When I first looked at my Discover card statement and saw an interest charge that didn’t match the rate I thought I had signed up for, I felt that same flicker of confusion many cardholders feel. The advertised range was wide. The actual rate wasn’t obvious. And nobody had clearly explained how the Discover credit card interest rate is set, why it changes, or what I could do about it.

The short answer: your Discover APR is a variable rate linked to the U.S. Prime Rate. It includes a margin set when your account was approved. You can often request a reduction.

Below, you’ll find every active card’s current rate range, how the math actually works on your balance, where to find your personal APR, and a script that has helped real cardholders lower their rate.

Key Takeaways

This guide explains how the Discover credit card interest rate works, including how your personal APR is set using the Prime Rate formula, how daily compounding calculates your monthly charge, what the four APR types cover, and how to request a rate reduction.

Core Facts:

- Discover’s purchase APR is variable and built from two components: the current U.S. Prime Rate plus a personal margin fixed at account approval. If the Prime Rate drops, your APR drops by the same amount automatically.

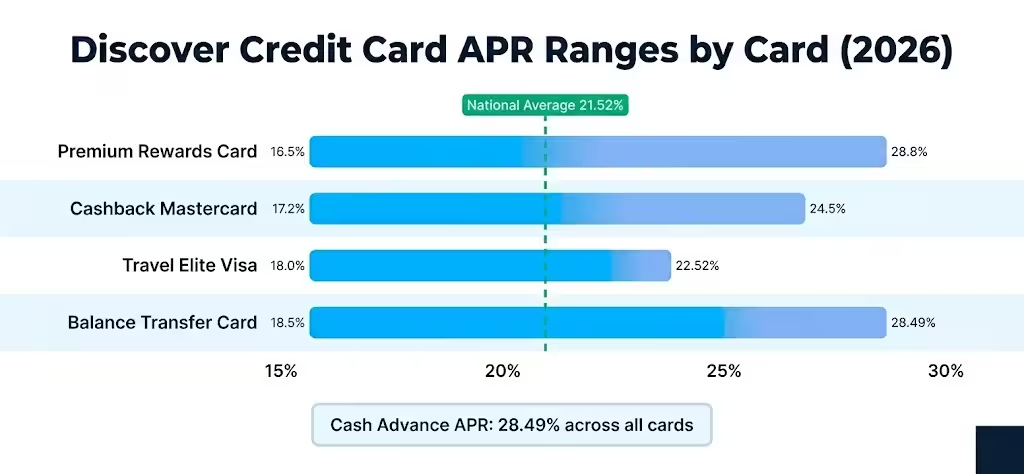

- The published purchase APR range runs from 17.49% to 26.49% variable. Your position within that range is determined by your credit score, income, debt load, and credit history length at the time of application.

- Discover applies interest daily using the Daily Periodic Rate (APR divided by 365), then multiplies by your average daily balance. A $1,000 balance at 20% APR costs approximately $16.44 in interest over a 30-day billing cycle.

- The cash advance APR is 28.49% variable across all Discover cards, with no grace period. Interest begins accruing on the day of the advance, plus a fee of the greater of $10 or 5% of the amount advanced.

- Discover does not charge a penalty APR for late payments, which sets it apart from many major issuers. A late payment can, however, cancel an active 0% intro APR offer, triggering the standard variable rate on the remaining balance immediately.

- Cardholders with at least 12 months of on-time payment history can request an APR reduction by calling 1-800-347-2683 or using the online chat inside the account dashboard. Possible outcomes include a permanent reduction, a temporary rate decrease, or a decline.

Best for:

- Discover cardholders carrying a balance who want to understand exactly why they are being charged a specific interest amount and how to calculate it themselves.

- Anyone considering requesting an APR reduction who wants to know the eligibility conditions, what to say, and what outcomes to expect before making the call.

- Prospective applicants comparing Discover’s rate range against the national average of 21.52% to assess whether Discover is a competitive option for their credit profile.

Discover Credit Card APR Rates by Card (2026)

Discover publishes a range, not a single number, for every card. The rate you receive sits somewhere inside that range based on your credit profile. All standard purchase rates are variable, which means they move when the Prime Rate moves.

