RV Loan Calculator

Estimate your monthly payments and see how your credit score impacts your loan.

Monthly Payment

$0.00Total Interest Paid

$0.00Total Loan Cost

$0.00Credit Improvement Impact

By improving your score to the next credit band ( APR), you could save:

How to Use This Calculator

- Loan Amount: The total price of the RV you wish to purchase.

- Down Payment: The amount of cash you're paying upfront.

- Loan Term: The number of years you plan to take to repay the loan.

- Credit Score: Your current credit score, which determines your estimated APR.

- Sales Tax: The sales tax rate in your state, applied to the loan amount.

Disclaimer: This calculator is for estimation purposes only and does not constitute a loan offer. The actual APR, monthly payment, and terms you may be offered will vary based on your credit history, financial situation, and the lender's policies. Always consult with a financial advisor and lender for precise loan details.

Shopping for an RV can get confusing fast when the sticker price is only the start. Taxes, down payment, term length, and your score can change the deal more than many buyers expect, so an RV loan calculator with a credit score can save a lot of guesswork. Experian says the average U.S. FICO Score was 713 as of September 2025, which shows how much score ranges still matter.

A solid estimate combines price, tax, APR, and loan term into one clear monthly payment.

The guide below breaks down the math, shows how to use the tool, and shares simple ways to lower borrowing costs before you apply.

Tip: → A few extra points on your score can change your rate. Track yours with the credit score tracker template.

What Is an RV Loan Calculator?

An RV loan calculator is a planning tool that estimates how much a camper, travel trailer, fifth wheel, or motorhome loan may cost each month. It combines the purchase price, taxes, down payment, repayment term, and estimated APR. This helps clarify affordability. That matters because myFICO says FICO Scores are used by 90% of top lenders, while Experian reports that the average U.S. FICO Score was 713 as of September 2025.

This kind of tool is especially helpful because RV financing is not based on price alone. The Consumer Financial Protection Bureau explains that lenders look at the loan-to-value ratio, which compares the amount borrowed with the vehicle’s value. A bigger down payment lowers that ratio, which can reduce lender risk and sometimes lower the interest rate.

Lender guidance also shows why buyers need more than a simple payment guess. Good Sam Finance Center notes that APR is often shaped by credit score, loan amount, down payment, loan-to-value ratio, RV age, and loan term. In other words, two buyers looking at the same RV may end up with very different monthly payments.

How This Calculator Works

This calculator uses five main inputs:

- Loan amount

- Down payment

- Loan term in years

- Credit score

- Sales tax rate

The tool first adds sales tax to the RV price. Then it subtracts the down payment to find the financed amount. After that, it places the credit score into an estimated APR range and uses a standard fixed-rate loan formula to estimate the monthly payment.

This calculator also shows more than one result, which is helpful for real buyers. It displays:

- Monthly payment

- Total interest paid

- Total loan cost

- Credit improvement savings

- Principal vs. interest breakdown

- Loan balance over time

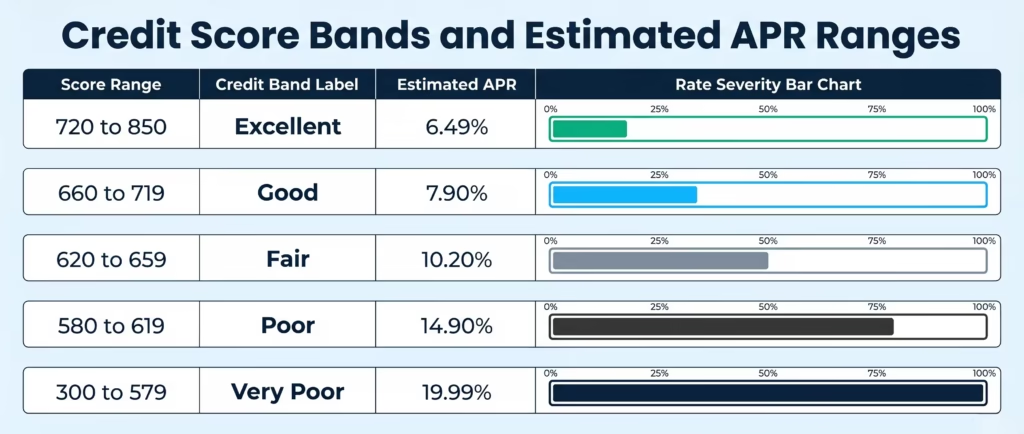

The built-in score bands used by this tool are:

| Credit Score Range | Credit Band | Estimated APR |

|---|---|---|

| 720 to 850 | Excellent | 6.49% |

| 660 to 719 | Good | 7.90% |

| 620 to 659 | Fair | 10.20% |

| 580 to 619 | Poor | 14.90% |

| 300 to 579 | Very Poor | 19.99% |

These are estimated bands for this calculator, not guaranteed lender offers.

