Ever checked your credit card bill and spotted a charge you don’t recognize? You’re not alone. The CFPB’s 2025 Consumer Credit Card Market Report found that cardholders disputed $9.8 billion in credit card charges in a single year. A well-written credit card dispute letter template gives you the fastest path to challenge those errors and protect your money.

A formal written dispute is the strongest tool you have under federal law. It forces your card issuer to investigate and respond.

This guide walks you through every step. You’ll learn what to include, how to fill out the template, and how to send it the right way. Ready-to-use templates are waiting for you right below.

Download Your Free Credit Card Dispute Letter Templates

4 ready-to-use templates are available to make your life easier. Each one has the sections you need. It includes a transaction table. There’s also a dispute explanation area, an attachments checklist, and a signature block.

Pick the format and paper size that works best for you:

These templates are 100% free. Just click the link, download, and start filling in your details!

What Is a Credit Card Dispute Letter?

A credit card dispute letter is a formal written notice sent to a card issuer. It tells the company that a charge on your statement is wrong. The letter asks the issuer to investigate and fix the error.

This isn’t just a complaint. It’s a legal document backed by the Fair Credit Billing Act (FCBA). When the issuer gets your written notice, they must follow specific rules. They have to confirm they got it within 30 days. Then they must resolve the issue within two billing cycles.

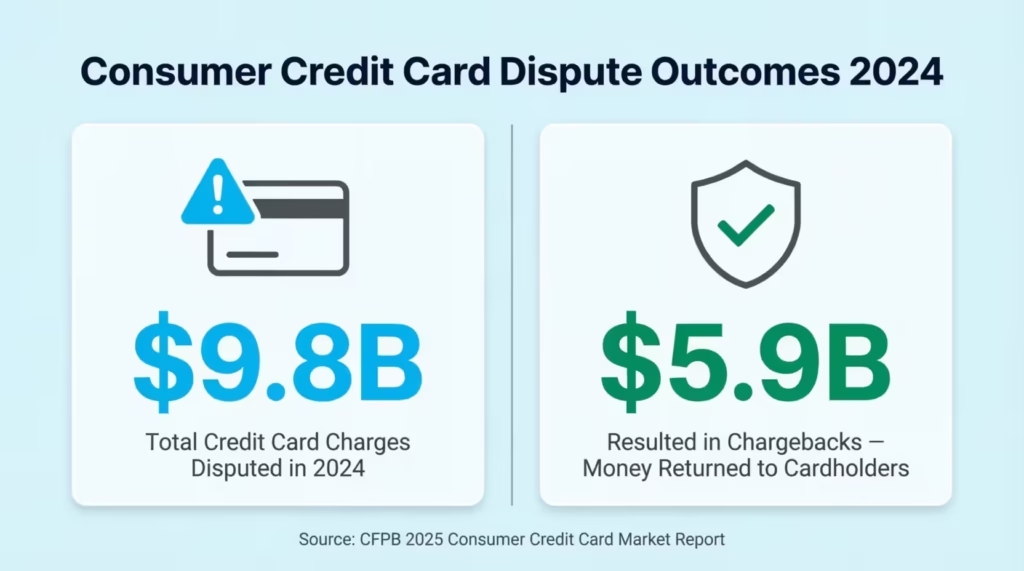

The scale of billing disputes is huge. The CFPB’s 2025 Consumer Credit Card Market Report reveals that $9.8 billion in credit card charges were disputed in 2024, with $5.9 billion resulting in chargebacks. That tells you two things. First, billing errors and fraud happen a lot. Second, disputing charges works.

A written letter creates a paper trail. Phone calls don’t give you the same legal protection. When you put your dispute in writing, you lock in your rights under federal law. You also create proof of when you sent it and what you said.

💡 Pro Tip: Even if you report a charge by phone or online first, always follow up with a written letter. The written notice is what triggers your full legal protection under the FCBA.

When Do You Need a Billing Dispute Letter?

