Daily Periodic Rate (DPR) Calculator

Instantly convert APR to DPR and see your daily interest costs.

Last Updated: September 5, 2025

Enter Your Details

Enter APR (e.g., 24 or 24%) — DPR = APR ÷ 365.

Your Results

Daily Periodic Rate (DPR)

-

(-)

Daily Interest Cost

-

Based on your balance

Estimated Interest Accrued

-

in 30 Days

Enter a balance to see your daily interest cost.

30-Day Interest Accrual

How to Use This Calculator

- 1 Enter your card's APR (e.g., 24 or 24%). The calculator instantly shows the Daily Periodic Rate.

- 2 Optionally, enter your current balance to see the actual dollar cost of interest per day.

- 3 Use the slider and preset buttons for quick comparisons and see the 30-day interest chart update live.

- 4 Download a PDF summary or share your results with a link that prefills the data for others.

Disclaimer

This calculator is for informational purposes only. The results are estimates based on the information you provide and may not be accurate or applicable to your specific financial situation. The information provided does not constitute financial, legal or tax advice. We do not guarantee the accuracy of the calculations or the applicability of any information. Always consult a qualified financial professional for advice specific to your personal circumstances. Credit card terms, conditions, rates and offers are subject to change by the issuing bank at any time. We are not responsible for any actions or decisions taken based on the information provided by this tool.

Most credit card holders know their APR number. But very few understand what it actually costs them each single day. That gap is silent, and it can drain your wallet faster than you’d think.

The Federal Reserve reports that the average credit card APR on accounts carrying a balance was 22.30% as of November 2025. This makes a credit card DPR calculator one of the most practical tools you can have.

The daily periodic rate is your APR divided by 365. It shows the exact interest your card charges on your balance every day.

Keep reading. This guide walks you through the formula, the key features, and every step you need to take full control of your daily interest cost.

Tip: → See how this daily rate fits into your full billing period with the credit card billing cycle calendar.

What Is a Daily Periodic Rate (DPR)?

The daily periodic rate is the interest rate your credit card applies to your balance every single day. It’s a small number. But don’t let that fool you. It compounds quietly, and over time, it adds up to real money.

Your APR (Annual Percentage Rate) is the number most credit card companies advertise. But here’s the thing. Your card doesn’t wait until December 31 to charge you interest. It works through your balance every day. That’s exactly where the DPR comes in.

Think of it this way. If your APR is 24%, your card takes that annual rate and slices it into 365 tiny pieces. Each piece is your DPR. Every day you carry a balance, that daily rate gets applied to what you owe.

Your DPR and your APR are always linked. One originates from the other. To lower your DPR, you need to lower your APR. There’s no shortcut around that.

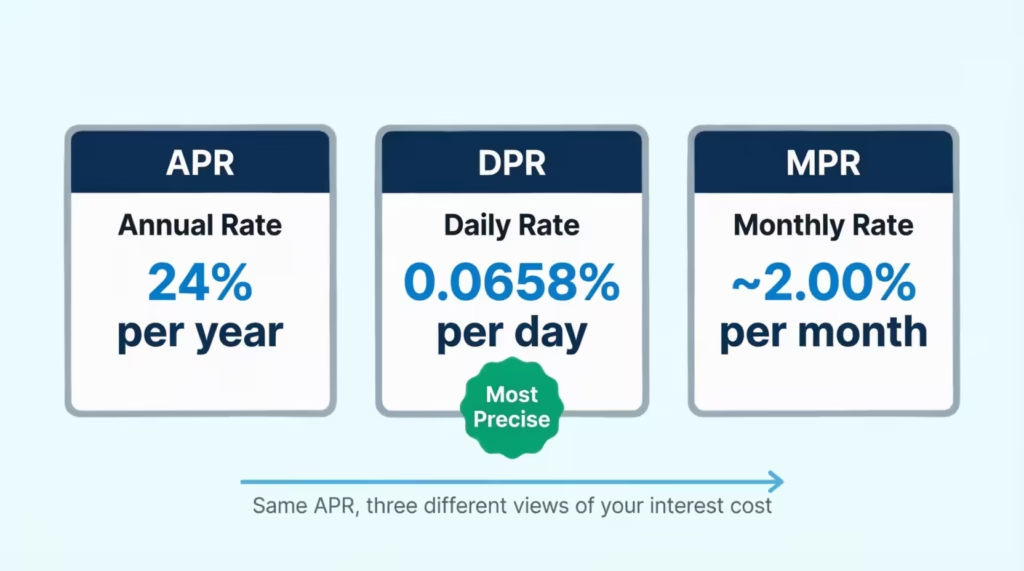

DPR vs. APR vs. MPR: What’s the Real Difference?

