If you’re staring at a Discover statement and watching the interest charges climb every month, you’re not alone. Maybe you’ve already tried to move that debt to a Capital One card and got blocked, or you’re not sure which cards will even accept your balance. I built this guide to walk you through every step, so you don’t waste a credit pull or get stuck with a surprise fee.

The short answer: You can transfer a Discover balance to most major issuers, including Chase, Citi, Wells Fargo, Amex, and U.S. Bank. However, you cannot transfer it to Capital One because of the May 2025 merger.

I’ll show you which cards work, how to request the transfer, what it costs, and how to avoid mistakes that can cost you hundreds of dollars.

Key Takeaways

This guide explains how to transfer a Discover credit card balance to another card, covering which issuers accept Discover balances, why Capital One is no longer an option, what the transfer costs, how long it takes, and how to protect your credit score throughout the process.

Core Facts:

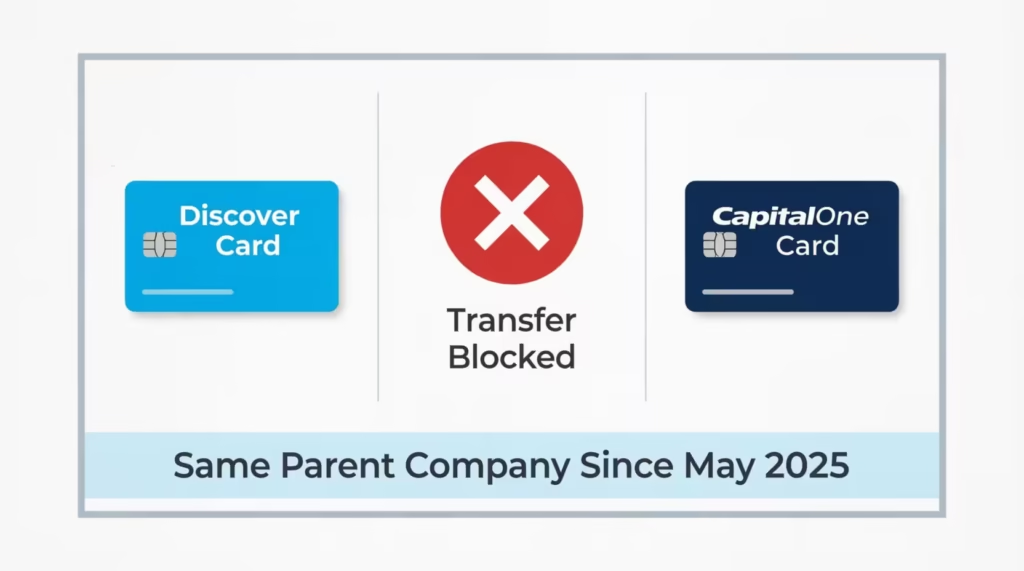

- You cannot transfer a Discover balance to a Capital One card because Capital One completed its acquisition of Discover on May 18, 2025, making them the same parent company. Card issuers do not allow transfers between accounts they own.

- Accepted destination issuers include Chase, Citi, Wells Fargo, American Express, U.S. Bank, Bank of America, and Barclays. You also cannot transfer between two Discover cards.

- Balance transfer fees at the destination card typically run 3% to 5% of the amount transferred, charged as a one-time fee on the day the transfer posts. Some cards charge 3% within the first 60 days and 5% after.

- Most 0% intro APR balance transfer offers require a minimum FICO score of 670, with the best offers (up to 21 months at 0%) generally requiring 720 or higher.

- Transfers take 5 to 21 days to complete on an existing card, or 2 to 4 weeks total when transferring to a newly opened card account.

- You must keep paying the minimum on your Discover card during the transfer window. A missed payment can drop your credit score by 60 to 110 points even if the transfer is in progress.

Best for:

- People carrying a Discover balance at a high APR who qualify for a 0% intro APR card at Chase, Citi, Wells Fargo, or a similar independent issuer.

- Anyone who attempted a Discover-to-Capital One transfer after May 2025 and received an unexpected denial.

- Cardholders who want to understand the full cost, timeline, and credit score impact of a balance transfer before applying.

Can You Transfer a Discover Balance to Capital One? (The Merger Changed This)

No. As of May 18, 2025, you cannot transfer a balance from a Discover card to a Capital One card, or from Capital One to Discover. This is the single biggest source of confusion right now, and it’s the reason many readers land on this page after a failed transfer attempt.

