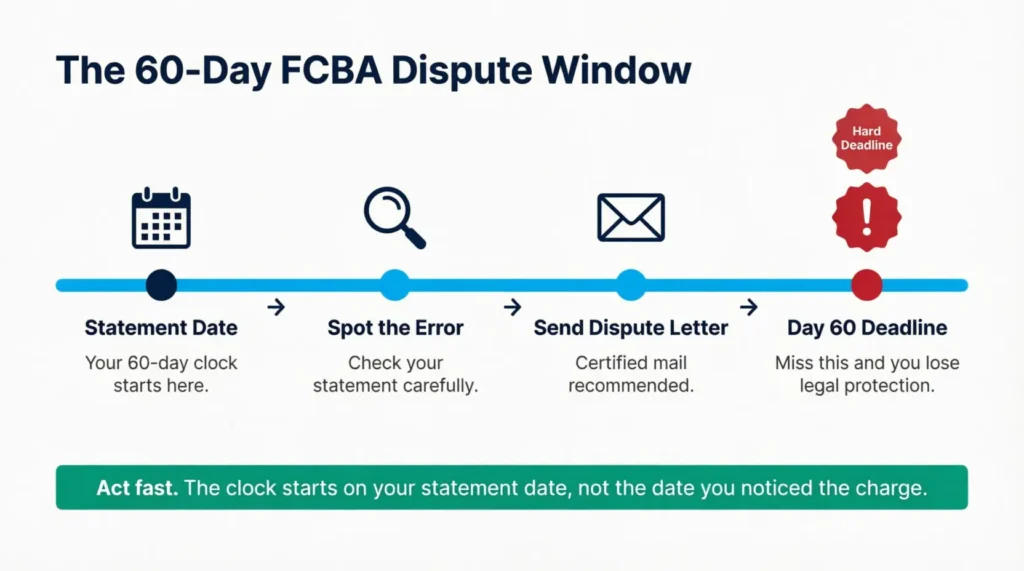

Seeing an unfamiliar charge on your credit card statement is unsettling. It could be a billing error, a duplicate transaction, or a fraudulent charge you never made. What many cardholders don’t realize is that the Fair Credit Billing Act gives you just 60 days from your statement date to take formal action

A well-crafted dispute credit card charge letter puts your complaint on record and legally requires your card issuer to investigate.

The fastest way to fix a billing error is to send a formal written dispute directly to your card issuer.

This guide includes everything you need. It has free templates to download. You’ll find a step-by-step guide for filling them out. It also covers your legal rights clearly. Plus, there are practical tips to help your dispute succeed.

Download Your Free Dispute Credit Card Charge Letter Templates

Three ready-to-use templates are available below. Each one includes every section your bank or card issuer expects to see, saving you time and guesswork.

Pick the format and paper size that works best for you:

Disclaimer: The Templates & Printables on this site are provided for informational and personal tracking purposes only. This is not financial, legal, tax, or credit advice. While reasonable efforts are made to ensure accuracy, Credit Card Wind makes no warranties as to the completeness, reliability, or accuracy of the calculations generated by these Templates & Printables. Users are responsible for independently verifying all data and calculations. Terms, conditions, rates, regulations, and legal requirements vary by institution, jurisdiction, and individual circumstances.

Always refer to your official statements, account agreements, and applicable laws, and consult a qualified professional before making any financial, legal, or other important decisions. By using these Templates & Printables, you acknowledge that Credit Card Wind and its owner shall not be liable for any damages, losses, or financial consequences arising from the use or misuse of these Templates & Printables.

This universal disclaimer applies to all templates and printables provided by Credit Card Wind (https://creditcardwind.com), created by Robert Williams (Owner at Credit Card Wind).

© Credit Card Wind. All rights reserved.

These templates and printables may be downloaded and used for personal, non-commercial purposes only. Redistribution, resale, or modification for commercial use without permission is strictly prohibited.

What Is a Credit Card Charge Dispute Letter?

A credit card charge dispute letter is a written notice you send to your bank or card issuer to formally challenge a transaction on your statement. It’s your official record that a problem has been reported, and it triggers a legal investigation process.

Under the Fair Credit Billing Act, card issuers are required by federal law to acknowledge your written dispute within 30 days of receiving it, and to resolve it within two billing cycles (but no longer than 90 days). Without a written record, you have no legal protection.

This isn’t only about making polite requests. A formal letter creates a paper trail. If the dispute isn’t resolved in your favor, that paper trail becomes evidence you can use to escalate the matter.