Here are the current published ranges for the active Discover lineup:

| Discover Card | Standard Variable Purchase APR | Intro APR Offer | Cash Advance APR |

|---|---|---|---|

| Discover it® Cash Back | 17.49% – 26.49% variable | 0% intro for 15 months | 28.49% variable |

| Discover it® Chrome | 17.49% – 26.49% variable | 0% intro for 15 months | 28.49% variable |

| Discover it® Miles | 17.49% – 26.49% variable | 0% intro for 15 months | 28.49% variable |

| Discover it® Secured | Standard variable purchase APR | No intro APR | 28.49% variable |

| Discover it® Student Cash Back | Standard variable purchase APR | 0% intro for 6 months | 28.49% variable |

| Discover it® Student Chrome | Standard variable purchase APR | 0% intro for 6 months | 28.49% variable |

Two things matter here. First, these are ranges, not assigned rates. You won’t know your exact annual percentage rate until your application is approved. Second, the 28.49% cash advance APR is consistent across the whole lineup, so don’t expect a better rate just because you chose a different card.

📌 Did You Know: Discover charges the same 28.49% variable APR on cash advances no matter which card you carry. There’s no “premium” card in the lineup that lowers this number.

How Discover Determines the APR You Receive

Discover determines each applicant’s position through underwriting, which creates the advertised range. Two people can apply on the same day and get very different rates.

The single biggest factor is your credit score. Applicants with excellent credit (typically 740 and up) tend to land near the lower end of the range. Applicants with fair credit usually land near the top. Income, total debt, and the length of your credit history also feed into the decision.

Here’s a simple example. Sarah, a marketing manager with a 780 FICO score and a steady salary, might be approved for a Discover it Cash Back card at around 17.49%. David, a freelance designer with a 660 score and several recent credit inquiries, could be approved for the same card at closer to 26.49%. Same card. Same product page. Very different cost.

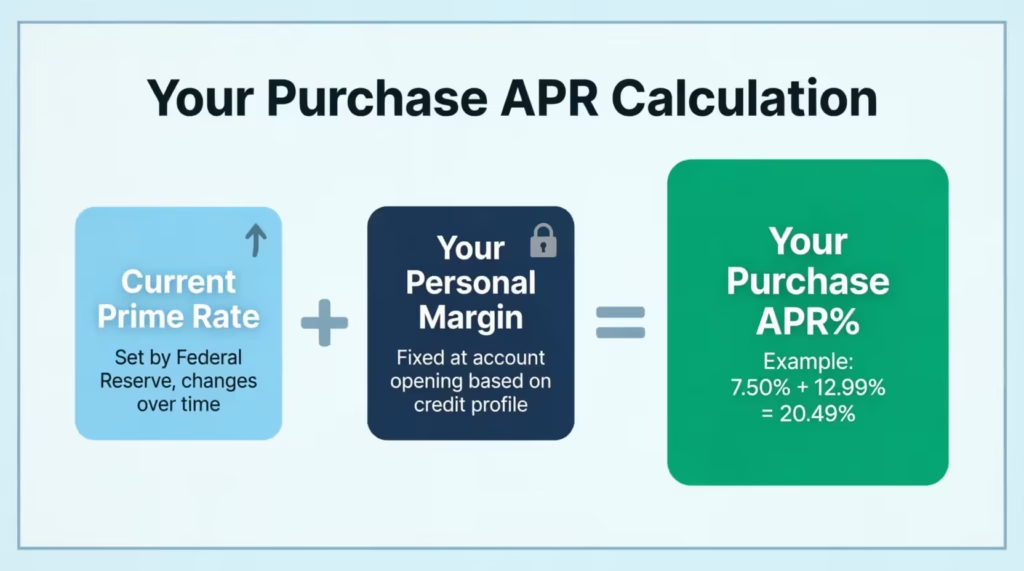

You cannot pick your rate. Discover assigns it during approval as a fixed margin above the Prime Rate, and that margin stays the same for the life of your account. What changes over time is the Prime Rate itself, not the margin.

