Credit Card Limit Calculator

Get a clear, defensible estimate of your potential credit card limit.

Your results will appear here

Fill in the form to get your estimated credit limit.

Estimated Credit Limit

$0

$0 - $0

Debt-to-Income (DTI)

0%

Projected Utilization

0%

How we estimated this:

Save or Share Your Estimate

How to Use This Calculator

- 1 Enter your annual income, monthly housing costs, and other monthly debt payments.

- 2 Select your credit score range. For a more accurate estimate, add your current card balances and limits.

- 3 Your results will update automatically as you type.

- 4 Review the estimated credit limit, confidence level, and key financial metrics like your DTI.

- 5 Use the "Download PDF" or "Copy Link" buttons to save or share your personalized estimate.

Disclaimer: This calculator is for informational purposes only. The results are estimates based on the information you provide and may not be accurate or applicable to your specific financial situation. The information provided does not constitute financial, legal or tax advice. We do not guarantee the accuracy of the calculations or the applicability of any information. Always consult a qualified financial professional for advice specific to your personal circumstances. Credit card terms, conditions, rates and offers are subject to change by the issuing bank at any time. We are not responsible for any actions or decisions taken based on the information provided by this tool.

Have you ever applied for a credit card without knowing what limit you’d actually get? It feels like a gamble, and a hard inquiry hits your score, whether the outcome is good or bad.

According to Experian, the average U.S. consumer held a total credit card limit of $33,980 in 2024, yet most applicants apply completely blind. Using a credit card limit calculator removes that uncertainty before you ever submit an application.

You can estimate your potential credit limit in minutes by entering your income, monthly debts, and credit score into a free tool.

This guide walks you through the exact formula. It offers a step-by-step tutorial, a real-world example, and proven expert tips. With these tools, you’ll walk into your next application with full confidence.

Tip: → See how this number affects your utilization with the credit card utilization template.

What Is a Credit Card Limit?

A credit card limit is the maximum dollar amount a card issuer allows you to borrow on a single account at any given time. Once you hit that ceiling, new charges are declined until you pay down your balance.

Your limit isn’t a random number. Experian data shows the average total credit card limit for U.S. consumers reached $33,980 in Q2 2024, up from $31,165 just two years prior. But averages don’t tell your story. Your personal limit relies on the specifics of your unique financial profile.

Here are the core factors lenders use to set a credit limit:

- Income: Your annual earnings signal how much new debt you can realistically manage.

- Debt-to-income ratio (DTI): This compares your monthly obligations to your gross monthly income.

- Credit score: A higher score signals lower risk, which typically leads to higher limits.

- Credit utilization: High balances on existing cards suggest you may already be financially stretched.

- Employment status: Full-time employees generally receive higher limits than part-time or unemployed applicants.

- Credit history: A long record of on-time payments strengthens every credit application.

Understanding these factors helps you predict where you’re likely to land well before you submit anything.

📌 Did You Know: Even two people with identical incomes and credit scores can receive very different limits from the same bank. Card issuers consider their risk models and customer profiles. This means your history with a lender can change the numbers a lot.

How This Calculator Works

This tool uses an affordability-based model to estimate your likely credit limit. It doesn’t pull your credit report. It doesn’t file any application. It simply takes the key inputs that lenders care about most and runs them through a transparent, defensible formula.

Here’s what the tool uses:

Required inputs:

- Annual income

- Monthly housing cost (rent or mortgage)

- Existing monthly debt payments (car loans, student loans, personal loans, etc.)

- Credit score category: Poor, Fair, Good, Very Good, or Excellent

Optional inputs:

- Current total card balances

- Current total credit limits across all cards

- Employment status

The more complete your inputs, the more reliable your result. Skipping the optional fields drops your confidence level from “High” to “Medium,” which simply means the range is wider.

💡 Pro Tip: Take 30 extra seconds to add your current card balances and total limits. It upgrades your confidence level to High and gives you a much tighter, more actionable estimate range.

The Formula Explained

The calculation runs through several clear steps. Here’s exactly how each one works.

