Used Car Loan Calculator With Credit Score

Estimate your monthly payments, total interest, and see how your credit score impacts your APR.

Vehicle Information

Payment & Fees

Loan Details

Manual APR (%)

How to Use This Calculator

- Enter the vehicle's price and any trade-in value or down payment you have.

- Adjust the sales tax rate for your area.

- Choose your desired loan term in months.

- Use the slider or input box to set your credit score to see an estimated APR.

- Optionally, toggle "Manual APR" to enter a specific interest rate.

- Review your estimated monthly payment and total costs, then download or share your results.

Disclaimer: This calculator is for informational purposes only. The results are estimates based on the information you provide and may not be accurate or applicable to your specific financial situation. The information provided does not constitute financial, legal or tax advice. We do not guarantee the accuracy of the calculations or the applicability of any information. Always consult a qualified financial professional for advice specific to your personal circumstances. Credit card terms, conditions, rates and offers are subject to change by the issuing bank at any time. We are not responsible for any actions or decisions taken based on the information provided by this tool.

Buying a used car is exciting, but figuring out your loan costs can be confusing, especially when your credit score changes everything. Experian’s Q4 2025 data shows that used car APRs range from 7.70% for top-tier borrowers to 21.85% for those with poor credit. That gap can cost you thousands. This used car loan calculator with credit score input helps you see exactly what your number means for your wallet.

Enter your credit score, loan amount, and term, and the tool shows your estimated monthly payment, total interest, and APR in real time.

Read on for a complete guide to how the calculator works. You’ll find the math behind it, expert tips, and real-world examples to help with your next car purchase.

Tip: → New to how your score affects loan terms? The credit score worksheet for students is a great starting point.

What Is a Used Car Loan?

A used car loan is a type of installment loan. It lets you borrow money from a lender to buy a pre-owned vehicle. You repay the loan over a set period, called the loan term, in fixed monthly payments. Each payment covers part of the principal and part of the interest.

Used car loans work a bit differently from new car loans. There are three key differences:

- Higher interest rates: Lenders view used cars as riskier. They’re tough to value and can lose value quickly. That risk gets passed on to you as a higher APR.

- Varied loan terms: Loan terms for used cars typically range from 24 to 84 months. However, lenders may restrict longer terms on older vehicles.

- Lower loan amounts: Used cars cost less than new ones, so loan balances are usually smaller. But, this doesn’t always mean the loan is cheaper when you consider interest.

Who Offers Used Car Financing?

Several types of lenders can fund your used vehicle purchase:

- Banks: Traditional banks offer solid rates, especially for existing account holders.

- Credit unions: Nonprofit lenders known for offering lower APRs than most big banks. Worth checking before anything else.

- Dealership financing: Convenient at the point of sale, but dealer markups on rates are common. Always compare first.

- Online lenders: Fast approvals and competitive rates, particularly for fair-credit borrowers.

How Does Your Credit Score Fit In?

Your credit score tells a lender how risky you are as a borrower. The higher your score, the lower the risk, and the lower your interest rate. Lenders group borrowers into tiers: superprime, prime, nonprime, subprime, and deep subprime. Each tier carries a different APR range.

Experian’s Q4 2025 State of the Automotive Finance Market report shows that used car APRs range from 7.70% for top-tier borrowers to 21.85% for those with poor credit. That gap represents thousands of dollars in extra interest on the same vehicle, with the exact same loan term.

A jump of even 60 to 80 points can move you into a better tier and cut hundreds or even thousands of dollars off your total interest. That’s exactly why it helps to know your score before you walk onto a dealer lot.

How This Calculator Works

This tool gives you a clear, real-time estimate of your used car loan costs. It updates instantly every time you change a field. No submit button required.

