Missing a credit card payment puts both parties in an uncomfortable position. Informal reminders rarely work, and phone calls are easy to ignore. Federal Reserve Bank of New York data shows delinquency rates have climbed since 2022, making documented communication more important than ever. A credit card overdue notice template gives creditors a structured, professional way to request payment.

A formal overdue notice clearly states what is owed, how many days the account is late, and how to pay.

Read on for free downloadable templates in five formats. You’ll also find a step-by-step fill guide and expert tips on timing and tone that truly get results.

Download Your Free Credit Card Overdue Notice Templates

Five ready-to-use formats are available below. Each one includes all the essential fields a professional overdue notice should have. Pick the format that works best for your situation:

Disclaimer: The Templates & Printables on this site are provided for informational and personal tracking purposes only. This is not financial, legal, tax, or credit advice. While reasonable efforts are made to ensure accuracy, Credit Card Wind makes no warranties as to the completeness, reliability, or accuracy of the calculations generated by these Templates & Printables. Users are responsible for independently verifying all data and calculations. Terms, conditions, rates, regulations, and legal requirements vary by institution, jurisdiction, and individual circumstances.

Always refer to your official statements, account agreements, and applicable laws, and consult a qualified professional before making any financial, legal, or other important decisions. By using these Templates & Printables, you acknowledge that Credit Card Wind and its owner shall not be liable for any damages, losses, or financial consequences arising from the use or misuse of these Templates & Printables.

This universal disclaimer applies to all templates and printables provided by Credit Card Wind (https://creditcardwind.com), created by Robert Williams (Owner at Credit Card Wind).

© Credit Card Wind. All rights reserved.

These templates and printables may be downloaded and used for personal, non-commercial purposes only. Redistribution, resale, or modification for commercial use without permission is strictly prohibited.

What Is a Credit Card Overdue Notice?

A credit card overdue notice is a formal written document sent to an account holder whose payment is past due. It tells the recipient exactly how much they owe, how many days late the payment is, and what steps they need to take to bring the account current.

This kind of notice is very different from an informal reminder. It’s a documented, professional communication that creates a paper trail for the creditor. That paper trail becomes critical if the account ever needs to go to collections or legal review later.

The Federal Reserve Bank of New York’s household debt and credit data shows that credit card delinquency rates have risen consistently since 2022. That trend makes clear, documented creditor communication more important than it has been in years.

Overdue notices are commonly used by:

- Small business owners who extend store credit or offer payment plans

- Credit card issuers and financial institutions

- Property managers tracking tenant accounts

- Finance departments within larger organizations

Unlike a collection’s letter, an overdue notice is the first formal step in the payment recovery process. The tone is firm but not aggressive. The goal is to give the account holder a reasonable chance to resolve the issue before things escalate.