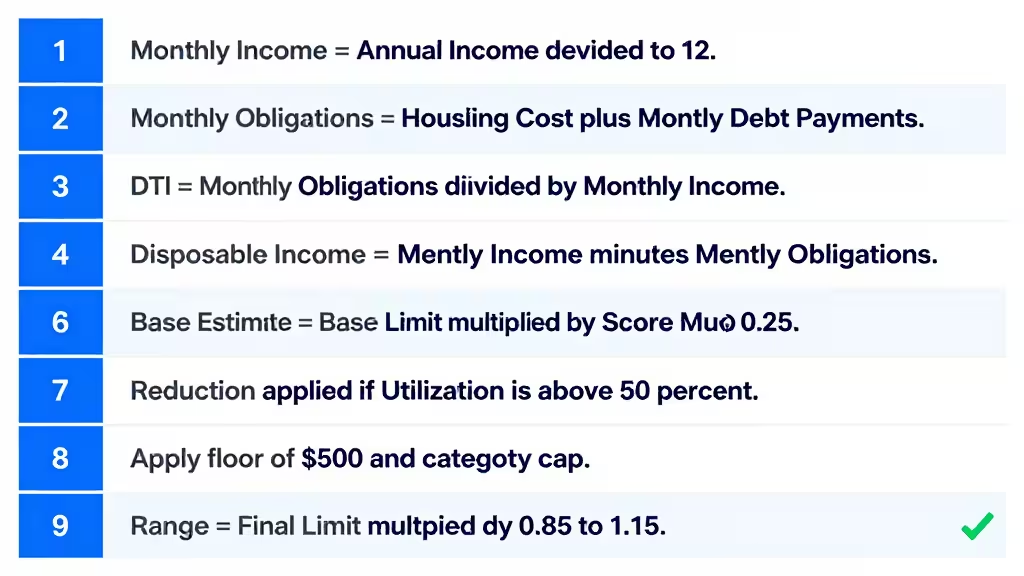

Step 1: Convert annual income to monthly income

Monthly Income = Annual Income / 12

Step 2: Calculate total monthly obligations

Monthly Obligations = Monthly Housing Cost + Existing Monthly Debt Payments

Step 3: Calculate your DTI ratio

DTI = Monthly Obligations / Monthly Income

As the Consumer Financial Protection Bureau explains, DTI measures the share of your gross monthly income that goes toward paying existing debts. A DTI at or below 36% is typically seen as manageable. A DTI above 50% signals serious financial strain to most lenders.

Step 4: Find your disposable income

Disposable Income = Monthly Income – Monthly Obligations

This is the heart of the calculation. Disposable income represents what’s actually available after your fixed commitments. It’s the most honest measure of your capacity to handle new credit.

Step 5: Build the base credit limit

Base Limit = Disposable Income x 0.25

The tool uses 25% of your disposable monthly income as the starting point. This view is conservative, yet realistic. It shows how much of your remaining income a lender thinks you can borrow.

