Running a business on tight margins means every fee matters. Credit card processing costs typically run between 1.5% and 3.5% per transaction, according to Federal Reserve Bank of Kansas City payment research. Across hundreds of daily sales, that drain adds up fast. That’s why many merchants now use a credit card surcharge notice template to recover those costs while keeping customers fully informed before they pay.

A clear surcharge disclosure stops checkout surprises. It cuts down on disputes and keeps your business compliant with card network rules.

Keep reading for four free, print-ready templates. You’ll also find a step-by-step setup guide, state-specific rules, and practical tips. These resources will help you roll out your surcharge without pushing loyal customers away.

Download Your Free Credit Card Surcharge Notice Templates

Four ready-to-use templates are available to make setup simple. Each one has all the sections your business needs. This helps you stay compliant and communicate clearly with customers. Pick the format and paper size that works best for you:

Editable Word Templates (Customize Everything):

Print-Ready PDF Templates (Quick & Simple):

Disclaimer: The Templates & Printables on this site are provided for informational and personal tracking purposes only. This is not financial, legal, tax, or credit advice. While reasonable efforts are made to ensure accuracy, Credit Card Wind makes no warranties as to the completeness, reliability, or accuracy of the calculations generated by these Templates & Printables. Users are responsible for independently verifying all data and calculations. Terms, conditions, rates, regulations, and legal requirements vary by institution, jurisdiction, and individual circumstances.

Always refer to your official statements, account agreements, and applicable laws, and consult a qualified professional before making any financial, legal, or other important decisions. By using these Templates & Printables, you acknowledge that Credit Card Wind and its owner shall not be liable for any damages, losses, or financial consequences arising from the use or misuse of these Templates & Printables.

This universal disclaimer applies to all templates and printables provided by Credit Card Wind (https://creditcardwind.com), created by Robert Williams (Owner at Credit Card Wind).

© Credit Card Wind. All rights reserved.

These templates and printables may be downloaded and used for personal, non-commercial purposes only. Redistribution, resale, or modification for commercial use without permission is strictly prohibited.

What Is a Credit Card Surcharge Notice Template?

A credit card surcharge notice template is a pre-formatted document. Merchants display it at their place of business to tell customers about an extra fee for paying by credit card.

Think of it as your business’s advance announcement. Before a customer reaches the register, the notice communicates: “Credit card payments carry an additional charge.” That kind of upfront disclosure is exactly what Visa and Mastercard require, and what customers deserve.

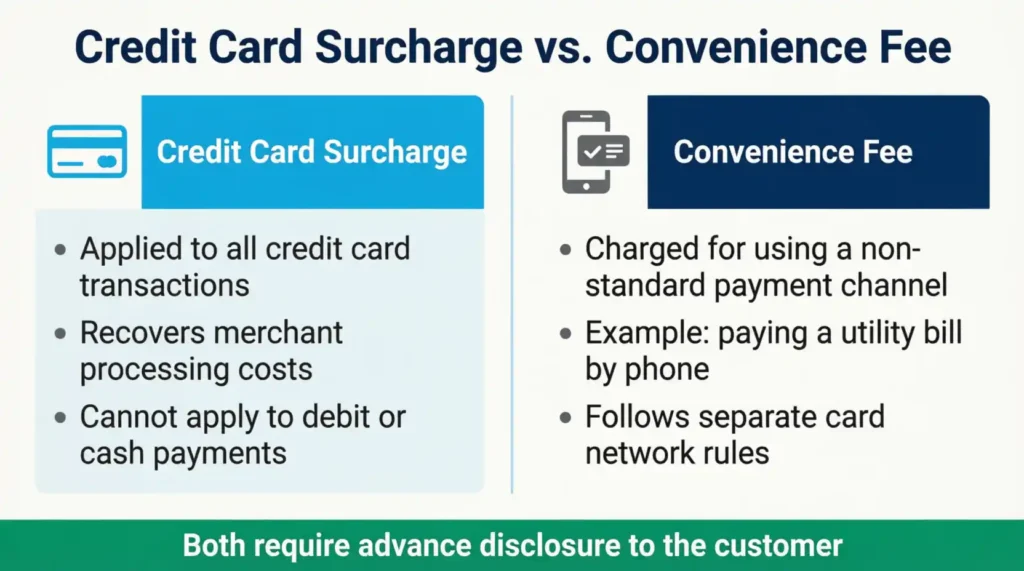

It’s also worth knowing how a surcharge differs from a convenience fee, since the two terms are often confused.