Here’s why. Capital One closed its $35.3 billion acquisition of Discover on May 18, 2025, making the combined company the largest credit card issuer in the United States. When that deal closed, Discover and Capital One became the same parent company. And every major card issuer has the same rule: you can’t move a balance between two cards that share an issuer.

This rule exists because a balance transfer is really an issuer paying off a debt at another bank. If the same bank owns both cards, there’s no debt to “buy out.” So when you try to move money from your Discover it® card to a Capital One Venture or Quicksilver, the request is rejected automatically. You don’t get a warning. You just get a denial.

If Capital One was your plan, here’s what to do instead. Check out issuers that remain fully independent from the new Capital One–Discover group. Chase, Citi, Wells Fargo, American Express, U.S. Bank, Bank of America, and Barclays are all good options. Any 0% intro APR balance transfer card from one of these banks will accept a Discover balance.

⚠️ Mistake to Avoid: Don’t apply for a Capital One card “just to see if it works” with a Discover balance attached. The application creates a hard credit inquiry that lowers your score by a few points, and the balance transfer portion will be denied even if the card itself is approved. You’ll have wasted a credit pull for nothing.

Why You Can’t Transfer Between Two Discover Cards Either

The same-issuer rule also blocks Discover-to-Discover transfers. If you have a Discover it® Cash Back card with a balance and a Discover it® Miles card with room on the credit limit, you can’t shift the debt between them. Both cards are issued by Discover Bank, so the request will be rejected at the system level.

This catches people who carry two Discover products and assume they can consolidate their own debt internally. They can’t. The only way to move debt off any Discover account is to send it to a card from a different bank.

Which Cards You Can Actually Transfer a Discover Balance To

The good news is that most major card issuers will accept your Discover balance. This is true, except for Capital One and some Discover-branded cards. The key is to choose one with good intro terms. Also, know when to ask for the transfer, as each issuer has a different request window.

Here are the four issuers most readers are comparing, along with the key thing you need to know about each one.

| Issuer | Where to Request the Transfer | Time Limit to Get the Intro Offer |

|---|---|---|

| Chase | During the online application, or in the Chase mobile app / website after approval | Usually within 60 days of account opening |

| Citi | During the application (preferred) or by phone after approval | Typically within 4 months of opening |

| Wells Fargo | During the application or through online banking after approval | Within 120 days of account opening |

| American Express | After approval, through your online Amex account | Usually within 60 days of account opening |

A few practical notes that matter more than they sound.

Chase lets you enter the Discover account number and the amount you want to move right on the application page. If you skip that step, you can still log into Chase.com later, click “Pay & Transfer” → “Transfer a Balance”, and submit the request. But you must do it within the promo window, or you’ll pay the regular APR from day one.

Citi is the strictest about the application window rule. The 0% intro APR offer often applies only to balances transferred in the first 4 months. Miss that, and the transfer still works, but at the standard variable APR, which defeats the whole purpose.

Wells Fargo gives you the longest cushion: 120 days. That’s helpful if you’re waiting on a paycheck or want to time the transfer around a Discover statement date.

American Express typically does not allow balance transfer requests during the application process. You have to apply, get approved, then log in and submit the request from your account dashboard within the offer window.

For all of these, the rule is the same: the intro APR only applies to balances transferred within the offer window. If you wait too long, the transfer still goes through, but at the regular rate. That’s the most common preventable mistake in this whole process.

How to Request a Discover Balance Transfer Step by Step

The actual mechanics are simpler than most people expect. You’re not “doing” a transfer yourself. You’re authorizing the new card’s issuer to pay Discover on your behalf. Once you submit the request, the new bank handles the rest.

There are two ways to start the process, and the right one depends on whether you already have the destination card or you’re applying for it now.

Requesting a Transfer on an Existing Card Account

If you already have a Chase, Citi, Wells Fargo, or Amex card with available credit and an active balance transfer offer, this is the faster path.

- Log in to your new card issuer’s website or mobile app.

- Find the balance transfer page. On most issuer sites, it’s listed as “Balance Transfer,” “Transfer a Balance,” or under a “Pay & Transfer” menu. On Chase, it’s under Pay & Transfer. On Citi, look for Services → Balance Transfer. On Wells Fargo, it’s listed directly in the main account menu.

- Enter your Discover account number (the full 16-digit card number on the front of your Discover card).

