A 2025 Junior Achievement survey found that 80% of teens have never heard of FICO credit scores or don’t fully understand how they work. If you’re a student trying to figure out your credit score worksheet for students, that gap in knowledge can feel overwhelming. Most schools don’t teach this stuff.

A structured worksheet helps you record scores, track changes, and set clear goals to build healthy credit from day one.

Here are free downloadable templates in different formats. You’ll also find a step-by-step guide to fill them out and tips for building credit wisely.

Download Your Free Student Credit Score Worksheets

Four ready-to-use templates are available to make your credit tracking simple. Each one covers scores, utilization, key factors, and an action plan.

Pick the format and paper size that works best for you:

Disclaimer: The Templates & Printables on this site are provided for informational and personal tracking purposes only. This is not financial, legal, tax, or credit advice. While reasonable efforts are made to ensure accuracy, Credit Card Wind makes no warranties as to the completeness, reliability, or accuracy of the calculations generated by these Templates & Printables. Users are responsible for independently verifying all data and calculations. Terms, conditions, rates, regulations, and legal requirements vary by institution, jurisdiction, and individual circumstances.

Always refer to your official statements, account agreements, and applicable laws, and consult a qualified professional before making any financial, legal, or other important decisions. By using these Templates & Printables, you acknowledge that Credit Card Wind and its owner shall not be liable for any damages, losses, or financial consequences arising from the use or misuse of these Templates & Printables.

This universal disclaimer applies to all templates and printables provided by Credit Card Wind (https://creditcardwind.com), created by Robert Williams (Owner at Credit Card Wind).

© Credit Card Wind. All rights reserved.

These templates and printables may be downloaded and used for personal, non-commercial purposes only. Redistribution, resale, or modification for commercial use without permission is strictly prohibited.

What Is a Credit Score Worksheet?

A credit score worksheet is a structured document that helps students organize and understand their credit information in one place. Think of it like a report card, but for your financial health.

Instead of grades for math or science, this sheet tracks your credit scores from the three major bureaus: Experian, Equifax, and TransUnion. It also breaks down the five key factors that affect those scores.

A Junior Achievement and Wakefield Research survey from 2025 revealed that 80% of teens have never heard of FICO scores or don’t fully grasp their purpose. That’s a big deal. Credit scores affect nearly every money decision after graduation, from renting an apartment to getting a car loan.

A student credit tracking sheet fills that gap. It turns confusing numbers into a clear picture. You can see where you stand, spot problems early, and take action before small mistakes become big ones.

Teachers, financial literacy programs, and self-learners use worksheets like this. They make credit education practical and hands-on.

How to Use This Worksheet (Step-by-Step Guide)

The worksheet is laid out in seven clear sections. Walk through each one in order to get the full picture of your credit health.

