Credit report errors are more common than most people realize. If you’ve spotted something wrong on your report, knowing exactly where to start isn’t always clear. Credit reporting has consistently ranked as the most complained-about financial product in the CFPB’s Consumer Complaint Database (CFPB), with inaccurate information affecting millions of Americans every year.

Using a well-structured credit report dispute letter template gives you a legally sound, effective way to formally challenge incorrect items with any of the three major credit bureaus.

The right dispute letter triggers a mandatory investigation, and it can get the error removed for good.

Keep reading for free, ready-to-use templates, a step-by-step guide, and expert tips to dispute credit report errors the right way.

Download Your Free Credit Report Dispute Letter Templates

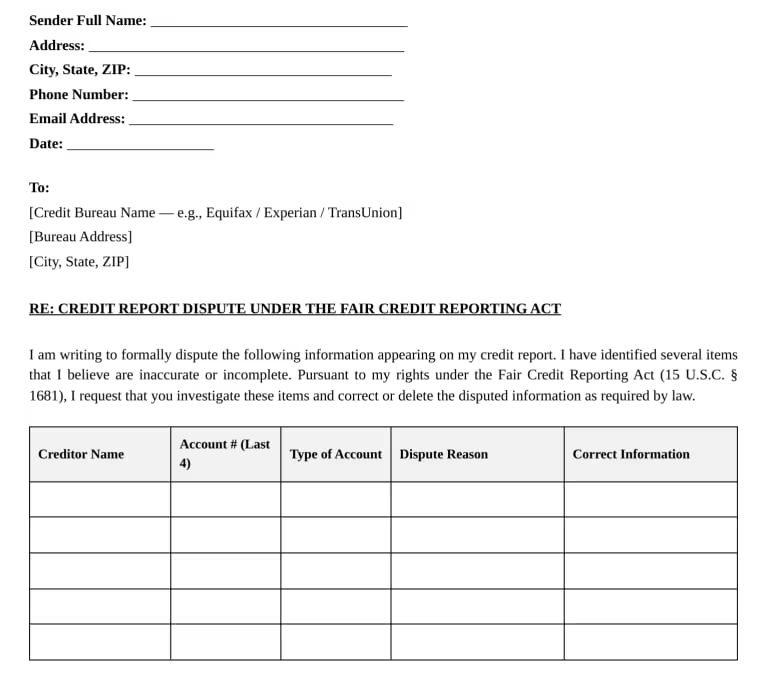

Three ready-to-use templates are available here to make the process as smooth as possible. Each one includes every section required under the Fair Credit Reporting Act. This includes your personal details, the credit bureau’s info, a dispute table for multiple accounts, and a signature block.

Pick the format that works best for you:

Disclaimer: The Templates & Printables on this site are provided for informational and personal tracking purposes only. This is not financial, legal, tax, or credit advice. While reasonable efforts are made to ensure accuracy, Credit Card Wind makes no warranties as to the completeness, reliability, or accuracy of the calculations generated by these Templates & Printables. Users are responsible for independently verifying all data and calculations. Terms, conditions, rates, regulations, and legal requirements vary by institution, jurisdiction, and individual circumstances.

Always refer to your official statements, account agreements, and applicable laws, and consult a qualified professional before making any financial, legal, or other important decisions. By using these Templates & Printables, you acknowledge that Credit Card Wind and its owner shall not be liable for any damages, losses, or financial consequences arising from the use or misuse of these Templates & Printables.

This universal disclaimer applies to all templates and printables provided by Credit Card Wind (https://creditcardwind.com), created by Robert Williams (Owner at Credit Card Wind).

© Credit Card Wind. All rights reserved.

These templates and printables may be downloaded and used for personal, non-commercial purposes only. Redistribution, resale, or modification for commercial use without permission is strictly prohibited.

What Is a Credit Report Dispute Letter?

A credit report dispute letter is a formal notice you send to one or more of the three major credit bureaus: Equifax, Experian, or TransUnion. You ask them to check and fix any wrong or missing information in your credit file.

The letter references your rights under the Fair Credit Reporting Act (FCRA), a federal law that guarantees every American the right to an accurate credit report. When a credit bureau gets your dispute, it has 30 days to investigate. It must either fix the information or remove it if it can’t be verified.

