New Car Loan Calculator With Credit Score

Estimate your monthly payments based on loan amount, term, and credit score.

Loan Details

Your Estimated Results

Monthly Payment

$0.00

Adjusted APR

0.0%

Total Interest Paid

$0.00

Total Loan Cost

$0.00

Loan Breakdown

Loan Amortization Schedule

Share & Learn More

How to Use

- 1 Enter the car price, loan term, and any down payment or trade-in value.

- 2 Select your credit score or input a specific APR to see your adjusted monthly payment.

- 3 Download a PDF report of your results or share them using the unique link.

Disclaimer

This calculator is for informational purposes only. The results are estimates based on the information you provide and may not be accurate or applicable to your specific financial situation. The information provided does not constitute financial, legal or tax advice. We do not guarantee the accuracy of the calculations or the applicability of any information. Always consult a qualified financial professional for advice specific to your personal circumstances. Credit card terms, conditions, rates and offers are subject to change by the issuing bank at any time. We are not responsible for any actions or decisions taken based on the information provided by this tool.

Most car buyers don’t know their real monthly payment until they’re sitting at the dealership. Without knowing your numbers upfront, you can end up agreeing to loan terms you simply can’t afford. Experian’s State of the Auto Finance Market puts the average new vehicle loan at $40,927 in Q3 2024. A new car loan calculator with a credit score puts that clarity in your hands before any negotiation starts.

Entering your credit score gives you an adjusted APR and an accurate monthly payment estimate in seconds.

Keep reading for the full formula, a step-by-step guide, a real-world comparison, and expert tips to lower your total loan cost.

Tip: → Planning to improve your score before buying? Track your progress with the credit score tracker template.

What Is a New Car Loan Calculator With Credit Score?

A new car loan calculator with a credit score is an online tool that estimates your monthly auto loan payment based on several key inputs. Those inputs include vehicle price, loan term, down payment, trade-in value, sales tax, credit score tier, and APR.

Most basic loan calculators only ask for the loan amount and interest rate. This one goes further. It adjusts your APR based on your credit score tier. That gives you a much more realistic payment estimate than a generic calculator can provide.

Here’s the core idea behind the credit score adjustment. Lenders use your credit score to decide how much risk you represent as a borrower. A higher score almost always earns a lower interest rate. A lower rate means less money paid in interest over the life of the loan. That difference can easily add up to hundreds or even thousands of dollars on a typical auto loan.

Think about it this way. Two people buy the same car for the same price. One has an excellent credit score. The other has fair credit. Even with identical loan amounts and terms, they’ll likely end up with meaningfully different monthly payments and very different total costs.

This calculator shows you that gap clearly, so you can plan.

How This Calculator Works

Behind the simple input fields, this calculator runs a complete loan analysis in real time. Here’s what it does at each step.