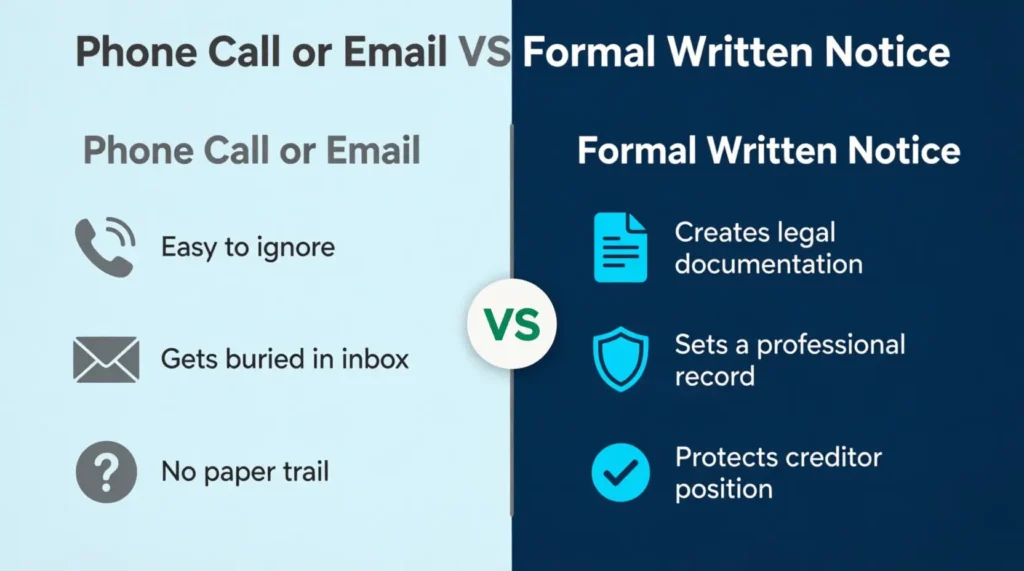

Why a Written Overdue Notice Works Better Than a Phone Call

Have you ever left a voicemail about a late payment and never heard back? You’re not alone. Phone calls get ignored. Emails get buried. A formal written notice is harder to dismiss. It signals that the matter is being handled seriously and that a record is being created.

Three reasons a written notice outperforms informal follow-ups every time:

1. It documents everything. A written notice records the amount owed, the due date, and exactly when the notice was sent. If the debt ever goes to collections or ends up in a legal dispute, this documentation is invaluable. Without it, creditors have a much harder time proving timely communication.

2. It sets a professional tone. A formal document alerts the account holder that this situation is being monitored. Many recipients pay faster simply because they understand the situation is now on paper.

3. It helps creditors stay legally protected. The Fair Debt Collection Practices Act, enforced by the Federal Trade Commission, requires third-party debt collectors to send a written notice within five days of first contact. Creditors who send written notices early are in a better spot if the account goes to collections.

Take Marcus as an example. He’s a freelance accountant. He handles billing for a small dental practice in Columbus, Ohio. After three accounts were overdue for over 90 days in a year, he changed from casual emails to formal written notices.

Within the next six months, he recovered payments on two of those accounts without involving a collections agency. The notices provided each account holder with a clear deadline and several payment options. This made a big difference.

📌 Did You Know: Under the FDCPA, once a written notice is sent, the debtor has 30 days to dispute the debt in writing. Creditors who skip the written notice step lose the ability to rely on this timeline if a dispute arises later. A well-documented notice protects both sides from misunderstandings.