- A surcharge applies specifically to credit card transactions. It’s designed to recover processing costs and can’t be applied to debit or cash payments.

- A convenience fee is charged when a customer uses a non-standard payment channel for that business. For example, paying a utility bill over the phone by credit card instead of in person.

Research from the Federal Reserve Bank of Kansas City on payment system costs shows that credit card interchange fees, the main driver of merchant processing costs, average between 1.5% and 3.5%, depending on the card type. That’s a real expense. A properly formatted surcharge disclosure helps merchants recover fees while being transparent with customers. This approach ensures that nothing is hidden from them.

Why Do Businesses Use These Notices?

There are three solid reasons merchants post a surcharge disclosure notice.

1. Card Network Requirements

Visa and Mastercard both require merchants to notify customers of a surcharge before a transaction is completed. This should happen in two places: first, at the entry point, like your front door or website landing page. Then, at the point of sale, such as the register or online checkout. Missing either location puts your business at risk of card network penalties.

2. Legal Compliance

Many states have their own rules about surcharging. A clear, written notice meets requirements. It also protects your business from future consumer complaints or regulatory problems.

3. Customer Transparency

Nobody likes a surprise charge. When customers see the notice before they pay, they can choose to use cash or a debit card instead. That choice is exactly what the regulations are designed to protect. A business that communicates clearly builds more trust, even when it charges a fee.

📌 Did You Know Visa and Mastercard both require merchants to register their intent to surcharge at least 30 days before the fee goes live. Skipping this step means your surcharge program is non-compliant from day one, even if your posted notice is perfectly worded.

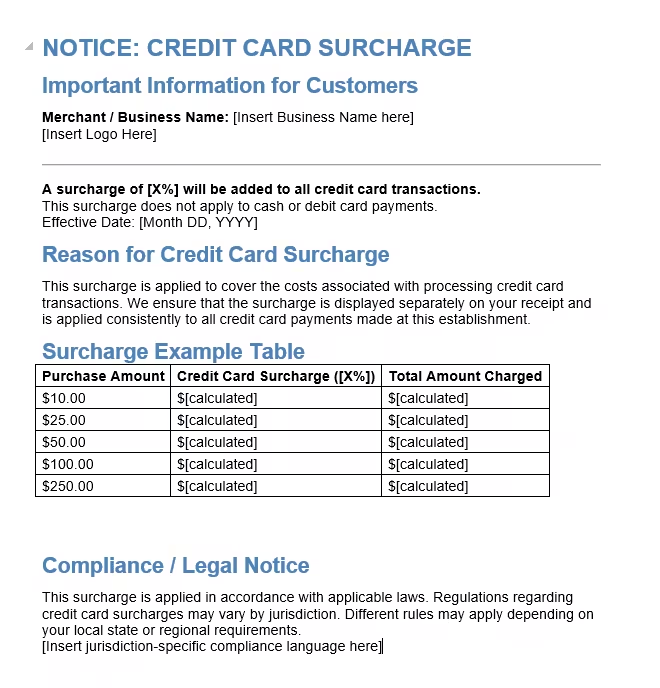

What’s Included in Our Credit Card Surcharge Notice Template?

Each template is built with every element a compliant, professional surcharge notice needs. Nothing is missing, and nothing is filler. After reviewing all four template files, each one contains the following sections:

Business Identification

A merchant name field and a logo placeholder so your branding stays consistent across every printed notice.

Core Surcharge Statement

A bold, clearly worded statement, such as “All credit card payments are subject to a surcharge of [X%].” A separate line confirms that cash and debit card payments are exempt, which is a card network requirement.

Effective Date

A dedicated field for the date the surcharge took effect. Card networks require this, and it reassures customers that the policy isn’t new or hidden mid-transaction.

