If you have a Discover card balance you just can’t pay anymore, you’re not alone, and you’re not stuck. Many cardholders feel scared after missing a payment or two. They worry about lawsuits, ruined credit, or rude calls from collectors. The truth is, you can negotiate credit card debt with Discover if you act early and speak honestly about your hardship.

Discover will often work with you, but only if you ask the right way.

This guide walks you through every step. You’ll learn what to say, when to call, how much to offer, and how to protect yourself from tax surprises and lawsuits later on.

Key Takeaways

This guide explains how to negotiate credit card debt with Discover, covering the three main relief paths, the best timing window for settlement, typical settlement ranges, how to handle the negotiation call, post-settlement steps, credit score effects, tax consequences, and what to do if Discover files a lawsuit.

Core Facts:

- Discover offers three debt relief paths: a hardship program for cardholders who can still make partial payments, direct settlement for accounts that are severely past due, and a nonprofit debt management plan through a credit counseling agency.

- Most Discover settlements fall between 40 and 60 percent of the balance owed; lump sum offers get the largest discounts, while payment plan settlements typically land higher.

- The 60/60 plan reduces the balance by up to 40 percent and lets the borrower repay the remaining amount over 60 months, often at a very low or zero interest rate; accounts generally need to be 90 to 120 days past due to qualify.

- The 120 to 180 day window before charge-off is typically the best period to settle, because Discover would rather collect a partial payment than transfer the file to outside legal counsel.

- Forgiven debt of $600 or more is reported to the IRS on Form 1099-C and counts as taxable income unless the borrower qualifies for the insolvency exclusion by filing IRS Form 982.

- Discover is known to file lawsuits after the 180-day charge-off; responding with a written answer within 20 to 30 days of being served prevents a default judgment, and settlement negotiations can continue even after a lawsuit is filed.

Best for:

- Cardholders who have missed payments or are on the verge of missing payments and want to understand their options before their account reaches charge-off status.

- People who have already received a settlement offer from Discover or a collection law firm and want to evaluate whether the offer is reasonable before accepting.

- Anyone who has received a Form 1099-C after a Discover settlement and needs to understand how the insolvency exclusion works before filing their tax return.

Does Discover Actually Negotiate Credit Card Debt?

Yes, Discover does negotiate. The company has a reputation for being one of the more consumer-friendly card issuers when a cardholder reaches out early and explains a real money problem. At the same time, Discover is also known as a very active litigator. If you ignore them, they will sue. So the door is open, but you have to walk through it.

Discover Financial Services offers debt relief in two main ways. The first is an internal hardship plan if you are still current or only slightly behind. The second is a direct debt settlement once your account is deeply past due. Both paths require proof of real financial hardship, like a job loss, a medical event, a divorce, or a sharp income drop.

What Discover will not do is reduce your balance just because you ask. You must show that paying the full amount is not possible. Bring numbers. Bring proof. Be ready to explain your story in plain words.

💡 Pro Tip: Reach out before you miss a payment if you can. Discover treats early callers very differently from people who go silent for 90 days. Asking for help while still current can unlock interest cuts that vanish later.

The Three Ways Discover Will Work With You on Debt

Discover has three main paths to lower what you owe or make payments easier. Each one fits a different stage of trouble. Picking the right path saves you money and stress.

The first path is a Discover hardship program. This is best for people who can still pay something each month but not the full minimum. Discover may lower your interest rate, waive late fees, or set a short-term lower payment.

The second path is direct debt settlement. You agree to pay a smaller lump sum or short-term plan. In return, Discover marks the rest of the balance as forgiven. This is the right path when you can’t keep paying, and the account is far behind.

The third path is a debt management plan through a nonprofit credit counseling agency. A counselor talks to Discover for you and sets one fixed monthly payment.

What Is Discover’s 60/60 Plan?

The 60/60 plan is one of Discover’s best-known hardship offers. It is not promoted on the public website, but agents can offer it when your account is deeply delinquent, and you can prove real hardship.

