Credit Card Debt Snowball Calculator

Plan your path to zero debt with the Snowball or Avalanche method.

Ready to See Your Plan?

Your personalized debt payoff plan will appear here. Fill in your details on the left and click 'Calculate' to get started.

Your Payoff Plan

Debt Balance Over Time

| Month | Date | Payment | Principal | Interest | Balance |

|---|

Important: This calculator uses simplified monthly interest calculations. Actual credit card interest is calculated using the Average Daily Balance (ADB) method, which accounts for your daily balance and payment timing throughout the billing cycle.

The estimates below assume paying immediately when your statement closes (rather than waiting until the due date), which can reduce your average daily balance. However, actual savings will vary based on:

- Your specific card issuer's calculation method

- When you make purchases during the cycle

- Whether you have a grace period on new purchases

- The exact number of days in each billing cycle

Note: This requires a 'Billing Due Date' for each debt in the input section.

Disclaimer: These savings estimates are approximations only and may not reflect your actual interest charges. Always verify with your credit card statements.

How to Use This Calculator

Add each of your debts (name, balance, APR, and minimum payment).

Enter any extra amount you can pay each month toward your debts.

Choose your strategy: Snowball (targets smallest debt balance first) or Avalanche (targets highest APR first).

Click Calculate to see your personalized payoff timeline and total interest paid.

Use the PDF/CSV buttons to save your plan or the Copy Link button to share it.

Disclaimer: This calculator is for informational purposes only. Interest calculations use a simplified monthly method and may not match your actual credit card statements. Real credit cards typically use Average Daily Balance (ADB) calculations that account for daily balance changes and payment timing. Your actual interest charges may differ based on when you make payments, purchase timing, grace periods, and your card issuer's specific calculation method. The results are estimates based on the information you provide and may not be accurate or applicable to your specific financial situation. The information provided does not constitute financial, legal or tax advice. We do not guarantee the accuracy of the calculations or the applicability of any information. Always consult a qualified financial professional for advice specific to your personal circumstances. Credit card terms, conditions, rates and offers are subject to change by the issuing bank at any time. We are not responsible for any actions or decisions taken based on the information provided by this tool.

Juggling multiple credit card balances can feel overwhelming. You pay every month, but the totals barely move. The Federal Reserve Bank of New York reports Americans now owe a record $1.28 trillion in credit card debt as of Q4 2025. A credit card debt snowball calculator can map your exact path to zero.

The snowball method targets your smallest balance first, then rolls that freed-up payment onto the next debt.

Keep reading for a step-by-step guide. You’ll find the real formula for the tool, a worked example, and expert tips. These will help you create a debt payoff plan that works.

Tip: → Got your snowball order? Log your progress month by month with the credit card payoff tracker template.

What Is a Credit Card Debt Snowball?

The debt snowball is a structured payoff strategy. It focuses on clearing your lowest credit card balance first, while paying only the minimum on every other account you have.

When the smallest debt is paid off, take that full payment. Add it to the minimum payment for your next smallest balance. That “snowball” grows bigger with each debt you clear. The freed money compounds month after month, building speed the further along you go.

The concept was made popular by personal finance educator Dave Ramsey. Today, it stands as one of the most widely taught debt reduction strategies in America.

It’s worth noting that the snowball method is built more for motivation than pure math. You won’t always pay the least interest possible by starting with the smallest balance. For many, completely clearing even a small account gives a big psychological boost. This win helps keep the entire plan on track when times get tough.

The numbers behind American credit card debt make a clear case for having any plan at all. The Federal Reserve Bank of New York’s Q4 2025 Household Debt and Credit Report confirms credit card balances reached $1.28 trillion by the end of 2025, a new all-time high and a 5.5% jump from just one year earlier.

For anyone carrying a balance month to month, that trend matters. High-interest debt compounds quickly when there’s no structured payoff plan in place.