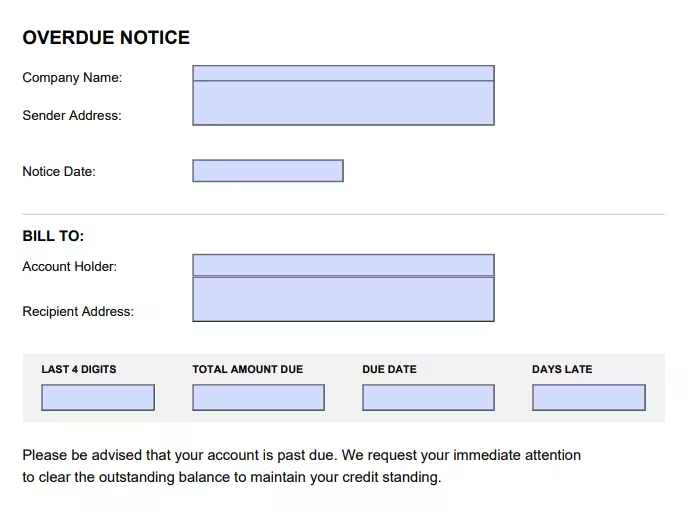

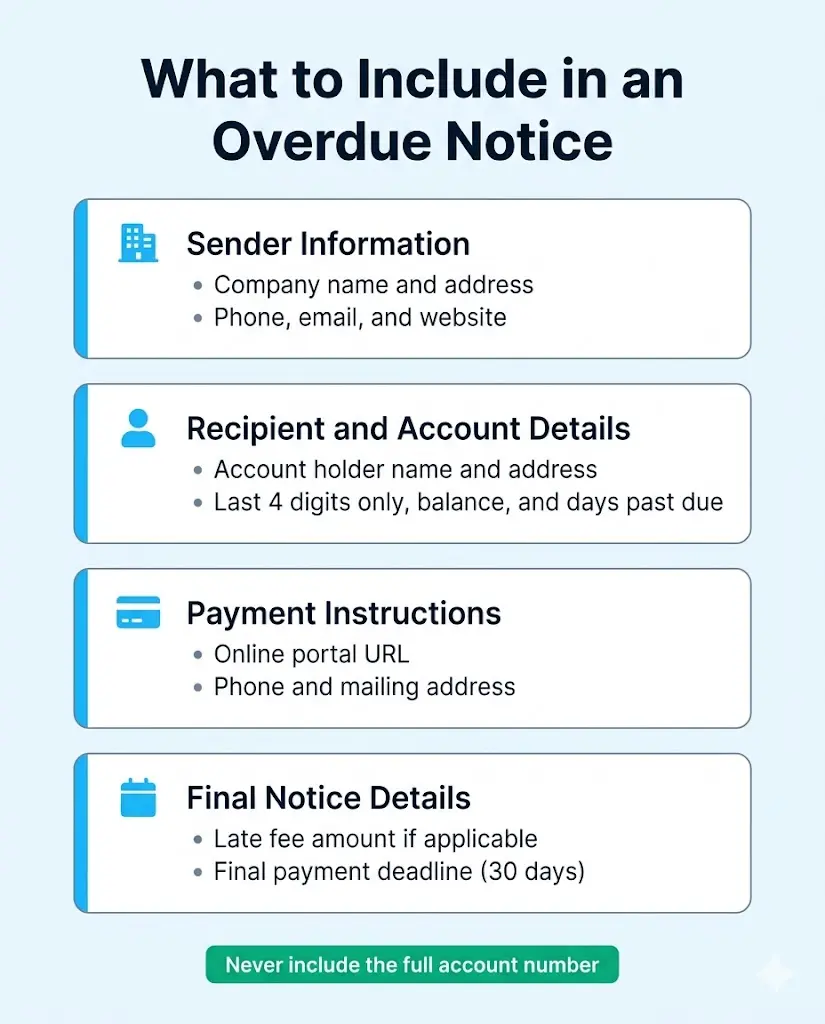

What Every Overdue Payment Notice Should Include

A strong notice is clear, specific, and easy to act on. Vague notices get ignored. Detailed ones get results. So what should actually go inside one?

Sender Information

- Company name and full mailing address

- Phone number, email address, and website for follow-up questions

Recipient Information

- Full name of the account holder

- Current mailing address

Account Details

- Last 4 digits of the credit card or account number (never the full number)

- Total amount due, including any applied late fees

- Original payment due date

- Number of days the payment is currently past due

Payment Instructions

- Online payment portal URL

- Phone number for phone payments

- Mailing address for check payments

Final Details

- Whether a late fee has been applied, and the percentage or dollar amount

- An authorized signature from a company representative

- A final payment deadline, typically 30 days from the notice date

⚠️ Mistake to Avoid: Never include a full account number on a mailed overdue notice. Using only the last 4 digits protects the account holder from identity theft and keeps the creditor in line with data privacy best practices. All five templates in this collection follow this rule by design, displaying the account in the standard ****XXXX format.

How to Fill Out the PDF and Word Templates

The PDF and Word templates are designed for single-account use. Each follows a professional letter format. It takes less than five minutes to fill in once you have the account details ready.

For the PDF Fillable Templates (US Letter and A4)

These are AcroForm PDFs, so every field is clickable. Open the file in Adobe Acrobat or any modern PDF viewer, click each field, and type directly into the form.

Fields to complete:

- Company Name and Sender Address at the top

- Notice Date (use the date you plan to send, not the original due date)

- Account Holder Name and Recipient Address in the Bill To section

- Last 4 Digits, Total Amount Due, Due Date, and Days Late in the account summary table

- Online payment URL, payment phone number, and mailing address in the Payment Methods section

- Whether a late fee has been applied

- Authorized Signature and any Office Notes

Save a completed copy for your records before printing and sending.

For the Word Templates (US Letter and A4)

Open the file in Microsoft Word. Each placeholder appears in brackets. Click any placeholder text and start typing over it.

