I’ve been there, standing at a tiny café in Florence with a Discover card in my hand and a tired waiter shaking his head. You don’t want that on day one of your trip. The truth is, Discover card acceptance varies. A card that works well in the US may not be accepted just a few streets from your hotel in Europe.

The short answer is this: Discover works very well in a few countries, poorly in most of Europe, and almost not at all in some.

This guide shows you exactly where your card will work, why acceptance varies, and how to set up a smart backup plan before you board your flight.

Key Takeaways

This guide explains whether Discover cards work internationally, covering acceptance tiers by country, the network fee differences driving refusals, partner network workarounds, and how the Capital One-Discover merger affects travelers in 2026.

Core Facts:

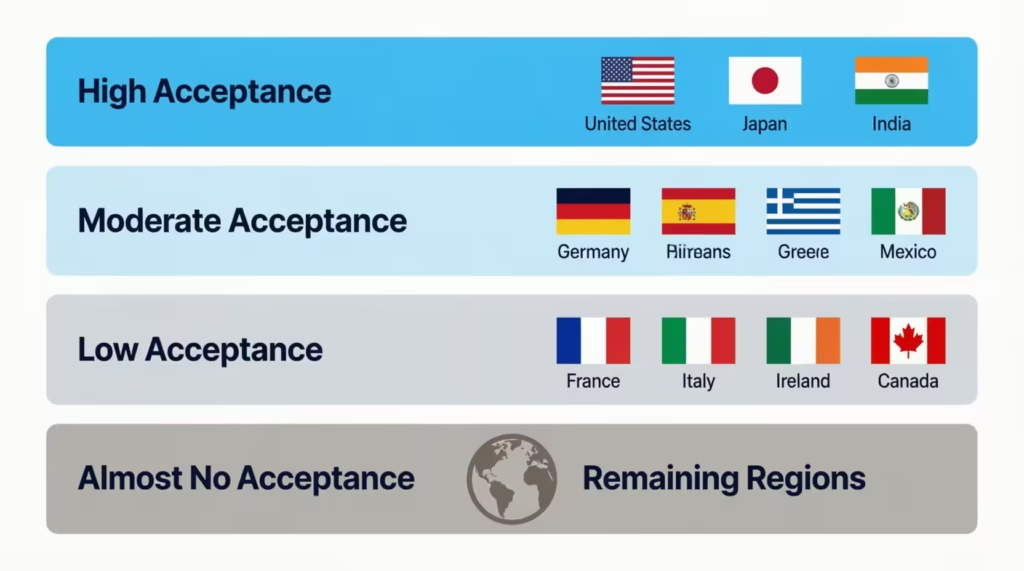

- Discover acceptance varies by tier: high in the United States, Japan, and India, moderate in Germany, Spain, and Greece, and low in France, Italy, Ireland, and most of Canada and South America.

- Discover charges merchants roughly 3% per transaction compared to about 2% for Visa and Mastercard, which discourages smaller merchants abroad from accepting it.

- Four partner networks extend Discover’s reach: Diners Club International, JCB in Japan and parts of Asia, UnionPay in mainland China, and RuPay in India.

- Discover charges no foreign transaction fees, but merchant refusal, not cardholder fees, is the main barrier to using it abroad.

