Daily Credit Card Interest Calculator

Instantly see how much interest your credit card balance accrues daily.

Daily Interest

$0.00

Total Interest Over 30 Days

$0.00

Have you ever stared at your credit card bill and wondered why the interest just keeps growing? Most Americans carry a balance without knowing exactly what it costs them each single day. The Federal Reserve puts the average credit card rate above 21% right now. Using a daily credit card interest calculator makes that hidden daily cost clear and easy to track.

This tool provides an immediate display of your exact daily interest charge and the total interest accumulated over any period you choose.

Keep reading. This guide shows the full formula. It includes a step-by-step walkthrough of the tool and real-world examples. These will help you reduce your credit card costs.

Tip: → See exactly when interest starts and stops with the credit card billing cycle calendar printable.

What Is Credit Card Daily Interest?

Credit card interest doesn’t just show up once a month. It builds up every single day.

When you carry a balance on your card, your issuer charges interest on that balance daily. By the time your billing cycle ends, all those small daily charges get added together. That combined total appears on your next statement as a finance charge.

This process is called daily interest accrual. It’s the reason your balance can grow even when you don’t make any new purchases.

The Consumer Financial Protection Bureau (CFPB) confirms that many card issuers calculate the interest you owe daily, based on your average daily balance. The rate used for this daily calculation is called the Daily Periodic Rate, or DPR.

Card issuers convert your Annual Percentage Rate (APR) into a daily rate. Then they apply that rate to your outstanding balance each day.

Most U.S. credit cards use a 365-day year for this conversion. That means interest accrues 365 times a year. It does not just compound 12 times as a monthly charge might suggest.

📌 Did You Know: Some lenders use a 360-day divisor instead of 365 to calculate the DPR. Credit cards in the U.S. almost always use 365. Always check your card’s terms and conditions to confirm which method your issuer uses, since it affects your actual daily cost.

Data published by the CFPB’s 2025 Consumer Credit Card Market Report reveals that in 2024, consumers were assessed $160 billion in interest charges. That’s up from $105 billion just two years prior in 2022. That staggering jump reflects rising APRs and more Americans carrying balances month to month.

How This Calculator Works

The daily credit card interest calculator on this page does all the math for you, instantly, as you type.

You enter three pieces of information:

- Your balance – the dollar amount you currently owe on your card

- Your APR – your card’s Annual Percentage Rate (found on your statement or in your card agreement)

- Number of days – the time period you want to project

The tool then produces two key results. First, it shows your daily interest charge. Second, it shows the total interest that builds up over the number of days you selected.

There’s also a Daily Compounding toggle on the left side. Turn it on if your card compounds interest daily. Most major U.S. card issuers do. Turn it off if you want to see the simple interest calculation side by side.

A line chart below the results updates in real time. It shows how your cumulative interest grows day by day. This visual makes the snowball effect of carrying a balance very easy to grasp at a glance.

You can also:

- Use the quick-select day buttons (7, 30, 90, or 365 days) for fast comparisons

- Drag the slider to fine-tune your projection period

- Download your results as a PDF for future reference

- Share your calculation directly to Facebook, X, WhatsApp, or Reddit

The Formula Explained

Don’t let the math intimidate you. The formula has just three steps. Here’s exactly how it works.

