Getting denied for a loan or apartment without knowing why is frustrating. Many consumers don’t realize their credit score was already used in that decision.

According to FICO, over 90% of top U.S. lenders use credit scores to evaluate applications. A credit score disclosure form is the legal document that makes this information transparent.

This notice formally informs a consumer which score was used, which bureau provided it, and how it influenced the outcome.

Keep reading for free downloadable templates, a full breakdown of all six sections, and a step-by-step guide to completing the form without errors.

Download Your Free Credit Score Disclosure Form Templates

Three ready-to-use templates are available to make the process easier. Each one includes all the sections required for a complete and compliant disclosure.

Pick the format and paper size that works best for you:

Disclaimer: The Templates & Printables on this site are provided for informational and personal tracking purposes only. This is not financial, legal, tax, or credit advice. While reasonable efforts are made to ensure accuracy, Credit Card Wind makes no warranties as to the completeness, reliability, or accuracy of the calculations generated by these Templates & Printables. Users are responsible for independently verifying all data and calculations. Terms, conditions, rates, regulations, and legal requirements vary by institution, jurisdiction, and individual circumstances.

Always refer to your official statements, account agreements, and applicable laws, and consult a qualified professional before making any financial, legal, or other important decisions. By using these Templates & Printables, you acknowledge that Credit Card Wind and its owner shall not be liable for any damages, losses, or financial consequences arising from the use or misuse of these Templates & Printables.

This universal disclaimer applies to all templates and printables provided by Credit Card Wind (https://creditcardwind.com), created by Robert Williams (Owner at Credit Card Wind).

© Credit Card Wind. All rights reserved.

These templates and printables may be downloaded and used for personal, non-commercial purposes only. Redistribution, resale, or modification for commercial use without permission is strictly prohibited.

What Is a Credit Score Disclosure Notice?

A credit score disclosure notice is a legal document that a lender, landlord, or creditor provides to a consumer. It tells the person that their credit score was checked from a consumer reporting agency. This score was used to check their application.

The document includes six important details:

- The numeric score

- The full scoring range

- The bureau that provided the score

- The scoring model used (like FICO or VantageScore)

- The date the score was obtained

This isn’t a courtesy gesture. FICO data shows that over 90% of top U.S. lenders use FICO Scores when making credit decisions. That means millions of Americans are evaluated using a single number they often never see unless it’s properly disclosed.

📌 Did You Know: Two of the most widely used scoring models are FICO and VantageScore, but specific versions vary by lender. The “Scoring Model Used” field on the form tells a consumer exactly which version was applied to their file, so they can cross-reference it with scores from other platforms.

Who Is Required to Provide a Credit Score Disclosure?

Not every business that checks a credit score must issue a formal disclosure. The requirement depends on the type of transaction and applicable federal rules.

Lenders and creditors are the most common issuers. This group includes banks, credit unions, mortgage companies, and auto lenders. When a credit score plays a role in the lending decision, disclosure to the consumer is required under federal law.

Landlords who check credit scores for rental applications may need to provide a disclosure. This is especially important if they deny the application or offer worse terms due to the score.

Employers using consumer reports for hiring decisions must follow Fair Credit Reporting Act authorization and disclosure rules. The requirements for employment-based checks differ slightly from those for credit transactions, but the obligation to inform the consumer still applies.

The general principle: any entity that uses a consumer’s credit score to make a material decision affecting that person’s access to credit, housing, or employment should be prepared to issue a formal score disclosure.

Tip: → Just received a score disclosure ahead of a mortgage application? See where you stand with the mortgage pre-approval calculator.

The Federal Law Behind Credit Score Disclosure Requirements

The legal foundation for this type of disclosure sits inside the Fair Credit Reporting Act (FCRA), a federal statute enforced jointly by the Federal Trade Commission and the Consumer Financial Protection Bureau.