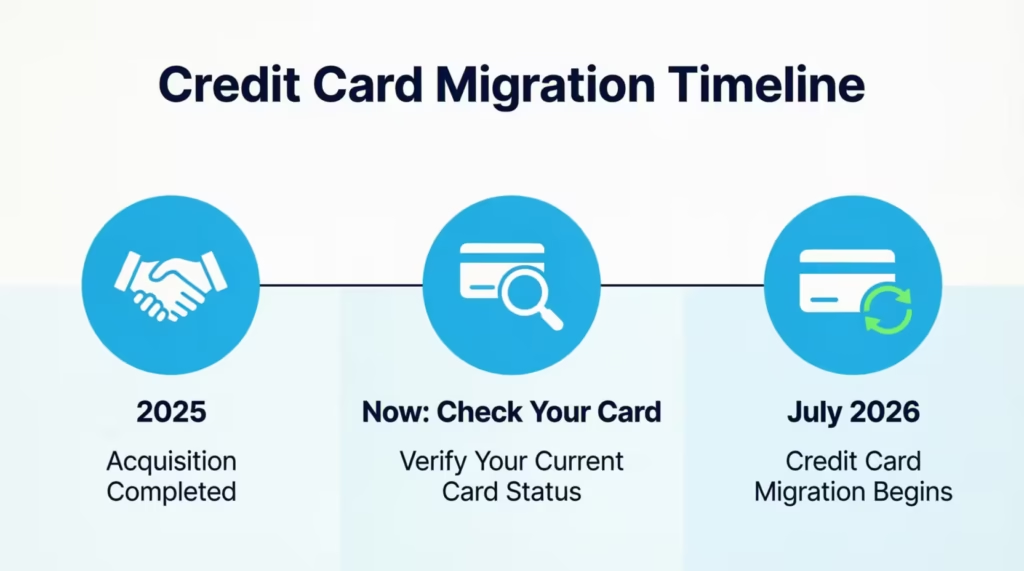

- Capital One completed its acquisition of Discover in 2025, and credit card migrations to the Discover network are expected to begin in July 2026.

- Recommended pre-trip steps include checking the Discover acceptance map, setting a travel notification, loading a mobile wallet, and packing a no-foreign-fee Visa or Mastercard as backup.

Best for:

- Travelers deciding whether to rely on a Discover card as their primary payment method abroad.

- Capital One cardholders trying to determine if their card is shifting to the Discover network ahead of the 2026 migration.

- Travelers heading to Japan, India, or China who want to use Discover’s strongest partner network coverage.

Where Discover Is Accepted Around the World

Discover says its network reaches more than 200 countries and territories, and the Discover Global Network reports acceptance in 185+ countries through its partner networks. That sounds huge.

In practice, the experience on the ground is much more uneven, because “accepted in a country” does not mean “accepted at the corner bakery.” Discover Global Network confirms this footprint, but the merchant count varies wildly by region.

To plan a trip, it helps to sort countries into four simple tiers based on real cardholder experience.

High acceptance. Your card works at most card-accepting merchants. This tier includes the United States, Japan (through the JCB partnership), and India (through the RuPay partnership). In these places, you can usually rely on Discover as your main card.

Moderate acceptance. Your card works at major hotels, big chains, airports, and tourist spots. It often fails at small shops, taxis, family restaurants, and rural businesses. This tier covers Germany, Spain, Greece, parts of the United Kingdom, Mexico, and parts of the Caribbean.

Low acceptance. Your card may work at a handful of luxury hotels and tourist chains, but you should not plan around it. This tier includes France, Italy, Ireland, Canada (outside Walmart and a few chains), and most of South America.

Almost no acceptance. Discover is so rare that you should treat it as a backup, not a main card. This includes many countries in Africa, Central Asia, and parts of Southeast Asia outside major hotel chains.

📌 Did You Know: A “country count” of 200+ does not reflect how often a card is taken in daily life. In France, for example, Discover may show up in the country list but still be turned away by most cafés, taxis, and small shops.

Why Discover Acceptance Varies So Much by Country

Acceptance comes down to one boring thing: cost to the merchant. Every time you swipe or tap a card, the shop pays a fee. Visa and Mastercard charge merchants around 2% per transaction in many areas.

Discover usually charges about 3%, depending on the agreement. Outside the US, shops that already pay low local network fees see no reason to add a more expensive option that few tourists carry. That gap is the simple reason your card gets refused. Global Payments breaks down this cost difference in detail.

There’s also a habit problem. In countries where most locals carry Visa, Mastercard, or a local card (like Carte Bancaire in France or Interac in Canada), shop staff are simply not trained to spot a Discover logo.