The CFPB’s Consumer Complaint Database shows that credit and consumer reporting have topped the bureau’s complaint rankings year after year. That means you’re not alone in dealing with this, and the dispute process exists specifically to protect you.

📌 Did You Know: You can get a free copy of your credit report from all three bureaus every week at AnnualCreditReport.com. Always check all three reports before writing a dispute letter. Each bureau maintains its own separate database, and errors don’t always show up the same way across all three.

How Credit Report Errors Hurt Your Credit Score

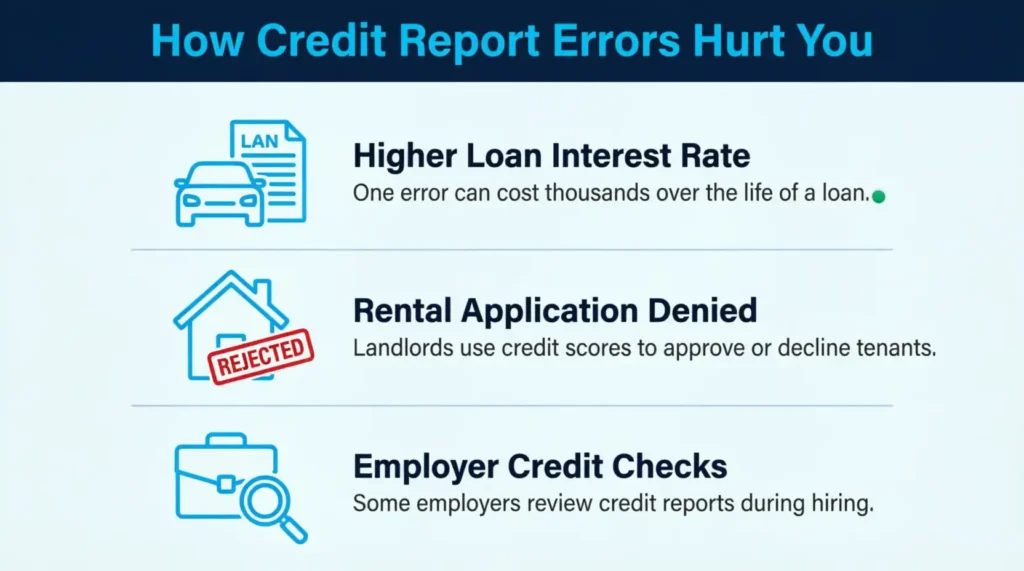

Your credit score is calculated directly from the data in your credit report. So when that data is wrong, your score takes the hit, whether you know about the error or not.

Even a single inaccurate item can cause real damage. A late payment that was never actually late, a collections account that belongs to someone else, or a duplicate entry can all push your score into a lower tier. And a lower score doesn’t just hurt on paper. It costs you money in very direct ways.

Lenders use your credit score to set interest rates. Landlords use it to decide whether to approve your rental application. Employers in certain states even review credit reports during the hiring process.

Take David, a 34-year-old teacher from Phoenix, as an example. He applied for a car loan and was quoted an interest rate 3.2 percentage points higher than his neighbor received for the same loan amount. After pulling his credit report, he found two collection accounts in his name from medical providers he had never visited. Those two errors cost him an estimated $1,800 in extra interest over the life of the loan before he even understood what had happened.

Credit report errors aren’t just a paperwork nuisance. They have real, measurable financial consequences that add up fast.

Common Credit Report Errors You Can Dispute

Not every issue on your credit file is worth challenging, but several types of errors are both widespread and worth acting on. The Federal Trade Commission identifies the following as the most common mistakes consumers make:

Personal information errors

These include misspelled names, outdated addresses, an incorrect Social Security number, or a date of birth that doesn’t match yours. While these don’t directly affect your score, they can signal that another person’s account data has merged into your file, a situation called a “mixed file.”

Account Status Errors

An account can show as open even when you’ve already closed it. It might also indicate past due status, even if you’ve paid it in full. These errors can unfairly drag your score down. These are among the most impactful errors to fix.

