Is checking Discover’s pre-approval tool going to hurt your credit score? This is a smart question to ask before you click anything. Many people worry that even looking at their options will damage the score they’ve worked hard to build. I’ve noticed this concern often, especially from readers managing their credit before a big financial decision.

The good news is clear: Discover’s pre-approval check does not affect your credit score.

Read on to learn exactly why it’s safe, when a hard inquiry does happen, and how to use pre-approval as a smart credit strategy tool.

Key Takeaways

This article explains whether Discover’s pre-approval tool affects your credit score, how soft and hard inquiries differ, when a hard pull is triggered, what credit scores qualify for pre-approval, and how to interpret your results before applying.

Core Facts:

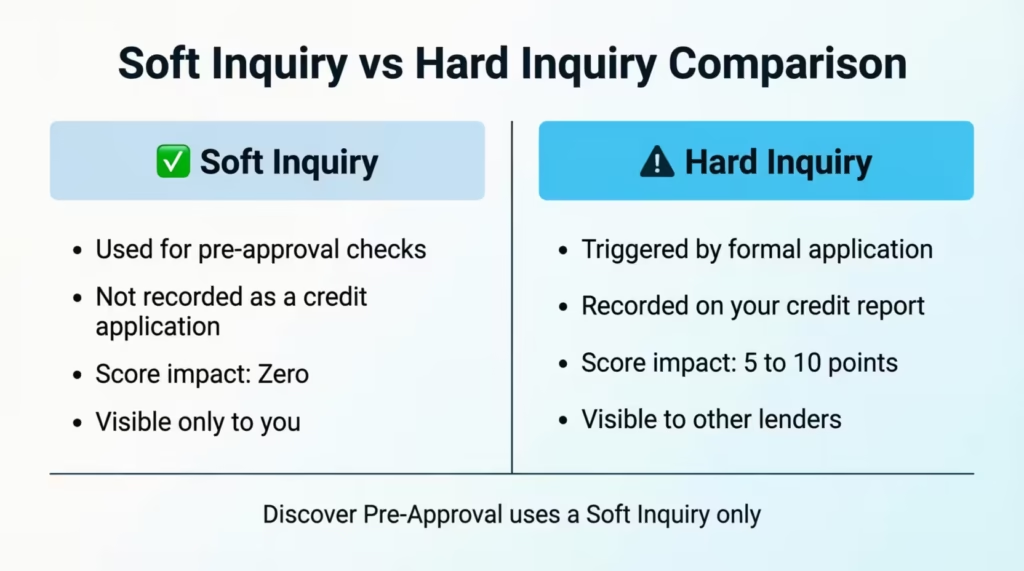

- Discover’s pre-approval check uses a soft inquiry, which does not appear as a credit application and causes zero impact to your credit score, regardless of how many times you check.

- A hard inquiry is only triggered at the moment you click Submit on a complete Discover credit card application, not during any earlier step in the pre-approval process.

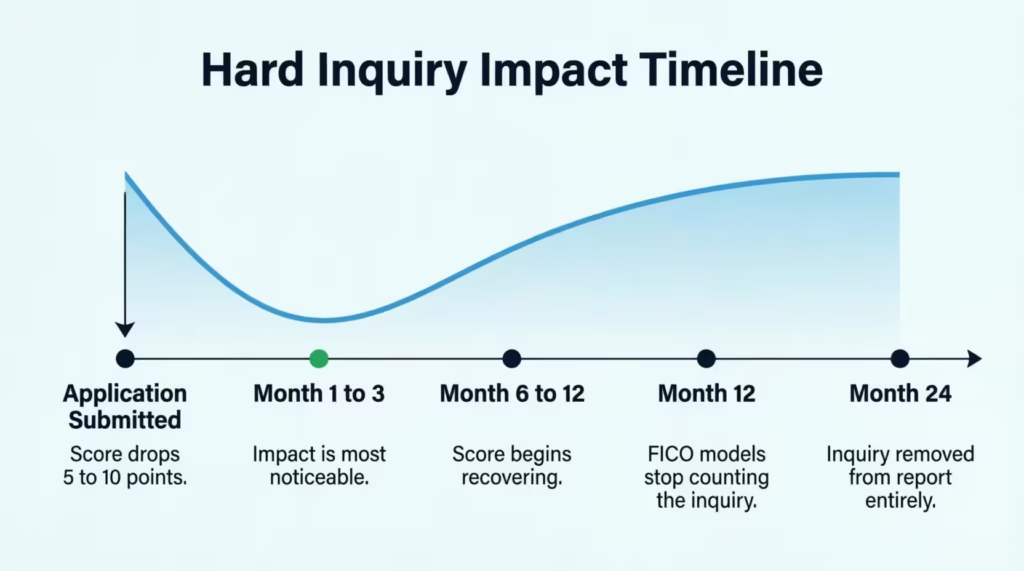

- A hard inquiry from a Discover application typically lowers a FICO Score by five to ten points and remains on your credit report for two years, though FICO models generally stop counting it after 12 months.