How the Prime Rate Affects Your Discover APR

The U.S. Prime Rate is the benchmark big banks use to price loans for their most creditworthy commercial customers. It moves up or down based on decisions made by the Federal Reserve. When the Fed raises its target rate, the Prime Rate usually rises shortly after. When the Fed cuts, the Prime Rate falls.

Discover’s variable APR formula looks like this:

Your Discover APR = Current Prime Rate + Your Personal Margin

So if the Prime Rate is 7.50% and your margin is 12.99%, your purchase APR is 20.49%. If the Fed cuts rates and Prime drops to 7.00%, your APR automatically becomes 19.99%. Discover doesn’t have to send you a special notice for this kind of change because the formula was disclosed when you opened the account.

This is why your rate can shift even when you’ve done nothing different. It’s also why financial news about the Federal Reserve directly affects what you owe on a carried balance.

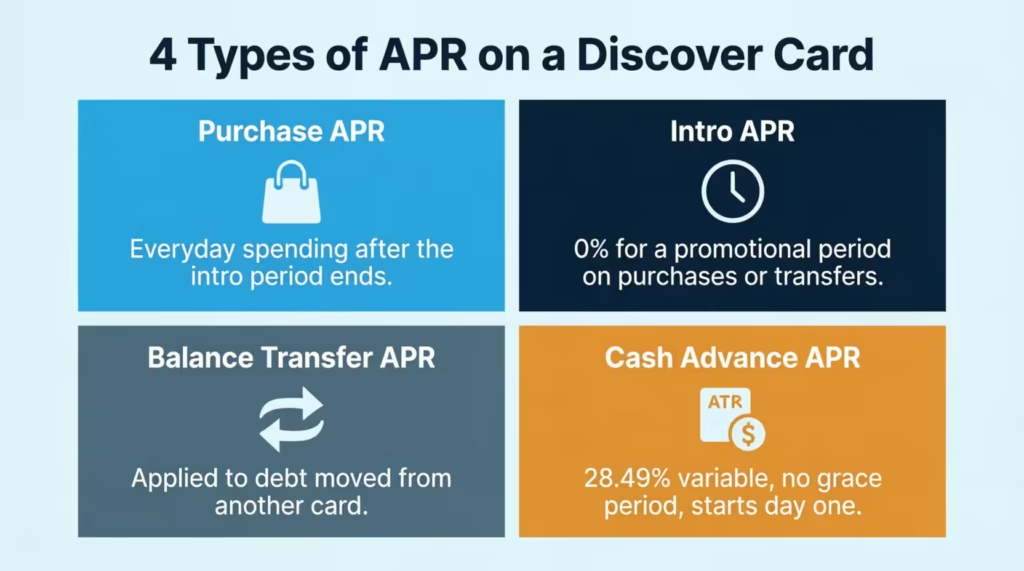

The Four Types of APR on a Discover Card

One Discover card carries multiple APRs at the same time. Each rate applies to a different kind of transaction, and confusing them can lead to surprise charges. The four types are purchase APR, intro APR, balance transfer APR, and cash advance APR.

Your purchase APR is the rate for everyday spending. This includes groceries, gas, and online shopping. It applies after the introductory period ends. This is the rate most people mean when they say “my Discover APR.” The other three rates kick in only for specific actions, and they each have their own rules.

Intro APR: What It Covers and How Long It Lasts

Discover regularly offers a 0% intro APR on new accounts. For the Discover it Cash Back, you usually get 0% on purchases for 15 months after opening your account. There’s also a separate 0% intro period for balance transfers, which can last from 15 to 18 months, depending on the current offer.

Two things to watch with intro periods. First, the 0% rate ends on a specific date, not when your balance hits zero. After that date, your standard variable purchase APR applies to anything still owed. Second, missing a payment can end the intro offer early, even though Discover does not add a penalty APR (more on that below).

Balance Transfer APR

A balance transfer moves debt from another credit card onto your Discover card. Discover often pairs balance transfers with a 0% intro APR, but the transfer itself is not free. A balance transfer fee of 3% applies during the intro period in most current offers, and up to 5% after the promotional fee window closes.