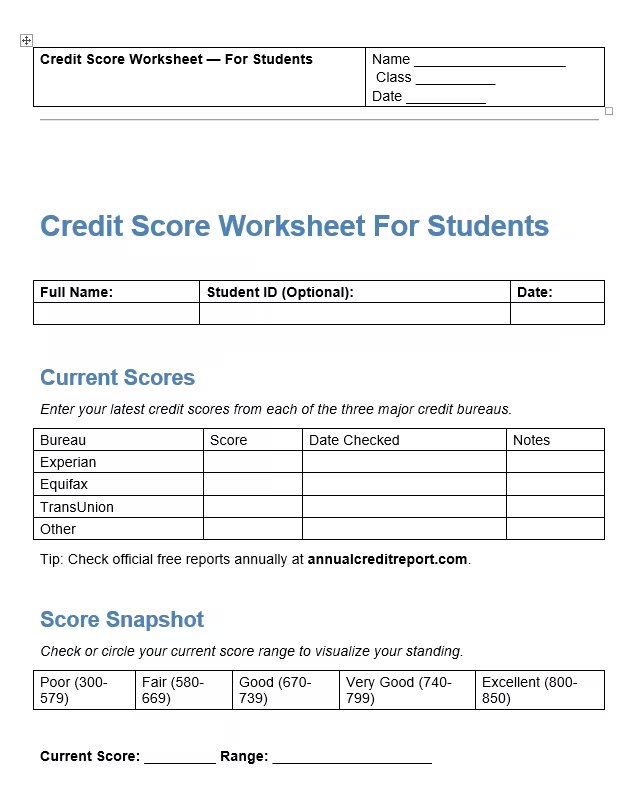

Step 1: Fill In Your Personal Details

Start at the top of the page. Write your full name, student ID (optional), and today’s date. If you’re using this in a class, add your school name and class period in the header row.

This section keeps things organized, especially if you print the sheet out and store it in a folder.

Step 2: Record Your Current Credit Scores

Move to the “Current Scores” table. Enter your latest score from each of the three major credit bureaus:

- Experian

- Equifax

- TransUnion

Write the score, the date you checked it, and any notes (such as “first time checking” or “score went up 15 points”).

If you don’t have a credit score yet, that’s completely normal. Write “No score yet” in the column and use the rest of the worksheet to plan your first steps.

💡 Pro Tip: Check your reports for free at AnnualCreditReport.com. This is the only site authorized by federal law to give you free reports from all three bureaus.

Step 3: Identify Your Score Range

Look at the “Score Snapshot” section. It shows five ranges:

Circle or highlight the range that matches your current score. Then write your exact score and range in the spaces provided.

This quick visual check tells you exactly where you stand on the credit spectrum.

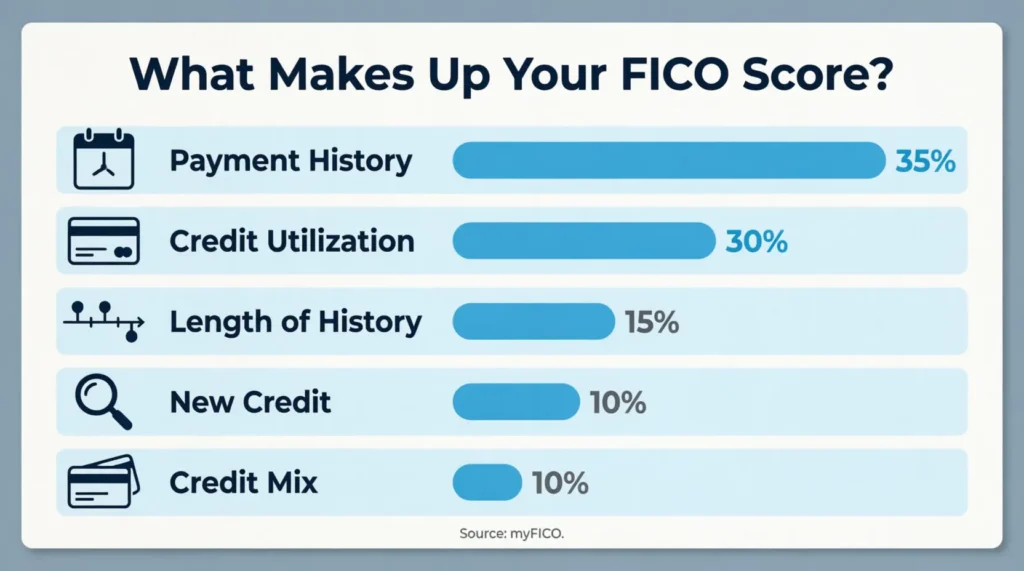

Step 4: Review the Five Credit Score Factors

The “Factors & Quick Actions” table is the educational heart of this worksheet. It lists the five factors that shape a FICO score, along with simple action steps.

Go through each factor one by one:

- Payment History (35%) – Check the boxes if you’ve set up auto-pay, signed up for due-date alerts, or committed to paying at least the minimum on time.

- Credit Utilization (30%) – Review whether your card balances stay under 30% of your limit (under 10% is even better).

- Length of History (15%) – Note whether you’ve kept your oldest account open and avoided opening too many new ones at once.