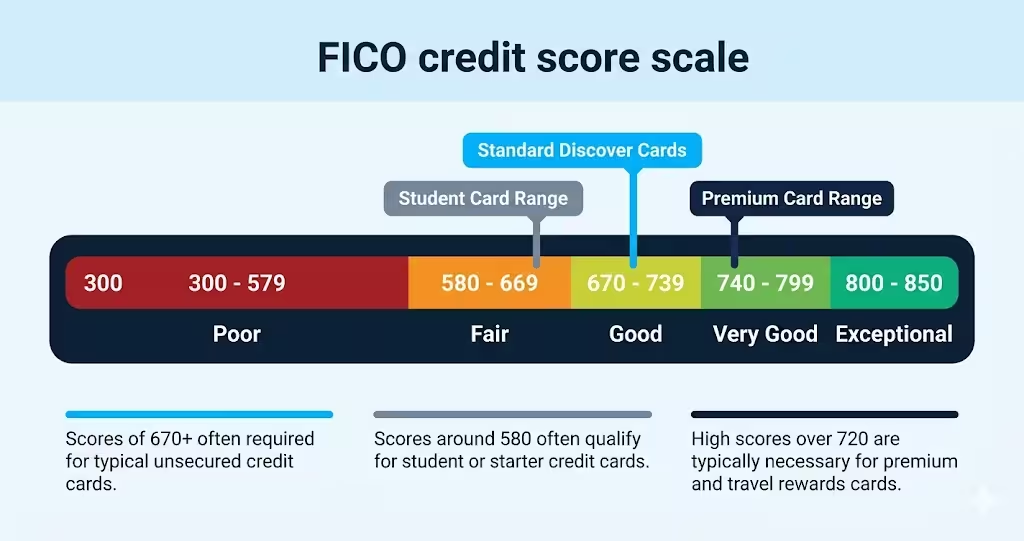

- Most standard Discover cards generally require a FICO Score of 670 or higher for pre-approval results to appear; student cards have a lower threshold, and premium cards typically require 720 to 750 or above.

- Pre-approval is a preliminary signal, not a guarantee. Formal applications also review income, debt-to-income ratio, and complete credit history, which can still result in a denial even after pre-approval.

- Each Discover application triggers its own separate hard inquiry. Credit card inquiries are not grouped the way mortgage or auto loan inquiries are, so multiple applications each count individually.

Best for:

- Anyone with a borderline credit profile who wants to gauge their Discover approval odds before risking a hard inquiry on their credit report.

- Consumers planning a major loan (mortgage, auto) in the next six to twelve months who need to protect their credit score from unnecessary hard pulls.

- First-time credit card applicants or students unsure which Discover card they qualify for and wanting to explore options without any score consequences.

Does Discover Pre-Approval Affect Your Credit Score

The short answer is no. Checking whether you’re pre-approved for a Discover card does not affect your credit score at all.

When you use Discover’s pre-approval tool on their website, Discover runs what’s called a soft inquiry on your credit file. A soft inquiry is a limited check. It lets Discover see enough of your credit profile to tell you whether you might qualify. It does not get recorded as a credit application. It does not show up as a new inquiry on your credit report in any way that can lower your score. Your score stays exactly where it is.

This applies whether you browse Discover’s pre-approval page once or return to check multiple times. The soft pull does not stack up. It causes no damage, no matter how many times it’s used.

The confusion is understandable. Most people know that applying for a credit card can ding their score. So it makes sense to wonder if the pre-approval step carries the same risk. It doesn’t. The pre-approval check and the formal application are two separate events, and only one of them affects your credit.

This article explains how soft and hard pulls differ. It covers when a hard inquiry occurs in Discover’s process and what pre-approval means for your chances of approval.