Here’s what it takes in and what it gives back:

Inputs the Calculator Uses

| Input | What It Does |

|---|---|

| Car Price | The full purchase price of the used vehicle |

| Trade-In Value | Your current vehicle’s value, which reduces your loan balance directly |

| Down Payment | The cash you pay upfront, which also lowers the amount you borrow |

| Sales Tax (%) | Your local tax rate, applied to the car price before calculating the loan |

| Loan Term | How long you’ll repay the loan: 24, 36, 48, 60, 72, or 84 months |

| Credit Score | Slider or input box ranging from 300 to 850; sets your estimated APR automatically |

| Manual APR (Optional) | Toggle this on if you have a real rate offer from a lender |

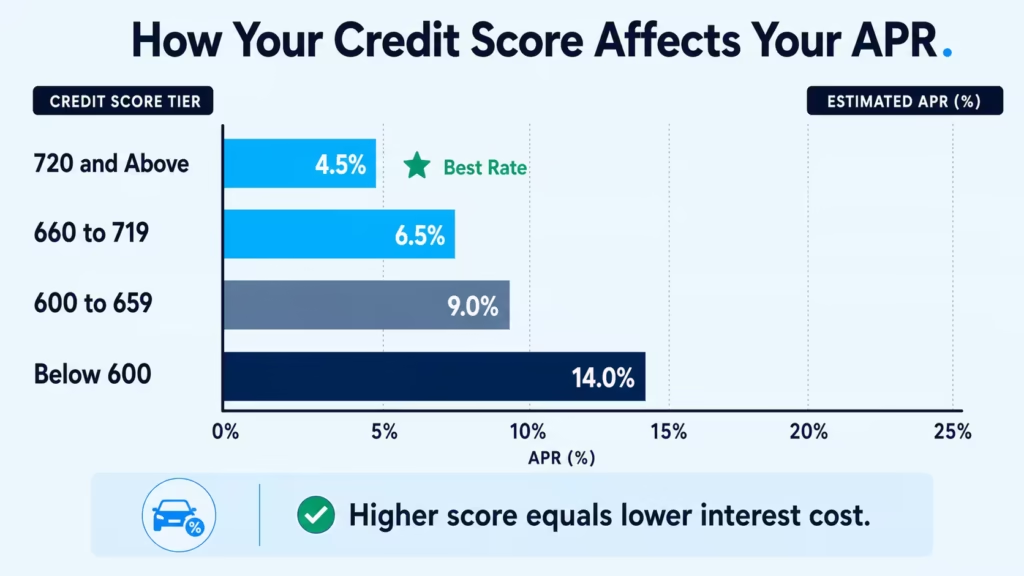

APR Tiers This Calculator Uses

The calculator assigns an estimated APR based on your credit score:

| Credit Score Range | Estimated APR |

|---|---|

| 720 and above | 4.5% |

| 660 to 719 | 6.5% |

| 600 to 659 | 9.0% |

| Below 600 | 14.0% |

📌 Did You Know: These APR tiers are designed for quick estimates, not exact lender quotes. Experian’s State of the Automotive Finance Market report shows that real-world used car APRs run significantly higher: prime borrowers (661-780) averaged 9.06%, and subprime borrowers (501-600) averaged 18.99% in Q1 2025. If you have an actual rate offer from a lender, use the Manual APR toggle for a more accurate result.

What the Calculator Shows You

Once you fill in the inputs, you’ll see all of this update instantly:

- Monthly Payment: Your fixed cost each month for the life of the loan

- Total Interest Paid: The extra you’ll pay above the loan principal

- Total Loan Cost: Principal plus all interest combined

- Loan Amount: What you’re actually borrowing, after tax, down payment, and trade-in

- Estimated APR: The rate used in the calculation

- Donut Chart: A visual split between principal and interest

- Smart Insight: A personalized message based on where your credit score lands

- PDF Export and Social Sharing: Download your results or share them on Facebook, WhatsApp, X, or Reddit

The Formula Explained

Every number this calculator produces comes from a standard financial formula. Here’s the full breakdown, step by step.

Step 1: Total Car Cost with Sales Tax

The calculator starts by adding your local sales tax to the car’s purchase price.