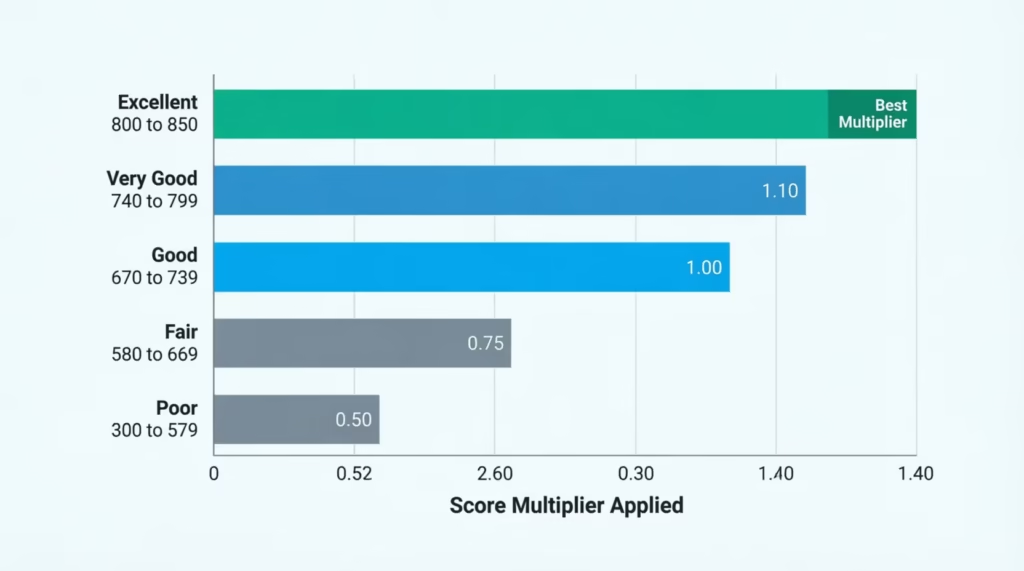

Step 6: Apply the credit score multiplier

Your credit score category multiplies the base limit up or down:

| Credit Score Category | FICO Score Range | Multiplier Applied |

|---|---|---|

| Poor | 300 to 579 | 0.50 |

| Fair | 580 to 669 | 0.75 |

| Good | 670 to 739 | 1.00 |

| Very Good | 740 to 799 | 1.10 |

| Excellent | 800 to 850 | 1.25 |

Raw Estimate = Base Limit x Score Multiplier

Step 7: Adjust for high credit utilization (if provided)

If your current utilization is above 50%, the estimate is reduced by up to 30%. The reduction scales linearly as utilization climbs from 50% toward 100%. A utilization of 75%, for example, triggers a 15% reduction.

Step 8: Apply floors and caps

- Minimum limit: $500 (no result drops below this)

- Poor credit cap: $2,000

- Final result: rounded to the nearest $100

Step 9: Build the estimate range

Lower Bound = Final Limit x 0.85 Upper Bound = Final Limit x 1.15

This 30% spread reflects the real-world variation across different card issuers. Two banks reviewing the same applicant may reasonably arrive at different numbers.

Tip: → Thinking your limit should be higher? The credit card limit increase request letter gives you a starting point.

How to Use This Calculator (Step by Step)

Here’s exactly what to do to get your estimate:

Step 1: Enter Your Annual Income

Type your total pre-tax annual income. List all your income sources: your main salary, freelance work, rental income, side jobs, and any other steady earnings. The least accepted value is $1,000.

Step 2: Enter Your Monthly Housing Costs

Enter your monthly rent or mortgage payment. If you live rent-free (for example, with family), enter $0. Don’t include utilities or renters insurance here. Just the base housing cost.

Step 3: Enter Your Existing Monthly Debt Payments

Enter the total of all recurring monthly debt payments you currently make:

- Car loan payments

- Student loan payments

- Personal loan payments

- Minimum payments on existing credit cards

Do not include everyday living expenses like groceries, gas, or subscription services. This field is for actual debt obligations only.

Step 4: Select Your Credit Score Category

Choose the range that best matches your current FICO score. Not sure what your score is? Check it for free at AnnualCreditReport.com, through your bank’s mobile app, or via a free credit monitoring service. Knowing your score before applying is always a smart move.

Step 5: Add Your Current Card Balances and Total Limits (Optional but Recommended)

For a more accurate result, enter:

- Your current total balances across all credit cards

- Your current total credit limit across all credit cards

These two optional fields allow the tool to apply the utilization change and raise your result to “High” confidence. Without them, the confidence level stays at “Medium” even if every other input is complete.

Step 6: Select Your Employment Status

Choose the option that best fits your current work situation. The available options are: Full-time, Part-time, Self-employed, Student, Retired, and Unemployed.

Step 7: Review Your Results

Results appear and update in real time as you fill in the form. There’s no “Calculate” button. The tool recalculates on its own as you type.

Once your estimate appears, you can:

- Download a PDF summary of your results using the “Download PDF” button.

- Save a shareable link to your inputs using the “Copy Link” button.

- Share your results directly to Facebook, X (formerly Twitter), WhatsApp, or Reddit using the social share buttons.