Soft Pull vs. Hard Pull: What Does the Difference Mean for You

A soft inquiry is a credit check that does not affect your score. It’s used when someone reviews your credit without you actively applying for new credit. Lenders use soft pulls to screen consumers for pre-approval offers. You also trigger a soft pull when you check your own credit report. Employers sometimes run soft pulls during background checks.

A hard inquiry is different. It happens when you formally apply for new credit, like a credit card, a car loan, or a mortgage. Hard inquiries are recorded on your credit report and are visible to other lenders. A hard pull can reduce your FICO Score by about five to ten points. The exact effect depends on your overall credit profile.

The important thing to know: only the formal Discover credit card application triggers a hard inquiry. The pre-approval check is a soft pull. These two steps are completely separate, and knowing where the line is gives you full control over when and whether to take the score risk.

When Does Discover Run a Hard Pull on Your Credit

Discover runs a hard inquiry only when you submit a complete credit card application. Not when you browse the pre-approval tool. Not when you see your pre-approval results. Not even when you click from a pre-approval offer to learn more about a specific card. The hard pull is triggered only at the point of formal application submission.

This is an important distinction. The pre-approval stage is a one-way check: Discover looks at a limited view of your credit file to determine if you’re likely to qualify. You haven’t applied for anything yet. You haven’t agreed to anything. You’re just gathering information, and that process is entirely score-safe.

When you do decide to move forward and submit a full application, Discover will pull your credit report from one of the three major credit bureaus. Discover usually gets information from Equifax or TransUnion.

This can change based on where the applicant lives and their credit profile. Some applicants report pulls from a single bureau; others report pulls from two. This isn’t something Discover publicly specifies in advance, but it’s worth knowing that the hard pull is real and will appear on your report.

⚠️ Mistake to Avoid: Don’t assume that clicking “Apply Now” from a pre-approval results page is still part of the soft-pull stage. The moment you submit a complete application, the hard inquiry is triggered. Decide before you click submit, not after.

The Exact Moment the Hard Inquiry Is Triggered

The hard pull happens when you click Submit on the full Discover credit card application form. That’s the moment of no return.

Everything before that point is safe. Visiting Discover’s pre-approval page is safe. Entering your personal details into the pre-approval form is safe. Reviewing the cards, Discover shows you as a pre-approved option, which is safe. Clicking through to read more about a specific card is safe.

After you finish the credit card application, you need to provide your full Social Security number. You also need to include your income, housing costs, and other financial details. Finally, you submit the application. Then, Discover asks for your full credit file from a bureau. That’s the hard inquiry.

Knowing this gives you a real advantage. You can explore your options completely before committing. If you’re not ready to apply today, you can use pre-approval to see where you stand and come back when the timing is right.

Can You Check Discover Pre-Approval Multiple Times

Yes, you can check Discover’s pre-approval tool as many times as you want without any penalty to your score. Because each check uses a soft inquiry, there’s no accumulation of damage. Five checks and one check have the same impact on your score: zero.

This is genuinely useful if your credit situation changes over a few months. You can check for pre-approval in January. Results may be limited. Then, work on improving your credit profile. Check again in April to see if better options are available. None of those checks will cost you a single point.

The only caveat: if you decide to submit a formal application multiple times, each submission triggers its own hard inquiry. More on that in a later section.

What Discover Pre-Approval Actually Means and What It Does Not

Pre-approval is a preliminary signal, not a guarantee. Discover looked at a part of your credit profile using a soft pull. They found that you meet some basic criteria for the card. That’s a meaningful piece of information, but it’s not the same as being approved.

During the pre-approval check, Discover looks at a snapshot of your credit history. This is a lighter review than what happens during the full application process. It’s enough to filter out people who clearly wouldn’t qualify, but it doesn’t capture everything a full underwriting review does.

When you formally apply, Discover runs a complete review. This includes a hard pull of your credit report. It also means checking your income, looking at your debt-to-income ratio, and checking for any negative marks on your file. Even if you passed the pre-approval screen, the full review can still result in a denial.

Common reasons a pre-approved applicant might still be denied include:

- Income that doesn’t meet the minimum requirements for the requested card

- A debt-to-income ratio that’s too high once fully verified

- Derogatory marks, such as late payments, collections, or charge-offs, show up more clearly in the full credit report.

- Too many recent hard inquiries from other credit applications

- A credit history that’s too thin or too new for the specific card applied for

The right way to read a pre-approval result is this: it means you’ve cleared a preliminary filter. It improves your odds of approval compared to applying blind. It does not eliminate the possibility of denial.