- Enter the dollar amount you want to transfer. You can transfer the full balance or just part of it.

- Confirm the creditor name (Discover Bank or Discover Financial Services, depending on how the form is worded).

- Review the balance transfer fee and intro APR terms one more time before you click submit.

- Submit the request. You’ll usually get a confirmation email within a few hours.

After you submit, do not stop paying your Discover card. The transfer can take 5 to 21 days to complete, and Discover still expects your minimum payment during that time.

Requesting a Transfer During a New Card Application

If you don’t have the new card yet, you can request the balance transfer right inside the application form. This is the cleanest path because it locks in the intro APR window immediately.

- Open the application page for the card you’ve chosen. For example: Chase balance transfer cards, Citi balance transfer offers, or Wells Fargo balance transfer cards.

- Fill in your personal information, income, and housing details as usual.

- Look for a section titled “Balance Transfer” or “Transfer a balance to this card.” It usually appears near the end, just before you sign and submit.

- Enter your Discover card number, the amount you want to transfer, and select Discover from the issuer dropdown.

- You can list more than one balance if you have other cards. Most issuers allow 2 to 3 transfers on a single application.

- Submit the application.

If you’re approved, the issuer will start the transfer automatically once your new account opens. You don’t have to do anything else. Your new credit limit will determine how much of the requested amount they can actually move, which is the next thing to plan for.

💡 Pro Tip: Before you hit submit on the application, double-check the Discover card number digit by digit. A single wrong digit kicks the request into a manual review queue, which can add 7 to 10 days to the process and may cause you to miss the intro offer window.

Will You Be Approved? Eligibility, Limits, and Minimums

Approval is two separate decisions stacked on top of each other. First, the issuer decides if you qualify for the card at all. Then, they decide how much credit to give you, which controls how much of your Discover balance you can actually move. Many people get approved for the card and still can’t transfer their full balance, so it helps to know what drives each decision.

The three factors that matter most for approval:

- Credit score. Most 0% intro APR balance transfer cards require a FICO score of at least 670, and the best offers (like 21-month intro periods) usually need 720 or higher. If your score is below 670, you’ll likely be denied or pushed to a card with a shorter intro period and a higher fee.

- Income and debt load. Issuers compare your monthly income to your existing debt payments. If your total minimum payments across all cards already eat up a big chunk of your income, they’ll either deny the application or approve you for a small credit limit.

- Recent credit activity. If you’ve opened several cards in the last 12 months, some issuers (Chase in particular, with its 5/24 rule) will deny the application regardless of your score.

Here’s the part most guides skip: even after approval, the new card’s credit limit caps the transfer. If you have a $7,000 balance on Discover and get approved for a $4,500 limit on the new card, you can only transfer $4,500. Usually, it’s less because the balance transfer fee counts against your limit. The remaining $2,500 stays on Discover at the original APR.

If that happens, you have three real options:

- Move the partial amount and aggressively pay down the remaining Discover balance with the money you save on interest.

- Request a credit limit increase on the new card after 3 to 6 months of on-time payments, then move the rest.

- Apply for a second balance transfer card from a different issuer to absorb the leftover balance. Just space the applications out by at least 30 to 60 days so the credit inquiries don’t pile up.

The latest Federal Reserve G.19 consumer credit data shows revolving credit balances continue to climb at an annual rate above 10%, which is part of why issuers have tightened approval amounts. Don’t take it personally if your approved limit is lower than you expected.

Minimum and Maximum Transfer Amounts

Most major issuers require a minimum transfer of $100. Anything smaller gets rejected. There’s no real maximum beyond your approved credit limit, but two practical ceilings apply:

- Some issuers cap balance transfers at 95% of your credit limit. So a $5,000 limit means a maximum transfer of about $4,750 before fees.

- The balance transfer fee counts against the limit. A 3% fee on a $5,000 transfer adds $150, so the total amount applied to your new card is $5,150. If that pushes you over the limit, the issuer will reduce the transfer amount automatically.

Plan the math before you submit. Aim to transfer no more than about 90% of your new credit limit minus the fee. That keeps your utilization ratio from spiking and protects your credit score during the move.

What a Discover Balance Transfer Actually Costs

The phrase “0% intro APR” makes it sound free, but there’s always a real cost. The question is whether the cost is small enough to make the move worth it. For most people carrying a Discover balance at 20% APR or higher, the answer is yes. But you need to do the math, not assume.

