refuses to help, that documentation becomes evidence in your dispute.

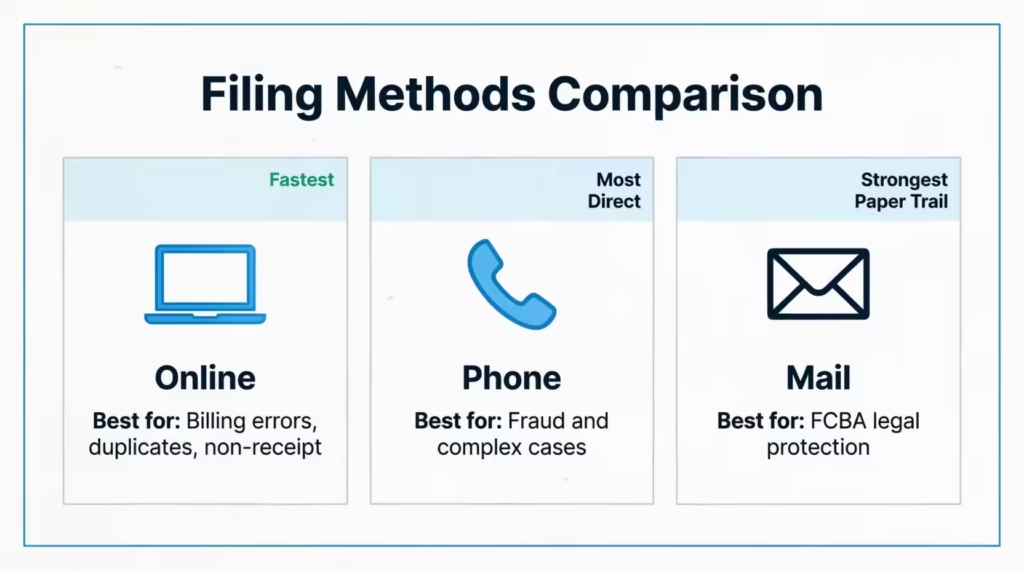

How to File a Dispute With Discover

Discover gives you three ways to file a dispute: online through your account portal, by phone, and by mail. Each channel works, but each suits different situations.

Online is the quickest way to resolve most billing errors, disputes over missing receipts, and issues with cancelled subscriptions. Phone is best for fraud or complex situations where speaking directly with a representative matters. Mail creates the strongest paper trail and is the most legally protective method under the FCBA.

How to Dispute a Discover Charge Online

Log in to your Discover account at discover.com. From the top navigation, click the Activity dropdown and select Activity and Statement. Find the charge you want to dispute in your transaction list.

Click on the transaction to expand it, then select Dispute This Charge. You’ll be asked to choose a dispute reason from a dropdown menu. Select the option that most accurately describes your situation.

Fill in the details: the merchant name as it appears on your statement, the date, the amount, and a brief explanation of the problem. Be specific and factual. The more precise you are, the easier it is for Discover’s investigators to check your claim.

To upload supporting documentation, go to the Disputes page, accessible under the Security dropdown in your account navigation, and use the Upload Documents section. Upload clear, legible copies of all evidence. If a document is small or scanned at low resolution, re-scan it at higher quality before uploading.

When you submit, record your dispute reference number. You’ll need it for any follow-up.

📌 Did You Know: You can only dispute posted transactions online. If a charge still shows as pending, it won’t appear in the dispute flow. Wait for it to post (typically 3 to 5 business days), then return to the file.

How to Dispute a Discover Charge by Phone

For standard billing disputes, call Discover customer service at 1-800-DISCOVER (1-800-347-2683). If your dispute involves fraud or unauthorized charges, call the dedicated fraud line at 1-866-240-7938 instead. Fraud specialists can quickly lock your account, cancel the compromised card, and speed up your case more than a general representative can.