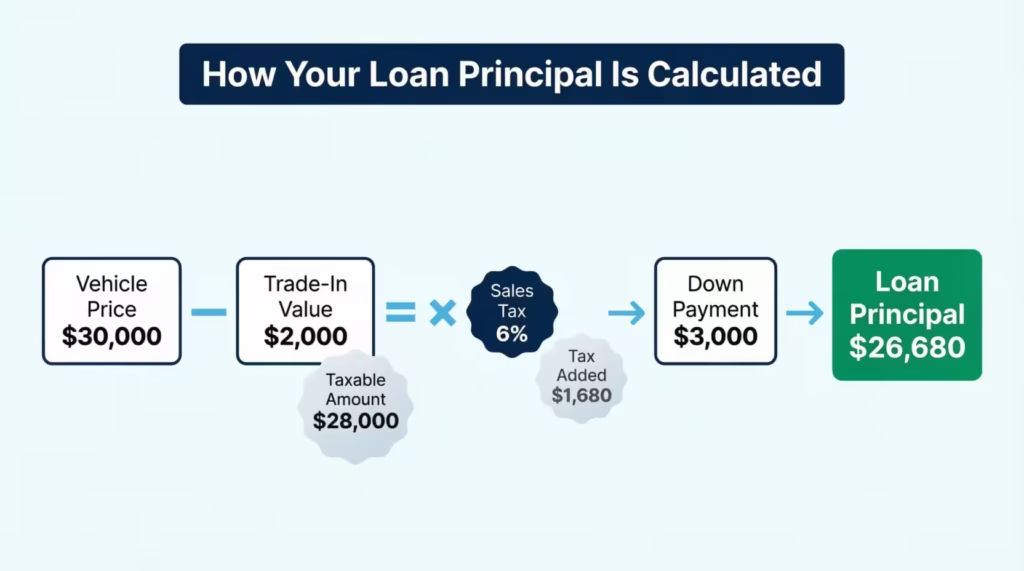

Step 1: Taxable Amount

The calculator subtracts your trade-in value from the vehicle price. Sales tax is applied to that difference, not to the full sticker price. This matches how most U.S. states calculate the taxable amount on a vehicle purchase.

Step 2: Principal Calculation

The calculator adds the tax amount to the taxable vehicle total. Then it subtracts your down payment. The result is your loan principal. This is the actual amount you’ll be borrowing and paying interest on.

Step 3: APR Adjustment by Credit Score

Your base APR is adjusted up or down based on your selected credit tier:

| Credit Tier | Score Range | APR Adjustment |

| Excellent | 720 and above | Base APR minus 0.50% |

| Good | 660 to 719 | Base APR plus 0.50% |

| Fair | 600 to 659 | Base APR plus 1.50% |

| Poor | 500 to 599 | Base APR plus 3.00% |

These adjustments reflect real lending patterns. As Experian’s State of the Auto Finance Market shows, deep subprime borrowers pay significantly higher rates than super-prime borrowers, often by several percentage points.

Step 4: Monthly Payment Calculation

The calculator applies the standard amortization formula using your principal, adjusted APR, and loan term in months.

Step 5: Amortization Schedule With Extra Payments

If you add an extra monthly payment, the calculator rebuilds the schedule month by month. It applies the extra amount directly to your principal each month. It then shows how many months sooner the loan is paid off and how much total interest you save.

The Formula Explained

The calculator uses the standard fixed-rate amortization formula used by banks and lenders across the country. Here it is:

M = P × [r(1 + r)^n] / [(1 + r)^n – 1]

Each variable has a specific meaning:

- M = Monthly payment (what you pay each month)

- P = Loan principal (amount borrowed after down payment, trade-in, and tax)

- r = Monthly interest rate (your annual APR divided by 12, then divided by 100)

- n = Total number of monthly payments (loan term in months)

Let’s break that down in plain English. You multiply your principal by a fraction. The top of the fraction grows with your interest rate compounding over time. The bottom accounts for that same growth minus one. Together, they produce a fixed monthly payment that pays off the loan completely by the last month.

What about 0% APR?

If your APR is zero, the formula simplifies completely. Your monthly payment is just your loan principal divided by the number of months. No interest is charged at all.

Principal Calculation Breakdown

Before the formula runs, the calculator determines your true principal:

- Taxable Amount = Vehicle Price minus Trade-in Value

- Tax Amount = Taxable Amount multiplied by your Sales Tax Rate

- Principal = Taxable Amount plus Tax Amount minus Down Payment

📌 Did You Know: A one-percentage-point difference in APR on a $35,000 car loan over 60 months adds more than $900 in total interest. That’s why your credit score tier has such a direct impact on the true cost of your car.