How to Read Your Results

After the tool calculates, you’ll see four key outputs. Here’s what each one tells you.

Estimated Credit Limit: This is your central estimate, rounded to the nearest $100. It’s the most likely starting point based on the data you entered.

Limit Range: This is a 30% window around the central estimate. Expect actual offers to fall somewhere within this zone, depending on which issuer you apply with and their internal policies.

Confidence Level

- High: You provided all inputs, including current balances and limits. Your estimate is the most reliable it can be with this tool.

- Medium: You skipped optional fields, or your current utilization is above 50%. The range is wider and less precise.

- Low: Your monthly obligations exceed your monthly income. This is a serious signal that a lender will likely see significant risk before setting any limit.

DTI and Projected Utilization: Your DTI result shows where you stand against typical lender benchmarks. Chase’s guidance on debt-to-income ratios indicates that a ratio at or below 36% puts you in a strong position for new credit approvals. Your projected utilization shows what your total credit usage would look like once a new card is added to the mix.

Tip: → Keep all your card limits organized in one place with the credit card tracker templates.

Real-World Example

Let’s run a complete example to see the formula in action from start to finish.

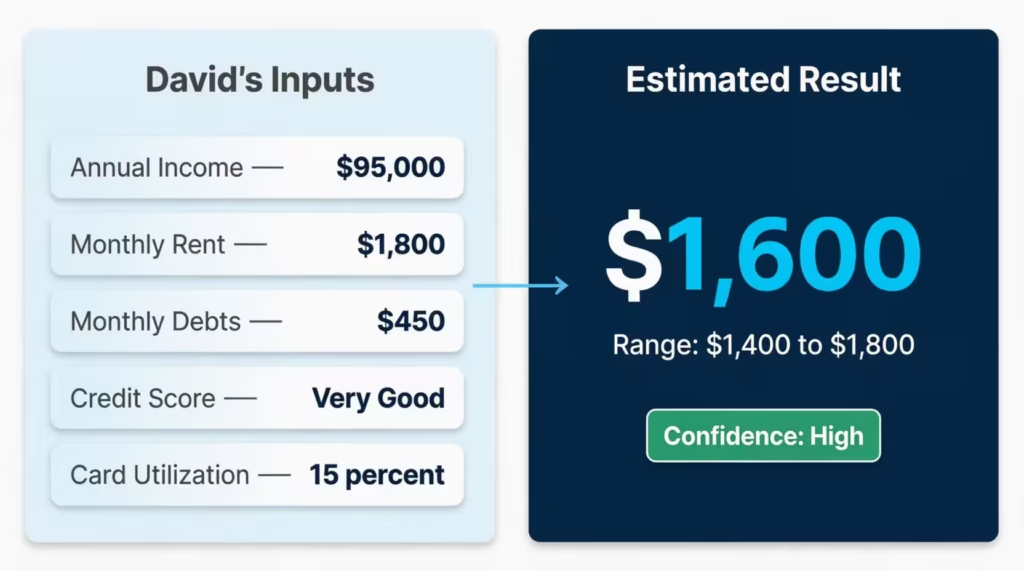

The person: David, a software developer at a SaaS startup in Austin, Texas.

David’s inputs:

- Annual income: $95,000

- Monthly rent: $1,800

- Existing monthly debt payments (car loan + student loan): $450

- Credit score category: Very Good (740 to 799)

- Current card balances: $1,200

- Current total card limits: $8,000

Step-by-step calculation:

Monthly income: $95,000 / 12 = $7,917

Monthly obligations: $1,800 + $450 = $2,250

DTI: $2,250 / $7,917 = 28% (well within the healthy range)

Disposable income: $7,917 – $2,250 = $5,667

Base limit: $5,667 x 0.25 = $1,417

Very Good score multiplier (1.10): $1,417 x 1.10 = $1,559

Current utilization: $1,200 / $8,000 = 15% (below the 50% threshold, so no reduction)

Final result: $1,600 (rounded to nearest $100)

Estimate range: $1,400 to $1,800

Confidence level: High

David now knows his most likely starting limit before applying to a single card. If he spends 60 to 90 days boosting his score to Excellent, the multiplier goes up to 1.25. This would raise his central estimate to $1,800 and the upper limit to $2,100. That’s a meaningful difference for just a score category shift.