Key fields to replace:

- [SENDER COMPANY NAME] and all contact details in the letterhead

- [ACCOUNT HOLDER FULL NAME] and their current mailing address

- [MASKED ACCOUNT NUMBER] shown in ****XXXX format

- [OUTSTANDING BALANCE], [ORIGINAL DUE DATE], and [NUMBER OF DAYS PAST DUE]

- [PAYMENT METHOD DESCRIPTION], [PAYMENT WEBSITE OR PORTAL URL], and [PAYMENT PHONE NUMBER]

- [FINAL PAYMENT DATE] in the payment summary table

- [AUTHORIZED REPRESENTATIVE NAME] and title in the signature block

The Word templates also include a company logo placeholder in the top-left corner. Replace it with your actual logo or remove it if you prefer a text-only header. Save a copy with the account holder’s name in the file name so you can find it easily later.

How to Use the Excel Template to Manage Multiple Accounts

The Excel template is the most powerful format in this collection. It’s not just a notice generator. It’s a complete account management tool. It can handle many overdue accounts at once. It auto-calculates days past due and late fees. Plus, it creates a print-ready notice with just one number change.

The workbook contains four sheets:

Sheet 1: Instructions

A plain-English guide to using the template. Read this sheet first if you’re opening the file for the first time.

Sheet 2: Data

This is where all account records live. Each row represents one account holder. The 12 columns are:

| Column | What to Enter |

|---|---|

| RecordID | A unique identifier for each account |

| AccountHolderName | Full legal name of the cardholder |

| RecipientAddress | Current mailing address |

| Last4Digits | Last 4 digits of the credit card only |

| MaskedAccountNumber | Auto-fills in ****XXXX format |

| AmountDue | Original overdue balance in dollars |

| OriginalDueDate | Date the payment was first due |

| NoticeDate | Auto-fills as today’s date |

| PaymentURL | Online payment portal address |

| PaymentPhone | Customer service phone number |

| MailPaymentAddress | Address for mailing check payments |

| LateFeePercent | Late fee rate (enter 5 for 5%) |

Sheet 3: PrintableNotice

This sheet creates a ready-to-print overdue notice. It formats the notice based on the account record you choose. To switch between accounts, change the number in cell N1 (labeled “SelectedRow”) to the row number from the Data sheet.

The sheet automatically pulls all account details. It counts the days past due. Then, it applies the late fee percentage to find the late fee amount. Finally, it shows the total amount due. The layout is already formatted to fit one US Letter page. Print using Ctrl+P.

Sheet 4: Disclaimer

Contains legal and copyright information for the template.

💡 Pro Tip: After entering all account records in the Data sheet, add a custom column for “Notice Sent Date” and a second one for “Follow-Up Date.” This keeps your outreach schedule tidy for all accounts. It also helps you see which accounts are nearing the 30-day or 60-day mark before moving to collections.

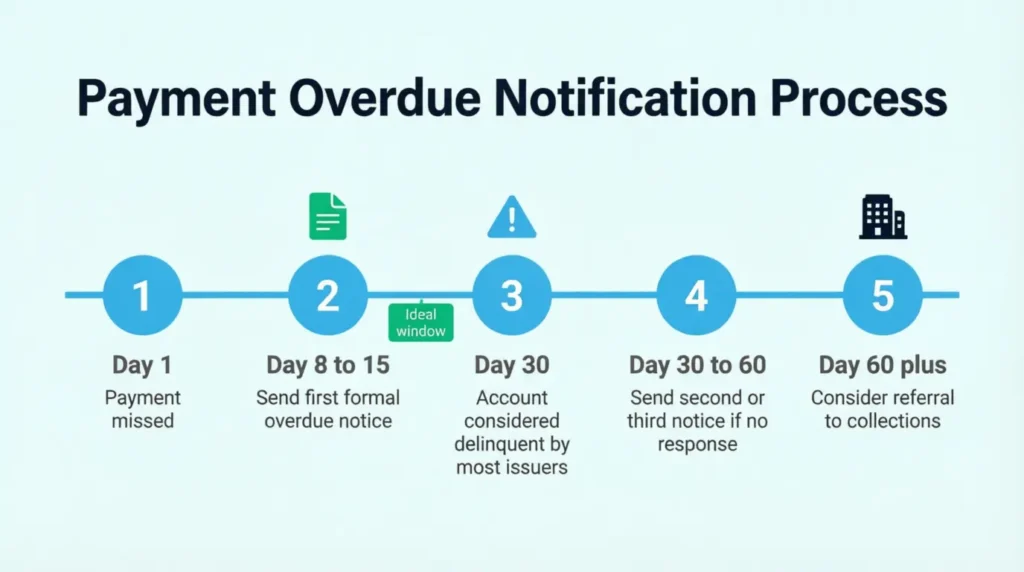

When Is the Right Time to Send an Overdue Notice?