Incorrect payment history

A payment marked late when it was made on time is one of the most damaging errors you can find. Payment history makes up 35% of your FICO score, so even one wrongly reported missed payment can cause a significant drop.

Duplicate accounts

The same debt listed more than once makes your total debt load appear higher than it actually is. This inflates your credit utilization and lowers your score.

Accounts that don’t belong to you

These may result from identity theft, fraud, or a data mix-up. If a stranger’s account appears in your file, you have every right to dispute it and request an investigation.

Outdated negative information

Negative items, like late payments and collections, must be removed after seven years under the FCRA. Bankruptcies fall off after ten years. If an old item is still showing up past those deadlines, that is a clear, disputable error.

⚠️ Mistake to Avoid: Don’t try to dispute accurate negative information just because it hurts your score. Credit bureaus will verify the item and may mark your dispute as frivolous, which creates additional delays. Focus only on items that are factually incorrect, unverifiable, or outdated.

Understanding Your Rights Under the Fair Credit Reporting Act (FCRA)

The Fair Credit Reporting Act (15 U.S.C. § 1681) is the federal law that forms the foundation of every credit report dispute. It gives you specific, enforceable rights, and your dispute letter derives its authority directly from it.

The CFPB’s consumer rights page outlines your key protections:

The right to access your credit report.

You can request a free copy from each of the three major bureaus every week through AnnualCreditReport.com. This right exists regardless of whether you’ve been denied credit or not.

The right to dispute inaccurate information.

The bureau must investigate any item you think is wrong, incomplete, or unverifiable within 30 days of getting your dispute letter. If you submit additional supporting documents after filing, the bureau gets up to 45 days.

The right to a written response.

After the investigation closes, the bureau must send you the results in writing. If any changes were made, you’ll also receive a free updated copy of your credit report.

The right to add a consumer statement.

If your dispute is denied but you still believe the item is inaccurate, you can add a statement of up to 100 words to your credit file. Future lenders who pull your report will see your explanation alongside the disputed item.

The right to take legal action.

If a credit bureau knowingly ignores FCRA rules, you can seek legal action. This may include actual damages and statutory damages.

Knowing these rights gives your dispute letter real authority. When your letter references the FCRA by name and cites 15 U.S.C. § 1681, the bureau understands that you know the law and the deadline it is required to meet.

Tip: → Fixing an error before a big application? See how a corrected score could improve your odds with the mortgage pre-approval calculator.

Why Do You Need a Credit Report Dispute Letter Template?

Writing a dispute letter from scratch sounds straightforward, but most people underestimate what needs to go into it. A letter that lacks key details—like your account number, the type of error, or the correct information—can slow down the process. It may even lead the bureau to return your dispute as incomplete.

A well-designed template solves that problem. It helps you stay organized. It makes sure you don’t miss anything important. Plus, it presents your request in a format that bureaus can easily handle.

The templates on this page include everything you need:

- Your contact details

- The bureau’s address

- A table for listing multiple accounts

- A dispute reason checklist

- A section for supporting documents

- A signature block

The Word version includes formal FCRA legal language from Section 611 (15 U.S.C. § 1681i). This shows the bureau that you understand what the law requires from them.

💡 Pro Tip: If the same error appears on more than one bureau’s report, send a separate letter to each bureau. Credit bureaus don’t share dispute results with each other. A dispute resolved at TransUnion will not automatically update your Equifax or Experian file.

How to Use the Credit Report Dispute Letter Template (Step-by-Step Guide)

Using the template correctly from the start saves time and increases your chances of a successful outcome. Follow these steps to complete and send your dispute properly.