📌 Did You Know: The Fair Credit Billing Act only covers billing errors, not disputes about product quality or satisfaction. For quality-related complaints, your card network’s chargeback process may be a better route.

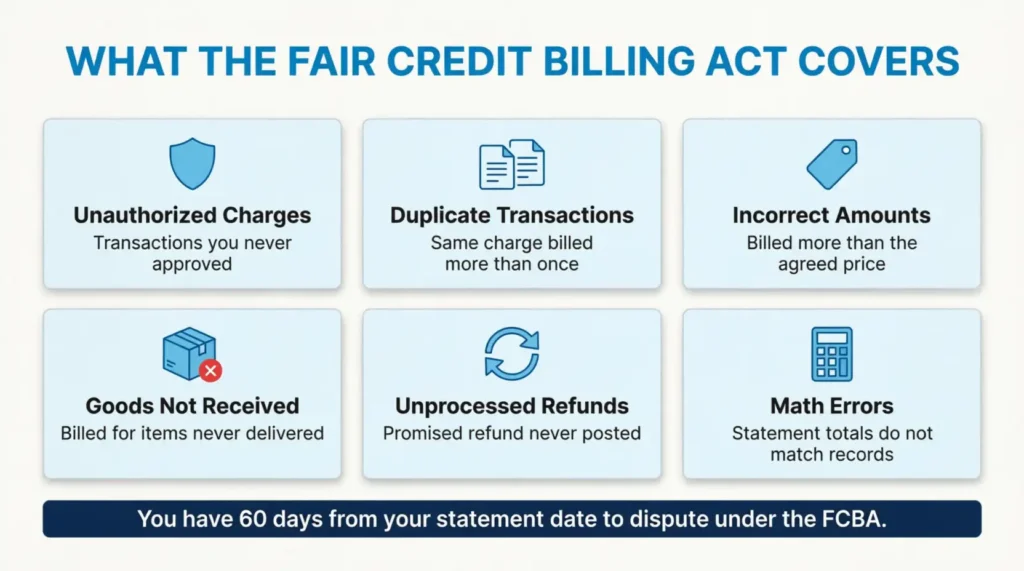

Your Legal Right to Dispute: What the Fair Credit Billing Act Covers

The Fair Credit Billing Act (FCBA) is a federal consumer protection law that shields cardholders from billing errors on credit card statements. It is enforced by the Consumer Financial Protection Bureau (CFPB) and the Federal Trade Commission (FTC).

Under the FCBA, you have the right to dispute the following types of charges:

- Unauthorized charges: Transactions you never approved or made

- Incorrect amounts: The merchant billed you more than the agreed price

- Duplicate transactions: The same charge appeared more than once

- Services or goods not received: You were billed for something that was never delivered

- Unprocessed returns or cancellations: A refund was promised but never posted to your account

- Math or calculation errors: Mistakes on your statement that don’t match your records

The FCBA sets a strict 60-day window. Your written dispute must be sent within 60 days of the billing statement date that shows the error. Miss that deadline and you could lose your legal right to challenge the charge.

One important distinction: the FCBA covers billing errors only. If you received what you paid for but were simply unhappy with it, the FCBA doesn’t apply. In that case, your card network’s chargeback process or a direct refund request from the merchant are your next best options.

⚠️ Mistake to Avoid: Don’t wait and hope the charge corrects itself. Many cardholders lose their right to dispute because they missed the 60-day window by just a few weeks. Act as soon as you spot a problem.

When Should You Send a Billing Dispute Letter?

Not every billing problem needs a formal written complaint. But in these situations, sending a dispute letter is the right move.

Send a written billing dispute when:

- A charge appears on your statement that you never authorized

- You returned a product but the refund never posted to your account

- A merchant charged you twice for the same acquisition

- You canceled a subscription but billing continued past the cancellation date

- A service was never delivered despite being billed

- The charged amount doesn’t match your receipt

- You suspect fraudulent activity on your account

A good starting point is to contact the merchant directly first. Many disputes get resolved quickly at the merchant level. Trying this step first shows good faith. If the merchant doesn’t cooperate or reply in time, the next step is to escalate to a formal written dispute with your card issuer.

Take Marcus, a freelance designer from Ohio, as an example. He noticed a $149 charge from a software company two weeks after he canceled his subscription. After not hearing back from the merchant, Marcus wrote to his card issuer. He attached his cancellation email. Then, he got a full credit to his account in 42 days.

Tip: → If the disputed charge is a fee, confirm whether it was applied correctly with the credit card fee calculator.