Under this plan, Discover may agree to reduce your balance by up to 40 percent. You then pay the remaining 60 percent over 60 months, often at a very low or zero interest rate. So if you owe $10,000, your new balance becomes about $6,000, paid over five years. That works out to roughly $100 a month.

To qualify, you usually need to be at least 90 to 120 days past due. You also must show that you cannot pay the full balance but can keep up with a smaller fixed payment. Agents do not always volunteer this plan. You may need to ask for it by name and explain why a long-term fixed plan is the only way you can repay anything at all.

When Discover Will (and Won’t) Negotiate, The Timeline

Timing changes everything. Discover treats a current account, a 60-day late account, and a charged-off account as three different worlds. Knowing where you stand helps you ask for the right thing.

Below is a simple view of how account age changes your options:

| Account Status | Days Past Due | What Discover May Offer |

|---|---|---|

| Current | 0 days | Lower APR, waived fees, short term payment plan |

| Early delinquent | 30 to 60 days | Hardship program, reduced minimum payment |

| Mid delinquent | 90 to 120 days | Settlement talks begin, 60/60 plan possible |

| Late stage | 120 to 180 days | Best settlement offers, 40 to 50 cents on the dollar |

| Charged off | 180+ days | Settlement with Discover recovery or a law firm |

Federal banking rules require banks to charge off credit card accounts at 180 days past due, per OCC guidance. This is why the 120 to 180 day window is often the sweet spot for settlement. Discover knows the charge-off is coming. They would rather collect 50 cents on the dollar now than send the file to a law firm later.

If you are still current, do not stop paying just to force a settlement. That can backfire. Instead, call and ask for a hardship plan first.

How Much Will Discover Settle For?

Most Discover settlements land between 40 and 60 percent of the balance owed. Some accounts settle for as low as 25 to 30 percent, but those are rare and usually involve very old debt or proven insolvency. A few settle for 70 percent or more when the account is fresh, and the hardship is mild.

So if you owe $8,000 on your Discover card, a realistic settlement falls between $3,200 and $4,800 as a lump sum. Payment plan settlements tend to land higher, often 60 to 70 percent, because Discover charges a small premium for waiting.

What Affects the Settlement Amount Discover Will Accept

Five factors push the settlement number up or down:

- Age of the debt: Older debt settles cheaper. A 150-day past due account settles lower than a 60-day account.

- Strength of your hardship: A documented job loss or medical event gets better offers than a vague “I’m struggling.”

- Lump sum vs installments: A one-time payment gets the biggest discount. Discover wants the cash today.

- How much cash you can show: If you can prove you only have $3,000 to your name, Discover may take it on a $9,000 balance.

- Whether a law firm is involved: Once the file moves to outside counsel, the law firm sets the floor, not Discover.

⚠️ Mistake to Avoid: Do not accept the first offer. Discover agents often start at 70 to 80 percent. Counter with 30 to 40 percent and meet somewhere in the middle. Silence is a tool. Pause before replying.

How to Prepare Before You Call Discover

Walking into this call cold is the fastest way to lose money. A short prep session puts thousands of dollars back in your pocket. Plan to spend about an hour on this step.

Gather these items before you dial:

- Your Discover account number and current balance

- Your last two pay stubs or proof of lost income

- A simple monthly budget showing income minus rent, food, utilities, and other debts

- A list of any other credit cards or loans you owe

- A clear hardship story in three sentences

- The exact amount you can pay today as a lump sum, plus a second smaller backup number

- A quiet room and a pen and paper to take notes

Write your hardship story on paper so you do not freeze on the phone. Keep it short and honest. For example: “I lost my job in March. I have not found steady work since. My savings are almost gone, and I can pay $3,000 today to close this account.”

Documents matter. If Discover asks for proof of hardship, you may need to send a termination letter, a medical bill, a divorce filing, or recent bank statements. Have copies ready as PDFs.