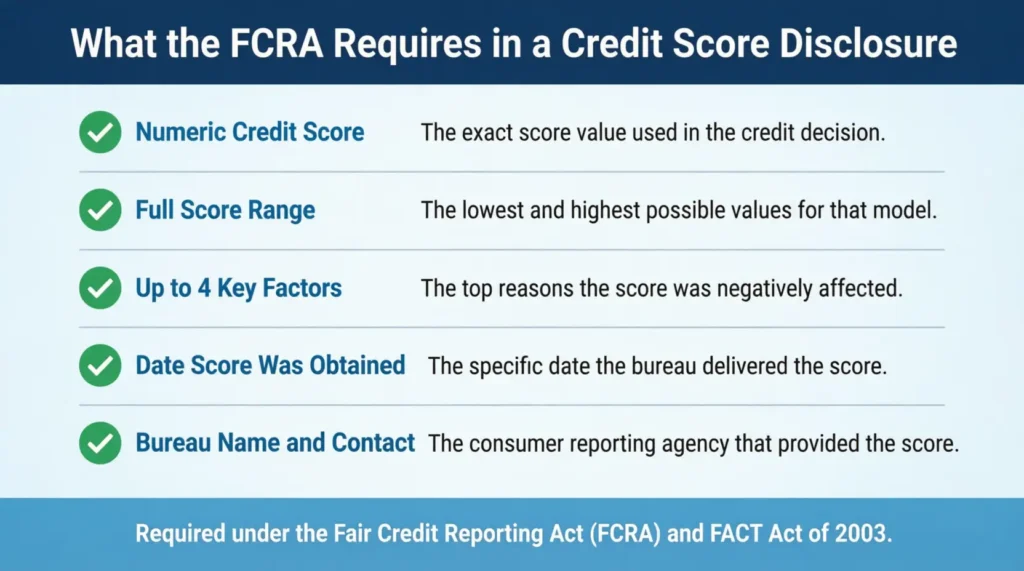

The Fair and Accurate Credit Transactions Act (FACT Act) of 2003 changed the FCRA. It added new rules about credit score disclosures. If a creditor uses a credit score to make an adverse action decision, they must give the consumer this information:

- The numeric credit score that was used

- The full range of possible scores under that scoring model

- Up to four key factors that negatively affected the score

- The exact date the score was obtained

- The name and contact information of the consumer reporting agency that provided it

This requirement is not optional. Failing to provide a proper disclosure is a violation of federal law. Consumers without a compliant notice can take action. Lenders who skip this step risk regulatory issues.

⚠️ Mistake to Avoid: Some creditors issue an adverse action letter that describes the credit decision but leaves out the actual numeric score. This does not satisfy the FCRA’s disclosure requirements. The notice must include the specific score value, not just a general reference to the consumer’s credit report.

What Every Section of the Form Means

The templates on this page include six clearly labeled sections. Understanding what each one captures makes it easier to complete the form correctly the first time.

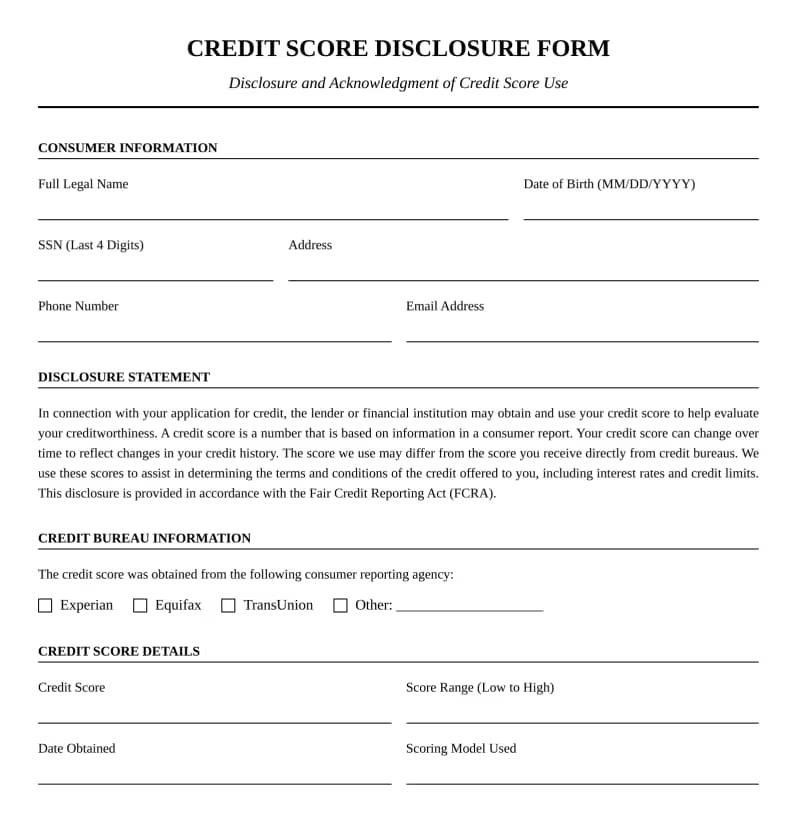

Section 1: Consumer Information

This section identifies the individual whose credit score is being disclosed. It collects the following fields:

- Full Legal Name

- Date of Birth

- Social Security Number (last four digits only)

- Current Address, City, State, and ZIP Code

- Phone Number

- Email Address

You only need the last four digits of the SSN. This reduces identity exposure while still allowing the lender to match the consumer to the correct credit file.