How This Calculator Works

This credit card debt snowball calculator handles the complete math of your debt payoff plan in real time. Here’s exactly what each part of the tool does:

Multiple Debt Entry

You can add as many debts as you need. For each one, you provide:

- The account name (for easy reference in your results)

- Current balance

- Annual percentage rate (APR)

- Your minimum monthly payment

- An optional due date (used for the Billing Cycle Planner)

Extra Monthly Payment

This field is where the real acceleration happens. Enter any amount above your combined minimum payments that you can put toward debt. Even a modest extra $50 or $75 per month can shave months off your payoff timeline.

Payoff Method Toggle

The tool supports both the snowball method (lowest balance first) and the avalanche method (highest APR first). You can flip between them with one click to compare both outcomes for your situation immediately.

Start Date

Pick the month you want to begin. The calculator uses this to give you a real calendar payoff date, not just an abstract number of months.

Results Panel

After clicking Calculate, the tool displays:

- Your projected payoff date

- Total months to debt freedom

- Total interest you’ll pay

- Total amount paid (principal plus interest)

Debt Balance Chart

A live line chart shows your total balance dropping each month. Watching that curve move toward zero is one of the most motivating features in the tool.

Amortization Table

Toggle this on for a full month-by-month breakdown: payment made, part applied to principal, interest charged, and your remaining balance after each payment.

Billing Cycle Planner

This bonus section shows how much you can save in interest. Pay your card right after your statement closes. Don’t wait for the due date. It assumes a typical 25-day gap between statement close and due date to calculate the estimate.

Export and Share

You can download your full results as a PDF or CSV file. There’s a “Copy Link” button that saves your entire plan as a shareable URL. This feature is perfect for bookmarking it or sending it to a financial counselor.

💡 Pro Tip: Use the “Copy Link” feature before closing the tab. Your full plan is encoded into that URL, so you can return to your exact entries at any time without starting over.

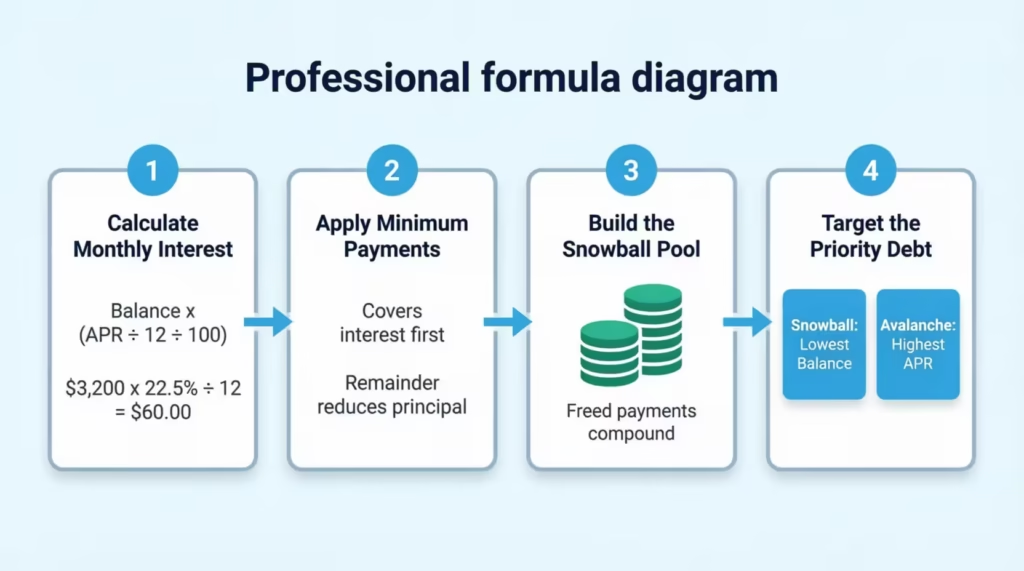

The Formula Explained

The calculator uses standard monthly compound interest math. Here’s what happens under the hood during each calculation cycle:

Step 1: Calculate Monthly Interest for Each Debt

The formula is:

Monthly Interest = Balance × (APR ÷ 12 ÷ 100)

For example, a $3,200 balance at a 22.5% APR accrues:

$3,200 × (22.5 ÷ 12 ÷ 100) = $60.00 in monthly interest

Step 2: Apply Minimum Payments

Each month, the tool applies your minimum payment to each debt. The payment first covers that month’s interest charge. Whatever remains after interest reduces the principal balance.

