Car Loan Calculator by Credit Score

Estimate your monthly payment and see how your credit score impacts your APR and total cost.

Loan Details

Down Payment (Optional)

Your Estimated Results

Monthly Payment

Estimated APR

Total Interest Paid

Total Loan Cost

Enter your loan details to see your personalized results.

Compare Costs by Credit Score

See how much you could save with a better credit score, based on your entered loan amount and term.

| Credit Score Range | APR | Monthly Payment | Total Interest |

|---|---|---|---|

| Enter your loan details for a comparison. | |||

Share Your Results

How to Use This Calculator

Enter your total Loan Amount (the vehicle price you'll finance).

Set your estimated Credit Score using the slider or by typing it in.

Choose your desired Loan Term in years from the dropdown.

(Optional) Expand and add a Down Payment to reduce your loan principal.

Your results update in real-time as you enter your details.

Use 'Download PDF' to save a copy of your results or the share icons to send your estimate to others.

Disclaimer

This calculator is for informational purposes only. The results are estimates based on the information you provide and may not be accurate or applicable to your specific financial situation. The information provided does not constitute financial, legal or tax advice. We do not guarantee the accuracy of the calculations or the applicability of any information. Always consult a qualified financial professional for advice specific to your personal circumstances. Credit card terms, conditions, rates and offers are subject to change by the issuing bank at any time. We are not responsible for any actions or decisions taken based on the information provided by this tool.

Shopping for a car is exciting. But many buyers miss one detail that changes their payment significantly. Borrowers with deep subprime scores pay more than twice the interest rate of excellent-credit borrowers on the same loan, according to Experian’s State of the Automotive Finance Market. A car loan calculator by credit score shows you your real numbers before you visit a dealer.

The best way to know what you’ll pay is to estimate your rate by credit tier first.

Keep reading. We’ll cover the formula, step-by-step usage, and real examples to help you plan smarter.

Tip: → If something on your report looks wrong, fix it first with the credit report dispute letter template.

What Is a Car Loan Calculator by Credit Score?

Most standard auto loan calculators ask you to enter an interest rate manually. But here’s the problem with that approach: most people don’t know their actual rate until after they apply.

A credit score-based auto loan estimator works differently. Instead of asking for a rate, it uses your credit score to assign a realistic APR automatically. It then runs the full math on your loan. You get your monthly payment, total interest, and overall loan cost, all based on your real credit tier.

Think of it this way. It bridges the gap between “I have a credit score of 620” and “here’s exactly what this car is going to cost me.”