Three numbers determine the true cost:

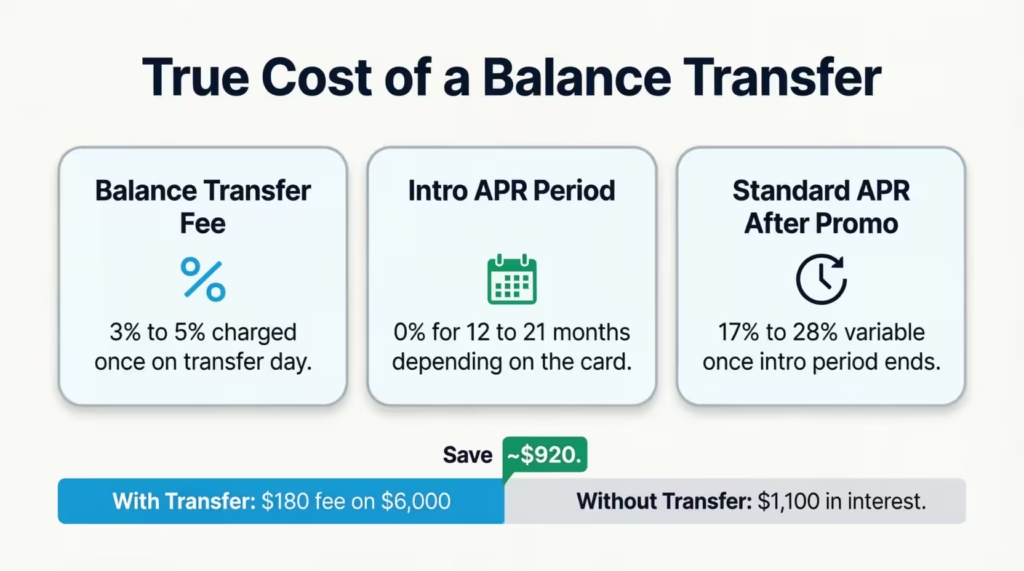

1. The balance transfer fee. This is a one-time charge that gets added to your new balance the day the transfer posts. Industry-standard fees are 3% to 5% of the amount transferred. A 3% fee on a $6,000 transfer adds $180. A 5% fee on the same amount adds $300. Some cards charge 3% if you transfer within the first 60 days and 5% after that, so timing matters.

2. The intro APR period. This is the window where you pay 0% interest on the transferred balance. Common ranges are 12, 15, 18, or 21 months. The longer the window, the more time you have to pay down the balance without interest piling up. Top-tier cards in 2026 offer up to 21 billing cycles at 0%, according to Bankrate’s June 2026 balance transfer card rankings.

3. The standard variable APR after the intro period ends. If you don’t pay off the full transferred balance before the promo ends, the leftover balance will start to accrue interest at the regular APR. This rate is usually between 17% and 28% variable. That can wipe out your savings fast.

The average credit card interest rate sits at 21.52% as of February 2026, the latest figure published in the Federal Reserve’s quarterly consumer credit report. If your Discover APR is in that range or higher, the math almost always favors the transfer, even with a 5% fee.

Real Example: Calculating Your Payoff Plan

Let’s run actual numbers so you can see how this works in practice.

Scenario: Sarah, a 34-year-old marketing manager, has a $6,000 balance on her Discover it® card at a 22.99% variable APR. She qualifies for a card with 0% intro APR for 15 billing cycles and a 3% balance transfer fee.

Here’s her math:

- Balance transferred: $6,000

- Transfer fee (3%): $180

- New balance on the destination card: $6,180

- Intro period: 15 months

- Required monthly payment to pay off the balance before interest kicks in: $6,180 ÷ 15 = $412 per month

If Sarah pays $412 every month for 15 months, she pays exactly $180 in total cost (just the transfer fee). She walks away debt-free with zero interest.

Now compare that to leaving the balance on Discover. At 22.99% APR with the same $412 monthly payment, she’d pay about $1,100 in interest over the same 15 months. The transfer saves her around $920.

But here’s the catch. If Sarah pays only $200 per month instead of $412, she’ll still owe roughly $3,180 when the intro period ends. That remaining balance then starts accruing the new card’s standard APR, which could be 24% or higher. Suddenly, the savings shrink, and she’s back where she started.

The rule: divide your total transferred balance (including the fee) by the number of intro months, and pay at least that amount every single month. Set up autopay for that exact figure the day the transfer posts. Don’t trust yourself to remember.