Step 3: Build the Snowball Pool

Once a debt reaches zero, its least payment doesn’t disappear. It gets added to a growing extra payment pool. This is the snowball effect in action. As each debt clears, the amount available to throw at the next target keeps growing.

Step 4: Target the Priority Debt

The snowball pool gets applied to one debt at a time:

- Snowball mode: the debt with the lowest current balance gets hit first

- Avalanche mode: the debt with the highest APR gets targeted first

The tool re-sorts your debts fresh every single month to make sure the correct debt always gets the extra funds.

Why does this formula matter in the real world? Data from the Federal Reserve’s G.19 Consumer Credit Report puts the average APR for cards actively accruing interest at 22.30% in Q4 2025. At that rate, a $5,000 balance left untouched for a full year generates more than $1,100 in interest charges on its own. That’s why a focused payoff strategy beats minimum-only payments every time.

⚠️ Mistake to Avoid: If your minimum payment is lower than your monthly interest charge, your balance will grow every month even though you’re making payments. The calculator flags this with a warning. Always set your minimum payment above the monthly interest amount to actually reduce what you owe.

How to Use This Calculator (Step by Step)

Follow these steps to build your personal payoff plan:

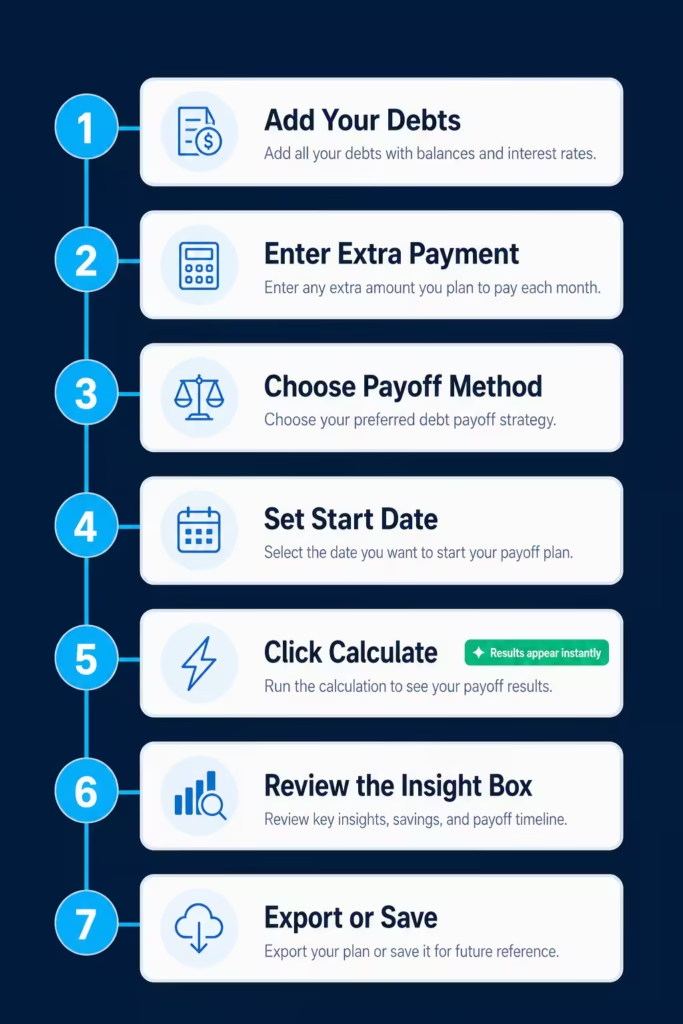

Step 1: Add Your Debts

Click “Add Another Debt” for each credit card you want to include. Enter the account name, current balance, APR, and your least monthly payment. Pull these numbers directly from your most recent credit card statement for the most accurate results. Don’t estimate, especially for the APR.