- New Credit (10%) – Check if you’ve spaced out credit applications by at least six months.

- Credit Mix (10%) – List the types of accounts you have (credit card, student loan, etc.).

Check off the action items you’ve already done. Leave the rest unchecked as goals to work toward.

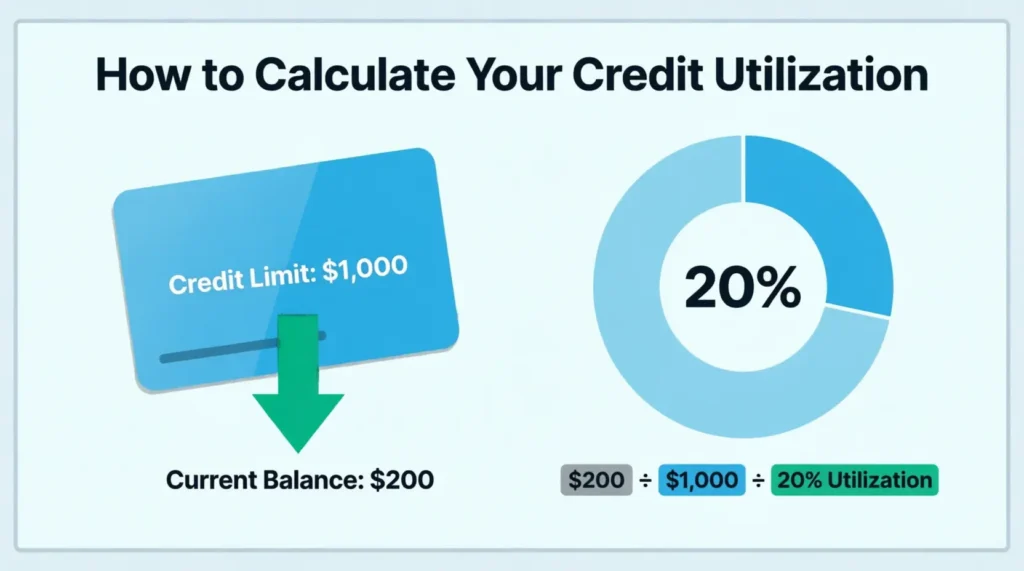

Step 5: List Your Accounts and Calculate Utilization

The “Accounts & Utilization” table is where things get hands-on. List every credit account you have:

- Account type (credit card, student loan, etc.)

- Institution name

- Credit limit

- Current balance

- Utilization percentage

- Statement closing date

To calculate utilization: Divide your current balance by your credit limit. For example, a $200 balance on a $1,000 limit equals 20% utilization.

The worksheet even includes a filled-in example row ($200 balance / $1,000 limit = 20%) so you can follow along.

⚠️ Mistake to Avoid: Only tracking one card’s utilization. Total utilization across all cards matters just as much as individual card ratios. Add up all balances and divide by all limits.

Step 6: Track Your Score Over Six Months

The “Score History” table gives you six columns to record your score over time. Each month (or each time you check), write the date, your score, and the change from last time.

This is where the real learning happens. You can see patterns. Did your score drop after a late payment? Did it rise after you paid down a balance? The trends tell a story that a single number can’t.

Step 7: Create a SMART Action Plan

The final section is the “Action Plan.” SMART stands for Specific, Measurable, Achievable, Relevant, and Time-bound.

Write down 2 to 3 concrete tasks. For example:

| Task | Target Date | Priority | Status |

|---|---|---|---|

| Set up auto-pay for student card | This week | High | Not started |

| Pay balance below 10% of limit | End of month | Medium | In progress |

Setting written goals makes you far more likely to follow through than keeping a vague plan in your head.

Understanding the Link Between Credit Cards and Credit Scores

Credit cards affect credit scores in important ways. They are often the best tool for students to build credit.

Credit Cards Are Credit-Building Tools

A credit card is essentially a small, repeatable loan. Each month, the card company lends money for purchases. When that money is paid back, the cardholder proves trustworthiness with credit.