📌 Did You Know: The balance transfer fee is added to your new balance the day the transfer posts, not billed separately. That means it starts counting against your credit use right away. This can lead to a small, temporary drop in your credit score until you pay it down.

How Long Does a Discover Balance Transfer Take

Most balance transfers take 5 to 14 days to complete from the day you submit the request. Some can take up to 21 days, and the timing depends on whether you’re using an existing account or a brand-new one.

If you’re requesting the transfer on an existing card you’ve held for a while, the process is usually faster. The new issuer already has your account active, your credit limit is set, and they can send the payment to Discover within 5 to 7 business days. Chase confirms most transfers process within a week, though some take up to 21 days.

If you’re requesting the transfer during a new card application, the timeline stretches because the new account has to be opened first. Add 7 to 10 days for the new card to be approved, set up, and activated, then another 5 to 14 days for the transfer itself. Expect the total to take 2 to 4 weeks from application to completion.

The receiving institution (the new card) needs time. They are processing a payment to Discover, either electronically or by check, and must wait for Discover to apply it to your account. Discover also has its own posting window of about 1 to 3 business days once the payment arrives.

You’ll know the transfer is complete when two things happen at the same time:

- Your Discover account shows the transferred amount as a payment received, and your balance drops to $0 (or to whatever you left behind if it was a partial transfer).

- Your new card shows the transferred amount, plus the balance transfer fee, as a new charge.

Once both sides match up, the transfer is officially done. Keep the email confirmation from your new issuer. Also, take a screenshot of your Discover statement showing the zero balance. This way, you have proof if there’s a dispute later.

Keep Paying Your Old Card Until the Transfer Posts

This is the single most overlooked step in the entire process, and skipping it can cost you. Keep making at least the minimum payment on your Discover card until the transfer is fully posted and your Discover balance shows $0.

Here’s why. Discover doesn’t know a transfer is in progress until the payment from the new issuer actually arrives. If your payment due date falls during the transfer window, Discover still expects your normal minimum.

Miss it, and you’ll get hit with a late fee (usually $40), a possible APR penalty, and a late payment mark on your credit report that can drop your score by 60 to 110 points.

The safe rule: make your regular Discover payment as if no transfer were happening. If the transfer comes a few days later and your Discover account has a small credit balance (from both your payment and the transfer), Discover will refund the credit. They may also apply it to your future statements. That’s a much better outcome than a missed payment.

Set a calendar reminder for your Discover due date during the 2 to 4 week transfer window. The discipline of paying the old card until you literally see $0 on the statement is what separates a smooth transfer from an expensive one.

What Happens to Your Old Discover Account After the Transfer

Once the transfer posts and your Discover balance hits $0, your Discover account stays open by default. Discover doesn’t automatically close it. You now own a paid-off credit card with an active credit limit, and you have to decide what to do with it.

There are really only two paths, and the right one depends on your overall credit picture.

Path 1: Keep the Discover card open. This is usually the better move for your credit score. Two things help:

- Credit utilization drops. Your total available credit across all cards stays the same, but your debt is now sitting on the new card. As you pay down the new card, your overall utilization ratio falls, which can lift your score by 20 to 50 points over several months.

- Credit history stays intact. The age of your Discover account (which can be 5, 10, or even 20+ years) keeps counting toward your average account age. Closing it would shorten that average and pull your score down.

The catch: an open card with a zero balance can tempt you to start charging on it again. Set a reminder for a small recurring charge every 3 to 6 months, like a streaming subscription. Keep it open and pay it in full automatically. That keeps the account active without re-creating the debt you just moved.

Path 2: Close the Discover card. This makes sense only in specific situations:

- The card has an annual fee you don’t want to keep paying (most Discover it® cards don’t, but check yours).

- You’ve struggled with credit card debt in the past and know you’ll be tempted to charge it back up.

- The account is very new (less than 1 year old), so closing it won’t hurt your credit history much.

If you close it, expect a temporary credit score dip of 10 to 30 points, mostly from the loss of available credit. The dip usually recovers within 6 to 12 months as long as you keep the new card in good standing.

A note on partial transfers. If you only moved part of your balance (say, $4,500 of a $6,000 balance because of credit limit caps), the remaining $1,500 stays on Discover at the original APR. That portion does not get any 0% benefit.