Step 2: Enter Your Extra Monthly Payment

In the “Extra Monthly Payment” field, enter any amount you can put toward debt above your combined minimums. Start with whatever’s realistic for your budget. Even $25 to $50 extra per month moves the needle more than most people expect.

Step 3: Choose Your Payoff Method

Use the toggle to select Snowball or Avalanche. If staying motivated is your biggest challenge, choose Snowball. If you want to minimize total interest paid and can stay committed either way, choose Avalanche.

Step 4: Set Your Start Date

Select the month and year you plan to begin. This gives you a specific calendar date for your projected debt-free day, which makes the goal feel much more tangible.

Step 5: Click Calculate

Hit the blue Calculate button. Your results appear on the right panel instantly, showing your payoff date, total months, total interest, and total amount paid.

Step 6: Review the Insight Box

Check the blue insight box just below your summary cards. It often tells you how much faster you could pay off your debt by adding just a small extra amount per month. Try adjusting your extra payment in $25 or $50 increments to see how much the timeline shifts.

Step 7: Export or Save Your Plan

Download your results as a PDF for your personal records, or copy the permalink to save your plan and revisit it later. The CSV export is useful for tracking your progress in a spreadsheet.

How to Read Your Results

Once you click Calculate, four key numbers show up across the top of the results panel:

Payoff Date

This is the real calendar month and year when your last debt hits zero. It’s not a vague estimate. It’s based on your actual numbers and updates every time you recalculate.

Total Months

This shows exactly how many monthly payments stand between you and being debt-free. A specific number is far more actionable than a general range. Seeing “27 months” feels very different from “a few years.”

Total Interest

This is the total interest you’ll pay across every debt over the full repayment period. This number can be a real wake-up call. If it feels uncomfortably high, experiment with adding more to your extra payment and see how fast it drops.

Total Paid

This is your combined principal plus all interest. It shows the true total cost of carrying credit card debt over time, which is always higher than the original balances alone.

The Insight Box

The blue box just below the summary cards suggests a small extra monthly payment. This payment could help you save significant time and interest. For example, it might say: “Add just $50 more per month to pay off your debt 4 months faster and save $318 in interest.” These suggestions are calculated fresh based on your actual inputs.

The Balance Chart

The line chart tracks your total balance dropping month by month from your start date to zero. This visual is one of the most motivating features in the tool. Printing it out and marking monthly progress is a simple but effective tracking method.

Amortization Table

Toggle this on to view the complete details for each month: date, total payment, principal, interest, and ending balance. This level of detail is especially useful if you’re working with a credit counselor. It helps you track whether your actual payments are matching the plan you’ve set.

Billing Cycle Planner

If you entered due dates for your cards, this section estimates how much interest you could save. It does this by comparing payments made right when your statement closes to those made at the due date. Even small timing adjustments can reduce your average daily balance and cut interest charges.

Tip: → If the snowball plan still feels out of reach, see what a credit card settlement letter template could offer instead.