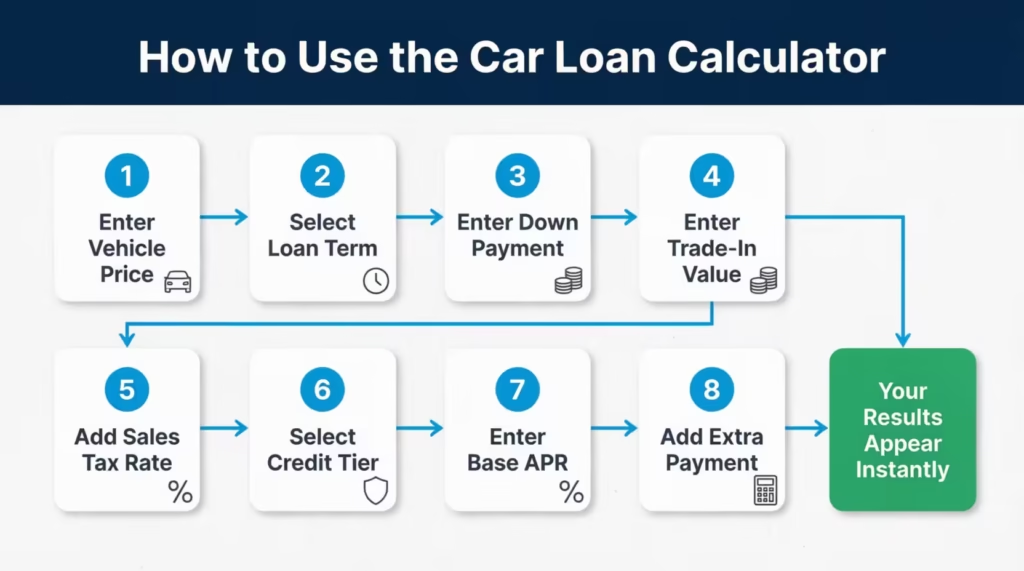

How to Use This Calculator (Step by Step)

Follow these steps to get your personalized auto loan estimate.

Step 1: Enter the Vehicle Price

Type the full price of the car in the “Vehicle Price” field. You can enter the full number (like 35000) or use shorthand notation (like 35k). The valid range is $500 to $200,000.

Step 2: Choose Your Loan Term

Select the number of months you want to finance the vehicle. Options range from 12 to 84 months. A shorter term means a higher monthly payment but less total interest. A longer term means a lower monthly payment but more interest paid overall.

Step 3: Enter Your Down Payment

Type how much cash you plan to put down at the time of purchase. A larger down payment reduces your loan principal directly. It also lowers your total interest cost and monthly payment.

Step 4: Add Your Trade-in Value

If you’re trading in a vehicle, enter its current market value. The trade-in reduces the taxable purchase price before sales tax is applied. This is one of the most tax-efficient ways to reduce your total car purchase cost.

Step 5: Enter Your Sales Tax Rate

Type your state or local sales tax rate as a percentage. The default is 7%. Check your state’s department of revenue website for the exact rate in your area.

Step 6: Select Your Credit Score Tier

Choose the credit range that best matches your current score. This adjusts your APR to reflect what lenders are likely to offer you. If you’re unsure of your exact score, check a free credit monitoring service before you apply.

Step 7: Enter Your Base APR

Type the interest rate you expect to receive. The default is 6.0%. You can check average auto loan rates by credit tier through sources like Experian or your bank’s website.

Step 8: Add an Optional Extra Monthly Payment

If you plan to pay a little extra each month, enter that amount here. Even a small extra payment can shorten your loan term significantly and cut your total interest cost. The calculator will show you the exact savings.

Step 9: Review, Download, and Share

Click the “Download PDF” button to save your full results. Use the social sharing icons to send your numbers to a financial advisor or a trusted friend.

💡 Pro Tip: Run the calculator twice. First, use your current credit tier. Then run it again using the next tier up. The dollar difference you see is exactly what improving your credit score before applying could save you.

How to Read Your Results

The calculator displays four key result cards and two charts. Here’s what each one tells you.

Monthly Payment

This is the fixed amount you’ll owe every month for the full loan term. It’s calculated using your principal, your adjusted APR, and your loan term. This number does not include auto insurance, registration fees, or maintenance costs.