Before you call, have the following ready:

- The merchant name exactly as it appears on your statement

- The transaction date and dollar amount

- A brief, clear explanation of why the charge is incorrect

- Any documentation or reference numbers you can cite

During the call, stay factual and organized. Dispute representatives work faster when the information is clear and specific. At the end of the call, ask for a case or reference number and note the representative’s name, the date, and the time.

How to Dispute a Discover Charge by Mail

Mail is the most legally protective dispute method. Under the FCBA, a written dispute creates the strongest record and gives you the most robust rights, including the requirement that Discover acknowledge receipt within 30 days.

Your dispute letter should include:

- Your full name and account number

- The merchant name, transaction date, and charge amount

- A clear explanation of why the charge is incorrect

- A list of all enclosed supporting documentation

Find the billing dispute address on the back of your monthly statement. This address is different from Discover’s main correspondence address. It’s meant only for FCBA disputes.

Send your letter via certified mail with a return receipt requested. This gives you a record of the postmark, which locks in your dispute date, and confirmation of delivery. Include copies of all evidence. Never send originals. Label each document clearly and reference it in the letter.

Keep a complete copy of everything you send, organized by date.

What Happens to Your Account During the Investigation

Once you file a dispute, Discover begins its investigation. Here’s what that process looks like.

Discover the contacts of the merchant who is involved and provide the details of your claim. The merchant then has a limited window, typically up to 30 calendar days, to respond. They can either accept the dispute or submit counter-evidence supporting the validity of the charge.

While the investigation is open, you can continue using your Discover card normally. The dispute does not freeze your account or restrict your purchasing ability.

The FCBA prohibits Discover from taking any negative credit action against you during the investigation. They cannot report the disputed amount as delinquent. They cannot close your account or restrict your credit limit based solely on the open dispute.

Continue paying the undisputed part of your bill on time each month. This is the correct approach. Skipping payment altogether is not protected under the FCBA and can lead to late fees and a credit impact.

Provisional Credit: Will You Get Your Money Back Right Away?

In many cases, particularly for fraud-related disputes, Discover may issue a provisional credit to your account while the investigation is ongoing. This temporary credit adds the disputed amount back to your available balance immediately. You can use the funds before the case is closed.

A provisional credit is not a final decision. If Discover’s investigation ultimately rules in the merchant’s favor, the provisional credit will be reversed, and the original charge will be reinstated.

Not all dispute types automatically receive a provisional credit. Billing disputes that are complex or have little initial documentation might not have a resolution until later in the investigation. Check your account’s dispute status page or call customer service if you’re unsure whether one has been issued.

Do You Have to Pay the Disputed Amount While the Dispute Is Open?

Under the FCBA, you are not required to pay the disputed portion of your balance while the investigation is active. That protection can last up to 90 days. This rule is here to stop cardholders from having to pay a charge while its validity is still unclear.

You must still pay the rest of your balance on time. Consider the example of Marcus, a project manager who disputed a $280 double-charge from a software vendor. He continued paying his full statement balance minus the $280 each month while the dispute was open. Discover’s investigation confirmed the error, the charge was removed, and his account showed no late payments or credit impact.

If you don’t pay the undisputed part of your balance, the FCBA won’t protect you from late fees, interest charges, or harm to your credit score. The protection applies only to the specific disputed amount.

How Long Does Discover Take to Resolve a Dispute?

Most cardholders want to know: how long will this actually take? The answer depends on the complexity of the dispute, but federal law sets firm outer limits.

The FCBA requires Discover to acknowledge your dispute within 30 days of receiving it. From there, the full investigation must be completed within two billing cycles and no more than 90 days total from the date they received your complaint.

Simple cases, especially fraud disputes backed by strong documentation, can be resolved faster. Some clear-cut unauthorized-charge cases close within 30 days. Complex cardholder disputes, especially ‘not as described’ claims with merchant counter-evidence, can last the full 90 days.

If Discover fails to meet these timelines, that is an FCBA violation in its own right. You can report that failure to the Consumer Financial Protection Bureau (CFPB) as a separate complaint.