A lot of people get these mixed up. Here’s a simple side-by-side comparison:

| Rate | What It Measures | Example at 24% APR |

|---|---|---|

| APR | Annual interest rate | 24% per year |

| DPR | Daily interest rate | 0.0658% per day |

| MPR | Monthly interest rate | ~2.00% per month |

The DPR is the most precise view of your interest cost. It’s the actual rate your card uses to calculate the finance charge on your balance day by day. As the Consumer Financial Protection Bureau explains, a daily periodic rate is used to calculate interest by multiplying the rate by the amount owed at the end of each day.

How This Calculator Works

This daily rate tool takes your APR and converts it into a DPR instantly. No math needed on your end.

Here’s what happens behind the scenes when you enter your numbers:

- You type in your APR (like 24%).

- The calculator divides that number by your chosen day base (365 or 360).

- It shows your DPR as both a percentage and a decimal.

- If you enter a balance, it shows the exact dollar amount of interest you pay each day.

- It then projects your cumulative interest over 30 days using a compound interest model.

The chart on the right side of the tool updates live as you type. It displays a 30-day line graph showing how your interest builds day by day. That visual makes it very easy to see how quickly a balance can grow, even without any new purchases.

Tip: → Curious how this number shows up on a real statement? Check the sample credit card statement.

Key Features of This Calculator

- APR input with a live slider and quick preset buttons (12%, 18%, 24%, 29.99%)

- Optional balance input to see real dollar interest costs

- 365 vs. 360-day base toggle for standard or financial-year calculations

- Live 30-day cumulative line chart to show interest accrual visually

- Monthly equivalent toggle to see your average monthly interest figure

- Copy Results button to grab your numbers instantly

- Download PDF button to save a full summary to your device

- Save Inputs toggle so the calculator remembers your data on your next visit

- Social share buttons to share your results on Facebook, WhatsApp, X, or Reddit

📌 Did You Know: Some financial institutions calculate DPR using a 360-day year instead of 365 days. This slightly raises your effective daily rate. It’s more common in business lending and some older cardholder agreements. Always check your card’s terms to confirm which base your issuer uses.

The Formula Explained

The math powering this tool is simple and transparent. Three formulas drive everything you see in the results.

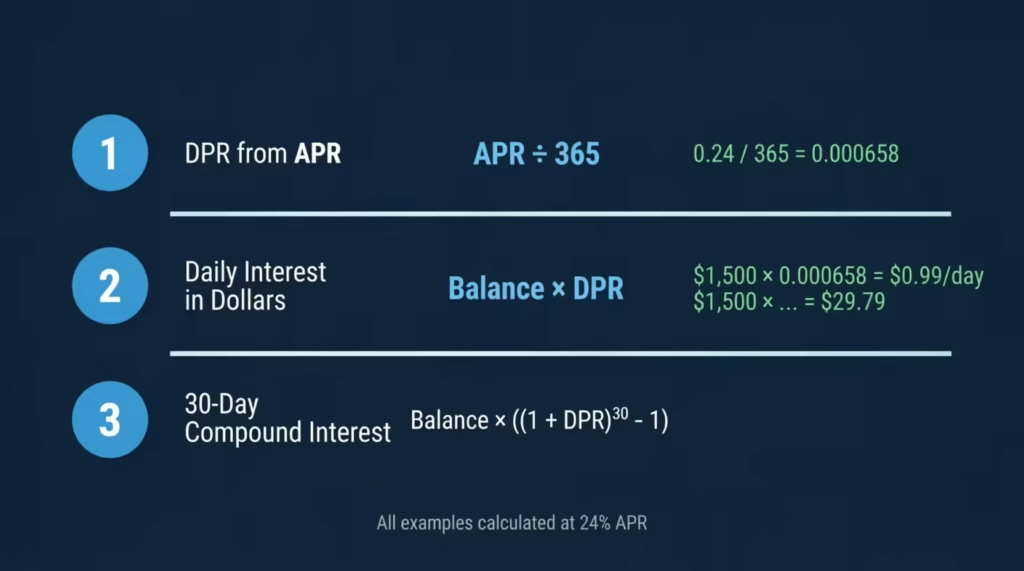

Formula 1: DPR from APR

DPR = APR divided by the number of days in a year

In decimal form:

DPR (decimal) = (APR / 100) / 365

With a 24% APR:

DPR (decimal) = 0.24 / 365 = 0.000657534

As a percentage:

DPR (%) = 0.000657534 x 100 = 0.0658%

That works out to roughly 6.6 cents in interest per day for every $100 you carry as a balance.