Adjusted APR

This is your effective interest rate after the credit score tier adjustment is applied. For example, if your base APR is 6.0% and your credit score falls in the “Fair” range, your adjusted APR becomes 7.5%. This is the rate used for all calculations.

Total Interest Paid

This is the total amount of interest you’ll pay over the full life of the loan. It’s the gap between your original principal and your total repayment amount. This number reveals the true cost of financing your vehicle.

Total Loan Cost

This is your loan principal plus all interest paid. It represents the complete amount you’ll repay to the lender from your first payment to your last.

The Doughnut Chart

This chart shows how your total loan cost splits between principal and interest. A larger interest slice signals a high-cost loan. You want the interest slice to be as small as possible.

The Amortization Chart

This line chart shows your remaining loan balance decreasing month by month. In the early months, most of your payment goes toward interest. As time passes, more of each payment goes toward the principal. This pattern is called front-loaded amortization, and it’s standard for all fixed-rate installment loans.

Real-World Example

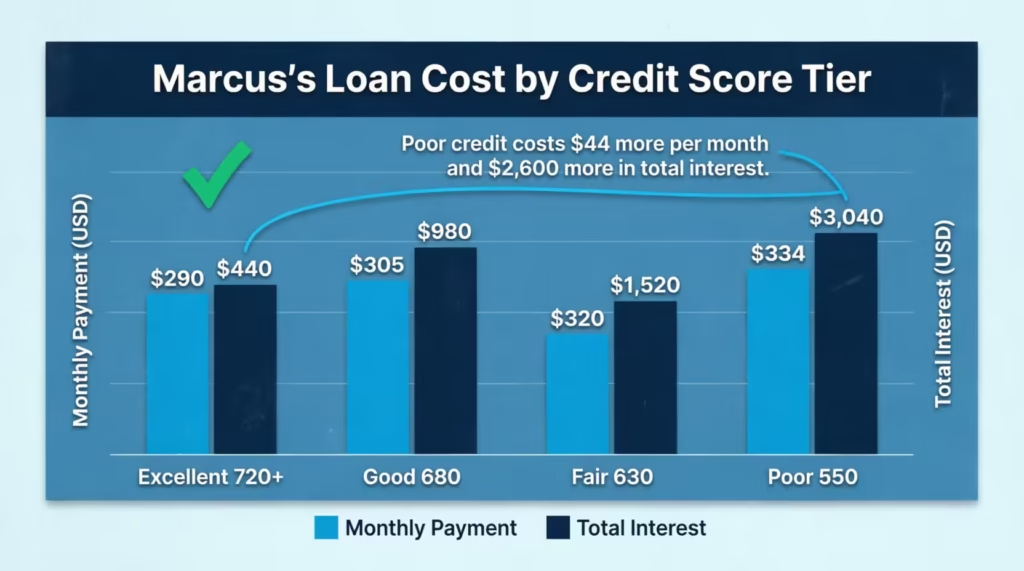

Here’s a concrete side-by-side comparison to show how a credit score changes the total cost of the same car.

Scenario: Michael vs. Sarah

Both Michael and Sarah are buying a $32,000 new sedan in Georgia. Both are putting $3,000 down and trading in a vehicle worth $4,000. Georgia’s sales tax rate is 7%. Both plan to finance for 60 months at a base APR of 6.0%.

The only difference: Michael has a credit score of 685 (Good tier). Sarah has a credit score of 625 (Fair tier).

Shared Inputs for Both:

- Taxable Amount: $32,000 minus $4,000 trade-in = $28,000

- Tax: $28,000 times 7% = $1,960

- Principal: $28,000 plus $1,960 minus $3,000 down payment = $26,960

Michael’s Results (Good Credit, Adjusted APR: 6.5%)

Using the formula M = P × [r(1 + r)^n] / [(1 + r)^n – 1]:

- Monthly Rate: 6.5% / 12 = 0.5417%

- Monthly Payment: approximately $527.75

- Total Interest Paid: approximately $4,705

- Total Loan Cost: approximately $31,665

Sarah’s Results (Fair Credit, Adjusted APR: 7.5%)

- Monthly Rate: 7.5% / 12 = 0.625%

- Monthly Payment: approximately $541.00

- Total Interest Paid: approximately $5,460

- Total Loan Cost: approximately $32,420

The Difference

Sarah pays roughly $13 more per month than Michael. That sounds small. But over 60 months, she pays about $755 more in total interest for the same car with the same terms. That’s money she could have kept if she had spent a few months improving her credit score before applying.