Even when the terminal could, in theory, take it through a card network partnership, the human at the till may say “we don’t take that” before trying. So, the merchant acceptance rate is shaped by both card fees and staff awareness.

The good news: Discover has built a wide web of partner deals to close some of these gaps. That brings us to the regional picture.

Is Discover Accepted in Europe?

Europe is a mixed bag. Some countries treat Discover almost like Visa, while others treat it like a strange American novelty. Big hotels, airline counters, and global chains like Hilton, Marriott, Starbucks, Apple Store, and Zara are found all over Europe. Small cafés, family restaurants, taxis, public transport, and corner shops often do not.

Discover also has a long-standing tie with Diners Club International, which is more common in Europe than you’d think. When a shop window shows the Diners Club logo, your Discover card should work there too. It’s worth scanning the terminal for that small circle logo before you panic.

Italy

Acceptance in Italy is patchy. Big hotels in Rome, Milan, and Florence often take Discover. Outside that, most trattorias, gelaterias, taxis, and small museums will reject it. Pack a Visa or Mastercard as your daily driver and treat Discover as a backup for big-ticket items like a hotel bill or a car rental from a major brand.

Spain

Spain leans a bit more friendly than Italy. Major chains, large hotels in Madrid and Barcelona, and tourist-area restaurants on the Costa del Sol often accept it. Small tapas bars, local markets, and family pensions usually don’t. Carry euros for small spends and keep Discover for hotels, big retailers, and El Corte Inglés.

Greece

Athens, Santorini, and Mykonos accept Discover at many large hotels, ferry desks, and bigger restaurants. Once you get to small islands or village tavernas, expect mostly cash or a Visa terminal. ATMs that accept Discover exist in Greece, but are not on every corner, so plan cash withdrawals around the big cities.

Germany

Germany is one of the better discovery countries in Europe. Most large stores, hotels, and chain restaurants in Berlin, Munich, Frankfurt, and Hamburg take it. Germans, though, love cash and direct debit (Girocard), so even Visa can fail at a small bakery. Bring euros for the same reason locals do.

France

France is the weakest of the major European tourist countries for Discover. Even some five-star hotels in Paris will quietly route you to a Visa or Mastercard reader. Outside Paris, acceptance drops sharply. If France is your only European stop, don’t rely on Discover at all. Bring a no-foreign-fee Visa or Mastercard as your main card.

Ireland

Ireland is hit or miss. Dublin Airport, big hotels, and some pubs in tourist areas take it. Rural pubs, B&Bs, and bus operators in the countryside usually don’t. Since Ireland mainly uses Visa, Mastercard, and contactless debit, consider Discover as your backup card, not your main one.

💡 Pro Tip: Before you sit down at any restaurant in Europe, ask “Do you accept Discover?” while you’re still standing. It is far easier to walk out than to wash dishes.

Is Discover Accepted in Canada?

Canada has a mixed reputation, and the reports you read online are often outdated. The honest 2026 picture: Find work at Walmart Canada, many big hotel chains, major car rental brands, airports, and some large tourist spots. It is rarely taken at small shops, Tim Hortons (varies by location), corner stores, cabs, and many restaurants outside hotels.

Canadians have moved heavily to contactless Visa and Mastercard debit, so unfamiliar logos get turned away fast. Plan to bring a Visa or Mastercard as your main card in Canada and use Discover only at the chains you’ve checked in advance.

Is Discover Accepted in Asia?

Asia is where Discover quietly shines, thanks to two big network partnership deals.

Japan

Japan is the single best country in the world for Discover acceptance outside the US. The JCB alliance, signed in 2008, means that any merchant displaying the JCB logo accepts Discover, too. That covers a huge share of Tokyo, Osaka, Kyoto, and even smaller cities. You’ll see the JCB sticker on convenience store doors, ramen shop windows, taxi dashboards, and hotel front desks. Tap or insert your Discover card, and it usually works without a word.