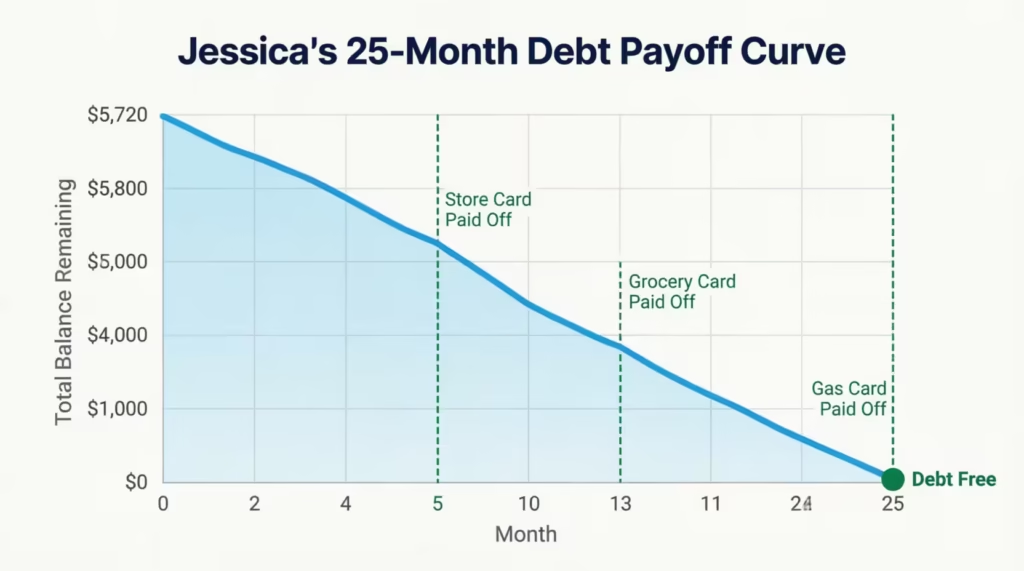

Real-World Example

To see how the numbers actually play out, consider Jessica, a school administrator in Phoenix, Arizona. She’s carrying three credit card balances she wants to cut:

| Card | Balance | APR | Minimum Payment |

|---|---|---|---|

| Store Card | $820 | 24.9% | $30 |

| Grocery Card | $1,600 | 19.99% | $25 |

| Gas Card | $3,300 | 22.5% | $70 |

Jessica enters all three debts, sets an extra monthly payment of $150, chooses the snowball method, and sets her start date to April 2026.

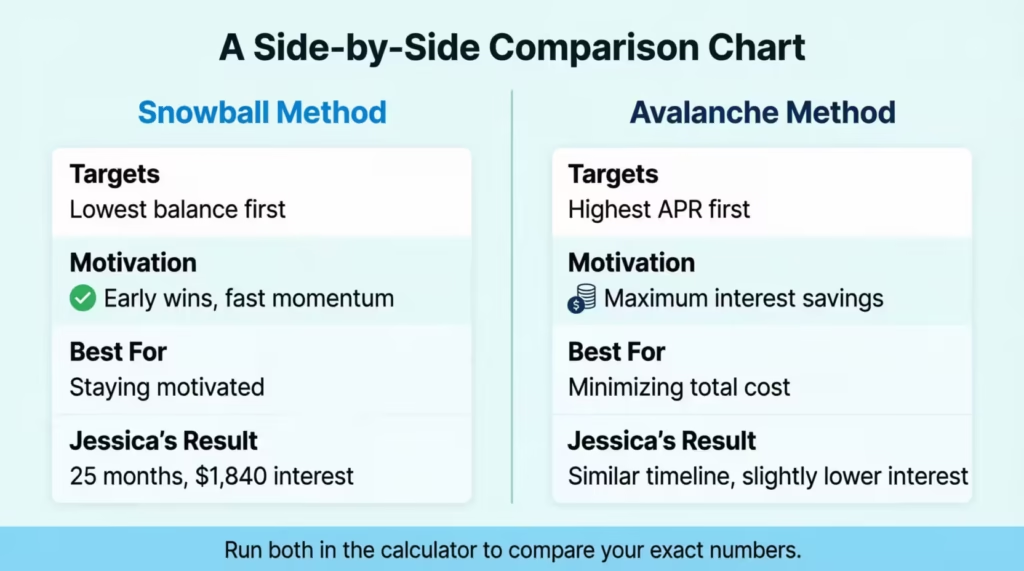

Snowball Method Results:

- Payoff date: approximately May 2028 (25 months)

- Total interest paid: approximately $1,840

- Total amount paid: approximately $7,560

The calculator targets the Store Card first because it has the lowest balance ($820). That clears in roughly 5 months. Jessica’s $30 minimum payment gets added to the extra pool and redirected to the Grocery Card. Once that’s gone, the full combined payment attacks the Gas Card until it reaches zero.

Switching to the Avalanche Method:

In Jessica’s case, the Store Card also happens to carry the highest APR at 24.9%. So the avalanche method targets it first, too. The results are similar, but if your highest-APR card has a big balance, switching to avalanche can save you more in interest.