Not every billing issue needs a formal letter. But several common situations call for one. Here are the most frequent reasons cardholders file written disputes:

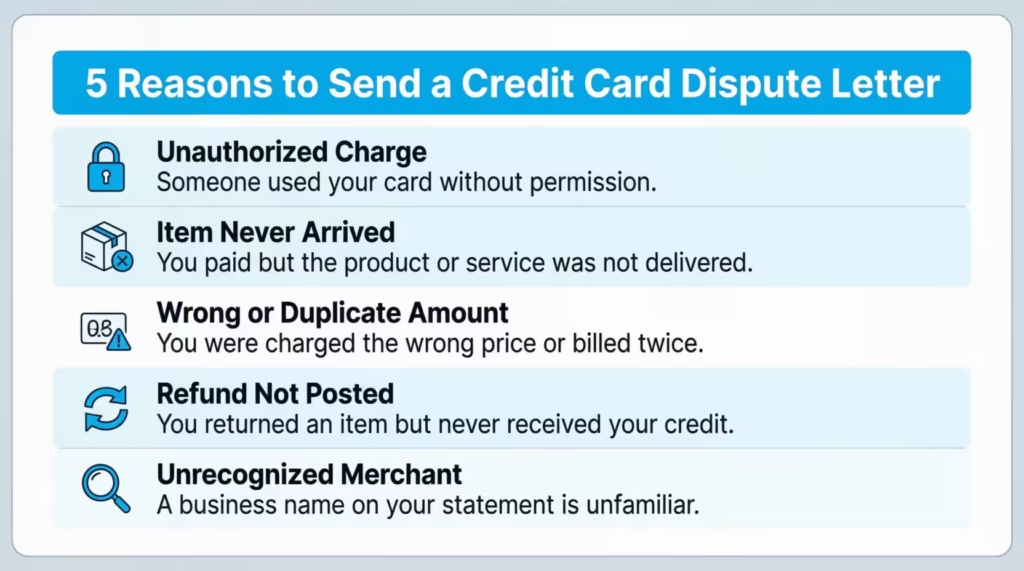

Unauthorized or Fraudulent Charges

Someone used your card without permission. Maybe your card number was stolen online. Or a thief used a lost or stolen card. Federal law caps your liability at $50 for unauthorized charges on credit cards. But you still need to report them.

Charges for Goods or Services Not Received

You paid for something that never showed up. The seller promised delivery by a certain date, but the product never arrived. A dispute letter starts the formal process to get your money back.

Wrong Amounts or Duplicate Charges

The merchant charged $250 instead of $25. Or the same purchase shows up twice on your statement. These math errors and double charges are classic billing mistakes.

Charges After a Cancellation or Return

You returned an item or canceled a service. But the refund never posted to your account. The merchant may have dropped the ball, and the issuer needs to step in.

Charges You Don’t Recognize

A merchant name on your statement looks unfamiliar. Sometimes this is just a “doing business as” name. Other times, it’s a sign of fraud. Filing a written dispute gets the issuer to dig into the details.

⚠️ Mistake to Avoid: Don’t wait too long to send your letter. Federal law requires your written notice to reach the card issuer within 60 days of the first statement showing the error. Miss that window, and you could lose your dispute rights.

What to Include in Your Billing Dispute Letter

A strong dispute letter has specific parts. Miss one, and the issuer may delay or deny your claim. Here’s what every written billing error notice needs:

Your Personal Information

- Full legal name (as it appears on the account)

- Current mailing address

- Phone number and email address

Account Details

- Credit card account number (or last 4 digits)

- Dispute reference number, if you have already reported by phone

Transaction Details

For each charge you’re disputing, include:

- Transaction date

- Merchant name

- Amount posted to your account

- The amount you’re disputing

- Reason for the dispute

The templates provided above include a ready-made table where you can fill in all of these details for up to five transactions at once.

A Clear Explanation

Write a short, factual explanation of why you believe the charge is wrong. Stick to the facts. For example:

- “This charge was not authorized by me.”

- “I returned the item on [date], but no refund was posted.”