📌 Did You Know: Discover’s pre-approval and a guaranteed approval are two different things. Think of pre-approval as passing a first interview. The final decision still depends on a deeper review.

Pre-Screened Mail Offers vs. Checking Pre-Approval Yourself

Many consumers get Discover pre-approval offers in the mail. They often wonder if these offers are different from checking online. The answer is yes, they’re triggered differently, but both use soft pulls, and neither affects your credit score.

Pre-screened mail offers are governed by the Fair Credit Reporting Act (FCRA). Under FCRA rules, Discover can purchase a list of consumers from credit bureaus based on specific credit criteria. The bureau runs a soft pull on each consumer’s file to check whether they meet the criteria. If they do, their name goes on the list. Discover then sends those consumers a pre-screened offer in the mail. You didn’t initiate this. The soft pull happened before you ever saw the offer. Your score was not affected.

Self-initiated online pre-approval works differently. You go to Discover’s website, enter your information, and Discover runs a soft pull in response to your request. You’re the one who started it, not Discover. The result is the same, though: a soft inquiry that doesn’t affect your score.

In both cases, the hard pull only occurs if you decide to formally apply. Whether you received a mailer or checked online, submitting that application is the trigger. Everything before that point is score-safe.

One additional note: if you’d prefer not to receive pre-screened credit offers in the mail from any issuer, you can opt out through OptOutPrescreen.com, which is the official FCRA opt-out service maintained by the major credit bureaus. This stops the soft-pull screening that generates those mail offers, though it does not affect your actual credit score.

What Credit Score Do You Need for Discover Pre-Approval

Discover intentionally does not share specific credit score thresholds for its pre-approval tool. The criteria they use are proprietary. That said, consumer-reported data and industry knowledge point to some reliable general ranges.

Most standard Discover cards, such as the Discover it Cash Back or Discover it Miles, usually require a FICO Score of 670 or above for pre-approval. This puts you in the “good credit” tier according to standard FICO score ranges. Consumers in the 700 to 750 range and above generally see stronger offers with better terms.

For student-specific cards, like the Discover it Student Cash Back, the threshold is lower. These cards are designed for people with limited or no credit history. A thin credit file, or even a score in the fair credit range below 670, may still return pre-approval results for these products.

For premium cards, the bar is higher. If Discover adds more products or you’re eyeing a card with great rewards or low APR, expect pre-approval to need scores between 720 and 750 or higher.

It’s also worth knowing that a credit score is only part of the picture. Discover’s pre-approval screen looks at things like credit utilization, recent inquiries, and the age of your credit history. A high score alone doesn’t guarantee pre-approval results if other factors are out of range.

If the pre-approval tool returns no offers, that’s useful information too. It means your current credit profile doesn’t meet the initial criteria for Discover cards. It’s not a rejection, and it didn’t hurt your score. It just asks you to review your credit file closely. Find out what you can improve before trying again.

How a Discover Hard Inquiry Affects Your Score and How Long It Lasts

A Discover hard inquiry, triggered when you formally apply for a card, typically lowers your FICO Score by five to ten points. The exact impact depends on your full credit profile.

If you have a long, clean credit history with no recent inquiries, the impact will likely be at the lower end of that range. If you have a short history, a thin file, or recent inquiries, the effect might be more obvious.

The hard inquiry stays on your credit report for two years. However, the actual impact on your score fades much faster. Most FICO scoring models ignore a hard inquiry after 12 months. The impact on your score usually fades even sooner.

For most consumers with established credit, a single hard inquiry from a Discover application is a minor, short-term event. If your score goes from 720 to 712 for a few months, it likely won’t affect your chances of qualifying for other credit products you need.

The calculation changes if you’re in a sensitive credit window. If you’re six to twelve months away from applying for a mortgage or an auto loan, even a small score dip can affect the interest rate you’re offered. In that case, it makes sense to use the pre-approval tool to gauge your odds first. Then, wait until after your major loan closes before applying for the Discover card.

According to FICO’s published guidance, new credit applications account for about ten percent of your overall FICO Score. That’s a meaningful but manageable factor, and a single well-timed hard inquiry isn’t a crisis for most people.

What Happens If You Apply for Discover Multiple Times

Each Discover application triggers its own separate hard inquiry. Credit card inquiries don’t get treated like mortgage or auto loan inquiries. The scoring models group those loans together over a short time, assuming you’re shopping for rates. Credit card inquiries, however, don’t follow this rule. Each one counts individually.