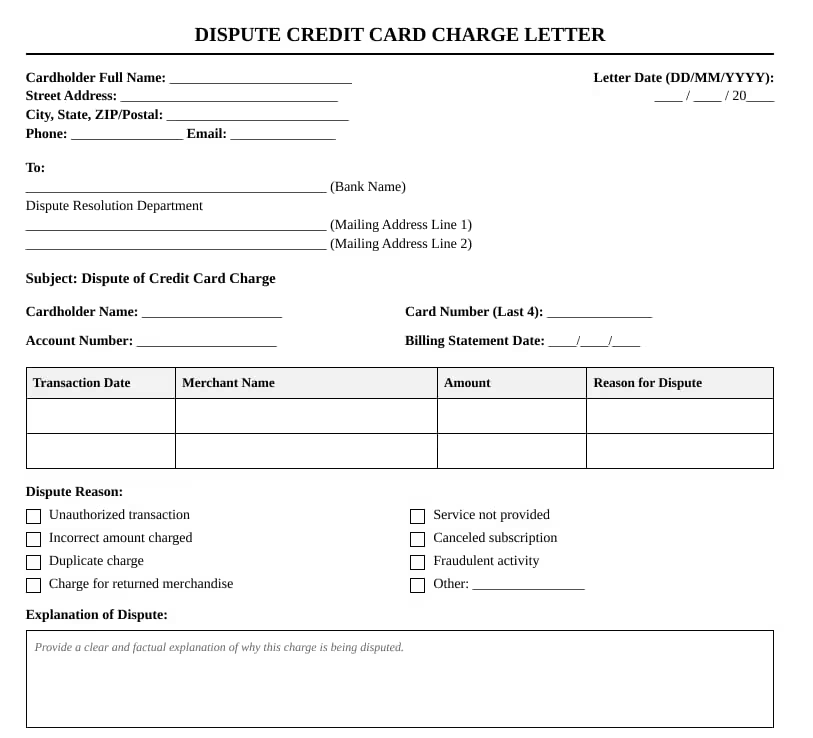

How to Fill Out Your Dispute Letter Template (Step by Step)

The templates provided above have several key sections. Each one plays a specific role in making your dispute clear, complete, and credible. Complete each part by following these steps carefully.

Step 1: Add Your Personal Information

Write your full legal name, mailing address, phone number, and email address at the top. Use the exact name associated with your credit card account.

Step 2: Add the Date

Write the current date at the top of the letter. This establishes your submission timeline and is important for proving that you acted within the 60-day legal window.

Step 3: Address the Card Issuer

Write the full name of your bank or credit card company. Address the letter specifically to the Billing Inquiries Department or Dispute Resolution Department. Most card issuers have a separate mailing address for written disputes. This address is different from their general customer service address. Check the back of your monthly billing statement or your card issuer’s website to confirm the correct address.

💡 Pro Tip: Many card issuers print their designated dispute mailing address directly on the back of your monthly statement. Always use that address. Sending your letter to a general customer service address can delay processing or result in it being misrouted entirely.

Step 4: Fill In Your Account Details

Record your name as it appears on the card, the last 4 digits of your card number, and the relevant billing statement date. Never write your full 16-digit card number on the letter. The last 4 digits are enough to identify your account.

Step 5: List the Disputed Transaction

Use the table in the template to record the transaction details. For each disputed charge, include:

- The exact transaction date

- The merchant’s full name

- The amount charged

- Your reason for disputing it

Be specific here. “I did not authorize this charge” is clear and direct. “There was a problem with my account” is too vague to be useful.

Step 6: Select Your Dispute Category

Check the box that best describes the type of error. The template includes common categories such as unauthorized charge, duplicate transaction, returned merchandise not credited, and suspected fraudulent activity. If none of the listed categories apply, use the “Other” field and briefly describe the issue in your own words.

Step 7: Write Your Explanation

This is the most important section of the letter. In the explanation field, describe what happened in plain, factual language. Include:

- When you first noticed the charge

- Why do you believe it is incorrect

- Any steps already taken to resolve it with the merchant

- Dates of relevant calls or emails with the merchant

Stick to the facts. Emotional language doesn’t strengthen a dispute. Clear, documented facts do.

Step 8: State Your Requested Resolution

Tell the card issuer exactly what outcome you are seeking. Common options include a full refund, a partial refund, a charge reversal, or an account correction. Select the one that fits your situation.

Step 9: Attach Supporting Documents

Check every box in the supporting documents section that matches what you are enclosing. Common attachments include:

- A copy of your billing statement with the disputed charge highlighted

- A receipt or invoice showing the correct amount

- Proof of return or cancellation confirmation

- Emails or letters exchanged with the merchant

Always send copies, never originals. Keep the originals in your personal records.