This cycle of borrowing and repaying gets reported to the credit bureaus and builds credit history over time.

The Right Way to Use Credit Cards

Credit cards should be used to boost a credit score rather than hurt it. Follow these guidelines:

- Charge small, regular purchases — Use the card for things like gas or groceries (expenses you already have the money to cover).

- Pay off the full balance every month — This keeps you out of debt and shows a perfect payment track record.

- Keep your balance low throughout the month — Credit card companies report your balance on your statement closing date, not your payment due date. So even if you pay in full later, a high balance at closing time can push up your utilization ratio.

- Never carry a balance just to build credit — This is a myth. Paying in full works just as well and saves you money on interest.

Student Credit Cards vs. Regular Cards

Many banks offer credit cards built specifically for students. These usually have:

- Lower credit limits (often $500 to $1,500)

- No annual fee

- Easier approval requirements

- Basic rewards programs

- Tools to help build credit the right way

Student cards are a great starting point. The lower limits act as a natural guardrail against overspending.

Secured Credit Cards as a Starting Point

If approval for a regular student card is not possible, a secured credit card is a solid option. A deposit is required—typically $200 to $500—and that amount becomes the credit limit.

The card is used just like a regular credit card. After several months of smart use, many card companies will upgrade the cardholder to an unsecured card and return the deposit.

How Credit Card Activity Appears on Your Worksheet

When credit card activity is tracked on a tracking sheet, the following information becomes visible:

- How many cards are held (affects credit mix and history length)

- Total available credit (affects utilization)

- Current balances (affects utilization)

- Payment history (the most important factor)

This view makes it easy to see exactly how credit card habits are affecting credit health.

Why Tracking Your Credit Score in College Matters

Many students assume credit scores don’t matter until after graduation. That’s a costly mistake.

The FICO Score Credit Insights report from Fall 2025 found that Gen Z borrowers saw their average score drop to 676. That’s 39 points below the national average of 715, and it marks the steepest year-over-year decline of any age group since 2020.

Why the drop? Student loan repayments resumed, inflation stayed high, and many young adults had little savings to fall back on.

Here’s why tracking early makes a real difference:

- Apartment applications. Landlords check credit. A score under 620 can lead to rejection or a bigger security deposit.

- Car loans. A student with a 680 score might pay $2,000 more in interest over five years compared to someone with a 740 score on the same loan.

- First credit card offers. Better scores unlock lower interest rates and higher limits.

- Job screenings. Some employers review credit reports during the hiring process, especially in finance-related roles.

A student named Marcus, a junior at a state university, started tracking his score during his sophomore year. Within 12 months, he raised it from 620 to 705 simply by paying on time and keeping his card balance under 10% of his limit.

Tracking doesn’t just show you a number. It teaches you the habits that keep that number climbing.

Understanding the Five Credit Score Factors

Every FICO score is built from five categories. Knowing what each one means helps you focus your energy where it counts the most.

Payment History (35%)

This is the single biggest factor. It measures whether bills get paid on time. Even one payment that’s 30 or more days late can cause a score to drop by 50 to 100 points.

For students just starting out, the rule is simple: never miss a due date. Auto-pay and calendar reminders are the easiest way to stay on track.

Credit Utilization (30%)

Credit utilization is the percentage of available credit currently in use. Experian notes that keeping utilization under 30% is recommended, but under 10% produces the best results.

For a student with a $500 credit limit, that means keeping the balance below $150 at all times, and ideally below $50.

Length of Credit History (15%)

This factor looks at the average age of all open accounts. Students naturally have shorter histories, and that’s okay. The key is to keep your oldest account open, even if you rarely use it.

Closing a first credit card can shorten your history and lower your score.

New Credit Inquiries (10%)

Every time a lender pulls your credit report for a new application, a hard inquiry appears. Too many hard inquiries in a short period signals risk.

Students should space out credit applications by at least six months. Checking your own score (a soft inquiry) does not affect it at all.