- “The correct charge should be $45.00, not $450.00.”

Your Requested Action

State what you want the issuer to do. Common requests include:

- Investigate the charge

- Remove or reverse the disputed amount

- Issue a credit or refund

Supporting Documents

List and attach copies (never originals) of any evidence. The FTC recommends including receipts, billing statements, proof of return or cancellation, and any messages between you and the merchant.

Your Signature and Date

Sign the letter and date it. If you’re using the Word template, you can type your name and add a digital signature.

How to Fill Out the Credit Card Dispute Letter Template (Step by Step)

Each template follows the same layout. Here’s how to complete it from top to bottom.

Step 1: Add the Date

Write today’s date at the top. Use a clear format like “April 3, 2026” or “03 April 2026.” This date matters because it proves when you prepared the letter.

Step 2: Fill In Your Contact Details

Enter your full name, street address, city, state, ZIP code, phone number, and email. This section appears right below the date.

Step 3: Enter the Card Issuer’s Information

Add the name of your credit card company, the disputes department, and their mailing address. Look on the back of your card, your monthly statement, or the issuer’s website for the correct billing inquiry address.

This address is usually different from the one where you send payments. Using the wrong address can delay your dispute.

Step 4: Add Your Account Information

Fill in the subject line with your account number (last 4 digits) and any dispute reference number you already have. The subject line in the template reads: “Re: Billing Dispute – Credit Card Account Ending [Last 4 Digits].”

Step 5: Complete the Transaction Table

This is the core of your letter. For each charge you’re disputing, fill in one row of the table:

- Date – The date the transaction was posted

- Merchant – The name of the business

- Posted Amount – What appeared on your statement

- Disputed Amount – The amount you’re challenging

- Reason – A brief reason code or phrase (e.g., “Unauthorized,” “Duplicate,” “Not received”)

The templates support up to five transactions. If you have more, use a second copy of the template.

Step 6: Write Your Dispute Explanation

Below the table, there’s a text area labeled “Dispute Explanation” or “Detailed Dispute Explanation.” Write 2 to 4 sentences explaining the facts. Be specific. Include dates, amounts, and what happened.

Example: “The charge from Electronics Giant on January 5, 2026, for $899.00 was not authorized by me. I did not visit this store or make this purchase. I believe my card number was compromised.”

Step 7: Check Your Resolution Request Boxes

The templates include checkboxes for what action you want:

- Investigation requested

- Charge removal requested

- Refund or credit requested

Check one or more boxes that match your situation.

Step 8: Complete the Attachments Checklist

Mark, which supporting documents are you including:

- Copy of credit card statement

- Receipt or invoice

- Proof of return or cancellation

- Messages or emails from the merchant

- Police report (for fraud cases)

Step 9: Sign and Date the Letter

Print your name, sign above it (or add a digital signature), and write the date you signed. This finalizes the letter and makes it official.

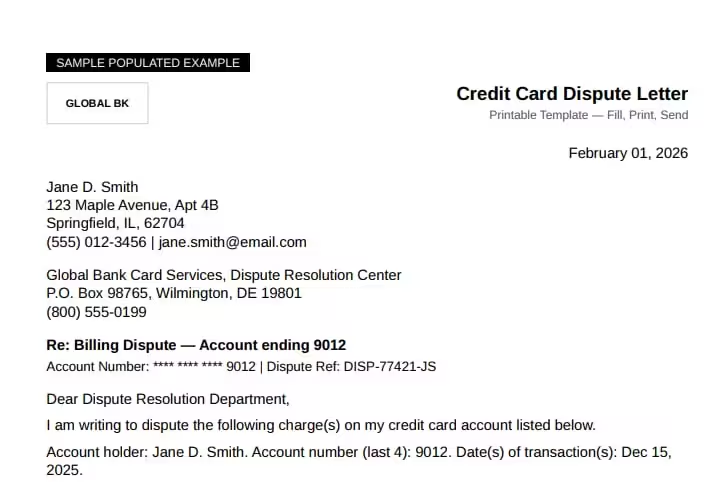

📌 Did You Know: The PDF templates come with a pre-filled sample on page 2. One shows “Jane D. Smith” disputing an unauthorized charge and a duplicate charge. The other shows “Robert Smith” challenging an unauthorized charge and a math error. These samples show you exactly how a completed letter should look.