Formula 2: Your Daily Interest Charge in Dollars

Daily Interest = Balance x DPR (decimal)

Example with a $1,500 balance at 24% APR:

$1,500 x 0.000657534 = $0.99 per day

That’s almost one dollar of interest every single day on a $1,500 balance. It’s not devastating on its own. But it adds up fast.

Formula 3: 30-Day Cumulative Interest (Compound)

This calculator uses compound interest for its projections. That’s the right approach, because your credit card actually applies and compounds interest daily. Simple interest would understate the real cost.

30-Day Interest = Balance x ((1 + DPR)^30 – 1)

Example with $1,500 at 24% APR:

$1,500 x ((1 + 0.000657534)^30 – 1) = $29.79

That’s about $30 in interest charges in just one month on a $1,500 balance.

For the monthly average, the tool uses 365.25 / 12 = 30.4375 days. This accounts for leap years and gives a more precise monthly estimate.

💡 Pro Tip: Switching from 365 to 360 days raises your DPR slightly. At a 24% APR, the 365-day base gives a DPR of 0.0658%, while the 360-day base gives 0.0667%. On a $5,000 balance, that difference adds up to about $8 more per year. It’s small per day, but worth knowing when comparing cards.

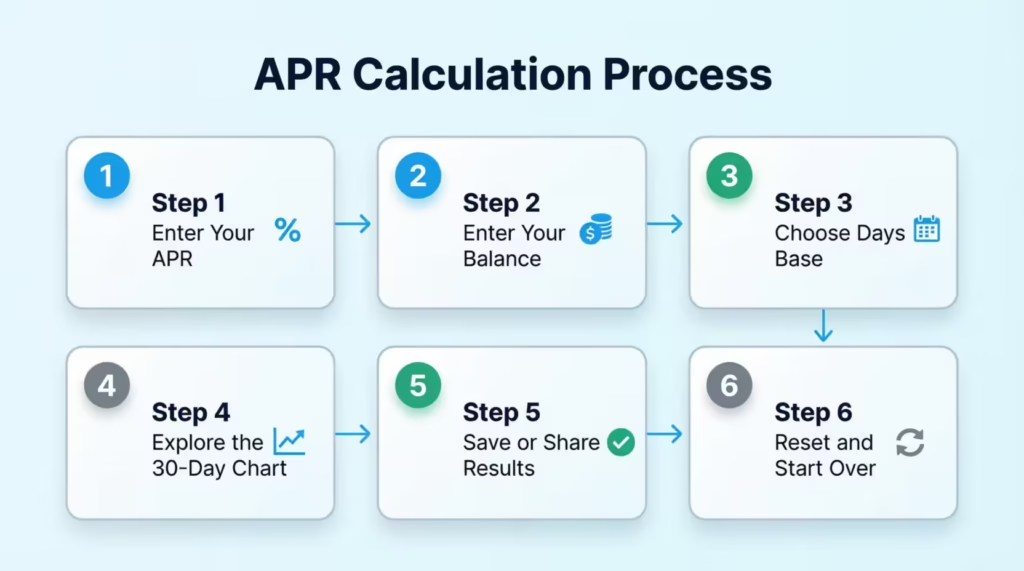

How to Use This Calculator (Step by Step)

Using this tool is fast and easy. Follow these steps to get your results:

Step 1: Enter Your APR

Type your card’s APR into the input field. You can enter “24” or “24%”. Both formats work. You can also drag the slider to your rate, or tap one of the quick preset buttons: 12%, 18%, 24%, or 29.99%.

Not sure what your APR is? Check your latest monthly statement or log into your card’s mobile app. It’s usually listed as “Purchase APR” or “Variable APR.”

Step 2: Enter Your Current Balance (Optional)

Type your current card balance to see the real dollar cost of your interest. This step is optional, but it is the point at which the results become truly useful. Without a balance, you’ll only see the DPR as a rate. With a balance, you’ll see the exact dollar amount leaving your pocket every day.

Step 3: Choose Your Days Base

Toggle between 365 (standard) and 360 (financial). Most credit cards in the U.S. use 365 days. If you’re not sure which your card uses, start with 365. You can easily flip to 360 and compare the difference.