Total Car Cost = Car Price x (1 + Sales Tax Rate / 100)

Example: A car priced at $18,500 with a 7.5% sales tax:

Total Car Cost = $18,500 x 1.075 = $19,887.50

Step 2: Loan Amount

Next, it subtracts your down payment and trade-in value from the total car cost.

Loan Amount = Total Car Cost – Down Payment – Trade-In Value

Example: With $2,000 down and a $1,500 trade-in:

Loan Amount = $19,887.50 – $2,000 – $1,500 = $16,387.50

This is the actual principal you’ll be borrowing.

Step 3: APR Assignment

If the manual toggle is off, the calculator assigns your APR based on which credit score tier you fall into. If you toggle manual APR on, it uses the rate you enter directly. The manual APR is capped at 25% to prevent unrealistic inputs.

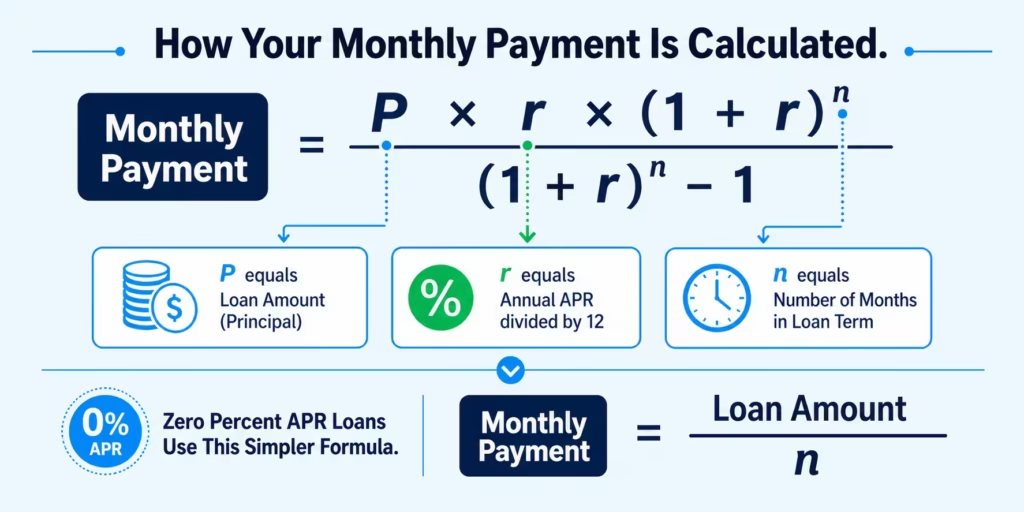

Step 4: Monthly Payment Calculation (The PMT Formula)

This is the core formula used in all standard loan amortization:

Monthly Payment = P x [r x (1 + r)^n] / [(1 + r)^n – 1]

Where:

- P = Loan Amount (principal)

- r = Monthly Interest Rate = Annual APR / 100 / 12

- n = Number of months (loan term)

For a 0% APR loan, the formula simplifies to:

Monthly Payment = Loan Amount / n

Step 5: Total Cost and Total Interest

Total Cost = Monthly Payment x Number of Months

Total Interest = Total Cost – Loan Amount

These two figures together give you the real cost of the loan. The total interest is what the financing actually costs you on top of the car’s price.

💡 Pro Tip: Try running the calculator twice, once with your current credit score and once with a score that’s 50 to 60 points higher. Even a modest improvement in your score can drop your APR by a full percentage point or more, which adds up to real savings over a 48 to 60-month term.

How to Use This Calculator (Step by Step)

Follow these steps to get the most accurate estimate possible:

Step 1: Enter the Vehicle’s Price.

Type in the car’s asking price. Avoid adding tax manually. The calculator handles the tax calculation on its own in a separate field.

Step 2: Add Your Trade-In Value (Optional)

If you’re trading in a car, enter what it’s worth. Even a modest trade-in reduces your loan amount, which directly lowers your monthly payment and total interest.

Step 3: Enter Your Down Payment.

Enter the cash amount you plan to put down upfront. A bigger down payment means a smaller loan, which means less interest overall.