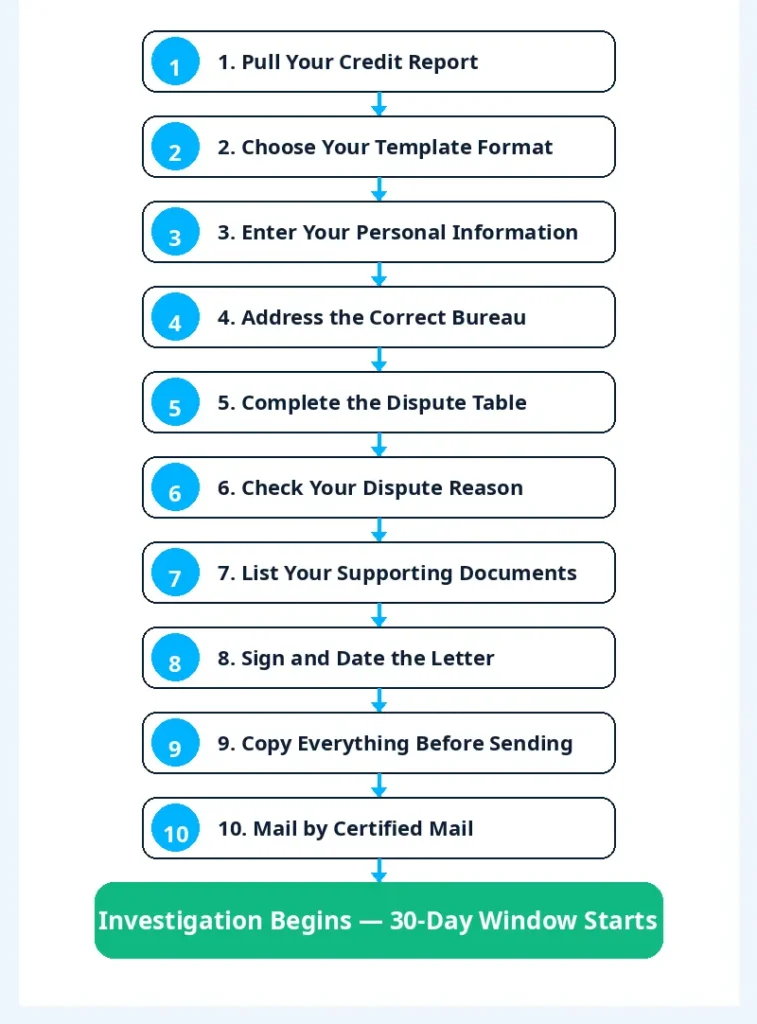

Step 1: Pull your credit report first.

Before filling out any template, get a free copy of your report from AnnualCreditReport.com. Review each section carefully and write down every item you plan to dispute. Don’t file from memory.

Step 2: Choose the right format.

Pick the template that fits your situation. Use the fillable PDF if you prefer typing everything digitally. Use the printable PDF if you plan to write by hand and mail the letter. Use the Word file if you want a formal letter with full paragraphs and FCRA legal language built in.

Step 3: Fill in your personal information.

At the top of the letter, enter your full name, street address, city, state, ZIP code, phone number, and email address. The Word template also has fields for your Social Security number and date of birth, which helps the bureau locate your file faster.

Step 4: Address the letter to the correct credit bureau.

Direct your letter to the bureau where the error is appearing. Use each bureau’s official dispute mailing address:

- Equifax: P.O. Box 740256, Atlanta, GA 30374

- Experian: P.O. Box 4500, Allen, TX 75013

- TransUnion: P.O. Box 2000, Chester, PA 19016

Step 5: Complete the dispute table.

In the PDF templates, fill in the following details:

- Creditor name

- Last four digits of the account number

- Account type (credit card, auto loan, mortgage, etc.)

- Dispute reason

- Correct information as it should appear

In the Word template, fill in the account name, full account number, and the reason for the dispute.

Step 6: Check your dispute reason.

The PDF templates include a dispute reason checklist.

Check all that apply:

- The account does not belong to me

- Incorrect balance

- Incorrect payment history

- Account duplicated

- Incorrect account status

- Identity theft or fraud

Step 7: Note your supporting documents.

Check the boxes for any documents you are including. This can be a government-issued photo ID, proof of address, billing statements, or a police report if your dispute involves fraud or identity theft.

Step 8: Sign and date your letter.

Always include a signature and printed name. An unsigned dispute letter is frequently returned without action.

Step 9: Copy everything before sending.

Make a copy of your completed letter and all supporting documents before putting anything in an envelope. Keep these copies in a safe place in case you need to follow up.

Step 10: Send by certified mail with return receipt.