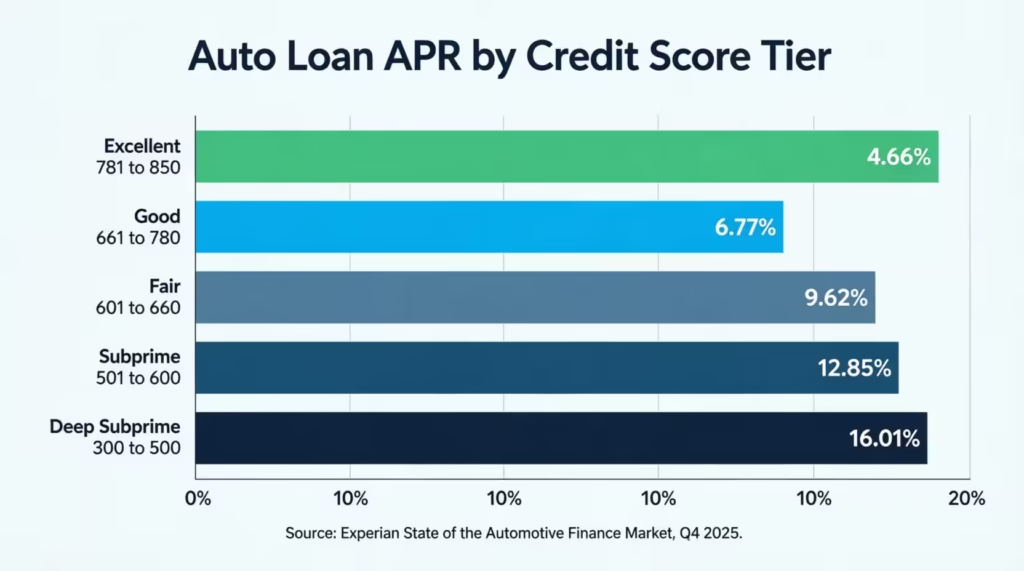

This tool uses five credit score tiers. Each tier carries a different APR based on Experian Q4 2025 data:

| Credit Score Range | Credit Tier | Updated APR |

|---|---|---|

| 781 to 850 | Excellent | 4.66% |

| 661 to 780 | Good | 6.77% |

| 601 to 660 | Fair | 9.62% |

| 501 to 600 | Subprime | 12.85% |

| 300 to 500 | Deep Subprime | 16.01% |

These APR figures are aligned with average new vehicle loan rates. Experian’s State of the Automotive Finance Market tracks these rates each quarter and shows clearly how credit tier affects what borrowers actually pay.

📌 Did You Know: Moving from the “Fair” tier (9.29% APR) to the “Good” tier (6.88% APR) on a $25,000 loan over 5 years saves you about $1,732 in total interest. That’s a meaningful amount of money, and it comes down entirely to your credit score.

How This Calculator Works

This tool handles all the math in real time. Here’s what’s happening behind the scenes each time you enter your details:

Credit Score to APR Mapping

The moment you type in your credit score, the calculator checks it against five APR bands. It assigns the market-rate APR for your tier right away. There’s no manual rate entry required.

Real-Time Amortization

With your loan amount, APR, and term set, the calculator runs the standard amortization formula. Your results auto-update as you make changes. There’s no calculate button to press.

Full Cost Breakdown

The results panel shows four key figures at once:

- Monthly payment

- Estimated APR

- Total interest paid over the full loan

- Total loan cost (principal plus all interest combined)

Side-by-Side Comparison Table

This is one of the most powerful parts of the tool. The table compares your monthly payment and total interest for each of the five credit tiers. You’re using your own loan amount and term, so the comparison is specific to your situation, not a generic estimate.

Visual Bar Chart

The bar chart displays monthly payments across all five tiers in one view. You can see the cost gap between excellent and deep subprime credit without doing a single calculation yourself. It’s a quick, visual way to grasp how much your score matters.

PDF Download and Social Sharing

Once you see your results, you can save them as a PDF. You can share your estimate directly on Facebook, X, WhatsApp, or Reddit.