Step 4: Set Your Sales Tax Rate.

Look up your state’s sales tax rate and enter it as a percentage. This gets folded into the car’s total cost before your down payment, and trade-ins are subtracted.

Step 5: Choose Your Loan Term.

Select how many months you want to repay the loan. Options include 24, 36, 48, 60, 72, and 84 months. Shorter terms carry higher monthly payments but much lower total interest.

Step 6: Enter Your Credit Score.

Drag the slider or type your score into the number field. The calculator assigns an estimated APR from the built-in tier table and updates all results automatically.

Optional Step: Toggle Manual APR.

Already have a rate offer in hand? Flip the Manual APR switch and type in the exact rate. This replaces the estimated APR with your real offer, giving you a more precise calculation.

Final Step: Review and Export.

Check your monthly payment, total interest, and the donut chart. If the numbers work, download a PDF of your results or share them with a co-signer or family member using the built-in share buttons.

How to Read Your Results

Each result the calculator displays tells you something different. Here’s what to pay attention to and why it matters.

Monthly Payment

This is your fixed payment amount each month. It includes both principal and interest. A lower monthly payment might feel like a win, but it often comes from a longer loan term, which means more total interest paid over time. Don’t treat the monthly number as the only measure of a good deal.

Total Interest Paid

This is the true cost of borrowing. It’s the extra money you’ll hand over to the lender, on top of the car’s purchase price. A higher APR or a longer loan term pushes this number up fast. Comparing the total interest between the two loan scenarios gives you a clearer picture than the monthly payment alone.

Total Loan Cost

This adds your loan principal and total interest together. It shows the full amount you’ll repay to the lender from the first payment to the last. Think of this as the real price tag on the car once financing is factored in.

Loan Amount (Principal)

This is what you’re actually borrowing: the car price plus tax, minus your down payment and trade-in. Lowering this number, by increasing your down payment or trade-in value, is one of the most effective ways to reduce your total interest paid.

Estimated APR

This is the annual percentage rate used in the calculation. In auto-assign mode, it’s an estimate based on your credit score tier. In manual mode, it reflects the actual rate you entered. This single number has more influence on your total cost than almost any other input.

The Donut Chart

The chart splits your total loan cost into two sections: principal (blue) and total interest (yellow). If the yellow section is close to the same size as the blue section, or larger, your APR or loan term deserves a second look. Ideally, you want the yellow slice to be as small as possible.

Smart Insight Message

The calculator generates a personalized message below the chart. A score below 660 triggers a note about how improving your credit could reduce your interest. A score between 660 and 719 confirms you’re in a competitive range. A score of 720 or above gets a message confirming you’re well-positioned for a strong rate.

⚠️ Mistake to Avoid: Never finalize a car acquisition based only on the monthly payment. Two different loans can produce the exact same monthly payment but differ by thousands of dollars in total interest. Always compare both the monthly payment and the total loan cost before you decide.

Real-World Example

Here’s how a real scenario plays out using the calculator’s math.

Meet Marcus, a 34-year-old electrician from Dallas, Texas. He’s shopping for a certified pre-owned 2022 Honda Accord priced at $18,500.

His numbers:

| Input | Marcus’s Values |

|---|---|

| Car Price | $18,500 |

| Down Payment | $2,500 |

| Trade-In Value | $1,500 |

| Sales Tax | 6.25% (Texas rate) |

| Loan Term | 60 months |

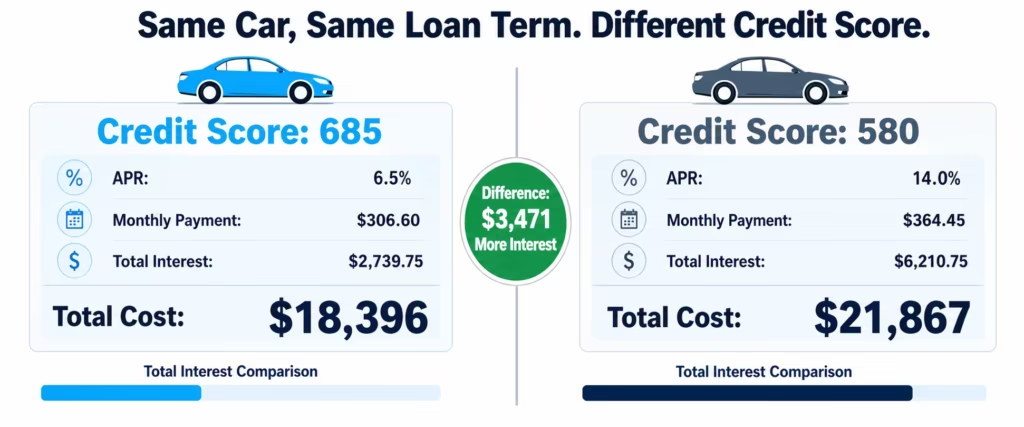

| Credit Score | 685 |

Calculation Walkthrough:

Total Car Cost = $18,500 x 1.0625 = $19,656.25

Loan Amount = $19,656.25 – $2,500 – $1,500 = $15,656.25

APR = Score of 685 falls in the 660-719 tier, so APR = 6.5%

Monthly Rate = 6.5% / 12 = 0.5417% (0.005417)

Monthly Payment Calculation:

Monthly Payment = $15,656.25 x [0.005417 x (1.005417)^60] / [(1.005417)^60 – 1]

(1.005417)^60 = approximately 1.3829

= $15,656.25 x (0.007492 / 0.3829)

= $15,656.25 x 0.019571

= $306.60 per month

Total Cost = $306.60 x 60 = $18,396

Total Interest Paid = $18,396 – $15,656.25 = $2,739.75

Now let’s see what happens if Marcus’s score drops to 580.

A score of 580 falls into the under-600 tier, pushing the APR to 14.0%.

Monthly Rate = 14% / 12 = 1.1667% (0.011667)

(1.011667)^60 = approximately 2.0057

Monthly Payment = $15,656.25 x [0.011667 x 2.0057] / [2.0057 – 1]

= $15,656.25 x (0.023400 / 1.0057)

= $15,656.25 x 0.023268

= $364.45 per month

Total Cost = $364.45 x 60 = $21,867

Total Interest Paid = $21,867 – $15,656.25 = $6,210.75

The bottom line: The only thing that changed was Marcus’s credit score. Yet the lower score costs him an extra $3,471 in total interest on the same vehicle, with the same down payment and loan term. That’s the real-world cost of a weaker credit profile.

Expert Tips and Insights

These strategies can help you lock in a better rate and lower your total cost before you finance a single dollar.