Mailing your letter via USPS certified mail gives you a paper trail and proof of delivery. Keep the tracking number and the green return receipt card as part of your records.

💡 Pro Tip: Write the date you mailed the letter and the tracking number on your copy of the dispute letter right away. If you need to escalate later, this documentation is what proves the bureau received your dispute and when its 30-day investigation window began.

Tips for Writing an Effective Credit Report Dispute Letter

Getting the letter right on the first attempt saves time and improves your results. Keep these practical points in mind before sending.

Be specific about what is wrong.

Instead of writing “this account is incorrect,” explain exactly what the error is and what the correct information should be. The more precise your claim, the easier it is for the bureau’s investigator to verify and correct it.

Keep the tone professional and factual.

A dispute letter is a legal document. State the facts clearly, cite your rights under the FCRA, and avoid emotional language. A calm, factual letter is taken more seriously than a frustrated one.

Never send original documents.

Always send copies of supporting evidence, not originals. Bureau investigations can take up to 30 days, and keeping your original documents protects you if anything is lost or if you need to file again.

Dispute each account separately and clearly.

If you have errors across multiple accounts, list each one in its own row in the dispute table. Mixing multiple accounts into a single description creates confusion and can slow the investigation.

Follow up if you don’t hear back within 35 days.

If 35 days pass without a written response, follow up in writing. Note the date you originally mailed your letter and cite the bureau’s 30-day obligation under the FCRA. Keep a written record of every follow-up attempt.

Tip: → Planning a car purchase too? The car loan calculator by credit score shows what a corrected score could mean for your rate.

Real-Life Example: How Marcus Got His Credit Report Corrected

Marcus, a 41-year-old warehouse supervisor from Columbus, Ohio, noticed his credit score had dropped 87 points over the span of two months. When he pulled his credit report, he found a collection account for $1,240 from a medical provider he had never heard of. The account was listed under his Social Security number, but had an address that wasn’t his.

He downloaded the printable PDF template, filled in the dispute table with the creditor name and account details, and checked the “account does not belong to me” and “identity theft or fraud” boxes. He attached a copy of his driver’s license and a recent utility bill as supporting documents.

He sent the completed letter via USPS certified mail to TransUnion, where the account was appearing. Twenty-six days later, he got a written note. It confirmed that the account was investigated and removed from his report. His credit score recovered within one billing cycle.

The entire process cost him nothing but a stamp and about 20 minutes of his time.

Which Credit Bureau Should You Send Your Dispute Letter To?

One of the most common questions when starting a dispute is about the error’s location. The answer depends on where the error appears.

Start by reviewing your reports from all three bureaus. An inaccurate item may appear on only one bureau’s file, or it may show up across all three. Because each bureau maintains its own independent database, they don’t automatically apply each other’s corrections.

If an error appears on reports from all three bureaus, send a separate dispute letter to each one. Use the same template, but adjust the recipient address for each bureau and send each letter independently.

If an error appears on only one bureau’s report, direct your letter only to that bureau. There’s no need to contact bureaus that don’t show the error.

When in doubt, pull all three reports first and compare them side by side. That comparison tells you exactly where the problem lives.

Should You Dispute by Mail or Online?

Both methods are valid under the FCRA, but they come with different trade-offs worth considering.

Disputing by certified mail creates a paper trail. It allows you to include detailed supporting documents and provides proof of when the bureau received your letter. Most consumer advocates suggest using certified mail for initial disputes. This is especially true if the error is major, involves identity theft, or has complex documents.

Disputing online through each bureau’s dispute portal is faster and more convenient. Equifax, Experian, and TransUnion all have online platforms where you can submit your dispute and upload supporting files. However, online disputes can sometimes limit the detail you’re able to include. This can make it harder to document everything thoroughly if you ever need to escalate the process.

For most consumers, sending a completed letter through USPS certified mail is the best choice. This method works well when there’s a clear error backed by strong evidence. It creates a verifiable record and gives you more control over how your case is presented.