The 0% balance transfer rate only works if you transfer the balance within the qualifying window in your offer. When the intro period ends, any leftover transferred balance starts to earn interest. This is at your standard variable purchase APR.

Cash Advance APR

A cash advance is when you pull cash from your Discover card at an ATM, use a convenience check, or use the card for certain cash-like transactions. The cash advance APR is 28.49% variable, the highest rate on the card. There is no grace period on cash advances. Interest starts the day you take the cash.

You also pay a cash advance fee: the greater of $10 or 5% of the amount advanced. So a $500 cash advance costs you $25 upfront in fees, plus interest accruing daily from day one at 28.49%.

⚠️ Mistake to Avoid: Treating a cash advance like a regular purchase. A $500 cash advance carried for one month can cost roughly $25 in fees plus about $12 in interest, while a $500 purchase paid by the due date costs you nothing.

Does Discover Charge a Penalty APR?

No. Discover does not charge a penalty APR. If you pay late, your interest rate will not jump to 29.99% the way it might at other issuers. This is one of the clearest differences between Discover and most major bank-issued cards.

Discover also waives your first late fee. After that, late fees can be up to $41 per occurrence. That’s a real cost, but it’s a one-time fee, not an ongoing rate hike on your entire balance.

Industry-wide, penalty APRs have historically pushed rates as high as 29.99% on the affected balance, often for at least six months. Staying clear of that risk with a Discover card offers real protection. This is important for those whose income or schedule may lead to missed payments.

There’s one important exception to keep in mind. Missing a payment will not trigger a penalty APR, but it can end a 0% intro APR offer. If that happens, your standard variable purchase APR kicks in immediately on the remaining balance. So while you don’t face a penalty rate, you can still lose a valuable promotional rate by paying late.

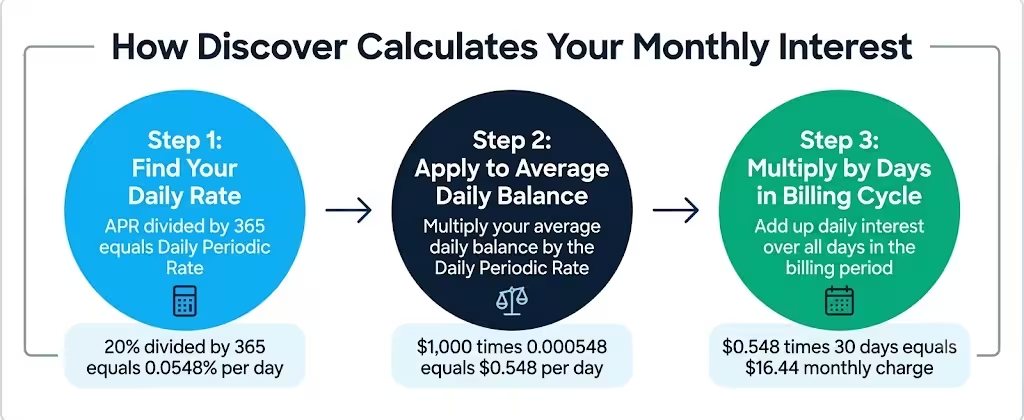

How Discover Calculates Your Monthly Interest Charge

Your APR is an annual figure, but Discover doesn’t apply it once a year. Interest is calculated daily, then added up at the end of the billing cycle. The mechanics break down into three simple steps.

Step 1: Convert APR into the Daily Periodic Rate (DPR). The DPR is your APR divided by 365.

If your purchase APR is 20%: DPR = 20% ÷ 365 = 0.0548% per day

Step 2: Apply the DPR to your average daily balance. Discover tracks your balance every day of the cycle, averages it, and multiplies that average by the DPR for each day in the billing period.

Step 3: Add it up. The daily interest amounts compound over the cycle, then appear as a single line on your statement.