How to Check the Status of Your Discover Dispute

Log in to your Discover account and navigate to the Disputes page. The status of all open and recent disputes appears there, updated as the investigation progresses.

Discover will also inform you in writing. This can be by mail or through your account’s secure message centre for any important update or decision. Keep your contact preferences current so you don’t miss a deadline-sensitive notification.

If you’ve heard nothing within 30 days of filing, call customer service and provide your dispute reference number. Confirm that your case was received and is active. Keep a note of who you spoke with and what you were told.

Understanding Your Dispute Outcome

Once Discover completes its investigation, they’ll notify you in writing of the decision. Two outcomes are possible, and neither one is necessarily the end of the road.

If Discover Rules in Your Favor

A favorable ruling means the charge is officially removed from your account. If a provisional credit was issued during the investigation, it becomes permanent. You’ll see the final credit reflected on your next statement.

After a favorable ruling on a fraud dispute, verify that your card replacement has been issued. Then review the past 30 to 60 days of account activity carefully. Fraudulent charges rarely appear in isolation. If one unauthorized transaction occurred, others may have as well. Report any additional suspicious charges to Discover’s fraud team right away.

If Discover Rules Against You

An unfavorable ruling means Discover determined the charge was valid based on the evidence reviewed. Any provisional credit granted while we investigate will be reversed. The original charge will then return to your account.

You’ll receive a written notice explaining the decision. Read it carefully. The explanation will tell you what evidence or reasoning Discover used. This matters because any appeal you make must directly address that reasoning and provide new evidence.

One number to remember: you have 10 days from the date of the denial notice to file an appeal. This is not a soft deadline. It’s the window Discover gives you to act before the case is considered closed.

Also note that if interest and fees are accrued on the disputed amount during the investigation period, Discover may reinstate those charges alongside the original transaction. Review the full reinstatement carefully before deciding whether to appeal.

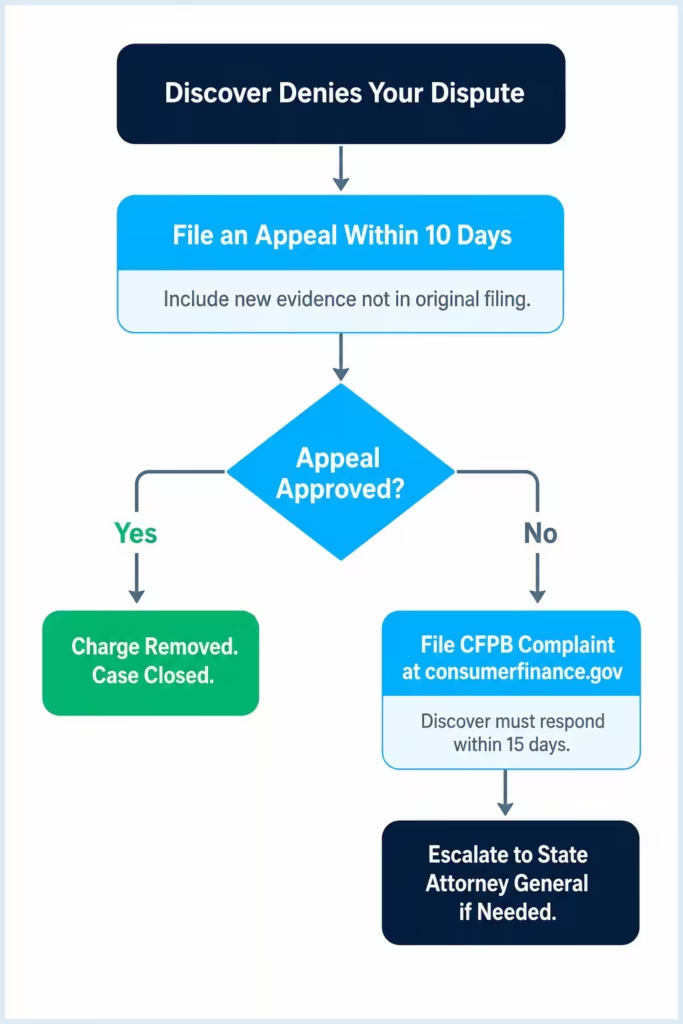

If Discover Denies Your Dispute: The Appeal and Escalation Path

A denial is frustrating, but it’s not final. Discover’s process includes a formal appeal path, and beyond that, federal regulators provide an additional escalation option.