Step 10: Sign and Date the Letter

Sign your name clearly in the signature section and print your full name below it. Add the date next to your signature. An unsigned dispute letter is often returned unprocessed, so double-check this before sealing the envelope.

How to Send Your Dispute Letter to the Card Issuer

Filling out the template is only half the job. How you deliver it matters as much.

The Recommended Method: Certified Mail

Send your letter through USPS Certified Mail with a return receipt requested. This gives you three key pieces of evidence:

- Proof that you mailed the letter on a specific date

- Delivery confirmation with the exact date it arrived

- A signed receipt acknowledging that the card issuer received it

Keep the mailing receipt. It’s your proof that you submitted the dispute within the 60-day legal window.

Online and App-Based Disputes

Many card issuers now accept disputes through their website or mobile app. These are faster and more convenient, but they may not provide the same level of documented proof as a physical certified letter.

If you choose the digital route, take screenshots of your submission confirmation and save any confirmation emails you receive. This creates a digital paper trail that works in a similar way.

The CFPB advises consumers to keep copies of all dispute correspondence, regardless of the delivery method used. Always keep a copy of the letter for your personal records before it leaves your hands.

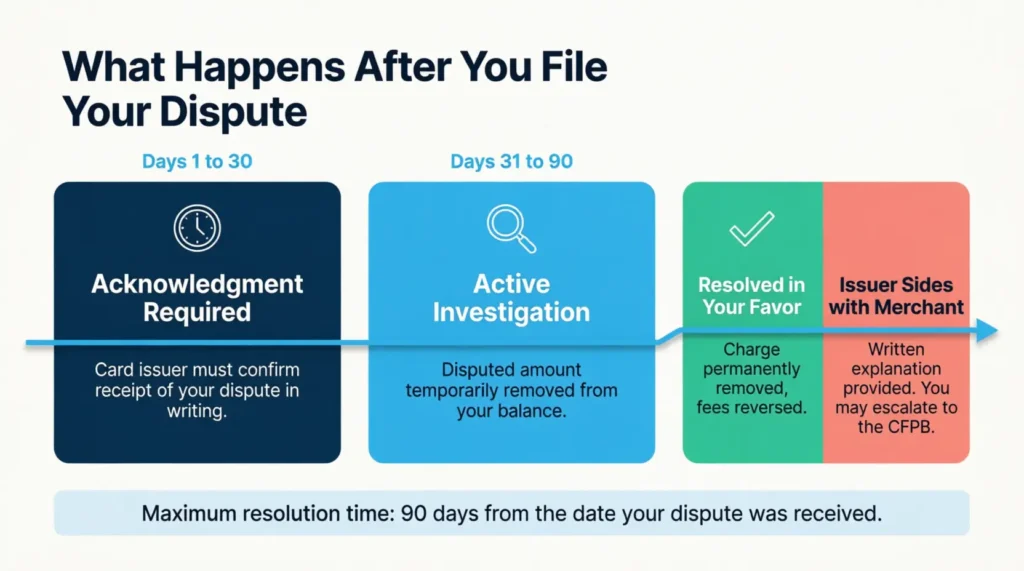

What Happens After You Submit Your Dispute?

Once your card issuer receives the written complaint, a legally required timeline kicks into effect.

Days 1 to 30: Acknowledgment

The card issuer must acknowledge your dispute in writing within 30 days of receiving it. This is a federal requirement under the FCBA. If you don’t receive an acknowledgment within that timeframe, send a follow-up letter immediately.

Days 31 to 90: Investigation

The issuer investigates the disputed charge. During this period, the disputed amount is typically removed from your balance temporarily. You don’t have to pay the disputed amount during the investigation. However, you must still pay the rest of your bill on time.

The Final Resolution

The card issuer must complete its investigation within two billing cycles, and never more than 90 days from the date they received your dispute. After the investigation, you will receive a written explanation of their decision.

If the dispute is resolved in your favor, the charge is permanently removed and any related interest or fees are reversed.

If the issuer sides with the merchant, they are required to explain their reasoning in writing. You then have the right to request the supporting documents they used to reach that conclusion.

⚠️ Mistake to Avoid: Some cardholders stop paying their entire credit card bill during a dispute. Don’t do this. The FCBA only allows you to withhold the disputed amount. Withholding other payments can trigger late fees and hurt your credit score.

Tips to Strengthen Your Credit Card Dispute

A well-documented dispute is far more likely to succeed. These practical tips can make a real difference in the outcome.

Gather evidence before writing the letter.