India

India is another strong country, thanks to the RuPay partnership. RuPay is the local network used by hundreds of millions of Indian cardholders, so its logo is everywhere. When you spot “RuPay accepted” in a shop in Mumbai, Delhi, Bengaluru, or Goa, your Discover card should work. Smaller cash-only shops still exist, especially in markets, so carry rupees for street food and rickshaws.

For China, the UnionPay deal lets Discover be used at many UnionPay merchants and ATMs. This includes over 4 million merchants on the mainland, according to Discover’s partner data. Acceptance is best at hotels, department stores, and ATMs. Mobile wallets dominate daily payments in China, so a backup card and some yuan are still smart.

Network Partnerships That Expand Where You Can Use Discover

These deals are the real engine behind Discover’s international story. Knowing them changes your behaviour at the counter. You can spot a partner logo and feel sure your card will work.

The four main partners to memorize:

- Diners Club International — global, with strong reach in Europe and parts of Latin America. The compact “DC” inside a circle is the logo to watch for.

- JCB — Japan and growing across East and Southeast Asia. Look for the green, red, and blue stripes inside a small box on terminals and shop windows.

- UnionPay — mainland China, plus growing reach across Asia and parts of Africa. The blue, red, and green block letters “UnionPay” are easy to spot.

- RuPay — India only. The orange and green wordmark is on most ATMs and many store doors.

If the merchant displays any of these four logos and not the Discover logo, your card should still go through. Politely ask the cashier to run it as JCB, UnionPay, RuPay, or Diners Club, depending on which logo you see. If the terminal struggles, ask them to try the chip or contactless route, since some older swipe-only terminals fail to recognize the partner routing.

How the Capital One–Discover Network Switch Affects International Travel

Capital One completed its acquisition of Discover in 2025, and the migration of cards onto the Discover network is still rolling out. Capital One’s investor announcement confirms the deal’s close, while credit card migrations to the Discover network are expected to begin in July 2026. For travelers, three things matter.

First, if your old Capital One debit card was on Mastercard and is now on Discover, your card will face the same international quirks Discover has always had. The Mastercard you trusted in Paris last year may now be a Discover network card that gets refused at the same café. Check the back of your card for the small network logo before you fly.

Second, certain US merchants that don’t take Discover, most famously Costco, will also refuse a Capital One card once it moves to the Discover rails. That isn’t an international issue, but it surprises people who use their card at a Costco near their hotel in Iceland or Korea.

Third, fraud rules at Capital One and Discover are merging during migration, and some travelers have reported extra holds during the switch. Set a travel notice and keep your phone reachable.

Action step: Log in to your Capital One or Discover app. Check the card network on your account page. If it says Discover, plan your trip as a Discover cardholder would, not a Mastercard holder.

⚠️ Mistake to Avoid: Don’t assume your Capital One Mastercard will still be a Mastercard abroad in 2026. Check the network logo on the card itself before you pack.