Step 1: File an appeal within 10 days. Contact Discover within 10 days of the denial notice. State clearly why you disagree with the ruling. This part is critical: include new evidence that was not part of your original dispute filing.

A resubmission of the same documents won’t change the outcome. Your appeal should include something new. This could be: a written refusal from the merchant you didn’t submit before, a cancellation confirmation email, a police report, or proof that you were in a different location during the fraudulent transaction.

To submit your appeal materials, use the Upload Documents section on Discover’s Disputes page, or send them via certified mail to the billing dispute address on your statement. If you use mail, send it certified with a return receipt so you have proof of both submission and delivery.

When preparing your appeal, organize your evidence clearly. Label each document and reference each one in your written explanation. Walk through your reasoning step by step, addressing the specific basis for the denial.

How to File a CFPB Complaint If the Appeal Fails

If Discover denies your appeal and you believe their decision was incorrect, your next option is a complaint with the Consumer Financial Protection Bureau at consumerfinance.gov.

Here’s how the CFPB process works: once you submit a complaint, the CFPB forwards it to Discover. Discover is then required to respond within 15 days and provide a final response within 60 days. The complaint becomes part of a public regulatory record.

Be clear about what the CFPB can and can’t do. It functions as a mediator, not a court. It can make Discover respond, create an official record of your complaint, and highlight misconduct patterns. However, it can’t directly issue a refund. That said, companies often respond differently to CFPB complaints than to standard customer service escalations.

If the dispute involves a significant amount and the CFPB process doesn’t produce a satisfactory resolution, you have the option to escalate to your state attorney general’s office or state banking regulator. Some states have consumer protection agencies with their own dispute authority.

Immediate Steps If Your Discover Card Was Used Fraudulently

If someone used your Discover card without your permission, the process is faster and more urgent than a standard billing dispute. The goal isn’t just to recover the charge. It’s to stop any additional damage immediately.

Step 1: Call the fraud line right now.

Dial 1-866-240-7938 to reach Discover’s fraud specialists. Don’t start with the online dispute form. Fraud specialists can help with your account right away. Meanwhile, the online process sends your case through regular review queues.

Step 2: Request an immediate account freeze or card cancellation.

Ask the representative to freeze your account temporarily or cancel the compromised card. Then, request a replacement with a new account number. A freeze prevents further unauthorized charges while you work through the details. A new card number gives you a clean break.

Step 3: Review the last 30 to 60 days of account activity.

Go through every transaction with the fraud representative on the call. Fraudulent charges rarely appear alone. If a thief gets your card info and makes one purchase, they might have made others, too. These could be small amounts meant to slip by unnoticed.

Step 4: File a police report if warranted.

If the fraud is major, with many charges, a large amount, or identity theft beyond just your credit card, then report it to your local police. The report number strengthens your dispute and may be required if you escalate to regulatory agencies later.

Step 5: Monitor your credit reports.

Identity theft doesn’t always stop at credit card fraud. For 60 to 90 days after the incident, check your reports with all three major bureaus: Equifax, Experian, and TransUnion. Look for any new accounts or hard inquiries you didn’t authorise. You can access free reports at AnnualCreditReport.com.

After the Fraud Call: Protecting Your Account Going Forward

Once your replacement card arrives, take a few minutes to update any accounts set up with your old card number.