What to Say When You Call Discover to Negotiate

Call the number on the back of your card and ask for the “hardship” or “loss mitigation” department. Do not negotiate with the regular customer service line. They cannot approve settlements. Be polite, calm, and clear.

A simple call framework works best. Move through it in order:

- State your name and account number. Confirm you are speaking with the right team.

- Explain your hardship in three sentences. Stick to facts. No drama.

- Say what you want. “I want to settle this account for a one-time payment.”

- Make your opening offer. Start low, around 25 to 30 percent of the balance.

- Stay quiet after the offer. Let the agent respond first.

- Counter calmly. If they say 70 percent, say 35. Move in small steps.

- Ask for the agreement in writing before you pay. This step is not optional.

If the first agent says no, thank them and hang up. Call back the next day. A different agent may say yes. This is called “agent shopping,” and it works.

Never give Discover access to your bank account by phone before you have the written deal in hand. Once they have your routing number, they may pull more than you agreed to.

How to Make a Written Settlement Offer to Discover

Some people prefer to start in writing. A written offer creates a paper trail and protects you later. Send your offer by certified mail with a return receipt to the address on your monthly statement.

A strong written offer includes:

- Your full name, account number, and address

- A short statement of hardship

- The exact dollar amount you offer

- The exact payment method and date you will pay

- A clear request that Discover confirm in writing

- A line that says the settlement closes the account “paid in full” or “settled in full for less than full balance”

Give Discover 30 days to reply. If they counter, reply in writing again. Save every letter. These documents protect you if the debt ever resurfaces with a collector.

What Happens After Discover Agrees to a Settlement

Getting a verbal yes is not the finish line. The deal is only real when you have it in writing, and the payment clears. Skipping these steps can erase everything you fought for.

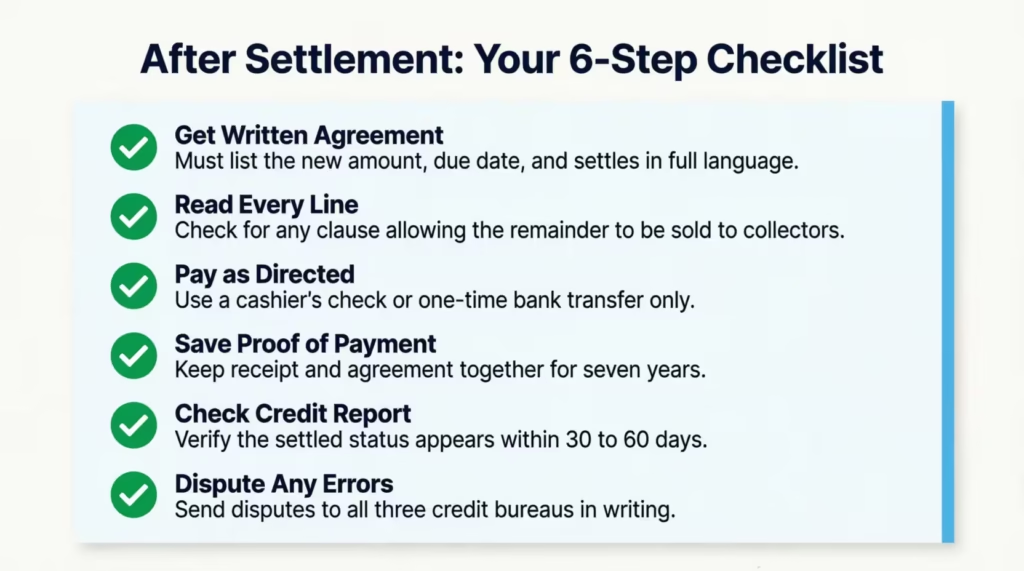

After agreement, follow this short checklist:

- Get the written agreement. It must list the new amount, the due date, and the words “settles the account in full.”

- Read every line. Watch for any clause that lets Discover sell the rest of the debt to a collector.

- Pay the way the letter says. Use a cashier’s check or a one-time bank transfer. Avoid giving open bank access.