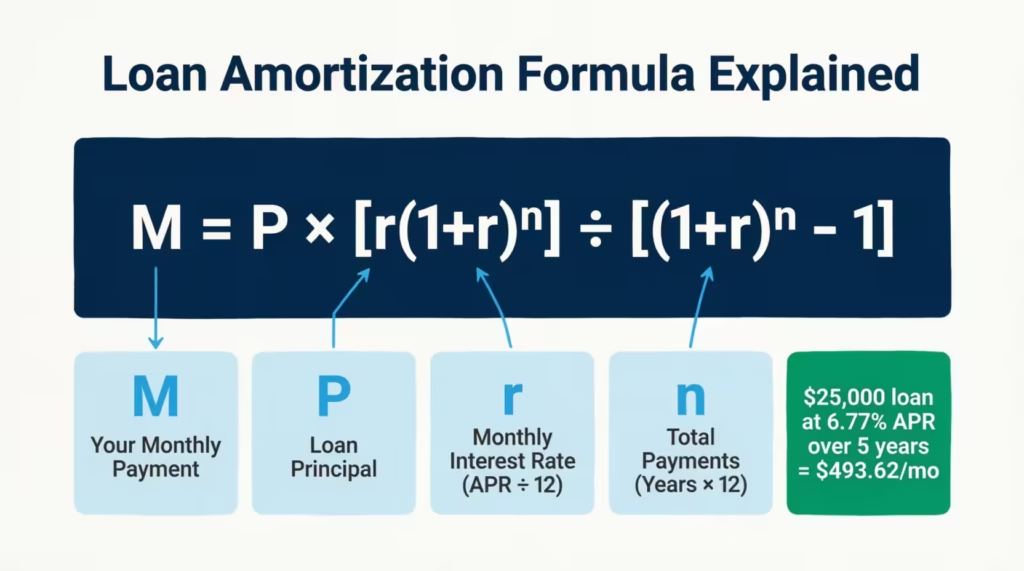

The Formula Explained

The math behind this tool is the standard loan amortization formula. Banks, credit unions, and auto lenders all use this same formula to calculate your monthly payment.

Here it is:

M = P x [r(1 + r)^n] / [(1 + r)^n – 1]

Here’s what each variable means:

- M = Your monthly payment (the number you’re solving for)

- P = Principal (your loan amount after subtracting any down payment)

- r = Monthly interest rate (your annual APR divided by 12, expressed as a decimal)

- n = Total number of payments (loan term in years multiplied by 12)

Let’s Work Through a Quick Example

Say you’re borrowing $25,000 at 6.88% APR (Good credit tier) for 5 years.

- r = 6.88 / 100 / 12 = 0.005733 per month

- n = 5 x 12 = 60 payments

Plug those in:

M = $25,000 x [0.005733 x (1.005733)^60] / [(1.005733)^60 – 1]

M = $493.62 per month

Total cost = $493.62 x 60 = $29,617 Total interest paid = $29,617 – $25,000 = $4,617

The calculator runs this exact formula for every credit tier, instantly, every time you update your inputs.

💡 Pro Tip: Your APR is largely determined by your credit score tier. A gain of just 30 to 40 points can push you into a lower band and cut your total interest by hundreds of dollars. It’s worth checking your score before you apply.

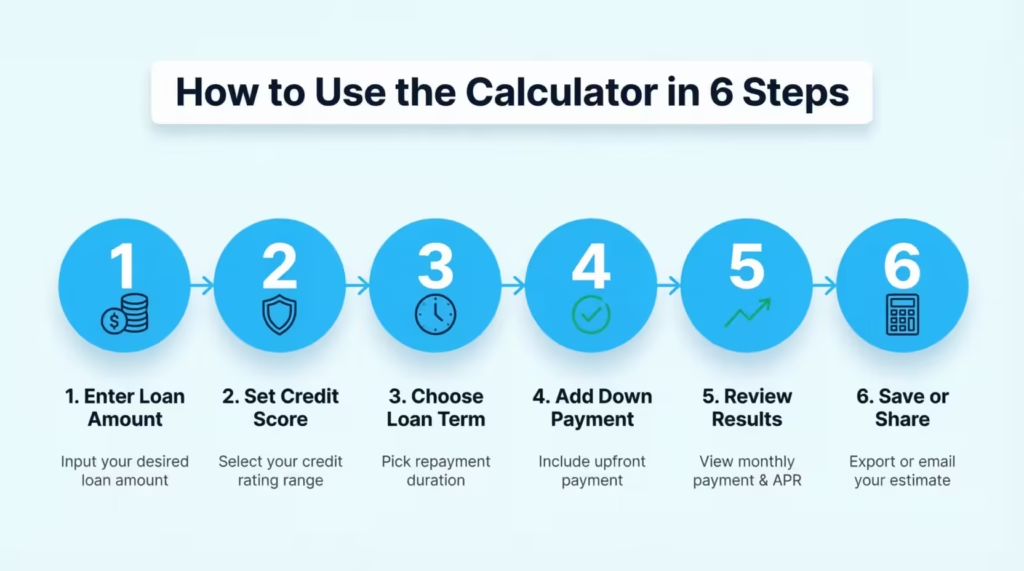

How to Use This Calculator (Step by Step)

Follow these six steps to get your personalized loan estimate:

Step 1: Enter Your Loan Amount

Type in the total amount you plan to finance. This is the vehicle price you’ll actually borrow, not necessarily the full sticker price. The tool accepts amounts between $1,000 and $100,000.