Timing matters more than most creditors realize. Send too early, and the notice feels premature. Wait too long, and the account becomes significantly harder to recover.

A practical timeline that works for most creditors:

| Days Past Due | Recommended Action |

|---|---|

| 1 to 7 days | Send an informal reminder by email or text |

| 8 to 15 days | Send the first formal overdue notice |

| 16 to 30 days | Send a second notice with a firm final payment deadline |

| 31 to 60 days | Issue a final notice before referring to collections |

| 60+ days | Refer the account to a collections agency or legal counsel |

Most creditors send the first formal notice between 8 and 15 days after a missed payment. This gives the account holder enough time to address a genuine oversight, without letting the debt age unnecessarily.

For credit card issuers, a payment is typically considered delinquent after 30 days past due. Sending a formal written notice before that threshold shows proactive, documented communication. This approach helps maintain a strong position for the creditor.

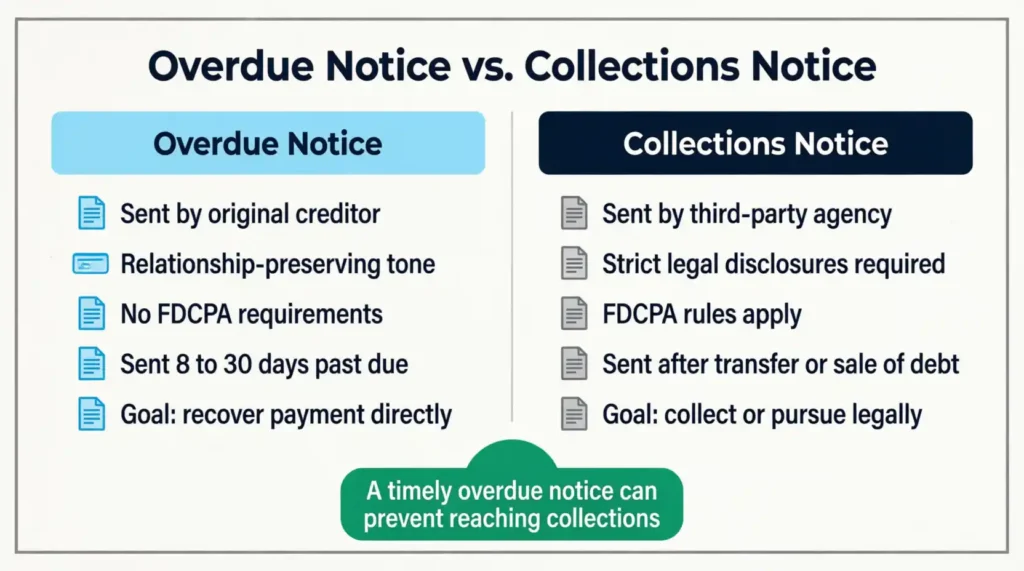

Overdue Notice vs. Collections Notice: What’s the Difference?

These two documents have different purposes. Sending the wrong one at the wrong time can lead to problems.

An overdue notice is an early-stage communication sent directly by the original creditor. The tone is professional and firm. It suggests that the account holder might have just forgotten or faced a temporary problem. The goal is to recover the payment without damaging the relationship or pulling in a third party.

A collections notice is sent after the debt has been transferred or sold to a third-party agency. At that stage, the FDCPA kicks in with strict requirements. Specific disclosures must appear in writing. Contact times and methods are restricted. The debtor gains the right to request written verification of the debt.

At a glance:

| Feature | Overdue Notice | Collections Notice |

|---|---|---|

| Sent by | Original creditor | Collections agency |

| Timing | Early stage (8 to 60 days) | Late stage (60 to 180+ days) |

| Tone | Professional reminder | Formal legal demand |

| Legal requirements | Varies by state | Governed by the FDCPA |

| Goal | Recover payment directly | Collect on behalf of creditor |

Sending a clear, well-timed overdue notice can stop the account from reaching the collections stage. This action benefits both parties involved.