If Discover denies your first application and you apply again shortly after, you’ve now taken two hard inquiries. If they deny you again and you apply a third time, that’s three hard inquiries in just a few months.

The practical advice is to wait. After a Discover denial, allow at least six to twelve months before reapplying. Use that time to review the reason for denial, which Discover is required to disclose, and address those specific factors. A hard inquiry after a denial, then a quick reapplication without credit improvements, usually won’t change the result. It costs you in two ways.

How to Check Discover Pre-Approval Without Affecting Your Credit Score

Checking Discover’s pre-approval is straightforward. Every step described here uses a soft pull only, meaning your score is not affected at any point during this process.

Step 1: Go to Discover’s official website and navigate to the credit card section. Look for the “See if you’re pre-approved” option, which is typically available on the homepage or on individual card product pages.

Step 2: Click the pre-approval link. Discover will ask you to enter some basic personal information. This usually includes your full name, home address, and either the last four digits of your Social Security number or your full SSN. The specific requirement depends on the version of the tool you are using. Entering this information does not trigger a hard pull.

Step 3: Submit the pre-approval form. At this stage, Discover runs a soft inquiry on your credit file. This happens in the background. You’ll typically see results within seconds.

Step 4: Review your results. Discover will show you one or more card offers you might qualify for. If not, it will let you know there are no pre-approval offers available right now. At no point during steps one through four has a hard inquiry occurred.

Step 5: Decide whether to proceed. If you see an offer you want, the next action will be a button that takes you to the full credit card application. This is where the process changes. Once you complete and submit that application, the hard inquiry is triggered. If you’re not ready to apply today, you can close the page and return later. Your score is unchanged.

💡 Pro Tip: Screenshot or note the specific card offer shown in your pre-approval results. Discover’s pre-approval tool might show different offers each day. This depends on your credit profile and current promotions. Knowing what you were shown helps you compare if you return to apply later.

What to Do After You See Your Discover Pre-Approval Results

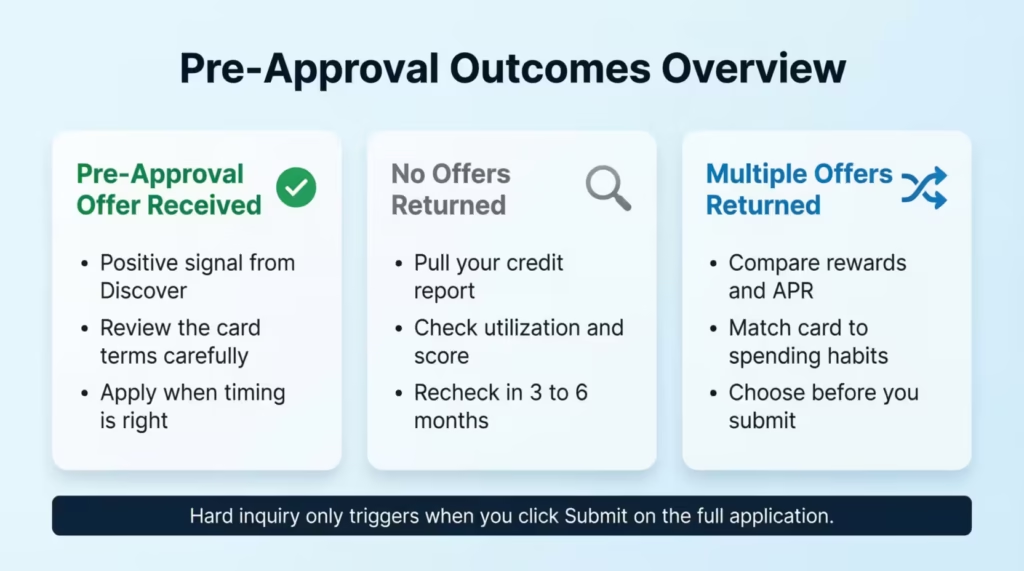

Your next step depends on which of the three outcomes you received.

Scenario 1: You received a pre-approval offer.

This is a positive signal. It means your credit profile met Discover’s preliminary criteria for that card. Review the specific offer shown: the card product, any indicated APR range, and the rewards structure.

If the card matches what you’re looking for, and your credit situation is stable, it makes sense to move forward with the formal application. Just know that approval isn’t guaranteed. The full underwriting review at the application stage will closely check your income. It will also review your debt-to-income ratio and your complete credit history. Go in with realistic expectations.

Scenario 2: No pre-approval offers were returned.