Section 2: Disclosure Statement

This section contains pre-written legal language that explains why the credit score was obtained and how it may be used. It also references the consumer’s rights under applicable federal and state regulations.

This text is standard and should not be modified by either party. The lender or creditor must ensure that the language complies with current regulatory requirements.

Section 3: Credit Bureau Information

This section identifies which consumer reporting agency provided the score. The form includes checkboxes for the three major bureaus: Experian, Equifax, and TransUnion. A separate text field accepts any other reporting agency not listed.

Since the score being disclosed comes from a single source per transaction, only one bureau is marked per completed form.

Section 4: Score Disclosure Details

This is the core data section of the document. It records:

- Credit Score (Numeric): The actual score the lender received from the bureau

- Credit Score Range: The full possible scale for that model (for example, 300 to 850)

- Date Score Was Obtained: The specific date the lender pulled the score

- Scoring Model Used: The name of the formula applied, such as FICO Score 8, FICO Auto Score, or VantageScore 3.0

The scoring model field matters more than it might seem. Different versions of FICO and VantageScore produce different numbers, even when pulling from the same bureau on the same day. A consumer might see a different score on a free monitoring app than what appears on this form. The scoring model field is what explains that gap.

Section 5: Authorization and Acknowledgment

This section contains a second block of standard legal text.

By signing, the consumer confirms three things:

- They got the disclosure.

- They understand their credit score was used in the evaluation.

- The personal information in Section 1 is accurate.

The text also notes that signing this form is not a guarantee of credit approval. The consumer’s signature acknowledges disclosure only, not agreement with the decision.

Section 6: Signatures

The final section collects two sets of signatures:

- Consumer Signature and Date

- Authorized Representative Name, Signature, and Date

Both parties must sign. The consumer’s signature confirms receipt. The authorized representative’s signature confirms the institution fulfilled its disclosure obligation. Together, these signatures create a verifiable, dated record of the disclosure event.

How to Fill Out the Form Step by Step

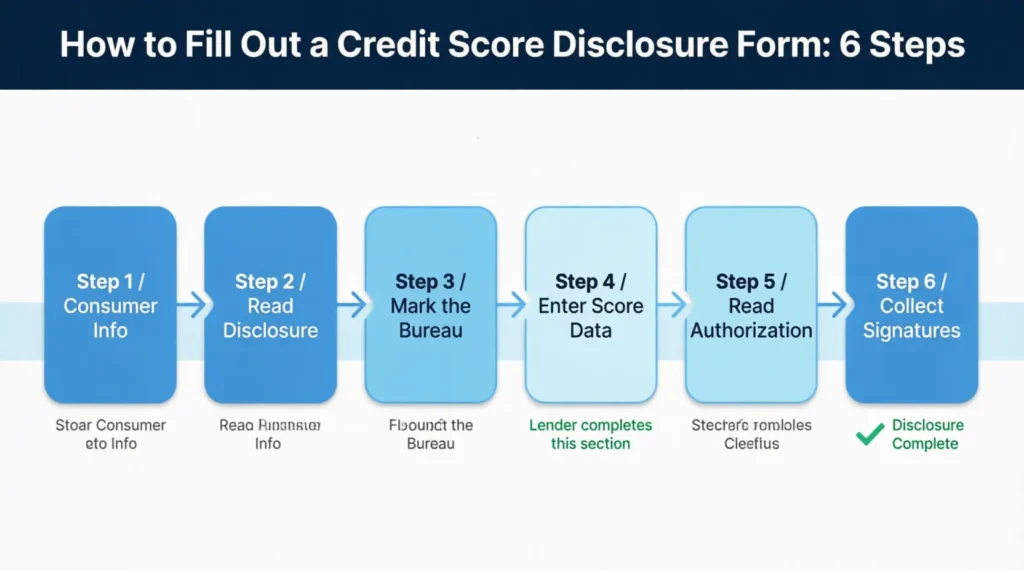

Completing a score disclosure document is straightforward when you work through it section by section. These steps apply to all three template formats available above.

Step 1: Complete the Consumer Information Fields

Start with Section 1. Write the consumer’s full legal name exactly as it appears on government-issued identification. Enter the date of birth in MM/DD/YYYY format. For the SSN field, enter only the last four digits, not the full number.

Fill in the full mailing address, including city, state, and ZIP code. Add the phone number and email address for contact purposes.

Step 2: Read the Disclosure Statement

Section 2 contains pre-written legal text that both parties should read before signing. This section explains why the credit score was obtained and references the consumer’s legal rights. No editing is needed here, and neither party should alter this language.

