Most people pick a credit card based on the last ad they saw. That’s a costly habit. The Federal Reserve reports that Americans now carry over $1.1 trillion in credit card debt, and a big part of that comes from choosing the wrong card. Without a solid credit card comparison worksheet, it’s easy to overlook a hidden annual fee or a rewards rate worth hundreds per year.

The fix is simple: compare every card’s key terms side by side before you apply.

This guide covers every field on the comparison chart, how to score each option, and how to walk away with a confident, data-driven choice.

Download Your Free Credit Card Comparison Worksheets

Four ready-to-use formats are available to help you start comparing right away. These pre-filled templates include all key fields so you don’t have to build your own from scratch.

Pick the format and paper size that works best for you:

- Download PDF (US Letter) – Perfect for standard 8.5″ x 11″ printing in the US

- Download PDF (A4) – Ideal for A4-sized paper or international use

- Download Word (.docx) – Type your details directly in Microsoft Word

- Download Excel (.xlsx) – Built for quick data entry and side-by-side data comparison

A Google Sheets version is also available for cloud-based access. [Link TBD]

Disclaimer: The Templates & Printables on this site are provided for informational and personal tracking purposes only. This is not financial, legal, tax, or credit advice. While reasonable efforts are made to ensure accuracy, Credit Card Wind makes no warranties as to the completeness, reliability, or accuracy of the calculations generated by these Templates & Printables. Users are responsible for independently verifying all data and calculations. Terms, conditions, rates, regulations, and legal requirements vary by institution, jurisdiction, and individual circumstances.

Always refer to your official statements, account agreements, and applicable laws, and consult a qualified professional before making any financial, legal, or other important decisions. By using these Templates & Printables, you acknowledge that Credit Card Wind and its owner shall not be liable for any damages, losses, or financial consequences arising from the use or misuse of these Templates & Printables.

This universal disclaimer applies to all templates and printables provided by Credit Card Wind (https://creditcardwind.com), created by Robert Williams (Owner at Credit Card Wind).

© Credit Card Wind. All rights reserved.

These templates and printables may be downloaded and used for personal, non-commercial purposes only. Redistribution, resale, or modification for commercial use without permission is strictly prohibited.

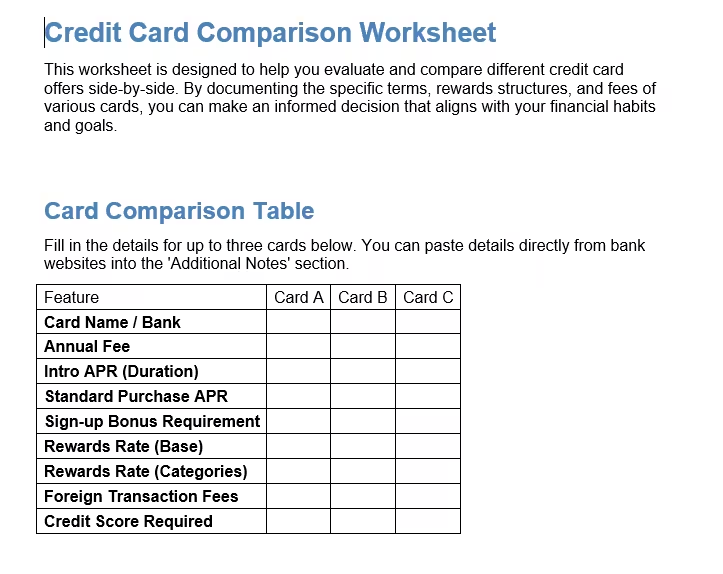

What Does a Credit Card Comparison Chart Actually Track?

A credit card comparison chart is a structured form that organizes multiple card offers in one place. Instead of switching between browser tabs and squinting at pages of fine print, you record key rates and terms, allowing you to review them at a glance.

A complete comparison spreadsheet tracks:

- Annual percentage rates — purchase APR, intro APR, and balance transfer APR

- Annual fees, foreign transaction fees, and penalty charges

- Reward types, earnings rates, and sign-up bonus requirements

- Credit score requirements

- Key perks and benefits

Having all of that in a single view makes it easy to see which card truly costs less and which one best rewards your spending habits.