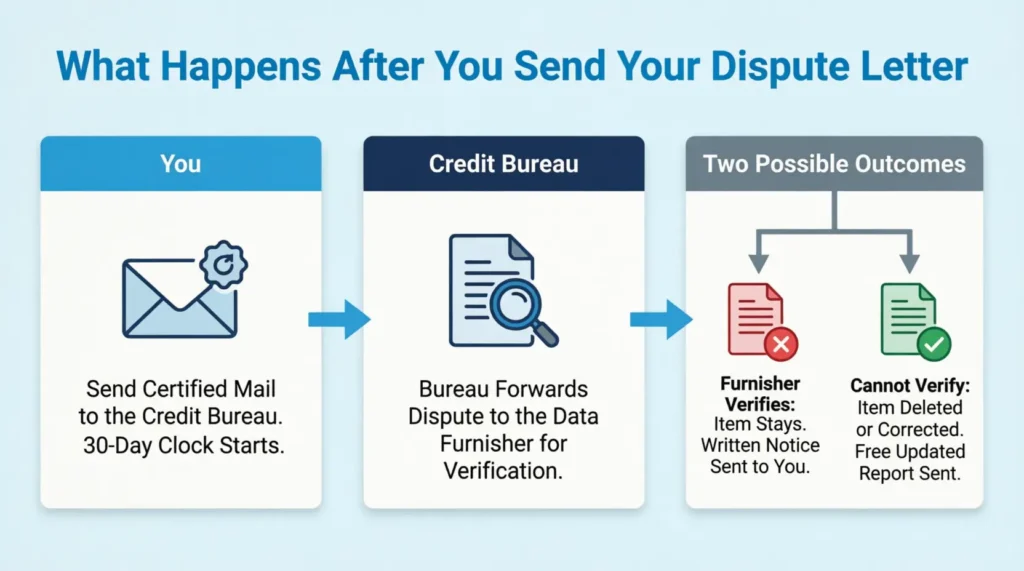

What Happens After You Send Your Dispute Letter?

Once the credit bureau receives your letter, the 30-day investigation window begins. Here is what happens during that period.

The bureau forwards your dispute to the company that originally reported the information, known as the “data furnisher.” This could be a credit card issuer, bank, medical billing company, or collections agency. The furnisher then reviews its own records to verify whether the information it reported is accurate.

If the furnisher confirms the information is correct, the bureau will keep the item on your report and notify you of the outcome in writing.

If the furnisher cannot verify the information within the investigation window, the bureau is required to delete or correct the item. You’ll receive written notification of the results and, if changes were made, a free updated copy of your credit report.

You can request the bureau to send a corrected version of your report to any creditor who received the old report within the last six months.

The CFPB’s dispute guide provides a full breakdown of the investigation process if you want to dig deeper into how it works.

How Long Does It Take to Remove Errors From Your Credit Report?

In most cases, the credit bureau must complete its investigation within 30 days of receiving your dispute. If you submit additional evidence after filing, the bureau is allowed up to 45 days to finish.

Once an error is confirmed and removed, it typically disappears from your report within a few days of the investigation closing. Your credit score recalculates at the next reporting cycle, which usually happens once a month.

Keep in mind that if the same inaccurate item appears on multiple bureaus’ reports, each bureau runs its own independent investigation on its own timeline. One bureau might resolve your dispute in 18 days while another takes the full 30. Sending your letters to all affected bureaus at the same time helps keep the timelines as close together as possible.

What to Do If Your Dispute Is Denied

A denied dispute doesn’t mean the process is over. Several practical options remain available.

Request a description of the investigation method.

Under the FCRA, you can ask the bureau to explain exactly how it verified the disputed item. If the investigation was incomplete or relied on unconfirmed data, that is grounds for filing a new dispute with additional evidence.

Dispute directly with the data furnisher.

Beyond disputing with the bureau, you can also send a dispute letter directly to the original company that reported the information. That company has its own legal obligation to investigate and correct inaccurate data under the FCRA.

Add a consumer statement to your credit file.

If the bureau maintains the item is accurate and you still disagree, you can add a written explanation of up to 100 words directly to your credit file. Future lenders who pull your report will see your statement alongside the disputed item.

File a complaint with the CFPB.

If you believe the bureau failed to conduct a proper investigation or violated your rights under the FCRA, file a formal complaint through the CFPB’s website. Bureaus are required to respond to CFPB complaints.