- Save proof of payment. Keep the canceled check, the wire receipt, and the agreement together for seven years.

- Check your credit report 30 to 60 days later. Discover should report the account as “settled” or “paid, settled for less than full balance.”

- Dispute any errors in writing. Send the dispute to all three credit bureaus with copies of your paperwork.

If the credit report still shows a balance after 60 days, send the agreement to Discover and ask them to update the bureaus.

How Settling With Discover Affects Your Credit Score

A settlement helps in the long run, but it does hurt in the short run. Knowing the truth helps you plan the next 24 months.

When Discover reports the account as “settled” or “settled for less than full balance,” your credit score drops. The drop is bigger if your account was still current before. It is smaller if the account was already past due or charged off, since the damage was already done.

Most people see a 50 to 100 point drop right after a settlement. The settled note stays on your report for seven years from the date of first delinquency. That said, the score begins to recover within 6 to 12 months as you add new on-time payments to other accounts.

A “paid in full” mark is better than “settled.” Some agents will agree to update the wording for an extra few hundred dollars. Ask for this in writing. It is sometimes called “pay for delete,” though true deletion is rare with big issuers like Discover.

📌 Did You Know: A charged off account already crushed your score before settlement. So settling a charged off Discover account often hurts less than settling a current one. The hardest hit happens at the moment of charge off, not at settlement.

The Tax Consequences of Settling Discover Debt

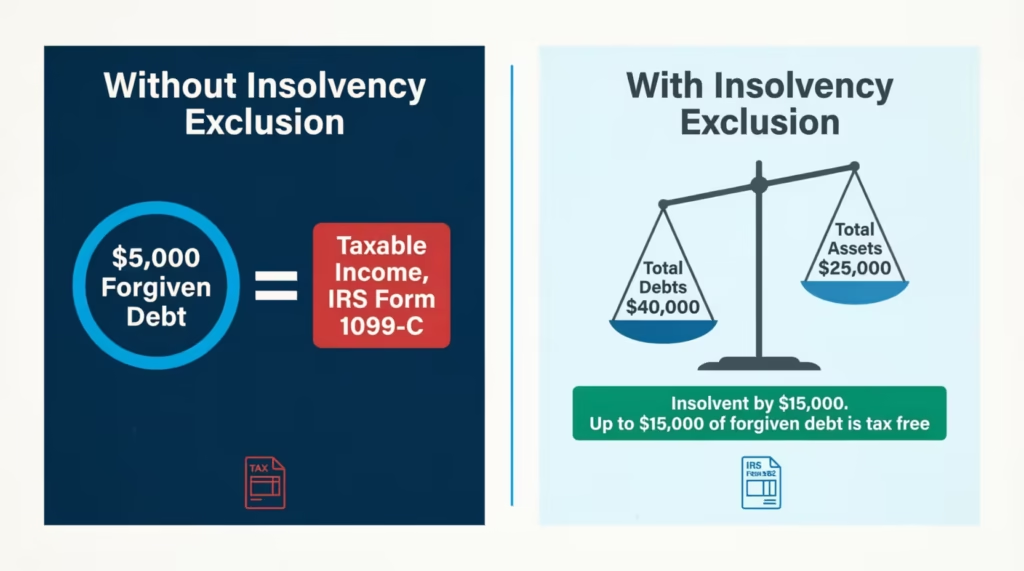

Here is the part most people miss. The IRS treats forgiven debt as income. So if Discover wipes out $4,000 of your balance, the IRS may treat that $4,000 as money you earned that year.

Per IRS rules, lenders must file Form 1099-C for any canceled debt of $600 or more. You will get a copy in the mail in late January of the year after the settlement. You must report that amount on your tax return, or the IRS will send a notice later.

The tax hit can be painful. If you settled $5,000 of debt and you are in the 22 percent bracket, you may owe about $1,100 in extra taxes. Plan for this when you set aside cash for the settlement itself.