Federal Reserve G.19 data shows that Americans carry more than $1.1 trillion in revolving credit card balances. A significant share of that debt comes from cardholders who choose a card without ever comparing their options side by side.

📌 Did You Know: A single percentage point difference in APR on a $5,000 balance adds up to more than $50 in extra interest charges every year.

Fields on Your Comparison Chart: What Each Column Means

This worksheet covers 13 core fields. Each field gives you a clearer picture of a card’s real cost and value. Skipping any of these fields, and you’re leaving gaps in your comparison.

APR Fields: Purchase, Intro, and Balance Transfer

There are three APR columns on the chart, and each one means something different.

Purchase APR is the ongoing interest rate charged on everyday purchases when you carry a balance. This is the rate that affects your wallet most if you don’t pay your statement in full each month.

Intro APR is a short-term, low rate, often 0%, used to attract new customers. Always record the duration alongside it. A 0% intro period lasting 21 months is far more useful than one that expires in 6 months.

Balance Transfer APR applies when you move existing debt from one card to another. If paying off debt is your main goal, this number deserves more attention than rewards ever will.

⚠️ Mistake to Avoid: Don’t let a flashy sign-up bonus pull focus away from a high ongoing APR. For cardholders who carry a balance, interest charges will often cancel out the bonus value within just a few billing cycles.

Fees: Annual, Foreign Transaction, and Penalty

Three fee types appear on almost every credit card comparison chart:

- Annual Fee: Some cards charge nothing. Others charge $550 or more. Always calculate the net value by subtracting the annual fee from your estimated yearly rewards earnings.

- Foreign Transaction Fee: Usually 1%–3% on purchases made abroad or in a foreign currency. If you travel even occasionally, prioritize cards that waive this fee entirely.

- Penalty Fees: Late payment and over-limit fees can run $29–$40 per occurrence. They’re easy to miss on the offer page but add up fast.

Rewards: Type, Rate, and Bonus Offers

Rewards look great in an advertisement. But they need context to mean anything real.

Rewards Type tells you whether you’re earning cash back, points, or miles. Cash back is the simplest because there’s no guessing about redemption value. Points and miles can be worth more, but only if you’ll actually use them before they expire.

Reward Rate is how much you earn per dollar spent. A card offering 3% back on groceries is far more valuable for a family than one offering 2% on travel bookings.

Bonus Offer is the sign-up incentive. Review the spend threshold thoroughly. A $250 bonus requiring $4,500 in spending within 3 months may not be realistic for your budget. Always run the math.

Credit Score Requirements and Key Benefits

Applying for a card for which your score doesn’t meet results in a hard inquiry on your report. That inquiry can shave a few points off your score without giving you anything in return. Always match the card’s credit requirement to your actual score before submitting an application.

The Key Benefits column is where you capture perks like cell phone insurance, travel delay protection, purchase coverage, and airport lounge access. These perks have real dollar values. Two cards with similar reward rates can look very different once you factor in what they protect you from.

How to Use the Worksheet Step by Step

The worksheet walks you through the comparison in three clear stages. Follow these steps to get the most out of every column.

Step 1: Collect 3–4 card offers you’re currently considering

Pull up the “Summary of Terms” or find the Schumer Box on each card’s application page. That table contains every APR and fee detail you’ll need to fill in the chart.

Step 2: Fill in the main comparison table

Enter each card’s details across the columns. Cover every row: APR fields, fees, rewards rate, bonus offer, credit score requirement, and key benefits. Use the Notes column for anything specific that stood out from the fine print or the card issuer’s website.

Step 3: Complete the Detailed Comparison section

This section appears on page 2 of the PDF version and in the Word version. It breaks into three focused parts:

- Cost Comparison: Enter your estimated monthly balance. The worksheet helps you calculate the annual interest cost, fee impact, and total estimated yearly cost for each card. This section makes the true cost of carrying a balance visible.

- Rewards and Benefits Evaluation: Estimate your annual rewards value for each card. Note any earning caps or redemption limits, and check off protections like travel delay or purchase coverage.

- Overall Evaluation: Name the best card for your situation and write down your reasons. This section also prompts you to flag any cards to avoid and explain why.