Step 2: Set Your Credit Score

Enter your credit score in the number box, or drag the slider to your score. The tool works with any score from 300 to 850. Not sure of your score? You can check it for free through your bank, your credit card issuer, or a service like Credit Karma.

Step 3: Choose Your Loan Term

Select how many years you want to repay the loan. The dropdown runs from 1 to 7 years. A shorter term means higher monthly payments but much less total interest. A longer term shrinks your monthly payment but raises your total cost.

Step 4: Add a Down Payment (Optional)

Click “Show” next to the Down Payment field if you plan to put money down upfront. Enter the amount. It gets subtracted from your loan principal before the calculation runs. This reduces both your monthly payment and total interest.

Step 5: Review Your Real-Time Results

You don’t need to press any button. Your results update live as you type. Check the monthly payment, estimated APR, total interest, and total loan cost in the results panel on the right.

Step 6: Save or Share Your Results

Once you’ve run your numbers, click “Download Results as PDF” to save a copy. You can also use the social share icons to send your estimate to someone who’s helping you with the decision.

How to Read Your Results

Once your details are entered, the results panel shows four figures. Here’s what each one means and why it matters:

Monthly Payment

This is your fixed payment amount each month for the entire loan term. It covers both principal repayment and interest. Use this number to check whether the loan fits your monthly budget comfortably.

Estimated APR

This is the annual percentage rate assigned to your credit tier. It’s the single biggest driver of your loan cost. A lower APR means a lower monthly payment and far less interest over time.

Total Interest Paid

This is how much extra you pay on top of what you borrowed. It’s the true cost of credit. Many borrowers are surprised when they see this number. A higher APR or longer loan term can make this figure climb fast.

Total Loan Cost

This combines your original loan principal with all the interest you’ll pay. It gives you the complete cost of owning this vehicle through financing. Analyze this number thoroughly across different loan scenarios.

The Comparison Table

Scroll below the main results to find the comparison table. It displays monthly payments and total interest for all five credit score tiers, calculated using your exact loan amount and term. This table makes it easy to see what you’d save with a better score, or what you’re paying right now with your current one.

⚠️ Mistake to Avoid: Fixating on the monthly payment alone is one of the most common and costly mistakes in auto financing. A longer loan term can lower your monthly payment. However, you may end up paying thousands more in interest.

Real-World Example

Let’s see how this plays out with a real scenario.