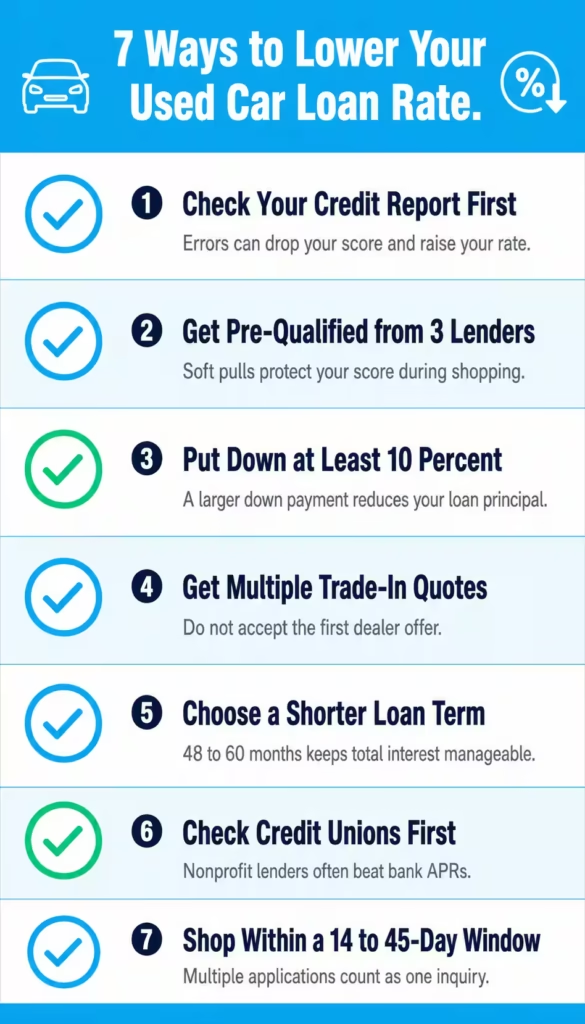

1. Check Your Credit Report Before You Apply

Pull your free credit report at AnnualCreditReport.com before you start shopping. Look for errors, such as accounts that aren’t yours or incorrect late payment records. Disputing and removing errors is free and can push your score up meaningfully. Even a 20-point gain can shift you into a lower APR tier.

2. Get Pre-Qualified from Multiple Lenders First

Pre-qualification uses a soft credit pull, which doesn’t affect your score. Collect rate estimates from at least three sources: a bank, a credit union, and an online lender. Then enter those actual rates into the Manual APR toggle to compare your real options side by side.

3. Bring a Larger Down Payment

Putting more cash down upfront shrinks your loan principal. A smaller principal means less interest, a lower monthly payment, and less risk of going underwater on the loan. The standard guidance in auto finance is to put down at least 10% on a used car. If you can reach 20%, you’ll be in a strong position.

4. Get Multiple Trade-In Quotes

Your trade-in is worth real money. Don’t accept the first estimate a dealer gives you. Get quotes from at least two or three sources, including CarMax or Carvana, which provide instant online offers. Use the highest quote as a baseline in your negotiation.

5. Favor Shorter Loan Terms

A 72 or 84-month loan can feel appealing because the monthly payment looks lower. Those extra months can raise your total interest a lot. But they also make it more likely that you’ll owe more than the car’s value halfway through the term. A 48 or 60-month loan is a smarter balance for most buyers.

6. Look at Credit Unions First

Credit unions are nonprofit financial cooperatives. They typically offer lower auto loan APRs than commercial banks because they return profits to members rather than shareholders. Bankrate’s analysis of auto loan interest rates consistently shows that credit unions offer some of the most competitive used car financing rates available. Many credit unions let you join online with minimal requirements.

7. Keep All Applications Within a 14 to 45-Day Window

Each formal loan application triggers a hard inquiry on your credit report. Too many hard inquiries in a short period can drop your score. The good news: most scoring models treat all auto loan inquiries made within a 14 to 45-day window as a single inquiry. So shop aggressively, but do it within that window.

Common Mistakes to Avoid

Smart buyers still fall into these traps. Knowing them in advance keeps you from making an expensive error.

Focusing Only on the Monthly Payment

This is the single most common financing mistake. A dealer can stretch your loan to 72 or 84 months to bring the monthly payment down, but the total interest you pay will be much higher. Jessica, a first-time car buyer from Phoenix, financed a $16,000 Honda at 9% APR over 84 months. Her payment was $252 per month, which felt manageable, but she paid over $5,200 in total interest. On a 48-month term, she would have paid $2,900 in interest. Always look at the total loan cost alongside the monthly figure.

Forgetting to Factor In Sales Tax

Sales tax adds directly to your loan balance if you roll it into the financing. A $17,000 car in a state with 8% sales tax costs $18,360 before your down payment is applied. Ignoring that number leaves you underestimating your true loan amount. Use the sales tax field in the calculator to see what your real balance looks like.

Skipping the Trade-In Comparison

Some dealers offer below-market trade-in values and bundle them into a confusing package deal. Get your car appraised separately before you step into the dealership. Treat the trade-in and the car purchase as two independent transactions.