Step 4: Explore the 30-Day Chart

Watch the cumulative interest chart update in real time. The chart plots your growing interest from Day 0 to Day 30. It’s a powerful visual that shows the compounding effect clearly. Many readers say this chart alone changes how they feel about carrying a balance.

Step 5: Save or Share Your Results

Once you have your numbers, you have several options:

- Click Copy Results to copy everything to your clipboard.

- Click Download PDF to save a clean summary as a PDF file.

- Use the social share icons to send your results to Facebook, WhatsApp, X, or Reddit.

- Check Save Inputs so the calculator auto-fills your data next visit.

Step 6: Reset and Start Over

Click the red Reset Calculator button at the bottom of the input section to clear all fields and start a fresh calculation.

How to Read Your Results

After you enter your APR, the results section shows four key outputs. Here’s what each one means:

1. Daily Periodic Rate as a Percentage

This is your APR broken down to a daily rate. For a 24% APR, this reads 0.0658%. It looks tiny. But multiply it by your balance, and it becomes a meaningful dollar figure fast.

2. DPR as a Decimal

This is the same rate in decimal form. For 24% APR, it displays as (0.000658). This is the number used in the background math. It’s shown here for full transparency.

3. Daily Interest Cost in Dollars

This is the actual dollar amount your account accrues in interest each day. It only appears when you’ve entered a balance. For $1,500 at 24% APR, this figure is about $0.99 per day. For $5,000 at 29.99% APR, it climbs to roughly $4.11 per day.

4. Estimated Interest Accrued Over 30 Days and Monthly

These are forward-looking projections. The 30-day figure shows total interest if you carry your current balance for exactly 30 days with no payments. The monthly figure uses the more precise 30.44-day average for added accuracy.

⚠️ Mistake to Avoid: Don’t assume the 30-day estimate matches your exact monthly statement charge. Your actual billing charge depends on your average daily balance across the full billing cycle, not just a flat 30-day run. Payments, new purchases, and credits all affect the final number. Use this estimate as a planning tool, not a guarantee.

Real-World Example

Here’s how all of this plays out in a real situation.

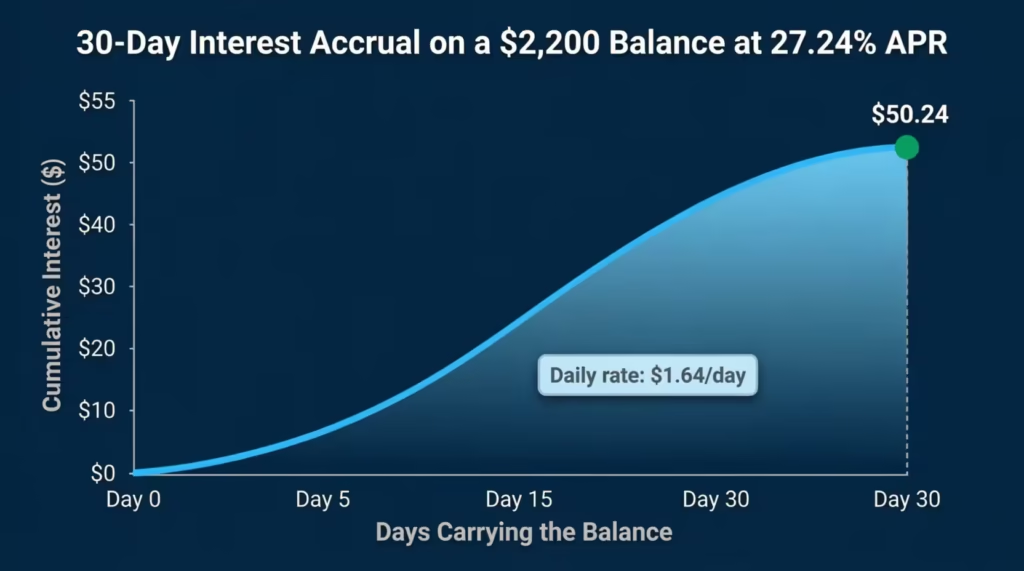

The Scenario:

Marcus is a project manager in Dallas, Texas. He carries a credit card with a 27.24% APR and a current balance of $2,200. He wants to know exactly how much that balance is costing him each day and what it adds up to over a full month.

Step 1: Calculate the DPR

DPR = 27.24 / 100 / 365 = 0.07463% per day

Decimal form: 0.0007463

Step 2: Find the Daily Interest Cost

Daily Interest = $2,200 x 0.0007463 = $1.64 per day

Every single day, Marcus carries that balance, and $1.64 in interest is added to what he owes.