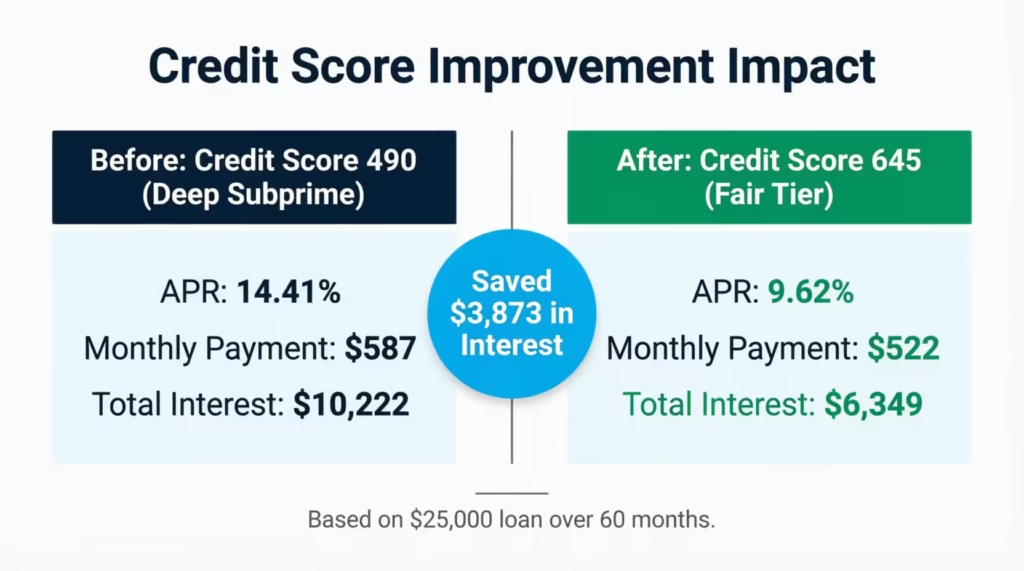

Marcus, a 29-year-old public school teacher from Columbus, Ohio, wanted to finance a $25,000 used SUV with no down payment. He planned to repay it over 5 years. His credit score at the time was 490, which places him in the deep subprime tier.

Here’s what the calculator shows across three scenarios, all based on the same $25,000 loan over 60 months:

| Scenario | Credit Score | APR | Monthly Payment | Total Interest |

|---|---|---|---|---|

| Marcus (current) | 490 | 14.41% | $587 | $10,222 |

| If score were 680 | 680 | 6.88% | $494 | $4,617 |

| If score were 800 | 800 | 5.19% | $474 | $3,438 |

The difference between Marcus’s current situation and a good credit score is $93 per month. Over 60 months, that adds up to $5,605 more in total interest paid just because of a lower credit score.

Marcus decided to hold off on the purchase for six months. He paid down two credit card balances and disputed an old error on his credit report. His score climbed from 490 to 645. That shift moved him into the “Fair” tier at 9.29% APR.

His new monthly payment dropped from $587 to $522. His total interest dropped from $10,222 to $6,349. He saved $3,873 in total interest just by waiting six months and doing the work on his credit first.

Tip: → Want to improve your score before applying? Start tracking it with the credit score tracker template.

Expert Tips and Insights

Here are five practical strategies for getting a better deal on your next vehicle loan:

1. Know Your Credit Score Before You Visit Any Dealer

Pull your credit report before you step onto a lot. Federal law entitles you to a free report from each of the three major bureaus every year through AnnualCreditReport.com. Knowing your tier before you walk in means you’ll recognize whether the dealer’s quoted rate is fair or inflated.

2. A Small Score Improvement Can Jump You to a Lower Tier

The APR bands have clear cutoffs. If your score is 598 today, you’re in the Subprime tier at 12.08% APR. Push it to 605, and you drop into the Fair tier at 9.29%. On a $25,000 loan over 5 years, that shift alone saves you over $1,700 in total interest. The cutoff points are worth targeting.

3. A Meaningful Down Payment Cuts Your Borrowing Cost

A down payment reduces your principal. A smaller principal means less interest accruing over the life of the loan. On a $25,000 vehicle, a $3,000 down payment reduces your financed amount to $22,000. That shrinks every number in the results: your monthly payment, total interest, and total loan cost.

💡 Pro Tip: Aim for a down payment of at least 10% of the vehicle price. On a $25,000 car, that’s $2,500. It also protects you from going “underwater” on the loan, which happens when you owe more than the car is currently worth.

4. Shorter Terms Save You Real Money

A 7-year loan on $25,000 at 6.88% APR produces a monthly payment of $376, but you’ll pay $6,572 in total interest. The same loan at 5 years costs $494 per month, but the total interest drops to $4,617. That’s nearly $2,000 in savings by choosing a shorter term. Pick the shortest term your monthly budget can handle.

5. Get Pre-Approved Before You Walk Into the Dealership

Dealer financing isn’t always the best offer available. Credit unions and online lenders frequently beat dealer rates. The Consumer Financial Protection Bureau recommends getting at least one pre-approval offer from an outside lender before you negotiate. It gives you a benchmark and real negotiating power.