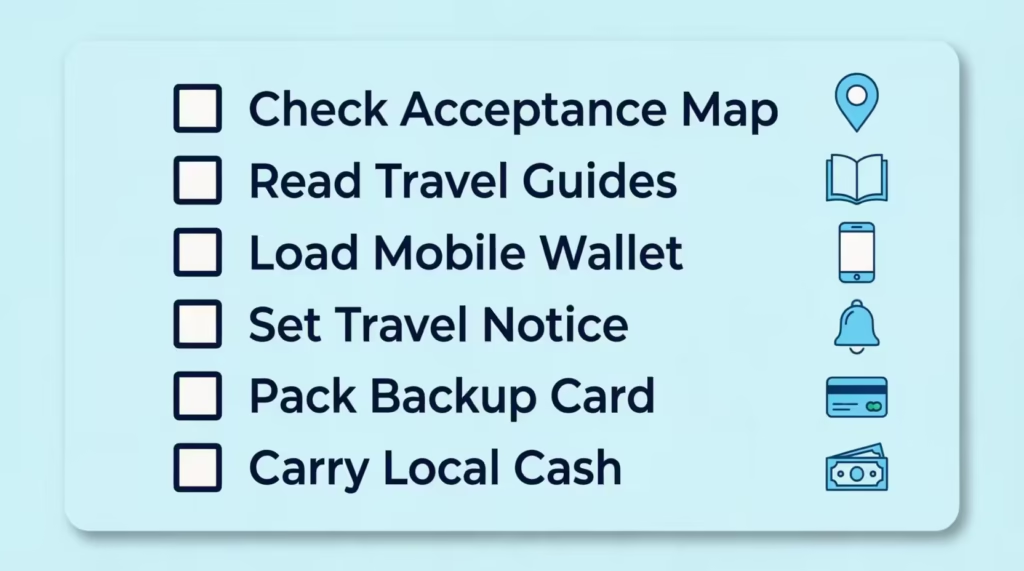

How to Check Discover Acceptance Before You Travel

A 10-minute check the week before your trip can save you a stressful day on arrival. Run through these steps in order.

1. Use the official Discover acceptance map. Visit Discover’s international acceptance page and search for your destination country. The map shows partner networks, common merchant types, and ATM access. It will not list every shop, but it will tell you which logos to look for.

2. Search the Discover Global Network travel guides. The travel guides site shows popular merchants in major destinations, so you can see in advance which hotels, restaurants, and stores are likely to accept your card.

3. Pre-load mobile wallets. Add your Discover card to Apple Pay or Google Wallet before you fly. Many international terminals accept contactless payments from your phone. Sometimes, a card might get refused when swiped, but the wallet can connect through a partner network behind the scenes.

4. Set a travel notification. In the Discover or Capital One app, open the card settings and add the countries and dates of your trip. This step alone prevents most “declined for fraud” surprises.

5. Pack a backup card. Bring a Visa or Mastercard with no foreign transaction fees as your daily driver in low-acceptance regions. Discover already has no foreign transaction fees, which is great, but a card that simply gets refused saves you nothing.

6. Carry a small amount of local cash. Even in card-friendly countries, taxis from the airport and tiny vendors often want cash. Pull out the equivalent of about $100 in local currency on day one from a partner-network ATM.

Avoiding Fraud Holds and Card Freezes Abroad

A travel notice is step one, but a few more habits keep your card alive the whole trip. Use the same card for similar spend categories so the pattern looks normal: one card for hotels, one for restaurants.

Don’t bounce between five cards in a day, since each odd transaction looks like fraud. Keep the Discover app installed and signed in, so you can lift a freeze or use the Freeze It feature yourself if something looks off.

Save the international collect-call number from the back of your card in your phone notes. This number works even if your data plan doesn’t. If a charge is declined, wait 30 seconds and try once more before walking out, since many holds clear on the second attempt.

What to Do If Your Discover Card Isn’t Accepted

It will happen at least once on a long trip. Stay calm. Run through this order, in this order, and you’ll seldom be truly stuck.

Try a different format of the same card first. If your chip insert fails, try tap-to-pay from your phone wallet. If contactless fails, ask the cashier to manually key in the card. Many terminals route partner networks better through one method than another.

Use your backup card. A no-foreign-fee Visa or Mastercard is the simplest fix. Pull it out, pay, and move on. This is why every traveler should carry two different networks.

Use a mobile wallet on the backup card. Apple Pay or Google Wallet with your backup Visa or Mastercard works at almost any contactless terminal in Europe, Canada, and Japan. Contactless payment abroad is now the default in most card-friendly countries.

Pay in local cash. Keep about a day’s worth of small bills on you. Hand the cashier exact change to avoid getting back a pocketful of unfamiliar coins.

Ask the cashier to try a partner network. If you see a JCB, UnionPay, RuPay, or Diners Club logo on the terminal or door, politely ask them to run your Discover card through that. Some staff have never tried it and are surprised when it works.