- Update autopay and subscription services with the new card number

- Update saved payment methods at online retailers you use regularly

- Update digital wallets (Apple Pay, Google Pay, etc.) with the new card

Also, turn on real-time transaction alerts in the Discover app if you haven’t already. These push notifications show you charges as soon as they’re authorized. This helps you spot any suspicious activity before it appears on your statement.

If you think your online account details were compromised, not just the card number, change your Discover account password right away. Use a unique, strong password that you don’t use on any other site.

Frequently Asked Questions (FAQs)

What are valid reasons for disputing a credit card charge?

The four valid dispute reasons are unauthorized charges, billing errors like duplicates or wrong amounts, goods or services never delivered, and items that arrived damaged or misrepresented. Forgetting to cancel a subscription, buyer’s remorse, or a purchase made by a family member does not qualify.

How late is too late to dispute a charge on Discover?

Under federal law, you have 60 days from the date your billing statement was issued to file a dispute with full legal protection. Discover’s own network allows up to 120 days from the transaction date, but the stronger FCBA rights apply only within that first 60-day window.

Do disputes hurt your credit score?

Filing a dispute does not hurt your credit score. Federal law prohibits Discover from reporting the disputed amount as delinquent or taking any negative credit action against you while the investigation is open, which can last up to 90 days.

Will the merchant know if I dispute a charge?

Yes. Once you file a dispute, Discover contacts the merchant directly and shares the details of your claim. The merchant then has up to 30 calendar days to either accept the dispute or submit counter-evidence supporting the validity of the charge.

What happens if a merchant never responds to a chargeback dispute?

If a merchant fails to respond within their allotted window, typically up to 30 calendar days, the dispute is generally resolved in the cardholder’s favor by default. Discover cannot keep a case open indefinitely and must complete the investigation within 90 days of receiving your complaint.

Is there a downside to disputing a credit card charge?

Disputing a charge has no direct penalty to your credit score and does not close your account. However, filing invalid disputes wastes time, and if Discover rules against you on a fraud case, any provisional credit issued during the investigation will be reversed and the original charge reinstated.

How do I dispute a credit card charge that I willingly paid for?

A charge you knowingly authorized generally cannot be disputed as fraud or a billing error. If the item arrived damaged, never arrived at all, or was significantly misrepresented, you can file a dispute under those specific grounds, but simply regretting a purchase is not a valid reason.

Is it better to dispute a Discover charge online or by phone?

Online is faster for straightforward billing errors, duplicate charges, and non-receipt disputes. Phone is better for fraud cases since calling 1-866-240-7938 connects you with fraud specialists who can freeze your account and cancel your card immediately, which the online form cannot do.

Does Discover have a 24/7 phone number for disputes?

Discover’s general customer service number is 1-800-DISCOVER (1-800-347-2683), and the dedicated fraud line is 1-866-240-7938. Both lines are available around the clock, and the fraud line connects you with specialists who can lock a compromised account right away.

What is Discover’s $0 Fraud Liability Guarantee?

Discover’s $0 Fraud Liability Guarantee means you owe nothing for unauthorized purchases made on your account. Federal law under the FCBA already caps your liability at $50, but Discover reduces that amount to zero, so you bear no financial responsibility for charges a thief makes.

Bottom Line

Disputing a Discover credit card charge is a structured process, and you have real protections at every stage. Federal law limits Discover’s investigation to 90 days. You will get an acknowledgment within 30 days. Also, your credit is protected while the case is open. Document your claim thoroughly, file before the deadline, and keep a record of everything you submit.

To make the most of the FCBA protections and Discover’s $0 Fraud Liability guarantee, act fast. Gather your evidence and file your claim. If you get a denial, follow the full escalation path. The 10-day appeal window is there for that reason. If the appeal doesn’t fix the issue, you can use the CFPB complaint process.

If someone you know has faced an unauthorized charge or billing error on their Discover card, this guide has all the steps they need to take next. Share it so they don’t miss a critical deadline.