Step 3: Project the 30-Day Cost

30-Day Interest = $2,200 x ((1 + 0.0007463)^30 – 1) = $50.24

Over 30 days, Marcus pays about $50 in interest on his $2,200 balance. If he only makes minimum payments, his balance barely moves. The daily interest keeps compounding on an almost unchanged principal.

What the Chart Shows:

The live chart in this tool plots Marcus’s interest from $0 on Day 1 to $50.24 by Day 30. The curve starts flat and steepens slightly near the end. That gentle upward bend is compound interest at work. It’s small early on, but it never stops.

The Takeaway:

If Marcus can pay down $500 of that balance, his daily interest cost drops from $1.64 to about $1.27 per day. That’s a savings of roughly $135 per year in interest alone, just from one targeted payoff.

Expert Tips and Insights

Tip 1: Check Your Rate Before You Ever Carry a Balance

The worst time to discover how your DPR works is after six months of carrying a balance. Look up your rate now, while you have time to plan. Even a $500 balance at a high rate costs more per month than many people expect.

Tip 2: Use DPR to Compare Cards, Not Just APR

APR looks like one clean number, but different lenders can arrive at similar APRs using different day bases. A card charging 21.99% APR on a 360-day basis costs more per day than a card charging 21.99% APR on a 365-day base. Comparing the actual DPR gives you a cleaner, more accurate picture of your real daily cost.

Tip 3: Let the 30-Day Chart Motivate You

Looking at the cumulative chart is surprisingly powerful. Watching $50, $80, or $120 climb steadily over 30 days turns an abstract APR into a concrete dollar drain. Many people see that visual and choose to pay more than the minimum. It also helps them stop adding new charges to a high-rate card.

💡 Pro Tip: Most credit card APRs in the U.S. are variable and tied to the prime rate. When the Federal Reserve raises or lowers rates, your card’s APR often follows. That means your DPR shifts, too. It’s worth running a fresh calculation whenever your card issuer sends a rate-change notice.

Tip 4: Pay Down Before Your Statement Closes

Credit card interest is typically calculated using the average daily balance method. Paying down your balance before your statement closing date reduces that average. Even a partial payment made a few days early can lower your finance charge for that cycle. You don’t have to wait for the due date to benefit.

Tip 5: The Grace Period Changes Everything

Many credit cards offer a grace period on new purchases. During this window, no interest accrues on your balance if you pay the full statement balance by the due date. If you use this feature every month, your effective daily rate is zero. The DPR only starts working against you the moment you carry a balance from one cycle to the next.

Common Mistakes to Avoid

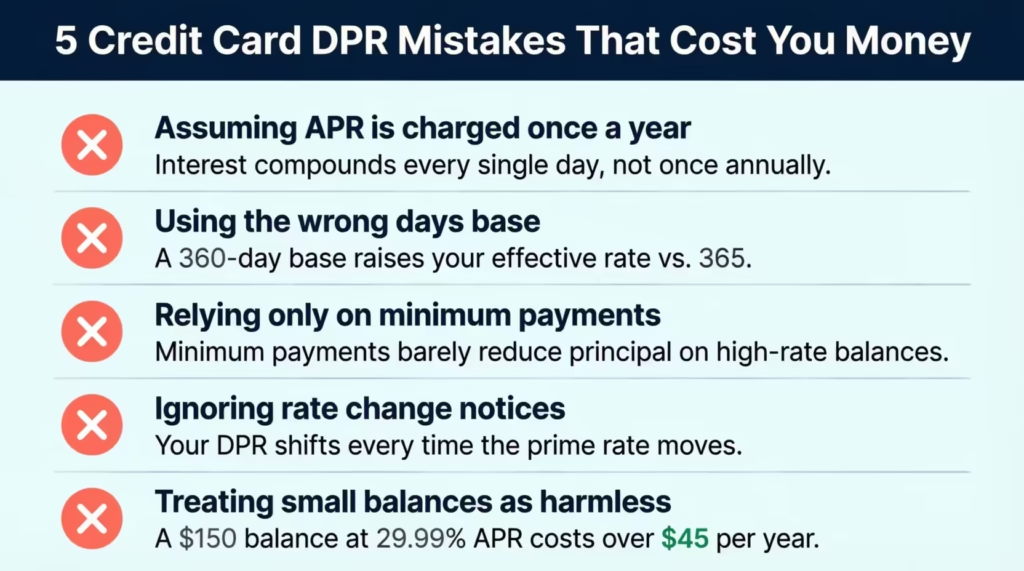

Mistake 1: Assuming APR Is Charged Once a Year

This is one of the most common misunderstandings in credit card use. Cardholders see a 24% APR and assume it means $240 per year on a $1,000 balance. That’s not how it works. The 24% gets divided into a daily rate and applied to the balance every single day. Because interest compounds, each day’s charge adds to the balance, which then earns more interest the next day.