Withdraw from a partner-network ATM. If you’re truly cash-short, find an ATM that displays one of the partner logos. Discover usually waives its ATM fee for international withdrawals, but local ATM operators may still charge their own fee. Check the screen carefully before confirming.

What to Look For and Say at Checkout

Walk up to the terminal with your eyes on three places: the door sticker, the cash-register sign, and the screen of the card reader. Look for the Discover logo first. If you don’t see it, scan for JCB, UnionPay, RuPay, or Diners Club.

A simple line that works almost anywhere: “Do you accept Discover, JCB, or Diners Club?” If the answer is no, slide your backup card out before things get awkward.

If the answer is yes, hand over the Discover card with the network logo facing the reader, and let the cashier tap, insert, or swipe based on the terminal type. Speak slowly, smile, and don’t argue if it fails. A polite second try usually works, and a polite switch to your backup keeps the line moving.

Frequently Asked Questions (FAQs)

Is a Discover credit card accepted internationally?

Discover is accepted in over 200 countries and territories, but daily acceptance varies sharply by location. It works reliably in the US, Japan, and India, moderately well in Germany, Spain, and Greece, and poorly across most of Italy, France, and Canada.

Which countries don’t accept Discover cards?

Discover has almost no acceptance in much of Africa, Central Asia, and parts of Southeast Asia outside major hotel chains. France and Italy also have very low acceptance, with even some five-star hotels routing payments to Visa or Mastercard instead.

Do I need to tell Discover I’m traveling?

Yes, setting a travel notification in the Discover or Capital One app before your trip helps prevent declined charges. Add your destination countries and travel dates in the card settings to avoid fraud-related freezes.

What is the downside to the Discover card?

Discover charges merchants about 3% per transaction, compared to roughly 2% for Visa and Mastercard. That higher cost means fewer international merchants accept it, especially in Europe and Canada, where shop staff are also less familiar with the logo.

How do I avoid the 3% foreign transaction fee?

Discover already charges no foreign transaction fees, so this isn’t an issue when using it abroad. The 3% figure refers to the merchant fee Discover charges businesses, not a fee charged to the cardholder.

Why is my Discover card declining internationally?

Declines usually happen because the merchant doesn’t accept Discover’s network, not because of an account problem. Setting a travel notification first and checking for partner logos like JCB or Diners Club can resolve most other declines.

What is the best way for Americans to pay in Europe?

Carry a no-foreign-transaction-fee Visa or Mastercard as your main card, since these are accepted almost everywhere in Europe. Keep Discover as a backup for hotels and large chains, and bring some local cash for small shops and taxis.

Why is Discover not widely accepted internationally?

Discover’s higher merchant fee, around 3% versus 2% for competitors, gives shops less financial incentive to accept it. Staff in countries where Visa, Mastercard, or local networks dominate are also less trained to process Discover transactions.

How can I tell if a foreign merchant will take my Discover card without asking?

Look for the Discover logo first, then check for JCB, UnionPay, RuPay, or Diners Club logos on the door or terminal. Any of these four partner logos means your Discover card should work even without the Discover name showing.

Which credit card is best for foreign travel?

A card with no foreign transaction fees and wide acceptance, such as a major Visa or Mastercard, works best as your primary travel card. Discover works well specifically in Japan, India, and China through its JCB, RuPay, and UnionPay partnerships.

Bottom Line

A Discover card can be a great travel companion in the right places, with no foreign transaction fees and strong reach in Japan, India, and many big-chain merchants worldwide. The catch is uneven acceptance across Europe, Canada, and much of Latin America.

The most effective approach is to use Discover, where its partners are strong, such as Japan, India, and China, through UnionPay. Then, carry a no-foreign-fee Visa or Mastercard everywhere else. Add a travel notice, a mobile wallet, and a little local cash, and you’re set.

If you know someone planning a trip with only a Discover card in their wallet, share this guide with them. It could save them a very long evening at a restaurant in Paris.