Make a separate plan to pay it down as fast as possible, ideally with extra payments above the minimum. Some people apply for a second balance transfer card after 60 days to cover the remaining amount. Only do this if your credit score and debt-to-income ratio can support another application.

Moving Discover Credit to a Bank Account, Cash App, or PayPal (Why This Isn’t a Balance Transfer)

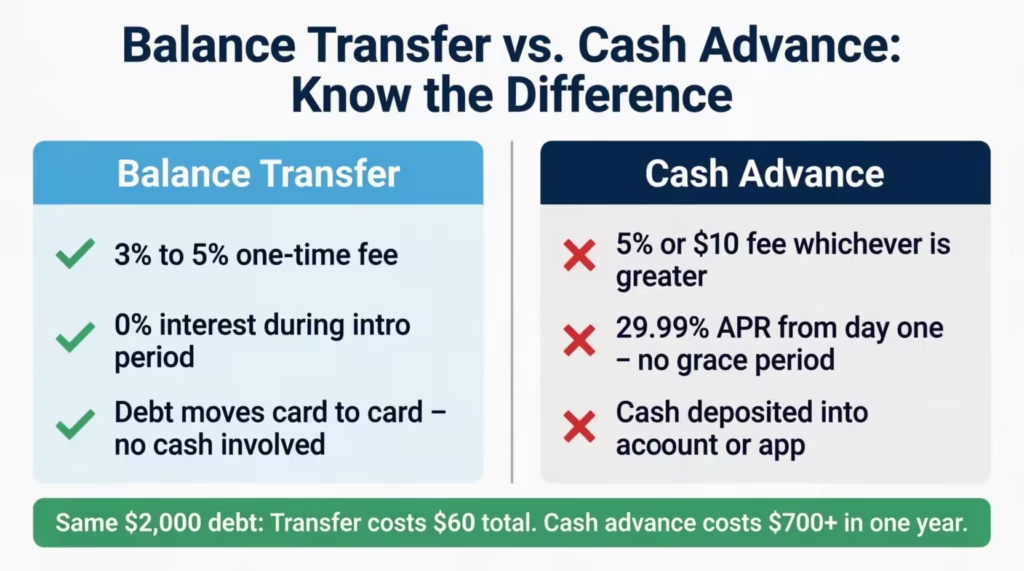

This is where people lose the most money on accident. Sending money from a Discover card to a checking account, Cash App, PayPal, or Venmo is not a balance transfer. It’s a cash advance, and the costs are dramatically higher.

The difference comes down to what’s actually moving. A balance transfer shifts debt from one credit card to another. No physical money changes hands; the new issuer just takes over what you owe.

A cash advance, by contrast, pulls actual cash out of your credit card and deposits it somewhere you can spend it. From the issuer’s point of view, you’re borrowing cash directly, which is a riskier product, so they charge more.

Here’s what a cash advance from Discover actually costs:

- No grace period. Interest starts accruing the moment the money leaves your account. There’s no 25-day window like with regular purchases.

- Higher APR. Discover’s cash advance APR is typically around 29.99% variable, often several points higher than the purchase APR.

- Upfront fee. Discover charges either $10 or 5% of the cash advance amount, whichever is greater. So a $1,000 cash advance costs $50 in fees, on top of immediate interest.

- Lower limit. Your cash advance limit is usually a fraction of your total credit limit, often $500 to $2,000, even on cards with $10,000+ credit lines.

The savings difference is brutal. A $2,000 balance transfer with a 3% fee costs $60 upfront and 0% interest during the intro period. A $2,000 cash advance costs $100 upfront, plus 29.99% interest starting day one. If it takes you a year to pay back the $2,000 cash advance, you’ll pay around $600 in interest plus the $100 fee. The same debt on a transfer card costs you $60 total.

Sending Money to Cash App, PayPal, or Venmo From a Discover Card

If you’ve been told you can “send money to Cash App from your Discover card to pay off another credit card,” stop. The mechanics work like this:

- When you link a Discover card to Cash App, PayPal, or Venmo, sending money to yourself or others counts as a purchase or a cash advance. This depends on the type of transaction. Most peer-to-peer transfers funded by a credit card are coded as cash advances.

- You’ll see the cash advance fee on your next Discover statement, along with immediate interest accrual.

- The cash sits in your Cash App or PayPal balance. Using that cash to pay another credit card means you’ve paid one card by taking a 30% loan from the other. That’s rarely a good trade.