Consult a consumer protection attorney.

In cases of willful FCRA violations, you may have legal grounds to seek damages. Many consumer attorneys offer free initial consultations for credit-related cases.

How Fixing Credit Report Errors Helps Your Credit Card Approvals

Credit card issuers review your full credit report when you apply. Just one incorrect negative item, like a late payment you didn’t make or a collections account that isn’t yours, can drop your credit score. This change can greatly affect your application outcome.

Fixing those errors can have a meaningful impact on both your approval odds and the terms you’re offered. A cleaner, more accurate credit file doesn’t just improve your score. It helps you get better credit card products.

You can enjoy lower APRs, higher credit limits, and premium rewards cards. These options need good or excellent credit to qualify.

Jennifer is a 38-year-old marketing coordinator from Denver. She spent eight months applying for a travel rewards card. Sadly, she got declined each time. After reviewing her credit report, she found a duplicate credit card account. This account was from a closed card but still appeared as active.

The duplicate was inflating her apparent credit utilization rate by nearly 30%. After disputing and removing it, her score increased by 44 points. She was approved for the travel card on her next application.

Disputes take time. But for anyone planning a significant credit application in the next six to twelve months, clearing up errors first is one of the most valuable steps you can take.

Frequently Asked Questions

Can I dispute a credit report error for free?

Yes. Disputing errors on your credit report is completely free under the Fair Credit Reporting Act. Credit bureaus are not allowed to charge any fees for submitting or processing a dispute.

Can I dispute multiple errors in a single letter?

Yes. The templates on this page include a dispute table with multiple rows so you can list several accounts or errors in one submission. Include each item on its own row with its own dispute reason and correct information.

Do I need a lawyer to send a dispute letter?

No. Any consumer can send a dispute letter on their own without legal help. An attorney may be useful only if your dispute is repeatedly denied or if you believe the bureau has willfully violated the FCRA.

What if the credit bureau does not respond within 30 days?

If the bureau misses the 30-day deadline without resolving or closing your dispute, it may be in violation of the FCRA. Document your timeline carefully and consider filing a complaint with the CFPB or speaking with a consumer attorney.

Will filing a dispute hurt my credit score?

No. Submitting a credit report dispute does not affect your score. If the dispute results in the removal of an inaccurate negative item, your score may improve once the corrected report is updated.

Can I dispute an error online instead of by mail?

Yes. All three major bureaus have online dispute portals. However, certified mail is often recommended for first-time or complex disputes because it creates a verifiable delivery record and allows you to include detailed supporting documents.

How many times can I dispute the same item?

You can dispute the same item more than once, but bureaus may classify a repeated dispute as frivolous if no new information is provided. Submit fresh supporting evidence with each new attempt to avoid that outcome.

What is a consumer statement and when should I use one?

A consumer statement is a brief explanation of up to 100 words that you can add to your credit file if a dispute is denied. Lenders who pull your report can see it. It doesn’t change the disputed item, but it gives future creditors important context.

How will I know if my dispute was successful?

The credit bureau is required by law to notify you of the investigation results in writing. If the disputed item was corrected or removed, you will also receive a free updated copy of your credit report.

Should I send the same dispute letter to all three credit bureaus?

Only if the error appears on all three reports. Pull your reports from all three bureaus first and check each one separately. If the error only shows up at one bureau, send your dispute only to that bureau.

Bottom Line

Credit report errors don’t fix themselves, and they don’t wait for a convenient time to damage your score.

To improve your chances of removing inaccurate information, follow these three steps:

- Understand your rights under the FCRA.

- Identify the specific errors in your file.

- Use a well-structured dispute letter.

The templates on this page are free, ready to use, and cover every required element. Whether you prefer the fillable PDF, the printable version, or the formal Word letter with FCRA legal language built in, all three are available for download right now.

For most consumers with proven errors, the best way is to send a certified mail dispute letter. Address it to the bureau where the error shows up. It meets every FCRA requirement, creates a paper trail, and gives you a solid record if escalation becomes necessary.

If you know someone facing a credit report error, share this guide and free templates. They could save money and avoid months of hassle.