Grab your billing statement, receipts, email confirmations, and any messages from the merchant before you start writing. The stronger your supporting documents, the harder it is for the issuer to dismiss your claim.

Describe the situation with specifics.

Use exact dates, transaction amounts, and merchant names throughout your letter. Vague language weakens your case. Compare the charged amount to the receipt or booking confirmation you have on file.

Try the merchant first, but document everything.

Attempting a resolution with the merchant directly before escalating is good practice. If they don’t cooperate, note the dates and outcomes of those attempts in your dispute letter.

Follow up in writing if needed.

If you don’t receive an acknowledgment within 30 days, send a follow-up letter immediately. Keep a written record of all communications. Write down the dates, times, and names of any representatives you spoke with.

Escalate to the CFPB if necessary.

If your card issuer dismisses a valid billing dispute, you can file a formal complaint through the CFPB’s complaint portal. The CFPB contacts companies directly on your behalf and tracks their responses publicly.

Common Mistakes That Get Disputes Rejected

Even a completely valid billing complaint can be denied if the letter is incomplete or submitted incorrectly. These are the most common errors cardholders make.

Missing the 60-day deadline.

The clock starts from your billing statement date, not the date you noticed the charge. Check your statements carefully and act without delay when something looks wrong.

Disputing the wrong type of charge.

A formal billing dispute under the FCBA applies to billing errors only. If you received the product or service but were unhappy with it, that’s not a billing error. Your card network’s chargeback process may be more appropriate in that scenario.

Sending the letter to the wrong address.

\Always use the specific address designated for billing disputes. Sending it to a general customer service address might misroute your letter. This can delay or even invalidate your dispute.

Not attaching supporting documents.

A letter with no evidence leaves your issuer with very little to work with. Attach relevant copies of receipts, statements, return confirmations, and merchant correspondence. Again, copies only, not originals.

Leaving the signature or date blank.

An unsigned or undated letter is commonly returned unprocessed. It’s a small detail, but it can set you back by weeks.

Frequently Asked Questions

How long do I have to dispute a credit card charge?

Under the Fair Credit Billing Act, you have 60 days from the date on the billing statement that shows the error. Missing this window can remove your legal right to challenge the charge.

Can I dispute a credit card charge online instead of sending a physical letter?

Yes, most card issuers accept disputes through their website or mobile app. For larger or more complex disputes, a physical letter sent via certified mail provides stronger documentation and legal protection.

Does filing a billing dispute affect my credit score?

No. Submitting a dispute does not directly affect your credit score. However, failing to pay the undisputed part of your bill during the investigation period can result in late fees and score damage.

What if my dispute is denied?

The card issuer must provide a written explanation of the denial. You can request the documents they used in their decision and, if the denial seems unjustified, file a complaint with the Consumer Financial Protection Bureau.

Do I need a lawyer to dispute a credit card charge?

No. Most billing disputes are resolved without legal help. A lawyer is usually needed for big cases or complex fraud. These cases often go beyond the usual dispute process.

Can I dispute a charge for goods or services I never received?

Yes. If you were billed for something that was never delivered, that qualifies as a billing error under the Fair Credit Billing Act and can be formally disputed.

How long does the credit card dispute investigation take?

The card issuer must resolve your dispute within two billing cycles, and no later than 90 days from the date they received your written dispute.

Is there a minimum dollar amount required to file a dispute?

The Fair Credit Billing Act does not set a smallest dollar threshold. For very small amounts, contacting the merchant directly may be faster, but there is no legal barrier to disputing any charge.

What supporting documents should I include with my dispute letter?

Please attach copies of your billing statement with the disputed charge highlighted. Include any receipts or invoices that show the correct amount. Also, add proof of cancellation or return, and any email or written communication with the merchant.

Can a merchant re-bill me after a successful dispute?

A merchant can attempt to re-bill after a dispute, but your card issuer must notify you before reinstating the charge. You retain the right to dispute again if you believe the re-billing is incorrect.

Bottom Line

Disputing a billing error is a straightforward process when you know your rights and follow the correct steps. The Fair Credit Billing Act gives cardholders a clear legal path to challenge unauthorized charges, duplicate transactions, and other billing mistakes.

The key actions are easy:

- Gather your evidence.

- Fill out your dispute letter fully and accurately.

- Send it by certified mail within 60 days.

- Follow up if needed.

A complete, factual, well-documented dispute credit card charge letter gives your case the best possible chance of a successful outcome. If you know someone who has been hit with an incorrect or suspicious charge, share this guide with them. It could save them real money and a lot of frustration.