What if Jessica adds $50 more per month?

Increasing her extra payment to $200 per month cuts her timeline by roughly 4 months and saves around $300 in interest. The insight box inside the calculator shows this change automatically after the initial calculation runs.

This example shows why running a few different scenarios matters. Adjusting the extra payment by even small amounts often produces surprisingly large savings.

Expert Tips and Insights

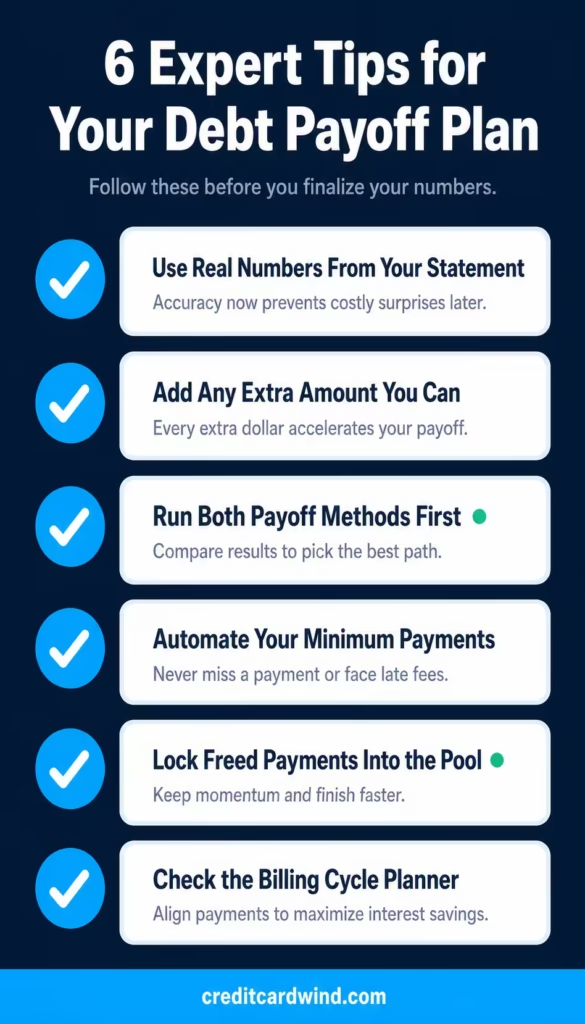

1. Always Use Real Numbers, Not Estimates

Rounded guesses lead to inaccurate timelines. Before you open the calculator, pull up your most recent credit card statements. Use the exact current balance, exact APR, and exact minimum payment for each account. Even a $200 balance difference can shift your payoff date by a month or more.

2. Add Any Extra Amount You Can

There’s no minimum requirement for the extra payment field. Even $20 or $30 above your combined minimums makes a real difference compounded over time. Cutting one subscription or skipping two meals out each month can give you a boost. This change can help speed up your plan.

3. Run Both Methods Before Committing

Don’t choose snowball or avalanche based on what you’ve read elsewhere. Run your actual numbers through both settings. Compare the payoff dates and total interest figures side by side. For some debt profiles, the total interest difference is small. In these cases, the benefit of early snowball payments is more motivating.

4. Automate at Least Your Minimums

Set up autopay for at least the minimum on every card before anything else. Missing a payment can trigger late fees and in some cases push your APR into penalty territory, which immediately throws off your plan. Automation removes that risk entirely.

5. Lock Freed Payments Into the Pool

When a debt gets paid off, keep that payment amount in your budget as a debt payment. Don’t allow it to blend into everyday spending. This discipline is what creates the compounding effect the snowball method is built on.

6. Check the Billing Cycle Planner

If you enter due dates for your cards, the planner shows estimated interest savings from paying at statement close instead of at the due date. For a high-balance, high-APR card, this can save $15 to $30 or more each billing cycle without changing the total payment amount.