Common Mistakes to Avoid

Mistake 1: Focusing Only on the Monthly Payment

Many buyers ask, “What can you do to lower my monthly payment?” Dealers can always lower it by stretching the loan term. But that approach often costs thousands more in total interest. Always check the total loan cost, not just the monthly number.

Mistake 2: Walking In Without Knowing Your Credit Score

Going to a dealership without knowing your score is like buying a house without knowing your budget. You won’t be able to tell whether the APR you’re quoted is reasonable. Check your score first, every time.

Mistake 3: Financing the Full Purchase Price With No Down Payment

Cars lose value fast. New vehicles can lose 15% to 20% of their value in the first year alone. Financing 100% of the purchase price means you may owe more than the car is worth almost immediately. A down payment creates equity from the start.

Mistake 4: Taking the Dealer’s First Finance Offer

The rate on the finance office paperwork is rarely the best rate available to you. Dealers sometimes mark up the rate above what lenders actually quoted them. Compare any dealer offer against a pre-approval from your bank or credit union before you sign.

Mistake 5: Spreading Rate-Shopping Inquiries Too Far Apart

Each loan application triggers a hard inquiry on your credit report, which can temporarily lower your score. However, major credit scoring models see multiple auto loan inquiries made within 14 to 45 days as just one inquiry. Do all your rate shopping within that window to protect your score.

Frequently Asked Questions

What credit score do I need to get a good car loan rate?

A score of 661 or higher places you in the “Good” tier, which typically qualifies you for below-average interest rates on auto loans. Scores of 781 and above put you in the “Excellent” tier and unlock the lowest available APRs from most lenders.

Can I get approved for a car loan with a score under 500?

Yes, approvals are possible below 500, but your APR will fall in the deep subprime range, typically around 14% or higher. Raising your score before applying can save you a lot of money. This is important because financing can be much more expensive.

How does a down payment change my loan results?

A down payment reduces the amount you borrow. A smaller principal means lower monthly payments, less total interest, and a reduced overall loan cost. It also lowers the chance of owing more than the vehicle is worth.

What is the difference between APR and interest rate on a car loan?

The interest rate reflects only the cost of borrowing the principal. APR (Annual Percentage Rate) combines the interest rate with lender fees. This gives you a clearer picture of your total borrowing cost. Always compare APRs, not just interest rates, when shopping with many lenders.

How long of a loan term should I choose?

A 48 to 60-month term (4 to 5 years) works well for most borrowers. It keeps monthly payments manageable while limiting total interest paid. Loan terms over 72 months (6 years) increase your total interest cost and raise the risk of going underwater on the loan.

Will getting pre-approved hurt my credit score?

Pre-approval does involve a hard inquiry, which may lower your score by a few points temporarily. But credit scoring models like FICO group all auto loan inquiries made within a 14 to 45-day window into a single inquiry. Shopping with various lenders in a short timeframe keeps the credit impact minimal.

Does this calculator work for used car loans, too?

Yes. Enter the financed amount for your used vehicle and your current credit score. The APR estimates reflect general market averages and apply to both new and used vehicle financing.

What happens to my payment if I improve my credit score by 50 points?

It depends on where your score sits now. If a 50-point gain moves you into a lower APR tier, both your monthly payment and total interest will drop. For example, moving from the “Fair” tier (9.29% APR) to the “Good” tier (6.88% APR) on a $25,000 loan over 5 years saves about $29 per month and roughly $1,732 in total interest.

Bottom Line

We’ve covered every part of this guide. We talked about how credit score tiers relate to real APRs. We also explained the amortization formula behind each result. Finally, we looked at a comparison table that shows the dollar value of better credit.

Run this tool before setting a car budget. Know your numbers first. If your tier isn’t what you want, check the comparison table. It shows how much a score improvement is worth. That’s powerful information to have before you negotiate.

If this helped you think more clearly about auto financing, please share it with a friend who’s car shopping right now. It could save them thousands of dollars.