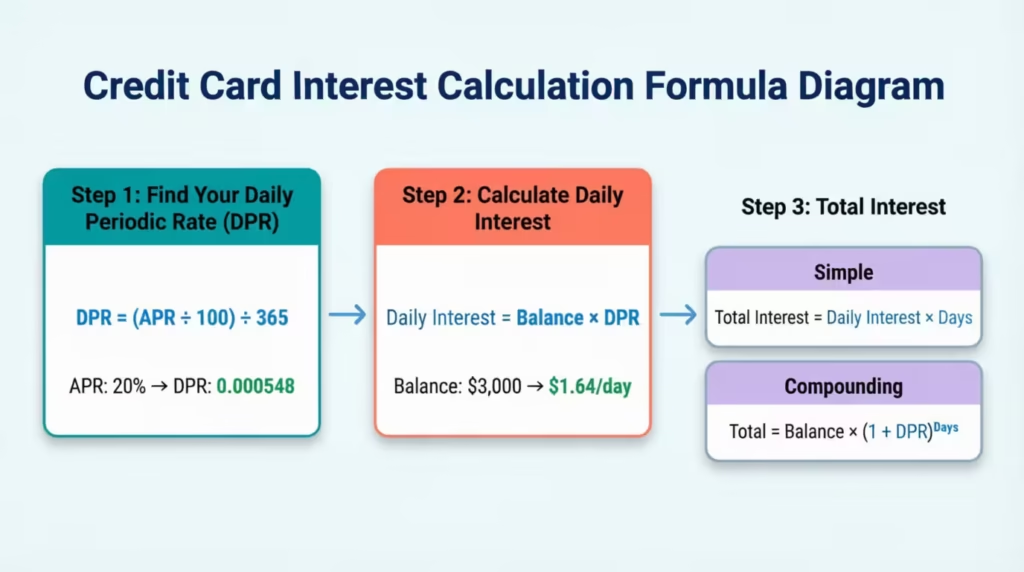

Step 1: Calculate the Daily Periodic Rate (DPR)

The DPR is how your APR gets converted into a daily charge.

DPR = (APR ÷ 100) ÷ 365

For a card with a 20% APR:

DPR = (20 ÷ 100) ÷ 365 = 0.000548 per day

That’s roughly 0.055% charged to your balance every single day.

Step 2: Calculate Your Daily Interest Charge

Multiply the DPR by your outstanding balance.

Daily Interest = Balance × DPR

For a $3,000 balance at 20% APR:

Daily Interest = $3,000 × 0.000548 = $1.64 per day

It sounds small. But let’s see what that adds up to.

Step 3a: Total Interest Without Compounding (Simple Interest)

When the compounding toggle is off, the calculator uses this formula:

Total Interest = Daily Interest × Number of Days

| Time Period | Total Interest Charged |

|---|---|

| 7 days | $11.51 |

| 30 days | $49.32 |

| 90 days | $147.95 |

| 365 days | $600.00 |

A $3,000 balance at 20% APR costs you $600 in simple interest over a full year, even without a single new charge.

Step 3b: Total Interest With Daily Compounding

When the compounding toggle is on, interest is added to your balance each day. The next day’s charge is then calculated on that slightly larger balance. This is where things compound quickly.

Total After N Days = Balance × (1 + DPR)^Days

Total Interest = Total After N Days - BalanceFor the same $3,000 balance at 20% APR over 365 days:

Total = $3,000 × (1.000548)^365 = $3,664.20

Total Interest = $3,664.20 - $3,000 = $664.20Compounding adds an extra $64.20 over the simple interest total. The longer you carry the balance, the wider that gap gets.

📌 Did You Know: The Federal Reserve G.19 Consumer Credit release tracks the average interest rate assessed on credit card accounts. Rates have been over 21% for accounts with a balance. This means these examples reflect a real situation for millions of cardholders.