How to Avoid Taxes on Forgiven Discover Debt: The Insolvency Exclusion

There is a legal way to skip the tax bill. It is called the insolvency exclusion. You qualify if your total debts were more than your total assets right before the settlement.

Here is how it works in plain terms. Add up everything you owe the day before the settlement. Then add up everything you own, like cash, cars, retirement accounts, and home equity. If your debts are bigger, you are insolvent by the difference.

For example, say you owe $40,000 in total debt and own $25,000 in assets. You are insolvent by $15,000. So up to $15,000 of canceled debt is tax-free.

To claim this break, file IRS Form 982 with your tax return for the year you got the 1099-C. The form is short, but the math behind it must be exact. Keep a worksheet showing every debt and asset on the day before the settlement. A tax pro who knows debt cancellation can help. The fee is usually worth it.

What Happens If Discover Sues You for the Debt

Discover is known to sue more often than many big issuers, especially through outside law firms. A lawsuit usually starts after the 180-day charge-off if you have not settled or set up a plan.

You will get served with a summons and complaint. Do not ignore it. If you do nothing, the court will enter a default judgment against you. That judgment lets Discover or its law firm garnish your wages, freeze your bank account, or put a lien on your property, depending on your state.

You have a short window, usually 20 to 30 days, to file a written answer with the court. The answer denies the parts of the lawsuit you can challenge, like the exact amount owed or the chain of ownership. Even a simple answer stops a default judgment and forces the other side to prove their case.

Can You Still Negotiate With Discover After a Lawsuit Is Filed?

Yes. In fact, many of the best settlements happen after a lawsuit is filed. The catch is that you now negotiate with the law firm, not Discover directly.

Law firms like Stenger & Stenger or similar collection counsel often handle Discover files in court. These firms have the authority to settle for 50 to 70 percent of the judgment amount. They prefer a fast deal over a long court fight because their fee structure rewards quick resolution.

To negotiate after a lawsuit, do these things:

- File your written answer first to protect against default

- Call the law firm listed on the lawsuit, not Discover

- Ask for the “settlement” or “resolution” department

- Offer a lump sum if you can. The discount is the biggest there.

- Insist on a written stipulation that dismisses the case once you pay

Never pay a court judgment without a signed dismissal. Otherwise, the judgment stays on your record even after you pay.

Should You Use a Debt Settlement Company or Credit Counseling Agency?

You do not have to handle this alone. Two kinds of help exist, and they are very different. Picking the wrong one can cost you thousands.

Debt settlement companies are for-profit firms. They tell you to stop paying Discover and instead send money to a savings account they manage. After 24 to 48 months, they try to settle your debts in bulk.

Their fees usually run 15 to 25 percent of your total enrolled debt. So a $20,000 case can cost $3,000 to $5,000 in fees alone. During the wait, your credit gets hammered, and Discover may sue before the company ever calls them.

Nonprofit credit counseling agencies work differently. The largest network is the National Foundation for Credit Counseling (NFCC), which connects you with member agencies that are nonprofit.

A counselor reviews your full budget for free, then may set up a debt management plan. Under a DMP, you make one monthly payment to the agency, which sends it to Discover and your other cards. Interest rates often drop to 6 to 10 percent. Fees are usually small, around $25 to $50 a month total.

For most people in early or mid-stage trouble, a nonprofit DMP is safer and cheaper. A debt settlement company makes more sense only if your debt is already charged off and you cannot afford full DMP payments.

What to Do If Discover Rejects Your Settlement Offer

A “no” is not the end. It is just the start of round two. Many successful settlements happen after one or two rejections.

If Discover turns you down, take these steps in order:

- Ask why. Was the offer too low? Was your hardship not documented enough? Was the timing wrong?

- Wait 30 to 60 days. Time often moves your account closer to being charged off, which boosts your bargaining power.

- Improve your file. Send better hardship proof. Add a doctor’s note, a layoff letter, or new bank statements.