How to Send Your Dispute Letter (The Right Way)

Writing the letter is half the battle. Ensuring its accurate delivery is equally important.

Use Certified Mail With Return Receipt

The best way to send a billing dispute notice is through USPS Certified Mail with a return receipt requested. This gives you:

- Proof that you mailed the letter

- Proof that the issuer received it

- The exact date of delivery

This paper trail becomes critical if the issuer claims they never got your letter.

Send It to the Right Address

Card issuers have a specific address for billing disputes. It’s different from the payment address. Check your monthly statement, the back of your card, or the issuer’s website for the “billing inquiries” or “disputes” address.

Sending your letter to the wrong address can delay the process and may not count as proper notice under the law.

Keep Copies of Everything

Before mailing, make copies of:

- The signed letter

- All attachments

- The certified mail receipt

- The return receipt (once you get it back)

Store these in a folder. You may need them later if the issuer doesn’t respond on time.

Follow Up in Writing

If you also filed by phone or online, the written letter is still necessary. Many card companies let you submit disputes through their website or app. That’s a good first step. But a mailed letter locks in your legal protections under the FCBA.

What Happens After You Send the Letter?

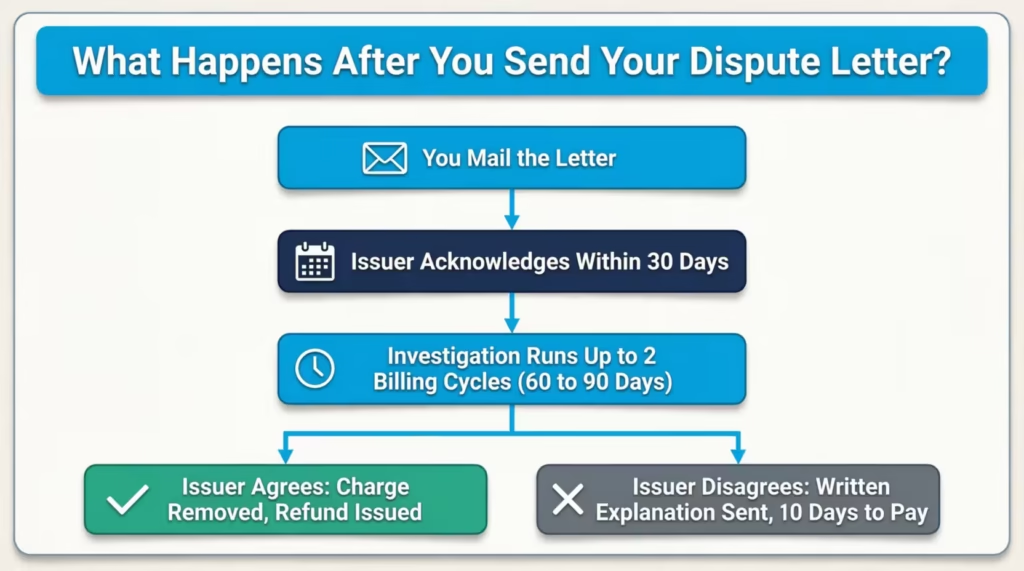

Once the card issuer receives your written dispute, a specific timeline kicks in. Federal regulation spells out every deadline.

30-Day Acknowledgment

The issuer must send you a written confirmation within 30 days of receiving your letter. This letter confirms they got your dispute and that it’s under review. The only exception is if they resolve the issue within that 30-day window.

Two Billing Cycle Investigation

CFPB billing error regulations require the issuer to complete its investigation within two complete billing cycles. That’s roughly 60 to 90 days, depending on your billing dates. They can’t take longer than 90 days in any case.