Not Reviewing Your Credit Report for Errors First

Errors on credit reports are more common than most people realize. The Consumer Financial Protection Bureau (CFPB) notes that consumers have the right to dispute inaccurate information on their reports for free. An error that drops your score by 30 points could push you into a higher APR tier and cost you thousands of dollars. Checking before you apply takes less than 10 minutes.

Accepting the First Financing Offer

Dealer financing is often marked up above the lender’s base rate. The dealership profits from the difference. Always have at least one outside loan offer in hand when you negotiate. It gives you real leverage and a clear benchmark to compare against.

⚠️ Mistake to Avoid: Always read the full loan agreement before you sign. Watch for prepayment penalty clauses. Some lenders charge a fee for paying off your loan early. If you plan to make extra payments or pay off the loan ahead of schedule, a prepayment penalty can cut those savings entirely.

Frequently Asked Questions (FAQs)

What credit score do I need to get a used car loan?

Most lenders approve used car loans for borrowers with scores of 601 or higher. In Q3 2025, the average credit score for used car financing was 691, based on data from Experian. Some specialty lenders work with scores below 601, but at much higher APRs.

How does my credit score affect my used car loan interest rate?

Your score places you in a specific APR tier. Borrowers with scores of 781 or higher averaged 7.70% on used car loans, while those with scores below 500 averaged 21.85%, per Experian’s Q4 2025 data. That difference can add thousands of dollars in interest on the same loan amount.

Can I get a used car loan with bad credit?

Yes. Many lenders specialize in subprime auto financing for borrowers with scores below 600. Expect a higher APR, which increases both your monthly payment and total interest. A larger down payment or a strong trade-in can offset some of that cost.

What is a good APR for a used car loan right now?

Anything below 10% is considered competitive for used car financing in 2025. Prime borrowers with scores from 661 to 780 averaged 9.06% APR on used vehicles in Q1 2025, according to Experian. Superprime borrowers can secure rates closer to 6.82%.

How much should I put down on a used car?

Auto finance professionals generally recommend at least 10% of the vehicle’s purchase price as a down payment. Getting to 20% gives you more equity from day one, lowers your monthly payment, and reduces the chance of owing more than the car is worth during the loan.

Does getting pre-approved for a car loan hurt my credit score?

Pre-qualification uses a soft credit pull and does not affect your score. A full application triggers a hard inquiry, which can reduce your score by a few points temporarily. Rate shopping with multiple lenders within a 14 to 45-day window is typically treated as one inquiry by most credit scoring models.

How long are typical used car loan terms?

Experian Q3 2025 data shows the average used car loan term is 67.43 months, or just over 5.5 years. This calculator offers terms from 24 to 84 months. Most financial experts suggest keeping your term at 60 months or less to manage total interest costs.

Can I refinance my used car loan to get a lower rate later?

Yes. If your credit score improves significantly after your original loan, refinancing can lower your APR and monthly payment. The biggest savings come when your score rises by at least 50 to 100 points. Check for prepayment penalties on your current loan before refinancing.

What is the difference between the interest rate and APR on a car loan?

The interest rate is the basic cost of borrowing. APR includes the interest rate plus any additional lender fees, giving a more complete view of the loan’s total cost. When comparing multiple loan offers, always use the APR as your primary comparison point.

How do I calculate my used car loan payment by hand?

Use this formula: Monthly Payment = P x [r x (1 + r)^n] / [(1 + r)^n – 1], where P is the loan amount, r is the monthly rate (annual APR divided by 1,200), and n is the number of months. Or skip the math and use this calculator for instant results.

Bottom Line

Understanding your true loan cost before you sign is one of the smartest moves you can make as a car buyer. This guide covered how credit score tiers influence your APR. It explained how the PMT formula drives every payment estimate. You learned to account for sales tax and trade-in value. It showed how to read your results in a way that enhances understanding.

My personal recommendation: use this used car loan calculator with credit score inputs to run at least two scenarios before heading to the dealership. Compare your current score with what a 50-point improvement would look like. The difference might be exactly the motivation you need.

If this guide helped you, share it on social media with a friend or family member who’s shopping for a used car right now.