Here’s a worked example. You carry an average daily balance of $1,000 at a 20% APR for a 30-day billing cycle:

- Daily interest = $1,000 × 0.000548 = $0.548

- Monthly interest ≈ $0.548 × 30 = $16.44

If you carry $3,000 instead, the monthly interest at the same rate climbs to roughly $49.32. Over a full year, the same $3,000 balance at 20% APR would cost about $600 in interest, before any new spending.

One small detail. If your interest works out to less than $0.50 for the month, Discover charges a minimum interest charge of $0.50.

What Happens to Your APR When You Carry a Balance

The moment you carry a balance from one billing cycle to the next, two things change. First, you lose your grace period. Second, interest starts compounding daily, not just on your old balance but on new purchases too, until the account is paid in full.

Daily compounding sounds harmless. It is not. Each day’s interest is added to your balance, and the next day’s interest calculation runs on that slightly larger number.

Over a year, that’s the difference between paying simple interest and paying interest on interest. This is why a $5,000 balance at 24% APR can quietly cost you more than $1,200 in a single year if you only make minimum payments.

How to Avoid Paying Interest on a Discover Card

The simplest way to pay zero interest on purchases is to pay your statement balance in full by the due date every month. Discover provides a grace period of at least 25 days from the close of your billing cycle to your payment due date. In February, that grace period is 23 days because the month is shorter.

If you pay the full statement balance during that window, you owe no interest on purchases that cycle.

Pay only the minimum, or any amount less than the full statement balance, and the grace period disappears until you pay back to zero. Cash advances are different. They have no grace period at all, so interest accrues from day one regardless of how you pay.

💡 Pro Tip: Set up autopay for the full statement balance, not the minimum. Autopay set to “minimum due” still triggers daily compounding on the unpaid portion, which defeats the purpose of paying on time.

Where to Find Your Current Discover APR

The advertised range tells you what’s possible. To see what you’re actually paying, check one of these four places.

1. Your monthly billing statement. Look for the section labeled “Interest Charge Calculation” near the bottom of your statement. It lists each APR (purchase, balance transfer, cash advance), the balance subject to each rate, and the interest charged.

2. Your online account. Sign in at Discover.com, open Statements, and download a recent PDF statement. The Interest Charge Calculation section will be there too.

3. The Discover mobile app. Open the app, tap your account, and view Account Details. Your current APRs are listed under the card details summary.

4. By phone. Call Discover customer service at 1-800-347-2683. A representative can confirm your purchase APR, balance transfer APR, cash advance APR, and the end date of any intro offer.

If you see a surprising rate on your statement, check the Interest Charge Calculation section. It will show which balance each rate applies to. That’s usually where the answer lives.

How to Request an APR Reduction From Discover

Discover does grant rate reductions, though they’re not guaranteed and they’re rarely advertised. Your odds improve when a few things are true.

You’re more likely to succeed if you have:

- A strong on-time payment history with Discover (12 months or more is ideal)

- A credit score that has improved since you opened the account

- Account tenure of at least one year

- A specific reason for the request, such as a competing offer or a high balance you’re trying to pay down

To make the request, call 1-800-347-2683 and ask to speak with someone about a rate reduction. You can also use the online chat feature inside your account dashboard, which works well for people who don’t want to negotiate over the phone.

What to say keeps it simple and respectful. A short script that works:

“I’ve been a Discover cardholder for [X years], my payment history is clean, and my credit has improved since I opened the account. I’d like to request a reduction on my purchase APR. I’ve also received offers from other issuers at lower rates, and I’d prefer to keep my business with Discover if we can adjust this.”

Saying you’ve found better balance transfer offers can prompt the representative to take action. Be ready for one of three outcomes. You might get a permanent rate reduction, a temporary lower APR (often six months), or a polite decline. If you’re declined, ask when you can try again. A “no” today doesn’t lock you out forever.

💡 Pro Tip: Call after a year of on-time payments, not in your first few months. Reps have more flexibility when your account history clearly supports the request.

How Discover’s APR Compares to the National Average

To know whether your Discover rate is competitive, you need a benchmark. The Federal Reserve publishes the average interest rate on credit card plans every quarter through its G.19 Consumer Credit report.