Credit Mix (10%)

This measures the variety of account types, such as credit cards, student loans, and installment loans. Having a mix shows lenders that different types of debt can be managed well.

Students shouldn’t open accounts just to diversify. A credit card plus a student loan already counts as a healthy mix.

Payment history and credit utilization together make up 65% of a FICO score. Focusing on just these two factors delivers the biggest improvement for the least effort.

How to Check Your Credit Score for Free

Students don’t need to pay a dime to see their credit scores or reports.

The Consumer Financial Protection Bureau (CFPB) recommends visiting AnnualCreditReport.com to get free weekly credit reports from Experian, Equifax, and TransUnion. This is the only federally authorized website for free reports.

Other no-cost options include:

- Your bank or credit union. Many provide free FICO or VantageScore updates through online banking or mobile apps.

- Student credit cards. Most issuers now include a free score on monthly statements or their app.

- Credit monitoring services. Tools like Credit Karma and Experian’s free tier show VantageScore or FICO updates regularly.

Important: Checking your own credit report or score is always a soft inquiry. It never hurts your score. Check as often as you like without worry.

Credit-Building Strategies That Work for Students

Building credit early gives graduates a head start on some of life’s biggest financial milestones. These strategies are proven and practical.

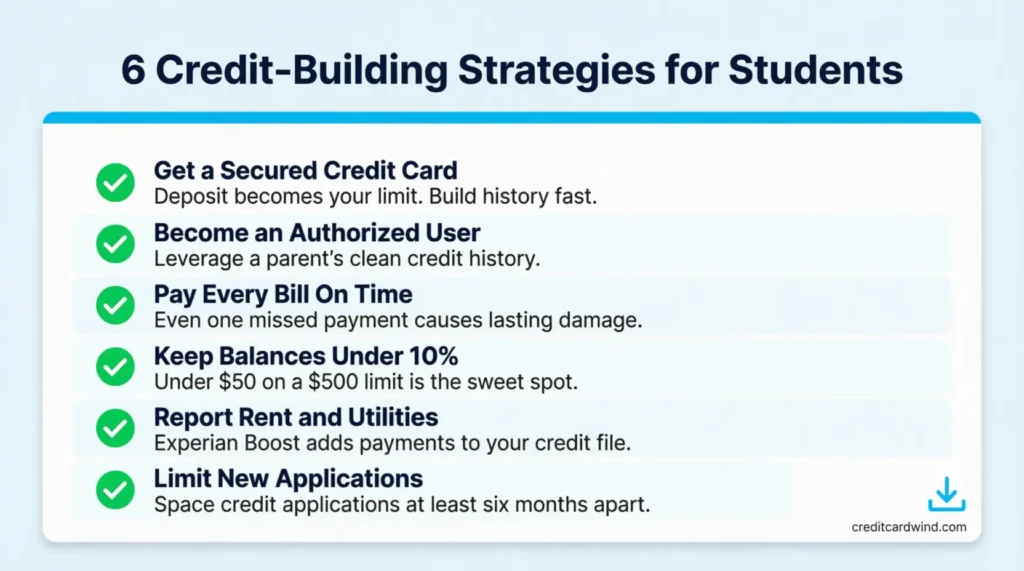

1. Get a secured credit card.

Secured cards require a refundable deposit (often $200 to $500) that becomes the credit limit. Use it for small purchases and pay the full balance each month. Most issuers report to all three bureaus, which builds history fast.

2. Become an authorized user on a parent’s account.

When a parent adds a student to a long-standing card with a clean payment record, that positive history can appear on the student’s credit report. It’s one of the fastest ways to establish a score without opening a new account.

3. Pay every bill on time, every time.

Set up auto-pay for at least the smallest payment. Even a single missed payment can cause serious damage to a new credit profile.

4. Keep balances low.

Aim to use less than 10% of available credit. If the limit is $500, try to keep the balance under $50 when the statement closes.