Expert Tips and Insights

Want a higher estimate next time you run the numbers? These strategies actually move the result.

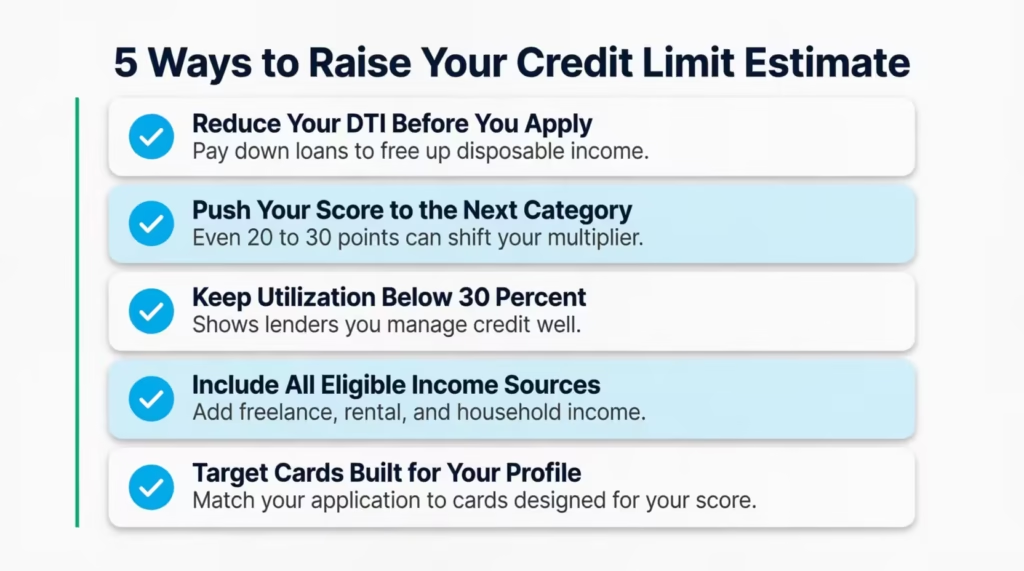

Tip 1: Reduce your DTI before you apply.

Paying off a car loan or making an extra payment on a personal loan directly raises your disposable income. A DTI drop from 40% to 28% can boost your estimated limit by several hundred dollars. This change often shifts your result from Medium to High confidence.

Tip 2: Push your credit score to the next category.

Moving from Good to Very Good adds a 10% multiplier. Moving to Excellent adds 25%. Even a small push of 20 to 30 points can cross a category line. To get there quickly, focus on paying down your existing balances. Also, don’t apply for other credit in the 60 to 90 days before your application. These two steps are the fastest ways to improve your chances.

Tip 3: Keep your utilization below 30%.

Research from Experian indicates that consumers with good or better FICO scores typically maintain average utilization below 30%. Staying below that limit helps your score. It shows new lenders that you manage credit responsibly.

Tip 4: Include all eligible income sources.

When you apply for a card, most issuers let you report household income, not just your personal salary. Freelance work, rental income, and spousal income can often be included. An increase in reported income results in a larger disposable income base, which raises your estimate.

Tip 5: Target cards built for your profile.

Premium rewards cards typically start with higher limits because they’re designed for higher-income applicants. A student card or secured card is built for lower limits and credit building. Applying for a card that matches your actual profile improves your odds of a strong limit from day one.

⚠️ Mistake to Avoid: Don’t apply for several cards at once, hoping one will come back with a high limit. Every application triggers a hard inquiry. Too many hard inquiries in a short time can drop your score by 5 to 15 points. This makes your next application weaker, not stronger.

Common Mistakes to Avoid

These are the most frequent errors people make when using a credit limit estimator or preparing for a credit card application.