Mistake 2: Using the Wrong Days Base

Most U.S. credit cards calculate DPR using 365 days. Some financial products use 360 days. Using the wrong base in your calculations gives you an inaccurate daily rate. The difference is small on any one day, but it becomes meaningful over months on a large balance. Always verify in your cardholder agreement.

Mistake 3: Relying Only on Minimum Payments

Jennifer, a freelance graphic designer in Chicago, made only minimum payments on her $3,400 balance for 14 months. At a 25.77% APR (DPR of 0.0706%), she paid over $680 in interest during that period. Her balance dropped by only about $320. The least payment was barely enough to cover the daily interest charges, let alone reduce the principal.

Minimum payments are important for protecting your credit score. But they do very little to protect your finances when you’re carrying a high-rate balance.

Mistake 4: Ignoring Rate Change Notices

Credit card APRs in the U.S. tend to change frequently. As the Consumer Financial Protection Bureau notes, many issuers calculate interest daily based on the average daily balance, using a rate that can change with market conditions. When the prime rate moves, your APR adjusts, and so does your DPR. Recalculate every time your issuer sends a rate-change notification.

Mistake 5: Treating Small Balances as Harmless

A $150 balance seems easy to ignore. But at a 29.99% APR, that balance accrues about $0.12 per day in interest. That’s over $45 per year on a balance many people simply forget about. Small leftover balances, especially on cards that are rarely used, are a quiet and constant leak.

Frequently Asked Questions (FAQs)

What is the daily periodic rate on a credit card?

The daily periodic rate is the interest rate applied to your credit card balance each day. It’s calculated by dividing your card’s APR by 365 (or 360, depending on your issuer’s terms).

Is the DPR the same as the daily interest rate?

Yes. The daily periodic rate and the daily interest rate are the same thing. Both refer to the part of your APR charged to your balance on any given day.

What is a typical DPR for a credit card in the U.S.?

At a 24% APR, the DPR is about 0.0658% per day using a 365-day base. At a 20% APR, it drops to about 0.0548% per day. Higher APRs produce higher DPRs.

Does credit card interest actually compound daily?

Yes. Most U.S. credit cards compound interest daily. Interest builds on your balance daily, so it earns even more interest the next day. This is why keeping a balance for months can cost much more than a basic APR calculation shows.

Why do some credit cards use 360 days instead of 365?

The 360-day convention is a holdover from older banking practices. Some issuers, particularly in commercial lending and older card agreements, still use it. A 360-day base produces a slightly higher effective daily rate than a 365-day base at the same APR.

What’s the difference between DPR and MPR (monthly periodic rate)?

The DPR is your daily interest rate, while the MPR is your monthly rate. MPR is calculated by dividing APR by 12. DPR is more accurate for credit cards because most issuers apply interest daily, not monthly.

Can I lower my credit card’s DPR?

Yes, but only by reducing your APR. You can request a rate reduction from your card issuer. You can also transfer your balance to a card with a lower rate. Additionally, working on improving your credit score can help you qualify for better rates over time.

Will my DPR change over time?

It can. Most credit cards carry variable APRs tied to the prime rate. When the prime rate shifts, your APR adjusts, and your DPR moves with it. Check your card agreement to find out if your rate is fixed or variable.

How is daily interest different from monthly interest on my statement?

Daily interest is the charge applied each day to your running balance. Your monthly statement charge is the total of all those daily charges across your full billing cycle, based on your average daily balance. They’re related, but not the same number.

Bottom Line

Understanding your daily interest cost is one of the simplest ways to get smarter with your credit cards. We’ve walked through what DPR is, how the formulas work, how to read your results, and which mistakes cost people the most money.

Of everything covered here, the most important takeaway is this: your APR is not a once-a-year event. It’s a daily charge that accumulates on every dollar you carry without drawing attention. Using a credit card DPR calculator to put a real dollar figure on that cost can genuinely change how you manage your balance.

If this guide helped you, please share it with a friend or family member who carries a credit card balance. It could save them real money.