Tip: → Need to include accrued interest on the overdue amount? The daily credit card interest calculator gives you the exact figure.

Common Mistakes to Avoid When Sending an Overdue Notice

Even a well-written notice can backfire if a few basic rules are ignored. These are the most frequent errors creditors make, and how to avoid each one.

Using accusatory or emotional language

Phrases like “you failed to pay” or “you have repeatedly ignored our reminders” put the recipient on the defensive. Neutral, factual language like “your account is currently past due” gets better results and is far less likely to trigger a dispute.

Leaving out payment options

A notice without clear payment instructions leaves the recipient with no actionable next step. Always include at least two ways to pay: an online option and a mailing option at a minimum. Adding a phone payment option gives three paths, which reduces friction further.

Skipping certified mail for high-balance accounts

For accounts over a certain limit, send the notice by certified mail. This way, you get proof of delivery with a return receipt. This matters significantly if the account ends up in collections or a legal dispute later.

Including the full account number

This is a data privacy and security issue. The templates in this collection use only the last 4 digits by design, displayed in the standard ****XXXX format. Never deviate from this practice.

Waiting more than 30 days to send the first notice

The longer a creditor waits, the harder it becomes to recover the payment. Accounts that are 90 days past due and lack formal communication are much harder to collect. Plus, the cost to recover them rises quickly at this point.

⚠️ Mistake to Avoid: Always verify the account holder’s current mailing address before sending a formal notice. Sending to an outdated address provides no legal protection and delays the entire recovery process. Check the mailing address against the most recent account records before printing anything.

Frequently Asked Questions

What is the difference between an overdue notice and a demand letter?

An overdue notice is an early-stage reminder that a payment is past due, sent directly by the creditor. A demand letter is a formal legal document, often sent by an attorney. It formally requests payment before any legal action is taken.

How many overdue notices should I send before moving to collections?

Most creditors send two to three formal notices over a 30 to 60-day period before referring an account to a collections agency. The exact number depends on internal policy and the size of the outstanding balance.

Can I send an overdue notice by email?

Yes, email is acceptable. For higher-balance accounts, sending a physical copy by certified mail gives proof of delivery. An email can’t provide that.

Is there a legally required format for an overdue notice?

No single federal law mandates a specific format for a creditor-to-debtor overdue notice. If a third-party collector takes over, the FDCPA says they must give certain disclosures in their first written message.

What should I do if the account holder disputes the balance on the notice?

Keep all payment records and account history on file before sending any notice. If there’s a dispute, check the notice details against the original account statements. Then, respond in writing instead of calling.

How long should copies of sent overdue notices be kept?

Hold onto records for three to seven years. This depends on the debt collection statute of limitations in the account holder’s state. Some states allow debts to be legally pursued for up to ten years.

Can a late fee be included in an overdue notice?

Yes, if the original cardholder agreement or credit contract includes a late fee provision. The notice must clearly say if a late fee is added and how much it increases the total balance.

What is the best way to track multiple overdue accounts at once?

The Excel template in this collection handles exactly this. Each row in the Data sheet shows one account. The PrintableNotice sheet automatically creates a formatted notice for the account you choose by its row number.

Does receiving an overdue notice affect the account holder’s credit score?

The notice itself does not impact credit scores. If the payment remains unpaid and gets reported as delinquent, it can hurt the account holder’s score. This drop can be significant, usually by 50 to 100 points or even more, based on the overall account history.

Can a small business owner use these templates without a legal or finance background?

Yes. These templates are designed to be simple enough for any business owner to use without specialized expertise. Each field is clearly labeled. The Excel template has an Instructions sheet to guide users through the process.

Bottom Line

A well-timed overdue notice shows the debt clearly. It gives the account holder a clear path to resolve it. This notice also protects the creditor’s position if the situation escalates.

Based on this guide, send the first formal notice 8 to 15 days after a missed payment. Include at least two payment options in the notice.

Make sure to keep a saved copy on file for your records. The credit card overdue notice templates above help you start quickly. They work for any account size or format you like.

If you know a small business owner or finance professional dealing with overdue accounts, share this page with them. A ready-to-use notice template can save hours of back-and-forth and help move payments forward faster.