Mistake 1: Only Entering Your Base Salary

Annual income isn’t limited to your paycheck. Freelance work, rental income, investment income, and bonus compensation can all count. Not including these sources means the tool has less information. This leads to a lower estimate than what you might actually qualify for.

Mistake 2: Including Living Expenses in the Debt Payments Field

The “Existing Monthly Debt Payments” field is for formal debt obligations only. Groceries, utilities, streaming services, and phone bills don’t belong here. Adding non-debt expenses raises your monthly costs. This reduces your disposable income and creates an estimate that appears too low.

Mistake 3: Skipping the Optional Balance and Limit Fields

These fields label themselves as optional, but filling them in makes a real difference. Without them, the tool can’t calculate your current utilization rate. That keeps the confidence level at “Medium” and limits the accuracy of the estimate. If you know your current balances and total limits, enter them.

Mistake 4: Taking the Estimate as a Guaranteed Outcome

This tool produces an estimate based on a standardized model. Real lenders use proprietary systems, pull a full credit report, and factor in details this calculator can’t access. The estimate is a strong planning tool, not a confirmed offer. Treat it as a realistic starting point.

Mistake 5: Applying for Multiple Cards at the Same Time

Some applicants apply to several cards at once, hoping at least one approves. Each application triggers a hard inquiry. Multiple hard inquiries in a short window can lower a credit score and signal financial strain to lenders. Apply for one card at a time. Space applications at least six months apart.

Mistake 6: Ignoring a High DTI

A high debt-to-income ratio doesn’t just affect credit card applications. It can impact mortgage approvals, auto loan rates, and other borrowing as well. If the DTI shown in the results is above 36%, it should be a broader financial priority. It’s not a matter of credit card debt.

Frequently Asked Questions (FAQs)

What credit score do I need to qualify for a high credit limit?

A FICO score of 740 or above (Very Good) typically unlocks access to higher starting limits. Excellent credit (800+) produces the strongest results and qualifies you for premium card products with the most generous initial limits.

Does income alone determine my credit limit?

No. Income is one key factor. However, lenders also consider your DTI, credit score, current utilization, and employment status. Two applicants with the same salary can have different limits. This depends on their overall credit profile.

Will using this calculator hurt my credit score?

Not at all. This tool doesn’t pull your credit report and doesn’t file any application. Everything you enter stays private and is only used to calculate your local estimate.

What is a good DTI ratio for a credit card application?

Most lenders prefer a DTI below 36%. A DTI between 36% and 42% may still get approved, but your limit and interest terms will likely be less favorable. A DTI above 50% is a significant barrier to approval.

Why did the tool produce a lower estimate despite my high income?

High monthly payments cut into your disposable income. This income is key to the whole calculation. If your housing and debt payments take up most of your earnings, your leftover money shrinks quickly. This happens no matter how much you earn.

What happens in the calculator if my utilization is above 50%?

The tool applies a reduction of up to 30% to your raw estimate. High utilization shows lenders you’re using a lot of credit. This makes them see you as a higher risk for repayment. As a result, they may lower the credit limit they offer.

Can I use my household income, not just my personal salary, on a credit card application?

Yes. Most major card issuers allow you to include household income if you have reasonable access to it. Spousal income, freelance earnings, and rental income often qualify. Always verify the specific policy with the issuer before you apply.

How long should I wait before requesting a credit limit increase on a new card?

Most issuers recommend waiting at least 6 to 12 months. A strong history of on-time payments and low utilization helps make the best case for a higher limit when you ask.

Bottom Line

Walking into a credit card application without a clear picture of your expected limit wastes hard inquiries and leads to real disappointment. This tool provides a data-backed estimate based on key factors lenders value: income, obligations, and credit score category.

Start by reducing your debt-to-income ratio before applying. This input has the greatest impact on the estimate and improves your overall financial situation at the same time. That one shift can unlock a credit card limit that is significantly stronger during crucial moments.

If this guide helped you understand your credit standing, please share it on social media. You might know a friend or family member who’s thinking about applying for a new card. It might save them a hard inquiry and a lot of frustration.