Step 3: Mark the Correct Bureau

In Section 3, check the box for the consumer reporting agency that provided the score. If the score came from an agency not listed, write its name in the “Other” field. Mark only one bureau per form.

Step 4: Enter the Score Details

Section 4 is completed by the lender, since they have direct access to the score data. Enter the following:

- The numeric score exactly as it appeared on the report

- The full scoring range (for example, 300 to 850)

- The exact date the score was pulled from the bureau

- The complete name of the scoring model used

Write the scoring model name in full rather than abbreviated form. For example, use “FICO Score 8” rather than just “FICO.” This helps the consumer identify the specific model if they want to investigate their score further.

Step 5: Read the Authorization Language

Section 5 is the consumer’s formal acknowledgment. The consumer examines this section in detail before signing. Their signature shows they got the disclosure. It also means their personal info in Section 1 is correct.

Step 6: Collect Both Signatures

In Section 6, the consumer signs and dates the form. The lender’s authorized representative then prints their name, signs, and adds the date.

Both parties keep a signed copy. The consumer retains theirs as documentation of the disclosure. The lender retains theirs as a compliance record.

💡 Pro Tip: If you’re using the editable Word template, complete all text fields digitally before printing. A digitally typed form is cleaner, easier to read, and less prone to errors in critical fields like the score value or scoring model name.

Score Disclosure vs. Adverse Action Notice: What’s the Difference?

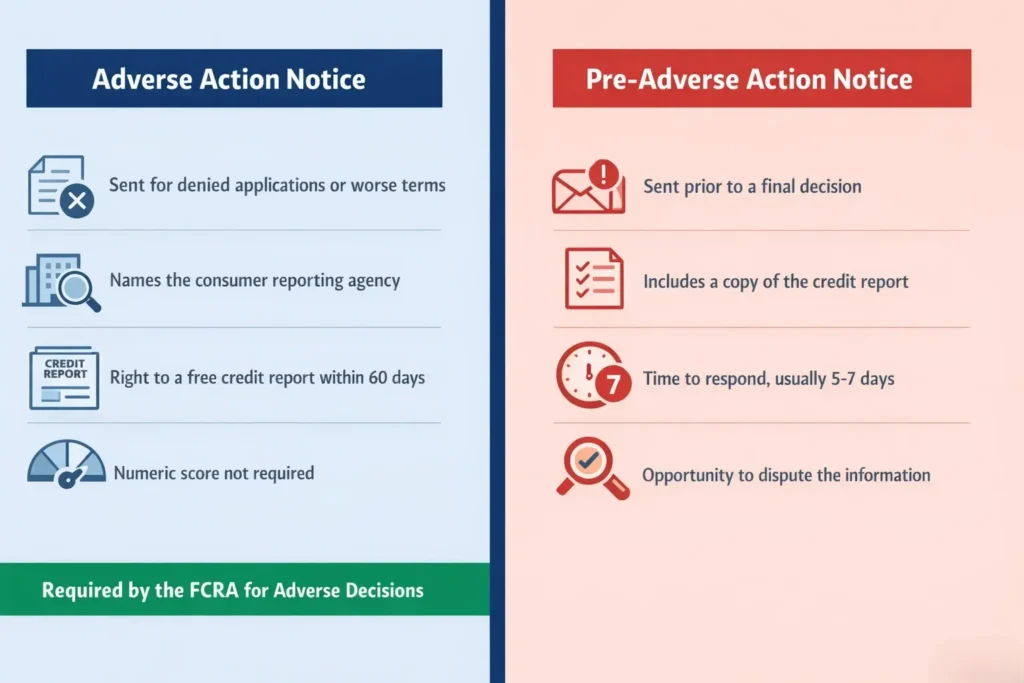

These two documents are frequently confused, but they serve different legal purposes.

A creditor sends an adverse action notice when they deny an application or offer worse terms. This decision is based on details from a consumer report. It must inform the consumer about the decision made. It should name the consumer reporting agency used. Also, it must explain the consumer’s right to a free credit report within 60 days.

A score disclosure is more specific. It centers on the credit score itself: the number, the model, the range, and the bureau that generated it. This disclosure is required when a credit score affects a credit decision. This applies whether the application is approved or denied.

In practice, many lenders combine both documents into a single notice when they deny an application. But they remain technically separate requirements under the FCRA and the FACT Act. A lender who issues an adverse action letter without including the credit score details is only partially compliant.