5. Report rent and utility payments.

Services like Experian Boost and similar tools let students add on-time rent, utility, and streaming payments to their credit file. This can raise a thin credit profile by several points.

💡 Pro Tip: Pay the credit card balance before the statement closing date, not just the due date. The balance reported to the bureaus is usually the statement balance. Paying early keeps the reported utilization low.

6. Limit new applications. Each hard inquiry can shave a few points off a score. Only apply for credit when it’s truly needed, and use pre-qualification tools (soft pulls) to check odds first.

Common Credit Mistakes Students Should Avoid

Small missteps can snowball quickly when a credit file is young and thin. Avoiding these common errors protects a score that’s still being built.

- Missing a payment because “it’s just $25.” Even a small missed payment gets reported after 30 days. Late payments stay on a credit report for up to seven years.

- Maxing out a student credit card. A $500 card with a $490 balance creates 98% utilization. That alone can tank a score.

- Closing the first credit card after getting a better one. Closing the oldest account shortens credit history and raises overall utilization.

- Ignoring the credit report entirely. Errors happen. The Federal Trade Commission has found that a significant share of consumers have errors on their reports. Catching mistakes early prevents bigger problems later.

- Co-signing for a friend. If the friend misses payments, both credit scores take the hit. Students should avoid co-signing until they have a strong financial cushion.

⚠️ Mistake to Avoid: Applying for multiple credit cards during the same week to “see which one approves.” Each application triggers a hard inquiry, and several at once can drop a score by 20 or more points.

When and How Often Should Students Check Their Credit?

A good rhythm is to check once a month. Many banking apps and credit monitoring tools make this easy with real-time alerts and score trackers.

Beyond the monthly check, pull your full credit report from all three bureaus at least once a year. Look for:

- Accounts you don’t recognize

- Late payments that were actually paid on time

- Incorrect balances or credit limits

- Outdated personal information

If something looks wrong, file a dispute directly with the bureau. Each bureau has an online dispute portal that walks through the process step by step.

Checking monthly and reviewing the full report yearly creates a solid safety net. It catches fraud early and keeps the credit file accurate.

Frequently Asked Questions (FAQs)

What credit score do you start with as a student?

There’s no starting score like zero or 300. Students begin with no credit score at all. A score only appears after at least one account has been open and reported to a credit bureau for about six months.

What is a good credit score for a college student?

A score of 670 or above is considered good by most lenders. For students just starting out, reaching 670 to 700 within a year or two of opening a first account is a solid and realistic goal.

Does checking my own credit score lower it?

No. Checking your own score is a soft inquiry, and it has zero effect on your credit. Only hard inquiries from lender applications affect the score.

Can I build credit as a student without a credit card?

Yes. Student loan payments reported to the bureaus count toward credit history. Tools like Experian Boost also let you add rent and utility payments to your credit file.

Should I become an authorized user on my parents’ credit card?

It can help, but only if the parent’s card has a long history and a clean payment record. If the account carries high balances or late payments, it could hurt rather than help.

How often should I update my credit score worksheet?

Once a month is a good pace. Check your score, update the tracking table, and review your utilization. Pull the full report from all three bureaus at least once a year.

Do student loans help or hurt my credit score?

They can do both. On-time payments build positive history. Missed or late payments cause significant damage. Keeping up with payments after the grace period ends is critical.

What is credit utilization and why does it matter?

Credit utilization is your total card balances divided by your total credit limits, shown as a percentage. It makes up 30% of a FICO score, so keeping it under 30% (and ideally under 10%) has a big impact.

Bottom Line

Tracking credit as a student doesn’t have to be complex. The right worksheet puts scores, factors, and goals on a single page. From recording bureau scores to calculating utilization and setting SMART goals, each section builds real understanding.

The best time to start is right now, even before that first credit card arrives. Based on the data, students who track early build stronger scores and avoid the traps that pull Gen Z averages down.

If you know a classmate, friend, or sibling about to open their first credit card, share this student credit score tracker with them. One worksheet today can save them thousands in interest tomorrow.