Step 4: Run through the built-in Guidance Checklist

The PDF version includes a checklist on page 3. Work through each item: low ongoing APR, no or low annual fee, strong rewards rate, useful benefits, credit score match, clear bonus terms, and fair penalty fees. Run through it for each card before making a final call.

💡 Pro Tip: Use the Excel or Word format if you prefer typing directly into the fields. Use the PDF version if you’d rather print and fill by hand. The Google Sheets version is a great choice. You can access your comparison from any device without needing to download a file.

How to Score Each Card Using the Built-In Rubric

The Word version of the worksheet includes a weighted scoring rubric. It removes guesswork from the final decision by putting a real number on each card’s total value.

The scoring categories and weights are:

| Category | Weight |

|---|---|

| Fees | 30% |

| Rewards | 40% |

| Sign-up Bonus | 20% |

| Perks | 10% |

Rate each card from 1 to 10 on every category. Then multiply each score by its weight and add up the totals.

Quick example: Card A earns a 6 on fees, an 8 on rewards, a 7 on bonus, and a 4 on perks.

Weighted total: (6 × 0.30) + (8 × 0.40) + (7 × 0.20) + (4 × 0.10) = 1.8 + 3.2 + 1.4 + 0.4 = 6.8 out of 10

Run the same calculation on every card you’re comparing. The highest score is likely your best match.

The system builds the default weights for a typical cardholder who values rewards most. If your situation is different, adjust the weights to match your real priorities. Someone focused on paying off debt, for example, should weight fees and APR much higher and reduce the weight on rewards. The rubric is a guide, not a locked formula.

Credit Card APR Comparison: Why Interest Rate Matters More for Balance Carriers

A credit card APR comparison is the most critical factor for anyone who carries a balance from month to month. Rewards earn attention. But interest charges work quietly in the background, billing cycle after billing cycle.

Consider this example:

| Balance | APR | Monthly Interest Cost |

|---|---|---|

| $3,000 | 20% | $50.00 |

| $3,000 | 25% | $62.50 |

| $3,000 | 29.99% | $74.98 |

A 5-point difference in APR costs $12.50 extra every single month on a $3,000 balance. Over 12 months, that’s $150 extra. Over 24 months, it’s $300. No rewards program closes that gap for a balance carrier.

The CFPB’s 2023 Consumer Credit Card Market Report found that average credit card interest rates hit record highs in 2023. For cardholders carrying balances, choosing a card based on rewards alone is one of the most expensive financial mistakes possible.

APR should be your top priority when:

- You carry a balance most months

- You’re consolidating debt with a balance transfer

- You’re early in your credit journey and your spending habits aren’t fully established

Rewards can lead when:

- You pay your full statement balance every month

- You spend consistently in a high-earning category like groceries, gas, or dining

- You have a reliable system for tracking due dates across multiple accounts

How to Read a Schumer Box Before You Fill In Your Comparison Chart

Every credit card application is required by federal law to include a Schumer Box. It’s a standardized table that lists the card’s key rates and fees in a consistent, readable format. Named after Senator Chuck Schumer, who championed clearer fee disclosures in the 1980s, it’s the fastest path to filling in your credit card comparison spreadsheet accurately.

Here’s what each row means:

Purchase APR: Usually listed as a range, such as 20.24%–29.24%. Your actual rate depends on your credit profile. When in doubt, use the higher end as your working number.

Intro APR: Shows the promotional rate and its duration. Note whether the clock starts at account opening or at first purchase, since issuers sometimes define it differently.

Balance Transfer APR and Fee: Check both the ongoing rate and the upfront transfer fee (typically 3%–5% of the transferred amount). Both affect your total cost of consolidating debt.

Minimum Interest Charge: The floor amount you’ll pay even if your calculated interest is lower. Usually $1–$2, but worth noting.

Annual Fee: Listed clearly. Some issuers waive it in the first year. Check whether the waiver is automatic or requires a call.

Late and Returned Payment Fees: Typically $29–$40. These apply automatically if you miss a due date, even by a single day.

💡 Pro Tip: Card issuers are legally required to include the Schumer Box in every offer. If you can’t spot it on the card’s page, scroll to the very bottom and look for a link labeled “Rates & Fees” or “Pricing and Terms.” It’s always there.