📌 Did You Know: For certain mortgage transactions, the FCRA requires a score disclosure even when the application is approved. The CFPB’s guidance on credit reports and scores covers how these disclosure obligations apply across different lending scenarios.

Common Mistakes When Completing a Score Disclosure Document

Even a well-designed form can create compliance problems when critical fields are skipped or filled in incorrectly. These are the most frequent errors to watch for.

Using a nickname instead of the full legal name.

The form requires the consumer’s name exactly as it appears on official identification. A mismatch between the form and the credit file can complicate verification and raise compliance questions.

Leaving the scoring model field blank.

Many lenders skip this field because it seems optional. It isn’t. Without it, the consumer can’t understand why their disclosed score differs from what they see on a free credit monitoring service.

Recording the wrong date for the score.

The date field should reflect when the lender actually pulled the score from the bureau, not when the form is being completed. These two dates can differ by days or even weeks in some application timelines.

Omitting the score range.

A score of 640 carries a very different meaning depending on the model’s scale. Without the full range, consumers can’t gauge their score against the maximum.

Missing one party’s signature.

A form signed only by the consumer but not by the lender’s authorized representative is incomplete. Both parties must provide their signatures for the document to serve as a valid disclosure record.

Tip: → Applying for an auto loan instead? The car loan calculator by credit score shows what your disclosed score means for your rate.

What Happens After the Form Is Signed?

Once both parties sign, the disclosure obligation is fulfilled. But there are practical next steps on both sides.

For the consumer: Store the completed form in a safe place. If your application was denied or you got worse terms, the FCRA lets you request a free copy of your credit report. Just ask the bureau listed on the form. You must make this request within 60 days of the adverse action.

For the lender: Keep a copy of the completed form in the applicant’s file. Lenders must keep records of adverse action notices and related disclosures. Federal compliance standards require this. These records can be reviewed during audits and referenced in consumer disputes.

If the score appears to be based on inaccurate data: The form identifies which bureau provided the score. A formal dispute can be filed with that bureau without intermediary steps. Under the FCRA, the bureau has 30 days to investigate and correct or remove inaccurate information if the review confirms an error.

Checking your full credit report through AnnualCreditReport.com is a smart next step after receiving any score disclosure, especially if the number was lower than expected. Reviewing the underlying report shows whether the score reflects accurate data.

Frequently Asked Questions

What is a credit score disclosure form?

It is a legal document that a lender or creditor provides to inform a consumer that a credit score was used in evaluating their application. It includes the numeric score, the scoring range, the bureau that provided it, and the scoring model applied.

When is a lender required to provide a credit score disclosure?

Under the Fair Credit Reporting Act, a lender must provide a score disclosure whenever a credit score is used as a factor in a credit decision. For certain mortgage transactions, this requirement applies even when the application is approved.

Is a credit score disclosure the same as a credit report?

No. A credit report is a detailed record of your full credit history. A score disclosure highlights one number from a single transaction. It includes the scoring range, the model used, and the bureau that created the score.

Which bureaus can appear on a credit score disclosure?

The three major consumer reporting agencies are Experian, Equifax, and TransUnion. Most lenders pull from one bureau per application, so only one box is marked per form. A text field for other reporting agencies is also included.

Does signing the form mean I agree with the lender’s credit decision?

No. Your signature confirms only that you received the disclosure and that your personal information on the form is accurate. It does not indicate agreement with or acceptance of the credit decision.

Can I dispute the score shown on the disclosure?

The form itself is not a dispute channel. However, If you believe there are errors in your credit report, you should contact the bureau identified on the form. Then, you can submit a formal dispute to address the issue. The bureau must investigate within 30 days under federal law.

What does the “Scoring Model Used” field mean?

It identifies the specific credit scoring formula applied to your file, such as FICO Score 8 or VantageScore 3.0. Different models give different results from the same data. This is why this field helps explain the gaps between your disclosed score and what free monitoring apps show.

How long does a lender have to provide a score disclosure after making a credit decision?

For adverse action situations, the FCRA requires the notice at or shortly after the adverse action is taken. For mortgage transactions, specific timing rules apply based on the application date and transaction type.

Conclusion

A credit score disclosure isn’t just paperwork. It’s a legal record that gives consumers real visibility into one of the most influential numbers in their financial lives.

This guide explained the disclosure notice. It shared the federal law that supports it, who needs to provide it, and how to fill out each section correctly. To meet the legal requirements and follow the template structure, fill out every field completely. This includes the scoring model and score range. Then, ensure both parties sign before filing their respective copies.

Share this guide with someone preparing to apply for a loan or rental. Understanding how their score is disclosed could protect their rights and spare them a lot of unnecessary confusion.