Your Payment Rights During the Dispute

While the investigation is open, you don’t have to pay the disputed amount. You also won’t owe finance charges or late fees on that specific charge. But you must keep paying the rest of your balance as usual.

The Outcome

After the investigation, one of two things happens:

- The issuer agrees with you. They remove the charge, refund any related fees, and correct your statement.

- The issuer disagrees. They send you a written explanation of why. They also tell you how much you owe and when payment is due. You then have at least 10 days to pay before any late fees apply.

⚠️ Mistake to Avoid: Don’t stop paying your undisputed balance while you wait for the investigation. Only the disputed charge is protected. Missing payments on the rest of your bill can trigger late fees and hurt your credit.

Common Mistakes That Can Weaken Your Dispute

Filing a billing dispute seems simple. But small errors can cost you time, money, or your legal rights. Here are the most common ones to watch for:

Waiting Too Long to Send the Letter

The 60-day deadline is strict. It starts from the date the first statement with the error was mailed to you, not when you noticed it. Mark your calendar when each statement arrives.

Sending the Letter to the Wrong Address

Sarah, an account manager at a mid-size tech company, sent her dispute letter to the wrong address. She mistakenly sent it to general customer service instead of the billing disputes department. It took three extra weeks before the right team even saw her letter. Always double-check the address for billing inquiries.

Not Including Enough Detail

Vague letters get vague results. “I don’t recognize this charge” is weaker than “I did not authorize the $350.00 charge from XYZ Electronics on March 12, 2026. I was traveling out of state on that date and have attached my flight itinerary as proof.”

Forgetting to Attach Evidence

A dispute letter without supporting documents puts all the burden on the issuer to figure things out. Attach statement copies, receipts, and correspondence. This shows the issuer that your claim is serious and well-documented.

Only Disputing by Phone

Michael, a freelance graphic designer, called his card company about a duplicate charge. The phone agent said they’d handle it. Six weeks later, nothing had changed. He had no proof he ever reported it. A written letter would have started the legal clock and created a record.

Not Keeping Copies

If the issuer loses your letter or says they never got it, keep copies of everything. This includes the letter, attachments, and certified mail receipt. These are your backups. Without them, the dispute becomes your word against theirs.

Tip: → Think a fee on your statement was charged incorrectly? Confirm it first with the credit card fee calculator.

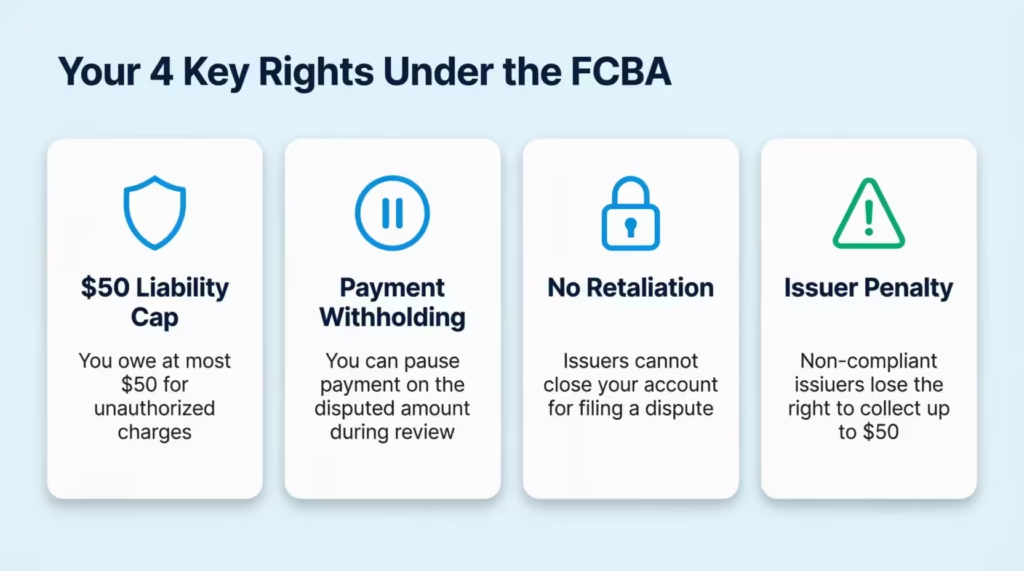

Your Rights Under the Fair Credit Billing Act (FCBA)

The Fair Credit Billing Act is the federal law that protects credit card users from billing errors. Knowing your rights helps you use your dispute letter with confidence.