- Raise the offer slightly. Move from 25 to 35 percent, or from a lump sum to a short payment plan.

- Try a hardship program instead. If full settlement is off the table, ask for the 60/60 plan or a temporary rate cut.

- Call back and ask for a supervisor. Frontline agents have lower approval limits than team leads.

- Get outside help. Talk to a nonprofit credit counselor for a free review of your options.

If all of this fails and a lawsuit is coming, talk to a consumer protection attorney. Many offer free first calls. In states with strong consumer laws, an attorney can sometimes settle for less than you could on your own.

Frequently Asked Questions (FAQs)

Will Discover Card settle credit card debt?

Yes, Discover does settle credit card debt, especially once your account is 90 to 180 days past due. Most settlements land between 40 and 60 cents on the dollar, and Discover is more willing to negotiate when you can document a real financial hardship.

What percentage will Discover settle for?

Discover typically settles for 40 to 60 percent of the balance owed, though some accounts settle as low as 25 to 30 percent when the debt is old or the borrower is clearly insolvent. Lump sum offers get the biggest discounts; payment plan settlements usually land closer to 60 to 70 percent.

Will Discover sue me for credit card debt?

Discover is one of the more aggressive issuers when it comes to lawsuits, and it typically files suit after the 180-day charge-off if no payment or settlement plan is in place. Ignoring a summons leads to a default judgment, which can result in wage garnishment or a bank account freeze, depending on your state.

How to get the Discover hardship program?

Call the number on the back of your card and ask specifically for the hardship or loss mitigation department. Discover may lower your interest rate, reduce your minimum payment, or offer the 60/60 plan, but you must explain your hardship clearly and be ready to show proof like a layoff letter or medical bills.

What is Discover’s 60/60 plan, and how do I qualify?

The 60/60 plan reduces your balance by up to 40 percent, and you repay the remaining 60 percent over 60 months at a very low or zero interest rate. You generally need to be at least 90 to 120 days past due and able to prove you cannot pay the full balance, but can maintain a smaller fixed monthly payment.

Will a debt collector settle for 30 percent?

A 30 percent settlement is possible but uncommon with Discover directly, usually reserved for very old debt or cases of proven insolvency. Starting your offer at 25 to 30 percent is a smart negotiating move, since Discover agents often open at 70 to 80 percent, and the final deal typically meets somewhere in the middle.

Does Discover give second chances?

Discover is considered one of the more consumer-friendly issuers when you reach out early and explain a genuine hardship. Calling before you miss a payment can unlock interest rate reductions and flexible plans that are no longer available once your account is severely past due.

Will Discover forgive my credit card debt?

Discover does not forgive debt simply because you ask, but it will cancel a portion of what you owe through a formal settlement once you can prove full repayment is not possible. Any forgiven amount of $600 or more is reported to the IRS on Form 1099-C and counts as taxable income unless you qualify for the insolvency exclusion.

What happens if I don’t pay my Discover credit card?

Missed payments trigger late fees, rate increases, and credit score damage, and Discover begins settlement discussions around 90 to 120 days past due. At 180 days, the account is charged off, and Discover typically refers the file to outside counsel, which significantly increases the risk of a lawsuit.

Can you still negotiate with Discover after a lawsuit is filed?

Yes, and some of the best settlements happen after a lawsuit is filed, often at 50 to 70 percent of the judgment amount. You must file a written answer with the court within 20 to 30 days to avoid a default judgment, then negotiate directly with the law firm handling the case rather than with Discover.

Bottom Line

We’ve walked through every part of working out a Discover balance, from the 60/60 plan and call scripts to credit score effects, tax forms, and what to do if a lawsuit lands on your doorstep. The most effective approach is to act early, document your hardship, and put every agreement in writing before paying a cent.

For most readers, talking directly with Discover and getting a written offer will yield the best results. This way, you avoid middleman fees and stay in control.

If you know someone losing sleep over Discover collection calls or a recent court summons, share this guide. It could save them thousands of dollars and months of stress.