💡 Pro Tip: If a score is close to the next band, run the numbers twice. A small score jump can change both the payment and the total interest more than most buyers expect.

The Formula Explained

The calculator follows a simple loan process.

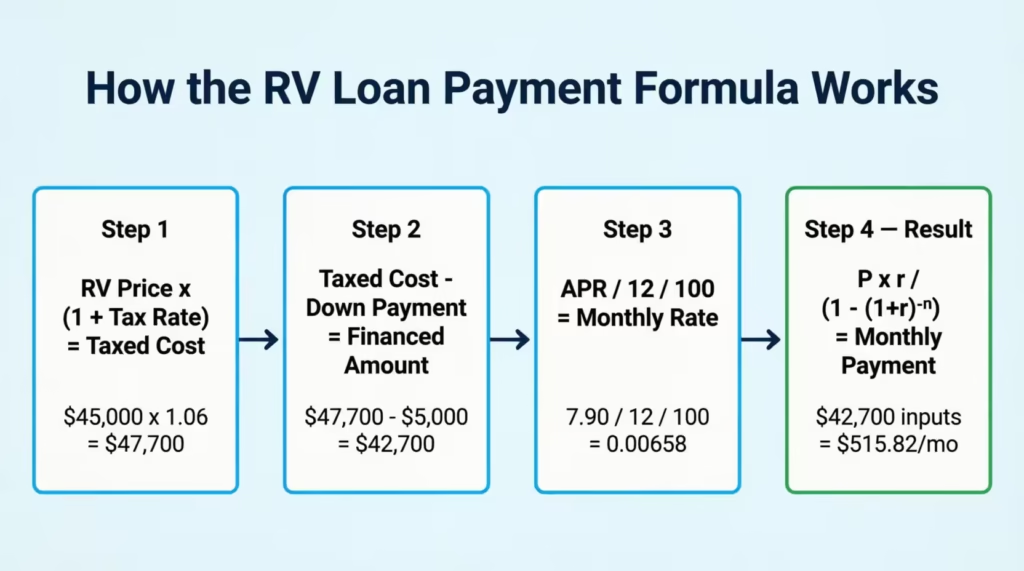

1. Find the taxed vehicle cost

Taxed cost = RV price × (1 + sales tax rate)

If an RV costs $45,000 and sales tax is 6%, the taxed cost is:

$45,000 × 1.06 = $47,700

2. Subtract the down payment

Financed amount = Taxed cost – down payment

If the down payment is $5,000:

$47,700 – $5,000 = $42,700

3. Convert APR to a monthly rate

Monthly rate = APR ÷ 12 ÷ 100

If APR is 7.90%:

7.90 ÷ 12 ÷ 100 = 0.0065833

4. Calculate the monthly payment

Monthly payment = P × r ÷ (1 – (1 + r)^-n)

Where:

- P = financed amount

- r = monthly interest rate

- n = total number of monthly payments

This is the standard formula used for fixed installment loans. It creates a steady monthly payment, but the split inside that payment changes over time. Early payments cover more interest. Later payments cover more principal.