The most recent reading puts the average APR on accounts assessed interest at 21.52%, based on Federal Reserve data published in early 2026 by the Board of Governors of the Federal Reserve System.

A complementary view from the LendingTree analysis of the same G.19 series confirms that average APRs on accounts accruing interest moved to 21.52% in Q1 2026, LendingTree Credit Card Debt Statistics 2026.

Discover’s published range of 17.49% to 26.49% brackets the average. Here’s what that means in practice:

- Excellent credit applicants (those landing near 17.49%) sit well below the national average, making Discover a competitive option.

- Fair credit applicants (closer to 26.49%) sit above the national average, which is typical for any major issuer at that credit tier.

APR isn’t the only piece of the cost picture. Discover doesn’t charge an annual fee on any of its consumer cards, and it doesn’t add a penalty APR for late payments. Both of these reduce your total cost of ownership compared to issuers that charge $95+ annual fees or spike your rate after a single missed payment.

For a credit-aware borrower comparing options, the most useful question isn’t “Is Discover’s APR low?” It’s “Where will I personally land in their range, and what’s my total cost over a year, given how I plan to use the card?”

Frequently Asked Questions (FAQs)

What is the average APR on a Discover card?

Discover’s published purchase APR range runs from 17.49% to 26.49% variable, depending on your credit profile. The national average APR for interest-bearing accounts is 21.52%. Discover’s rates span around this average instead of being fixed.

Why is my Discover card APR so high?

Your Discover APR is built from two pieces: the U.S. Prime Rate plus a personal margin set at approval based on your credit score, income, and debt. If your credit score was in the fair range when you applied, your margin likely placed you near the top of Discover’s 17.49% to 26.49% range.

What’s a decent APR for a credit card?

The national average APR on accounts accruing interest sits at 21.52% as of early 2026. Any purchase APR below that number is seen as competitive. Rates under 18% are strong for most borrowers.

Is 24% APR on a credit card high?

At 24%, you’re sitting above the national average of 21.52%, which puts you in above-average cost territory. On a $1,000 balance carried for a year, a 24% APR generates roughly $240 in interest charges.

Is 34.9% APR bad?

Yes. At 34.9%, your rate is more than 13 percentage points above the national average of 21.52% and well above Discover’s maximum published purchase rate of 26.49%. A $1,000 balance at 34.9% carried for a full year costs roughly $349 in interest.

How much is 26.99% APR on $1,000?

Using daily compounding, a $1,000 balance at 26.99% APR over a 30-day billing cycle costs approximately $22.19 in interest for that month. Carried for a full year without paydown, the same balance generates roughly $270 in total interest charges.

What is a good APR for a 700 credit score?

A 700 credit score is usually good. It often puts applicants in the middle of a card’s APR range, not at the low end. For Discover’s lineup, that likely means a purchase APR closer to the middle of the 17.49% to 26.49% range, roughly 20% to 23%.

Does Discover charge interest on purchases during a 0% intro period?

No. During the 0% intro APR period, Discover charges no interest on purchases. Interest starts only after the promotional period ends. Then, your standard variable purchase APR will apply to any remaining balance.

What credit score do you need to get the lowest Discover APR?

Applicants with excellent credit, generally a FICO score of 740 or higher, tend to land near the lower end of Discover’s APR range. A score below 700 will typically result in a rate closer to the top of the 17.49% to 26.49% range.

Wrapping Up

The Discover credit card interest rate isn’t one number. It’s a variable rate based on the Prime Rate plus a personal margin. This rate applies daily and is divided among purchases, balance transfers, and cash advances. Discover doesn’t charge a penalty APR and waives your first late fee, making it more forgiving than many competitors. However, daily compounding can still add up quickly on any balance you carry.

Based on the math shown above, pay your full statement balance each month. This is the best strategy for most cardholders. Watch the Prime Rate. It can hint at future APR changes. After 12 months of on-time payments, call and ask for a lower APR.

If you know someone weighing a Discover application or stuck paying a high rate they didn’t expect, share this guide with them. A single phone call after a clean year of payments has saved real cardholders hundreds of dollars in interest, and most never knew it was an option.