⚠️ Mistake to Avoid: Never assume the interest rate a dealer quotes you is the best available rate. Dealers sometimes mark up the lender’s approved rate to earn extra profit. Always get pre-approved through a bank or credit union first. That gives you a benchmark rate to compare against any dealership offer.

Expert Tips and Insights

These practical steps can meaningfully lower your total loan cost.

1. Improve Your Credit Score Before Applying

Moving from Fair to Good credit can cut your APR by 1% or more. On a $27,000 loan over 60 months, that saves roughly $750 in total interest. Pay down credit card balances to below 30% of their limits. Dispute any errors on your credit report before applying. Both actions can move your score up in just one or two billing cycles.

2. Aim for at Least 10% to 20% Down

A solid down payment reduces your principal right away. It also prevents you from going “underwater” on the loan, meaning you owe more than the vehicle is worth. Many new cars depreciate by 10% to 15% in their first year, so starting with strong equity matters.

3. Choose the Shortest Term You Can Comfortably Afford

A 48-month loan costs far less in total interest than a 72-month or 84-month loan on the same vehicle. Yes, your monthly payment will be higher. But you’ll own the car free and clear much sooner, and you’ll pay hundreds less in interest. Use the calculator to compare terms directly.

4. Use Your Trade-in Value Strategically

The calculator correctly reduces the taxable purchase price by your trade-in amount before tax is calculated. In most U.S. states, this saves you real sales tax dollars. Always get an independent appraisal of your trade-in vehicle before the dealer quotes you a value. Services like KBB (Kelley Blue Book) and Edmunds give you a free estimate in minutes.

5. Add Even a Small Extra Monthly Payment

Try entering $50 or $100 in the “Extra Monthly Payment” field. You’ll likely see several months shaved off your loan term and a noticeable drop in total interest. That modest extra amount can save hundreds over the course of a 60-month loan.

6. Shop Multiple Lenders Before You Commit

The Consumer Financial Protection Bureau recommends comparing loan offers from at least two or three lenders before signing. Banks, credit unions, and online lenders all compete for your business. Credit unions in particular are worth checking. Under National Credit Union Administration rules, federal credit unions are capped at 18% APR, and many offer below-market rates to members with average credit.

💡 Pro Tip: Get pre-approved for a loan before visiting any dealership. Your pre-approval letter locks in a benchmark rate. Any financing the dealer offers must beat that rate to earn your business. This single step puts you in control of the conversation.

Common Mistakes to Avoid

These are the most common errors buyers make when estimating or applying for an auto loan.

Mistake 1: Focusing Only on the Monthly Payment

A lower monthly payment isn’t automatically a better deal. An 84-month loan at 7% APR on a $35,000 car could cost over $7,200 in total interest. A 48-month loan on the same car at the same rate costs roughly $3,900. Always check the “Total Interest Paid” figure, not just the monthly number.

Mistake 2: Ignoring Sales Tax in Your Estimate

Many buyers estimate their loan based on the sticker price alone. Sales tax can add a meaningful amount to your financed total. At 7% tax, a $32,000 car adds $1,960 to your financed amount if you roll the tax into the loan. That extra principal earns interest for the entire loan term.

Mistake 3: Skipping the Trade-in Tax Benefit

Your trade-in does more than reduce your loan balance. In most states, it reduces the taxable portion of your purchase price. That cuts the amount of sales tax you owe. Most online estimators don’t account for this correctly. This calculator does.