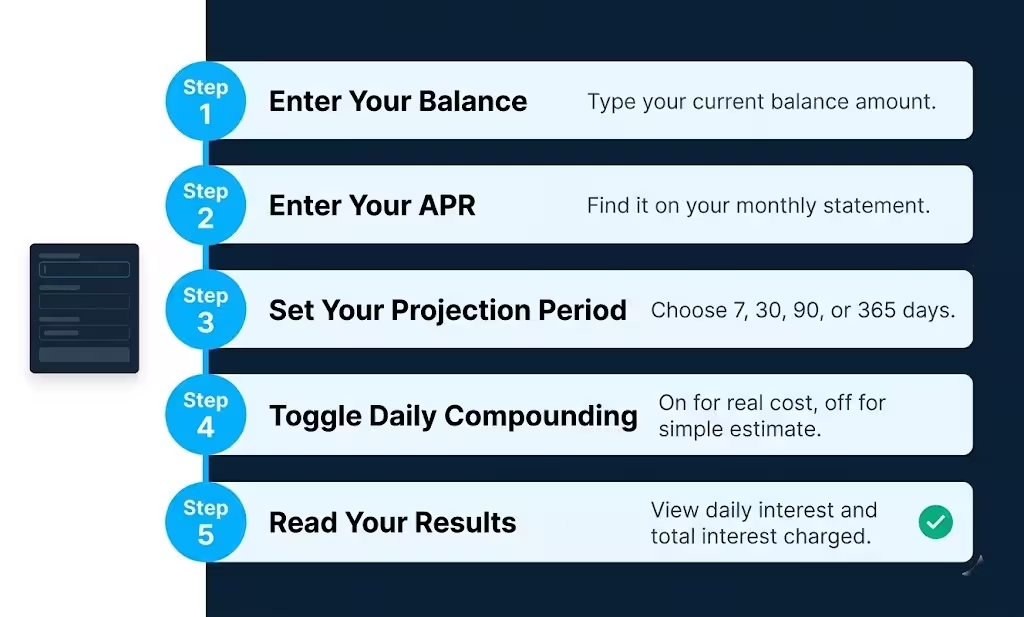

How to Use This Calculator (Step by Step)

Using the tool takes less than 60 seconds. Here’s exactly what to do.

Step 1: Enter Your Balance

Type your current credit card balance in the Balance field. You can enter a number like 3000 or a formatted amount like 3,000.00. The field accepts both. If you carry several cards, start with the one with the highest APR.

Step 2: Enter Your APR

Type your card’s APR in the APR field. You’ll find this on your monthly statement, usually listed as “Purchase APR” or “Variable APR.” If you have a promotional rate, use that number for now. Switch to your regular rate to see what happens after the promo ends.

Step 3: Set Your Projection Period

Choose how many days you want to project. You have three options:

- Click one of the preset buttons: 7, 30, 90, or 365 days

- Drag the blue slider left or right

- Type a specific number between 1 and 365

The 30-day preset is a great starting point since it mirrors one billing cycle.

Step 4: Toggle Compounding On or Off

Look for the Daily Compounding switch in the input panel. Turn it on to see the real compounding cost. Turn it off to see the simpler, lower estimate. Comparing both gives you the full picture.

Step 5: Read Your Results and Take Action

Your daily interest and total interest appear in the results panel immediately after the calculation. Use the chart to see the growth curve. Then scroll down for tips on what to do next. If you want to save or share your results, click the PDF button or choose a social share icon.

Tip: → Want to double-check this figure against a real statement? Compare it using the credit card statement template.

How to Read Your Results

The results panel shows two key numbers right at the top.

The first box shows your Daily Interest. This is the exact dollar amount your balance costs you each day. Even a number that looks small, like $1.64, adds up to hundreds of dollars per year.

The second box shows your Total Interest Over X Days. This is the cumulative cost over your chosen period. It gives you a concrete dollar amount to compare against what it would cost to pay down the balance faster.

Below those two numbers, you’ll see a short insight message. It confirms your total cost in plain language. For example: “Carrying this balance costs $49.32 over 30 days.”

The line chart below shows the growth of your interest day by day. When compounding is off, the line is straight. When compounding is on, the line curves slightly upward. That curve represents the extra cost of compound interest.

💡 Pro Tip: Switch the projection to 365 days to see your full annual cost. Then compare that number to what you’d save by making an extra $50 or $100 payment this month. You might be surprised how quickly a small payment reduces your annual interest bill.