What the FCBA Covers

The FTC explains that the FCBA covers credit cards and revolving charge accounts. It sets out a formal dispute process for billing errors, including unauthorized charges, incorrect amounts, and charges for undelivered goods.

Key Protections for Cardholders

- $50 liability cap. For unauthorized charges, cardholder liability is limited to $50 under federal law. Many issuers offer zero-liability policies that go even further.

- Payment withholding rights. During the investigation, the disputed amount doesn’t have to be paid. Finance charges on that amount are also paused.

- Protection from retaliation. The issuer can’t close your account, report you as delinquent, or take any negative action simply because you filed a dispute.

- Penalties for non-compliance. If the issuer doesn’t follow the dispute process, they lose the right to collect up to $50 of the disputed amount, even if the charge turns out to be valid.

The 60-Day Rule

Written notice must reach the card issuer within 60 calendar days from the date the first statement with the error was sent. This is the single most important deadline in the entire process. Don’t file your letter on day 61.

Dispute vs. Fraud Claim

A billing dispute and a fraud claim are different. Disputes cover billing errors like wrong amounts, undelivered goods, or duplicate charges. Fraud claims cover unauthorized use of your card by someone else. For fraud, there’s generally no 60-day time limit. But a written notice is still the best way to document it.

Frequently Asked Questions (FAQs)

Can you dispute a credit card charge after you’ve already paid it?

Yes. The CFPB confirms you can dispute a charge even after paying it. However, you likely won’t get a refund until the card company finishes its investigation and rules in your favor.

Does filing a credit card dispute hurt your credit score?

No. Disputing a charge on your credit card bill does not directly lower your credit score. The account may show a “dispute” notation on your credit report, but that notation alone does not affect scoring.

How long does a credit card dispute take to resolve?

The card issuer must complete its investigation within two full billing cycles, which is typically 60 to 90 days. They must also confirm receipt of your letter within 30 days.

What happens if you lose a credit card dispute?

The issuer sends you a written explanation of why. The disputed charge goes back on your account, and you’ll have at least 10 days to pay before any late fees or finance charges apply.

Can you dispute a credit card charge after 60 days?

You may lose certain legal protections under the FCBA after 60 days. However, many card issuers still accept disputes beyond that window, especially for fraud. Check with your specific issuer for their policy.

Do you need to send a dispute letter by certified mail?

It’s not legally required, but it’s strongly recommended. Certified mail with a return receipt gives you proof that the issuer received your letter and the exact date they got it.

What is the difference between a billing dispute and a chargeback?

A billing dispute is the formal notice you send to your card issuer about an error. A chargeback is the issuer’s action of reversing the charge and pulling the funds back from the merchant. Your dispute letter is what starts the chargeback process.

Can you dispute a charge if the merchant refuses a refund?

Yes. If the merchant won’t give you a refund for defective goods, undelivered items, or overcharges, you can escalate the issue. Just file a written dispute with your card issuer.

Conclusion

A billing dispute doesn’t have to be stressful. You now know what goes into a written notice, how to fill out the template step by step, and how to send it the right way. The templates provided in this guide cover both US Letter and A4 sizes, in both PDF and Word formats, so you’re ready no matter how you prefer to work.

Based on the protections built into the Fair Credit Billing Act, filing a written dispute is the most effective way to challenge a wrong charge and get your money back. The key is acting fast, being specific, and keeping records of everything.

If you know someone dealing with a mystery charge on their credit card statement, share this guide with them. A free credit card dispute letter template and a clear step-by-step process could save them real money and a lot of frustration.