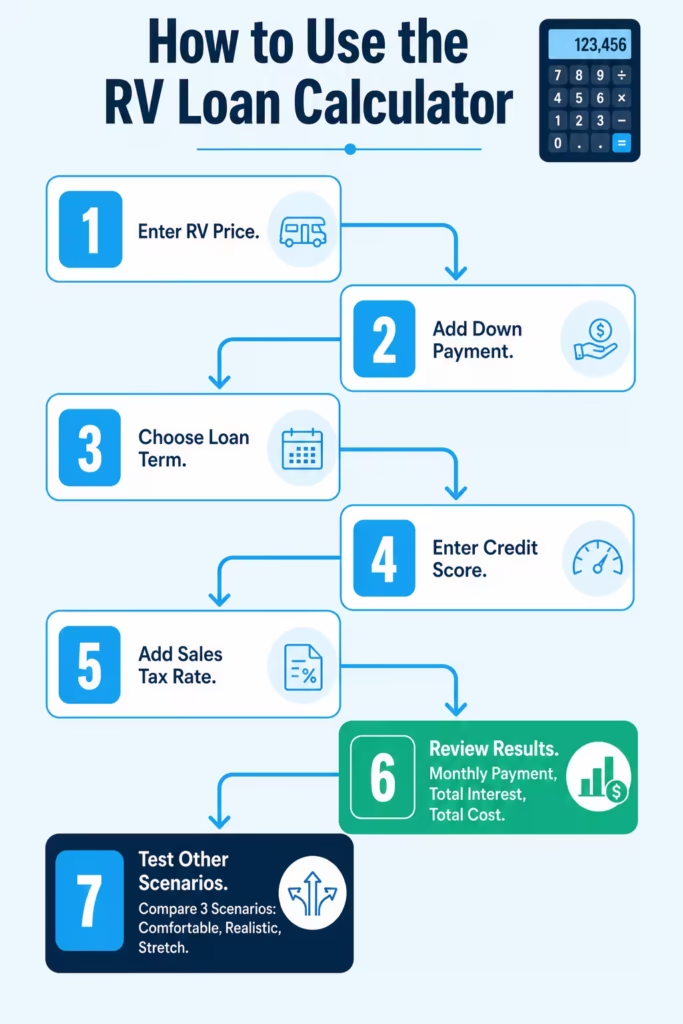

How to Use This Calculator (Step by Step)

Follow these steps to get a useful estimate:

- Enter the RV price. Type in the full purchase price of the RV.

- Add the down payment. Enter the amount planned for the upfront payment.

- Choose the loan term. Pick the number of years for repayment.

- Enter the credit score. Use the most recent score available.

- Add the sales tax rate. Use the local or state tax rate tied to the purchase.

- Review the results. Check the monthly payment, total interest, and total cost.

- Test other scenarios. Try a bigger down payment, shorter term, or better score to compare outcomes.

A smart way to use the tool is to build three loan plans:

- a comfortable payment option

- a realistic target option

- a stretch budget option

That gives a clearer range before talking to a lender or dealer.

How to Read Your Results

The monthly payment is the number most buyers notice first. It shows what the fixed payment may look like each month if the estimate is close to the final loan offer.

The total interest paid shows how much borrowing costs over time. This number is useful because a payment can look manageable while the loan still becomes expensive over the long term.

The total loan cost combines principal and interest. It answers a simple but important question: How much money will leave the budget by the time the loan is done?

The credit improvement section is one of the most useful parts of the tool. It compares the current estimate with the next better score band. That makes it easier to see whether waiting, paying down balances, or fixing report errors could save enough to be worth the delay.

The charts also help. One chart shows how much of the loan cost goes to principal and interest. The other shows how the balance falls over time.

⚠️ Mistake to Avoid: Do not judge the loan by the monthly payment alone. A lower payment can still lead to much more interest if the term stretches too far.

Real-World Example

Michael is a warehouse supervisor in Texas, shopping for a used travel trailer. He wants a realistic payment before he visits a dealer.

Here are the numbers he enters:

- RV price: $45,000

- Sales tax: 6%

- Down payment: $5,000

- Loan term: 10 years

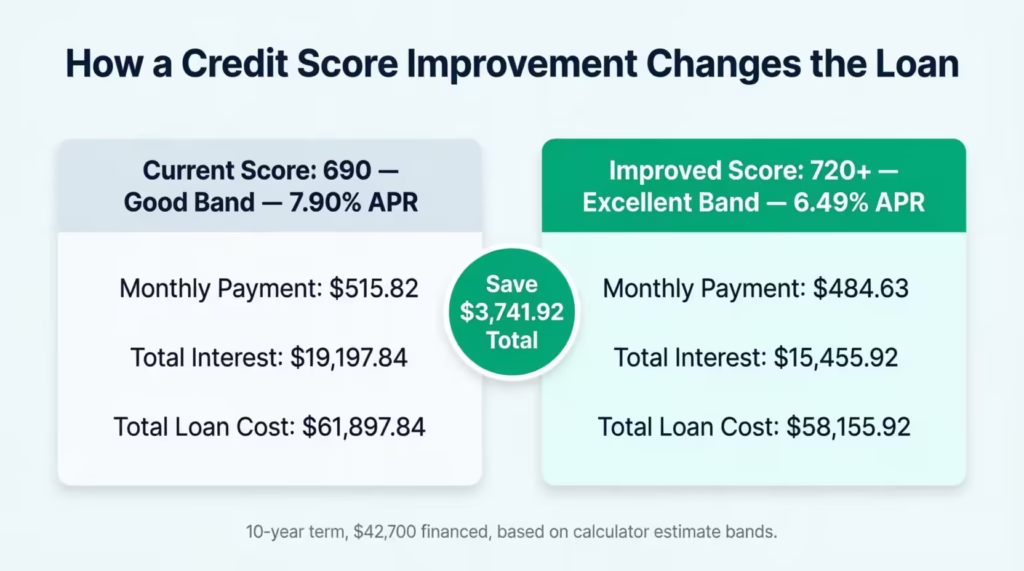

- Credit score: 690

- Estimated APR from this tool: 7.90%

Step 1: Add sales tax

$45,000 × 1.06 = $47,700

Step 2: Subtract the down payment

$47,700 – $5,000 = $42,700

Step 3: Estimate the payment

With a financed amount of $42,700, a 7.90% APR, and a 10-year term, the estimated monthly payment is:

$515.82 per month

Step 4: Review the full cost

- Monthly payment: $515.82

- Total interest paid: $19,197.84

- Total loan cost: $61,897.84

Now look at what happens if Michael raises his score into the next band and qualifies for 6.49% APR instead.