Common Mistakes to Avoid

1. Entering the Minimum Required Instead of What You Actually Pay

There’s a difference between the lowest payment your card issuer requires and what you currently pay each month. If you’ve been paying $90 a month on a card with a $25 required minimum, enter $90. Using the lower number makes your results look worse than your actual situation.

2. Leaving Small Balances Out of the Plan

Marcus, a sales representative in Atlanta, forgot to include a $240 store card balance when he set up his payoff plan. That card had a 26.99% APR. Over 18 months of not targeting it, it grew by more than $110 in interest charges while he focused on his two larger cards. No balance is too small to include. Every account you leave out is an account that keeps compounding.

3. Setting the Extra Payment Too Low to Feel Real

If you add $1 or $2 as your extra monthly payment to check results, the plan will still work. But, it will take much longer than you’d like. Try entering $25, then $75, then $150, and compare the payoff dates. Seeing how dramatically the timeline shifts at different payment levels is often the push needed to commit to a higher number.

4. Not Recalculating When Circumstances Change

Your income, expenses, and balances change over time. If you get a tax refund, pay off a card ahead of schedule, or pick up extra income, recalculate. Running a fresh calculation keeps you on the most efficient path. Sticking with outdated numbers means leaving potential savings on the table.

5. Ignoring the Minimum Payment Warning

If the calculator warns you that a minimum payment is lower than the monthly interest charge on that debt, take it seriously. Your balance on that account will grow every month regardless of whether you pay the minimum. The tool gives this warning to highlight cases where the payment structure doesn’t lower the debt.

6. Switching Strategies Without a Reason

Diana, a marketing coordinator in Dallas, began with the snowball method. After three months, she switched to the avalanche approach after reading about it. Her mid-course switch required her to rebuild her plan from scratch. As a result, she spent two weeks feeling unsure about which card to focus on. Pick one method, run the numbers, and commit to it. Switch only if a meaningful change in your debt profile makes it financially worthwhile.

Frequently Asked Questions (FAQs)

What is the difference between the snowball method and the avalanche method?

The snowball method pays off your lowest balance first to create quick wins and build momentum. The avalanche method targets your highest APR first to reduce the total interest you pay over time.

Can I include more than three credit cards in this calculator?

Yes. Click “Add Another Debt” to include as many accounts as you need. There’s no cap on the number of debts you can enter.

Does the extra monthly payment apply every month or just the first month?

It applies every single month. The calculator automatically adds the freed-up least payments from paid-off debts to your monthly pool. This is how the snowball grows over time.

How accurate is the interest calculation?

The tool uses a simplified monthly interest model. Your actual credit card statement may differ slightly because issuers use the Average Daily Balance method. The results are close but should be treated as a strong estimate rather than an exact figure.

What happens if my minimum payment is smaller than my monthly interest charge?

Your balance will increase every month even while you make payments. The calculator warns you when it finds this condition. You can either proceed or change your inputs before running the full calculation.

Can I save my plan and come back to it later?

Yes. Click “Copy Link” to generate a URL that stores all your entered data. Bookmark it or save it anywhere to return to your exact plan without re-entering anything.

Which method saves more money overall?

The avalanche method usually lowers total interest costs. It does this by paying off high-APR balances in a short amount of time. The exact difference depends on your specific balances and rates. Running both scenarios in the calculator shows you the precise comparison for your situation.

Does paying off a credit card damage my credit score?

No. Paying off your credit card balance lowers your credit utilization ratio. This ratio is key to your credit score. It generally helps your score. Keeping the paid-off account open with a zero balance is usually better for your credit than closing it.

Bottom Line

Understanding your debt is the first real step to eliminating it. We’ve discussed the snowball method, the calculator’s formula, how to enter your debts correctly, and how to read the results it gives. A worked example and the most common planning mistakes round out the picture.

Run both the snowball and avalanche settings before committing to one, as this approach yields the best results. For most people, the motivation to clear individual debts one at a time is greater than the small potential difference in total interest.

If this guide helped you, please share it on social media with a friend or family member who’s trying to get their credit card balances under control.