Common Mistakes to Avoid When Using a Credit Card Comparison Tool

A card comparison spreadsheet is only as useful as the process behind it. These are the errors that tend to cost people the most.

Comparing rewards without accounting for annual fees

A card earning 3% cash back with a $250 annual fee needs to produce at least $250 in rewards just to break even. Always calculate net value, not gross rewards. The difference can flip which card comes out ahead.

Chasing a sign-up bonus you can’t realistically hit

Consider David, a high school teacher in Cincinnati who applied for a travel card with a $600 sign-up bonus. The requirement was $5,000 in spending within 3 months. His typical monthly spend was around $1,200. He missed the threshold, lost the bonus, and was stuck paying the annual fee for the full year. Always run the math on the spend threshold before the bonus number grabs your attention.

Applying for multiple cards at once

Each credit card application triggers a hard inquiry on your credit report. Several inquiries in a short window can signal financial stress to lenders and temporarily lower your score. Compare 3–4 cards carefully and apply for just one at a time.

Comparing based on ideal spending, not actual spending

A card with 5x points on airline tickets means nearly nothing if you fly twice a year. Use the “Primary Use Category” field in the worksheet. This helps you compare your real monthly spending habits, not the lifestyle you wish you had.

Skipping the foreign transaction fee column

Even a 1%–2% fee on international purchases can quietly cancel out rewards on every overseas transaction. If you shop on international websites or travel more than once a year, this column matters more than most people realize.

Applying for cards your credit score doesn’t qualify for

Hard inquiries stay on your report whether the application is approved or denied. Before you submit anything, match the card’s stated credit score requirement to your actual score. The worksheet has a dedicated field for this, and filling it in takes 30 seconds.

Frequently Asked Questions

How many credit cards should I compare before picking one?

Comparing 3–4 cards gives you enough variety without making the process overwhelming. More than four options tend to cause decision fatigue without adding much useful information.

Will applying for a credit card hurt my credit score?

Yes, each application triggers a hard inquiry that can lower your score by a few points temporarily. The effect usually fades in 12 months. So, it’s smart to compare cards carefully before applying. This helps you avoid unnecessary inquiries.

What is the difference between purchase APR and cash advance APR?

Purchase APR is the interest rate on everyday card transactions. Cash advance APR kicks in when you take out cash with your card. It’s usually higher, often over 29.99%, and there’s no grace period.

Do credit card comparison worksheets work for business credit cards too?

Yes. The same fields apply to business cards: APR, annual fee, rewards rate, and credit score requirements. Business cards may also carry employee card fees and spending controls, so add those details to the Notes column.

How often should you review and compare your credit cards?

Once a year is a solid baseline. It’s also worth doing a fresh comparison whenever your financial situation changes significantly, such as after a raise, a major purchase goal, or a notable shift in your credit score.

Is a no-annual-fee card always the better choice?

Not always. A card with a $95 annual fee that earns 3% back on groceries can outperform a no-fee card earning 1.5% flat if your grocery spending is high enough. Always calculate the net value first.

What happens if I apply for a credit card and get rejected?

The hard inquiry stays on your report regardless of the outcome. Wait at least 6 months before applying again. During that time, check the card’s credit score requirement and compare it to your actual score.

Can this worksheet be used to compare secured credit cards?

Yes. The fields still apply, though secured cards typically have lower credit limits and different fee structures. Pay extra attention to the annual fee and deposit requirement when filling in the comparison table.

How do I compare credit card rewards programs fairly when they use different formats?

Convert all reward types to a cents-per-dollar value. If 1 point equals 1 cent, a card earning 3 points per dollar equals 3% back. This common unit lets you compare cash back, points, and miles on the same scale.

Bottom Line

Choosing a credit card without comparing your options is like buying a car without checking the sticker price. APRs, fees, rewards, and credit score requirements each tell part of the story. The scoring rubric ties it all together by putting a real number on which card fits your spending habits best.

For most readers, it’s best to start with the APR section if you carry a balance. If you pay in full each month, begin with the rewards section. Then let the rubric make the final call.

Download the free credit card comparison worksheet and run the numbers on the cards you’ve been eyeing. If you know someone comparing cards right now, share this guide with them. The right comparison tool could save them hundreds in fees before they ever swipe once.