Real-World Example

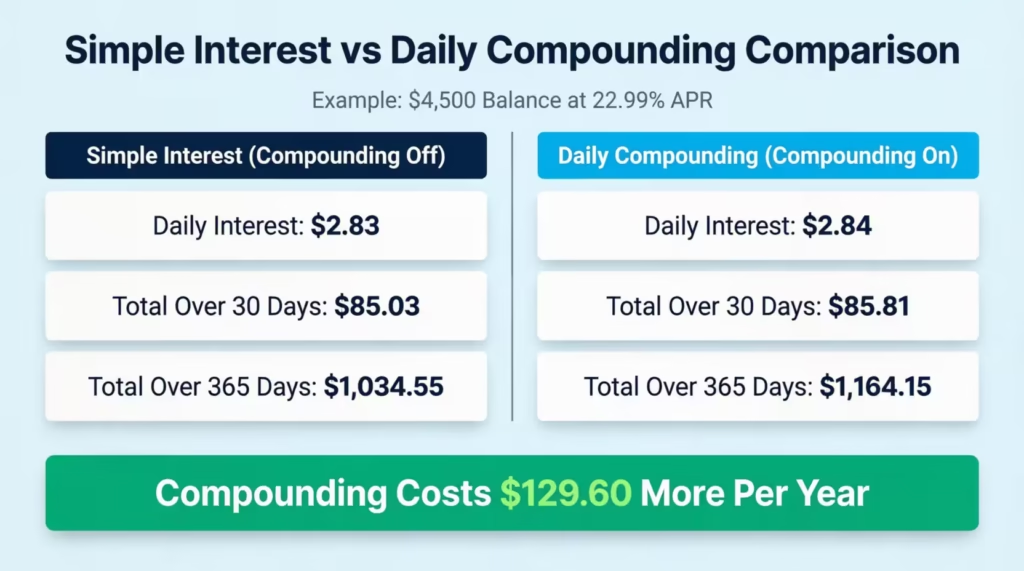

Meet Marcus. He’s a 34-year-old project manager at a mid-sized logistics company in Dallas. After a car repair and a few months of tight budgeting, Marcus is carrying a $4,500 balance on his rewards card at a 22.99% APR.

Marcus wasn’t sure how bad the daily cost really was. So he pulled up the interest tool and entered his numbers.

Here’s what the calculator showed him:

Inputs:

- Balance: $4,500

- APR: 22.99%

- Days: 30 (one billing cycle)

- Compounding: Off

Results (Simple Interest):

DPR = (22.99 ÷ 100) ÷ 365 = 0.000630 per day

Daily Interest = $4,500 × 0.000630 = $2.83 per day

Total Over 30 Days = $2.83 × 30 = $85.03That’s $85.03 in interest just for one billing cycle.

Marcus then switched the compounding toggle on to see the real picture.

Results (With Daily Compounding):

Total = $4,500 × (1.000630)^30 = $4,585.81

Total Interest = $85.81The difference for 30 days was small. Just 78 cents more with compounding. But Marcus wanted to see the full-year impact.

Annual Comparison:

| Calculation Type | Total Interest (365 Days) |

| Simple Interest | $1,034.55 |

| Daily Compounding | $1,164.15 |

| Difference | $129.60 extra |

Daily compounding alone costs Marcus an extra $129.60 per year. That’s money he could put toward his balance, his savings, or anything else he values more than interest charges.

This single calculation motivated Marcus to set up an automatic extra payment of $100 per month. Over time, that small habit will save him hundreds.

Expert Tips and Insights

1. Pay More Than the Minimum Payment

Minimum payments are designed to keep you in debt longer. Credit card issuers calculate them to cover a small part of the principal and most of the interest. Even an extra $25 or $50 a month helps pay down your principal faster. This also lowers the interest you pay each day.

2. Make a Payment Before Your Statement Closes

Most people wait until the due date to pay. But since interest accrues daily, paying earlier in the billing cycle lowers your average daily balance. A lower average daily balance means less interest charged for that cycle.

💡 Pro Tip: If your statement closes on the 25th of the month, making a payment on the 15th instead of the 25th reduces the balance that interest is calculated on for those 10 extra days. Over a year, that timing shift can save you a meaningful amount.

3. Use the 7-Day Preset to Stay Aware

Switching the tool to a 7-day view gives you a quick weekly cost snapshot. It’s a useful reality check. When you see that your balance costs you $19 a week to carry, the motivation to pay it down becomes more concrete.

4. Compare APRs Before Moving a Balance

Thinking of a balance transfer? Use this tool to compare your daily costs. Check your current APR against the transfer card’s APR or promo rate. Enter both APRs and compare the totals. The difference often justifies the transfer fee.