This doesn’t mean you’re permanently disqualified from a Discover card. It means your credit profile didn’t meet the preliminary filters right now. Pull your free credit report at AnnualCreditReport.com to review what might be holding you back.

Common factors are:

- A credit score under 670.

- High utilisation rates.

- Recent negative marks.

- Too many recent applications with other issuers.

Once you’ve identified the gaps, address them over the next three to six months and check again. Because each check is a soft pull, checking again later costs you nothing.

If you’re new to credit and no Discover cards are showing as pre-approved, consider whether the Discover it Secured Card might be an option. Secured cards help build credit and usually have different criteria than unsecured cards.

Scenario 3: Multiple offers were returned.

Compare the options based on what matters most for your situation. If you want cash back on everyday spending, the Discover it Cash Back is the standard recommendation. If you’re a student, the Discover it Student Cash Back is built for your profile.

If you want travel rewards, compare the Discover it Miles option against its current welcome bonus. Choose the card that fits your actual spending habits, not the one with the highest headline number.

In all three scenarios, the rule is the same: make your decision before you submit the application. Once you click submit, the hard inquiry is on your record.

Is Discover Pre-Approval Worth Using

Yes, and here’s why: it keeps you safe from a hard inquiry on a long-shot application.

If your credit profile is borderline for a given Discover card, the pre-approval tool acts as a soft-pull filter. If no offers appear, that’s a signal to wait. Applying anyway would cost you a hard inquiry and likely result in the denial you were trying to avoid. That’s a two-sided loss.

When pre-approval does show results, it’s a genuine indication that the application is worth submitting. It won’t guarantee approval, but it can really boost your chances compared to applying without a prior check.

Pre-approval has its limits. If your credit profile is on the edge of qualifying, the soft-pull screen might show offers. However, these offers may not be confirmed by the full underwriting review. In that case, pre-approval is still useful information, but you should go in knowing the full application outcome isn’t certain.

Frequently Asked Questions (FAQs)

Does Discover pre-approval affect your credit score?

No. Discover uses a soft inquiry for pre-approval, which does not appear as a credit application and causes zero impact to your score. Only a formal credit card application triggers a hard pull.

How much does your credit score go down when you get pre-approved for a Discover card?

Nothing changes during pre-approval because it uses a soft inquiry. If you move to a full application, expect a drop of about five to ten points from the hard inquiry. This depends on your overall credit profile.

What credit score do you need for Discover pre-approval?

Most standard Discover cards, like the Discover it Cash Back, usually require a FICO Score of 670 or more for pre-approval. Student cards have a lower threshold and may return offers for consumers with limited or fair credit.

Which credit bureau does Discover pull from when you formally apply?

Discover typically pulls from Equifax or TransUnion, though the specific bureau can vary based on your location and credit profile. Some applicants report a pull from one bureau; others see pulls from two.

How long does a Discover hard inquiry stay on your credit report?

A hard inquiry from a Discover application remains on your credit report for two years. However, FICO scoring models generally stop counting it against your score after 12 months, and the actual score impact usually fades before that.

Can you reapply to Discover after being denied?

Yes, but waiting at least six to twelve months is strongly advisable. Each new application creates a separate hard inquiry. If you reapply quickly without fixing the denial reasons, you often get the same result and it can hurt your score more.

Does a Discover pre-approval offer expire?

Discover does not publicly specify an expiration window for pre-approval results. Re-check the tool regularly. Your credit profile changes, and card promotions update. Don’t assume past results still show current offers.

Does opting out of pre-screened mail offers through OptOutPrescreen.com affect your credit score?

No. Opting out stops credit bureaus from sharing your info with issuers for marketing. It won’t create an inquiry or change your credit file, so it won’t affect your score.

Wrapping Up

Based on how Discover’s process works, checking pre-approval is one of the safest steps a credit-conscious consumer can take. It uses a soft inquiry, so it won’t affect your score. Plus, it provides useful information before you make any decisions. A hard inquiry happens only when you submit a formal application. Knowing this helps you plan confidently.

For most readers, start with the pre-approval tool. Check your results, then decide if the timing and offer suit you. If your results look strong and your credit window is clear, move forward. If no offers appear, use that signal to review your credit file and return in a few months at no cost to your score.

If this breakdown cleared up any confusion, share it with a friend or family member who is also making credit card choices. It could help someone avoid missing a great card due to worry. It can also stop them from applying at the wrong time without knowing the risks.