Discover convenience checks are a separate but related product. Discover sometimes mails you blank checks that draw against your credit card. Writing one of these checks to deposit in your checking account counts as a cash advance.

You’ll face the same fees and immediate interest. The only exception is if the convenience check includes a special 0% APR offer. Discover sometimes offers this to existing customers. Read the fine print carefully before using one.

The clean rule: If you need to pay off a credit card, use a balance transfer to another card. Don’t send cash through an app or a check. The savings difference can easily be hundreds of dollars on the same amount of debt.

Does Transferring a Discover Balance Affect Your Credit Score

Yes, a balance transfer affects your credit score, but usually in a predictable and short-term way. Many people notice a small dip in the first month. Then, they see a big improvement over the next 3 to 6 months. This happens as the new card’s lower utilization helps them.

Here’s what actually happens to your score, broken down by event.

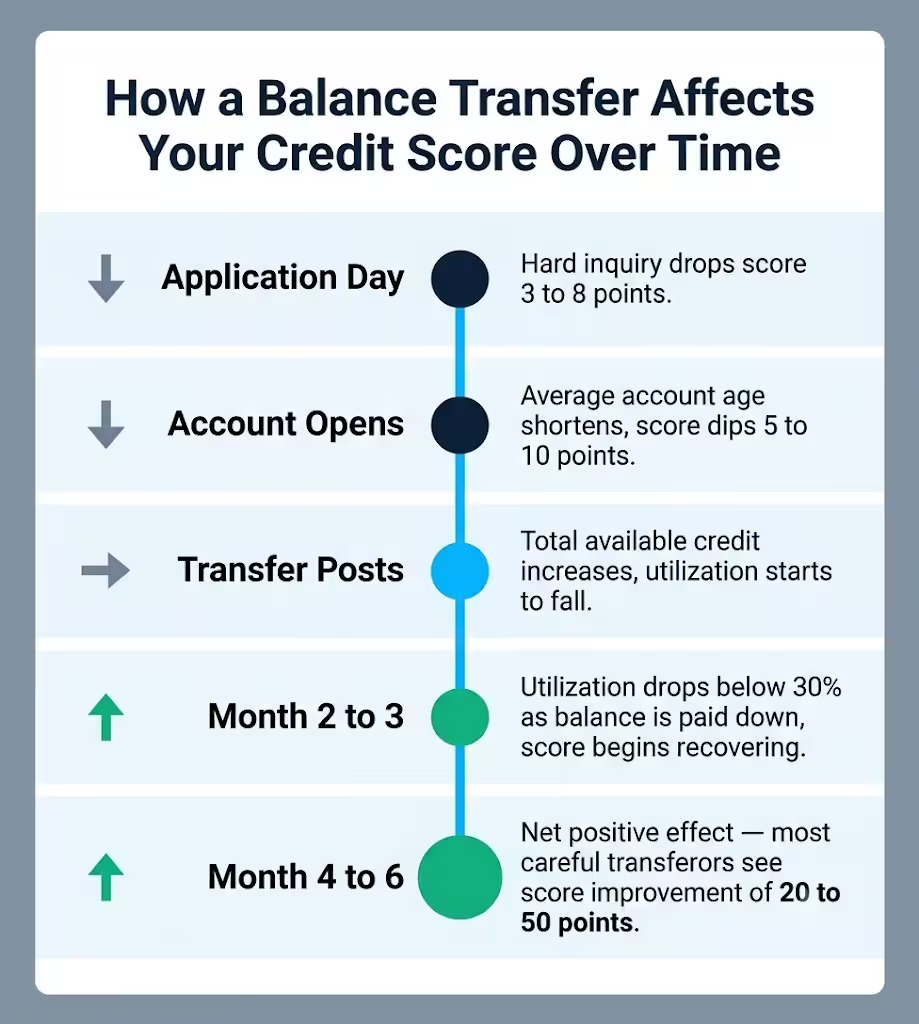

When you apply for the new card: Your credit report gets a hard inquiry, which typically drops your score by 3 to 8 points. The dip is small and recovers within a few months. Hard inquiries stay on your report for 2 years, but only affect your score for about 12 months.

When the new account opens: Your average account age drops slightly because you now have one brand-new account in the mix. This can shave another 5 to 10 points off temporarily, especially if your other accounts are old.

When the transfer posts: This is where the math often turns positive. Your total available credit increases since you have the limits from both the new card and the old Discover card. Meanwhile, your total debt remains about the same. That lowers your credit utilization ratio. This is the biggest short-term factor in your score after payment history.