- New monthly payment: $484.63

- Monthly savings: $31.18

- Total savings over the loan: $3,741.92

That is a good example of why score-based pricing matters. The monthly gap may look modest, but the long-term savings are still meaningful.

Expert Tips and Insights

A larger down payment can do more than lower the amount borrowed. The Consumer Financial Protection Bureau explains that a bigger down payment lowers the loan-to-value ratio, reduces interest paid over time, and may improve the rate a lender offers.

Loan term matters more than many buyers think. Alliant Credit Union says RV loan terms often range from 10 to 20 years, and Good Sam Finance Center notes that shorter terms can help borrowers qualify for better APRs. That means the lowest monthly payment is not always the best deal. Sometimes it is just a slower and more costly way to repay the same RV.

Rate shopping is usually worth it when done in a short window. The CFPB says shopping for the best auto loan deal generally has little to no impact on credit scores when similar inquiries happen within about 14 to 45 days. That makes preapproval a smart move for buyers who want to compare offers without dragging the process out.

Preapproval can also improve negotiating power. Alliant Credit Union recommends getting preapproved before heading to the dealer because it helps buyers compare terms and negotiate with a stronger benchmark in hand.

📌 Did You Know: The RV Industry Association expects 2026 RV wholesale shipments to range from 328,800 to 367,000 units. That steady market activity is one more reason to compare financing options early.

Common Mistakes to Avoid

Forgetting sales tax

A buyer may budget for the sticker price and forget the tax. That can throw off the financed amount by thousands of dollars.

Using the wrong credit score

A free score app can be helpful, but a lender may pull a different bureau or scoring model. The estimate is still useful, but the final offer may vary a little.

Stretching the term too far

A 15-year or 20-year loan can make the monthly payment look easier. It can also increase total interest by a lot.

Putting too little down

A low down payment keeps more cash available now, but it can raise the loan-to-value ratio and total borrowing cost.

Treating the estimate like a final approval

This tool is for planning. Final approval still depends on income, debt, RV age, credit file details, and lender rules.

⚠️ Mistake to Avoid: Comparing only one lender can cost more than expected. A lower APR can save a significant amount over a long RV loan.

Frequently Asked Questions (FAQs)

What credit score do you need for an RV loan?

Many RV lenders prefer scores around 700 or higher, but some may approve borrowers near 600. A stronger score usually improves the APR, the loan amount, and the available term options.

Can you get an RV loan with a 600 credit score?

Yes, some lenders may approve an RV loan with a 600 score, especially with a larger down payment or smaller loan amount. The trade-off is often a higher interest rate and stricter loan terms.

How long are RV loan terms?

RV loan terms often run from 10 to 20 years, depending on the lender, the loan amount, and the RV itself. Longer terms lower the monthly payment but usually raise the total interest paid.

How much down payment do you need for an RV?

Many buyers aim for 10% to 20%, though lender rules can vary. A larger down payment usually lowers the financed amount, improves the loan-to-value ratio, and may help with approval.

Does checking RV loan rates hurt your credit score?

Shopping for rates usually has little impact when similar loan inquiries happen within a short period. Keeping rate shopping within about two to six weeks is often the safest approach.

Can you finance a used RV?

Yes, many lenders finance used RVs, but the rate and term may depend on age, mileage, condition, and value. Older units often have more limits than newer ones.

Is RV loan interest tax deductible?

It can be in some cases if the RV qualifies as a main or second home and the loan meets IRS rules. The answer depends on how the RV is used and whether the loan is secured properly.

What lowers an RV payment the fastest?

The quickest ways are a bigger down payment, a lower APR, or a longer term. The best long-term savings usually come from a lower rate or more money down, not just stretching the loan out.

Bottom Line

Using this tool as a planning guide before meeting with a lender or dealer is the best approach. It helps break down the full cost of the RV, shows how score-based APR changes the payment, and makes it easier to test smarter options like a larger down payment or shorter term.

If I had to make one recommendation, I’d compare a few loan scenarios before applying so the numbers are clear ahead of time. If this guide helped, please share it on social media with anyone who may need it.