5. Know When Your Grace Period Ends

As the CFPB notes, since interest accrues daily, the sooner you pay off all or some of your balance, the less interest you pay. Most cards offer a grace period of at least 21 days for new purchases. If you pay your full statement balance before the due date, you pay zero interest. The daily cost only kicks in when you carry a balance past that point.

Common Mistakes to Avoid

Mistake 1: Thinking Interest Only Hits Once a Month

Many cardholders believe their APR is a monthly charge. It isn’t. Interest accrues every day from the moment a balance exists. By the time your statement is generated, 30 days of daily charges have already stacked up. Understanding this changes how urgently you prioritize payments.

Mistake 2: Not Knowing Your APR Before a Large Purchase

Some cardholders make a big purchase on a high-APR card without checking the rate first. A $2,000 purchase at 24.99% APR costs about $1.37 per day in interest. That’s $41 per month just sitting there. Knowing your APR in advance helps you decide whether to use a lower-rate card or pay it off fast.

Mistake 3: Only Paying the Minimum Balance

⚠️ Mistake to Avoid: Paying only the smallest balance each month means your principal barely shrinks. Most of that payment covers interest, not debt. On a $3,000 balance at 20% APR with a $60 minimum payment, it can take years to pay off the balance and cost hundreds of dollars in extra interest. Always pay more than the smallest whenever you can.

Mistake 4: Ignoring the Compounding Toggle

Simple interest and compound interest give different results. Most credit cards compound daily. Leaving the toggle off gives you an underestimate of your actual charges. Always run both scenarios, so you see the true range of your interest cost.

Mistake 5: Forgetting About Penalty APRs

Missing a payment can trigger a penalty APR on many cards. Penalty APRs often run 29.99% or higher. At that rate, a $3,000 balance costs roughly $2.46 per day instead of $1.64 per day at 20%. One missed payment can significantly raise your daily interest cost for months.

FAQs

What is the Daily Periodic Rate (DPR) on a credit card?

The DPR is your card’s Annual Percentage Rate divided by 365. It’s the small percentage your card issuer applies to your balance each day to calculate your daily interest charge.

Does credit card interest really compound daily?

Yes, most major U.S. credit card issuers compound interest daily. This means interest is added to your balance each day, and the next day’s interest is calculated on that slightly higher amount.

How do I find my credit card’s APR?

Your APR appears on your monthly statement, usually under “Interest Charge Calculation” or “Account Summary.” You can also find it in your original card agreement or by logging into your online account.

Can making a payment mid-cycle actually reduce my interest?

Yes. Because interest accrues on your daily balance, paying down your balance mid-cycle lowers the balance used for the remaining days. This reduces the total interest charged for that billing period.

What is the difference between a daily interest charge and a monthly finance charge?

The daily interest charge is the small amount applied to your balance each day. The monthly finance charge is all those daily charges added together. It’s the lump sum that appears on your statement.

What happens if I only pay the minimum balance every month?

Paying only the minimum means most of your payment covers interest, not your principal. Your balance shrinks very slowly, and you end up paying significantly more in total interest over the life of the debt.

Is there a grace period for credit card interest?

Most credit cards offer a grace period of at least 21 days. If you pay your full statement balance by the due date, no interest accrues. Interest only applies when you carry an unpaid balance past that deadline.

How much does a 1% difference in APR change my daily interest?

On a $3,000 balance, a 1% higher APR adds about $0.08 per day, or roughly $29.20 per year. On larger balances or over longer periods, that difference grows considerably.

Conclusion

We’ve covered a lot of ground in this guide. Credit card interest accrues every single day, not once a month. The Daily Periodic Rate is what drives your daily charge. Simple and compound interest produce different totals, and most U.S. cards use daily compounding. Knowing your exact daily cost changes how you think about every day you carry a balance.

Start with the 365-day projection to get the full annual cost in one number, the most effective approach. That single figure is often the wake-up call that motivates real action.

If this guide made your card’s interest clearer, please share it with a friend or family member. They might be unaware of the true cost of their credit card debt.