For example, if you had $6,000 in debt on a $7,000 Discover limit, your utilization was about 86%, which hurts your score badly. After the transfer, the same $6,000 sits on a card with, say, an $8,000 limit, while the Discover card now has $0 used.

Your overall use of both cards falls to about 40%. If you keep paying down the new card, it could drop below 30% in a few months. That utilization improvement often adds 20 to 50 points to your score.

What can hurt your score during a transfer:

- Missing a payment on your old Discover card during the transfer window is risky. A single late payment can lower your score by 60 to 110 points.

- Close the old Discover account after the transfer. This takes away your available credit and might shorten your credit history.

- Maxing out the new card by transferring an amount that uses up nearly all of its credit limit. Keep your transfer at about 70 to 80% of the new card’s limit if possible.

Most people who transfer carefully and keep both cards in good standing see a net positive effect on their credit score within 4 to 6 months. The temporary dip is just the cost of admission. The real win is using less. You gain space to pay off debt interest-free and improve your credit profile over time.

Frequently Asked Questions (FAQs)

How much does Discover charge for a balance transfer?

Discover doesn’t charge a balance transfer fee. You pay the fee to the card you’re transferring to, not to Discover. That destination card typically charges 3% to 5% of the amount transferred as a one-time fee.

How much will it cost in fees to transfer a $1,000 balance to a card?

At a 3% fee, transferring a $1,000 Discover balance costs $30 upfront, bringing your new card balance to $1,030. At a 5% fee, the cost rises to $50, making the new balance $1,050.

Can I transfer my entire credit card balance to another card?

You can move your entire Discover balance if the new card’s credit limit is high enough. It must cover the balance and the transfer fee. If your approved limit is lower than the total, only a partial amount transfers, and the rest stays on Discover at the original APR.

What is the disadvantage of a balance transfer?

The main drawbacks include an upfront fee of 3% to 5%. You may also see a short dip in your credit score from the hard inquiry. Plus, if you don’t pay it off before the intro period ends, you could owe the remaining balance at a high standard APR.

When should you not do a balance transfer?

Skip the balance transfer if you can’t pay off the full amount each month before the 0% intro period ends. Otherwise, any leftover balance will start to rack up the card’s normal APR, which is usually between 17% and 28%. It also makes no sense if you miss the issuer’s transfer request window, because the transfer would go through at the regular rate.

Can I do a balance transfer of $10,000?

Yes, but only if your new card’s credit limit is high enough to cover it. Most issuers cap transfers at 95% of your credit limit. The balance transfer fee counts towards that cap. So, a $10,000 transfer would need a limit of about $10,500 or higher.

Why can’t you do a balance transfer from Discover to Capital One?

Capital One completed its $35.3 billion acquisition of Discover on May 18, 2025, making them the same parent company. Card issuers don’t allow balance transfers between accounts they own. So, if you request a transfer between Discover and Capital One, it will be rejected.

How long does a Discover balance transfer take?

Most Discover balance transfers finish in 5 to 14 days after you submit your request. However, some may take as long as 21 days. If you are transferring to a newly opened card, add another 7 to 10 days for the account to be set up first, putting the total timeline at 2 to 4 weeks.

Should I close my Discover card after completing a balance transfer?

Usually, keeping your Discover card open is wise. It helps lower your credit utilization ratio and keeps the account’s age in your credit history. Close it only if it carries an annual fee you do not want to pay, or if having an open card will tempt you to accumulate new debt.

Do I need to keep paying my Discover card while the balance transfer is processing?

Yes. Discover does not know a transfer is in progress until the payment from the new issuer actually arrives, which can take up to 21 days. Missing a minimum payment during that window triggers a late fee of around $40 and can drop your credit score by 60 to 110 points.

Wrapping Up

To move a balance off a Discover card, you need to make four choices:

- Choose a destination that isn’t Capital One or another Discover card.

- Request the transfer during the new issuer’s promotional period.

- Pay enough each month to clear the balance before the intro APR expires.

- Avoid cash advances that seem like transfers but aren’t.

A 0% intro APR transfer with a 3% fee saves the average reader about $900 on a $6,000 balance over 15 months. This shows why the strategy works when done right.

If you know someone juggling Discover debt and a high APR, share this guide with them. The Capital One merger rule has made people lose a credit pull for no reason. A little planning can save them hundreds of pounds.