Mistake 4: Using a Stale Credit Score

Credit scores can shift by 20 to 30 points in a single month. Applying for a loan with an outdated score estimate can leave you unprepared for the rate you actually receive. Pull your most recent report at AnnualCreditReport.com before you run any loan estimates or visit a lender.

Mistake 5: Never Testing the Extra Payment Field

Many borrowers don’t realize how much even a small extra monthly payment can save. An extra $75 per month on a 60-month, $27,000 loan at 6.5% APR can pay the loan off roughly 8 months early and save over $450 in interest. Try it in the calculator. The results often surprise people.

Mistake 6: Accepting the First Financing Offer

According to a Federal Reserve Bank of New York consumer credit report, most auto loan borrowers accept the first offer they receive. That can be costly. A rate that is 0.5% higher than what a competitor would offer could cost you several hundred dollars over a standard loan term. Always compare.

Frequently Asked Questions (FAQs)

How does my credit score affect my car loan interest rate?

Your credit score signals your borrowing risk to lenders. A higher score typically earns a lower APR. Borrowers in the “Excellent” tier (720 and above) can qualify for rates 2% to 4% lower than those in the “Fair” tier (600 to 659), which adds up to significant savings over a 60-month loan.

What credit score do I need to get a good auto loan rate?

Most lenders consider scores of 660 or higher as “good” for auto financing. Scores of 720 and above typically qualify for the most competitive rates. Scores below 600 are considered subprime and will result in higher APRs and sometimes stricter lending requirements.

How is the loan principal different from the car’s sticker price?

The principal is the actual amount you borrow. It’s calculated by subtracting your down payment and trade-in value from the vehicle price, then adding sales tax on the taxable portion. It’s almost always a different number from what’s on the window sticker.

Does a longer loan term always mean a lower monthly payment?

Yes, but longer terms come at a cost. A 72-month loan at 7% APR generates significantly more total interest than a 48-month loan at the same rate, even though the monthly payment is lower. The monthly savings on longer terms often come with hundreds or thousands of dollars in extra interest cost.

What is APR, and how is it different from the interest rate?

APR stands for Annual Percentage Rate. For most auto loans, APR and the stated interest rate are very close or identical. APR becomes more relevant when a lender charges origination fees, which can raise the effective cost above the stated rate. This calculator uses APR directly for all payment calculations.

How does my trade-in reduce my total loan cost?

Your trade-in value is subtracted from the vehicle price before sales tax is calculated. This lowers both your taxable amount and your loan principal. In most U.S. states, this is one of the most tax-efficient ways to reduce the overall cost of buying a new vehicle.

Will making extra monthly payments hurt my credit score?

No. Extra payments reduce your principal faster and shorten your loan term. They do not hurt your credit score. Over time, paying down installment debt can actually help your score by lowering your total outstanding debt balance.

How accurate is the APR estimate this calculator produces?

The APR adjustment reflects realistic lender behavior across credit tiers. Your actual rate will depend on your specific credit profile, your lender, current market conditions, and your income. Use this calculator as a planning tool, then confirm your actual rate with a bank, credit union, or other lender.

What loan term do financial experts recommend for a new car?

Most financial advisors recommend 48 to 60 months for new vehicle financing. This balances a manageable monthly payment with reasonable total interest costs. Loan terms of 72 months or longer are generally discouraged because you pay significant interest on an asset that is depreciating throughout the loan term.

Bottom Line

Buying a car without knowing your numbers is one of the most common and costly mistakes people make in personal finance. In this guide, we walked through how the calculator handles your principal, how your credit tier adjusts your APR, and what each result actually means for your budget.

We also compared two real borrowers side by side and covered six expert strategies to lower your total loan cost.

I always recommend running the numbers at two different credit tiers before you apply. Seeing that dollar difference clearly is one of the most powerful motivators to improve your score first. If this guide helped you, please share it with a friend or family member who’s planning to buy a car soon.