Reason for the Surcharge

The fee includes credit card processing costs. It will show up as a separate line item on your receipt for clarity. This section keeps the notice honest and easy to understand.

Example Surcharge Calculation Table

A built-in table showing surcharge amounts and totals for common purchase amounts: $10, $25, $50, $100, and $250. The A4 PDF version comes pre-filled with a 3% example, so $10.00 becomes $10.30, $50.00 becomes $51.50, and $100.00 becomes $103.00. The Word versions let you enter your own rate and update the table manually.

Legal and Compliance Language Section

A clearly marked placeholder where you can insert the compliance language specific to your state or card network. The template labels this section so it’s impossible to skip.

Contact Information

Include fields for your business name, phone number, and website or email. This way, customers can easily find who to contact with questions.

QR Code Placeholder

A built-in box for a QR code that links customers to your full surcharge policy page online. It’s optional, but tech-savvy customers like to see all the details before paying.

How to Use the Credit Card Surcharge Notice Template (Step-by-Step)

Setting up your surcharge posting takes less time than you might think. Follow these steps and your notice will be compliant and ready to post.

Download the Right Format

Choose based on how you plan to use it. If you want to print right away, grab the PDF. If you want to customize the wording or enter your specific surcharge rate, choose the Word version.

Open the File

Open the PDF in Adobe Acrobat or any standard PDF viewer. Open the Word version in Microsoft Word or Google Docs.

Add Your Business Name and Logo

Replace the placeholder text with your actual business name. Insert your logo into the designated area to keep the notice looking professional and on-brand.

Enter Your Surcharge Percentage

Replace [X%] with your actual surcharge rate. It can’t exceed 3%, which is the current Visa and Mastercard cap, and it can’t exceed your actual cost of accepting credit cards.

Complete the Example Calculation Table

Fill in the surcharge amount and total for each purchase amount shown in the table. Customers appreciate seeing real numbers. It removes any guesswork about what they’ll actually pay.

Set the Effective Date

Enter the date the surcharge program officially began. It must be at least 30 days after you registered your intent to surcharge with Visa and Mastercard.

Add Jurisdiction-Specific Compliance Language

Check your state’s rules and insert the required legal language in the compliance section. If your state doesn’t have specific rules, you can use a general statement: “This surcharge follows federal and state laws.”

Fill In Contact Information and QR Code

Add your business name, phone number, and website or email. If you have a full surcharge policy page online, create a QR code. Then, paste it into the placeholder box on the notice.

Save, Print, and Post

Save your completed file. Print it on US Letter or A4 paper, depending on your template format. Consider laminating it for durability. Post it at your store entrance and at the checkout counter.

⚠️ Mistake to Avoid: Don’t post the notice only at the checkout counter. Card network rules require surcharge disclosure at the point of entry, meaning your front door or store entrance. Posting only at the register is one of the most common compliance gaps merchants make.

Why You Need a Credit Card Surcharge Notice (And What Happens If You Don’t Have One)

Not posting a surcharge notice isn’t a minor oversight. It can cause real, costly problems for your business.

Card Network Penalties

Visa and Mastercard set strict rules about surcharge disclosures. Visa’s merchant resources make clear that merchants who charge a surcharge without proper notice risk customer complaints that trigger network investigations. The outcome can vary. It might be a formal warning, or it could be a suspension of card acceptance privileges.

Customer Disputes and Chargebacks

When customers find an unexpected charge, they often respond with a chargeback. Each chargeback usually costs $20 to $100 in processing fees. Plus, you lose the original transaction amount. One month of hidden surcharges can cause enough chargebacks to erase all the money the surcharge aimed to recover.

State Law Violations

Some states have specific surcharge disclosure rules. Connecticut and Massachusetts currently prohibit credit card surcharges altogether. Businesses in those states can’t charge any surcharge, regardless of how the notice is worded.

Damaged Customer Trust

A hidden fee can shock customers. This surprise often leads them to review sites, beyond just the financial costs. One undisclosed charge can undo years of goodwill built with a loyal customer base.

The fix is easy: post the notice, follow the steps, and help customers choose before they pay.

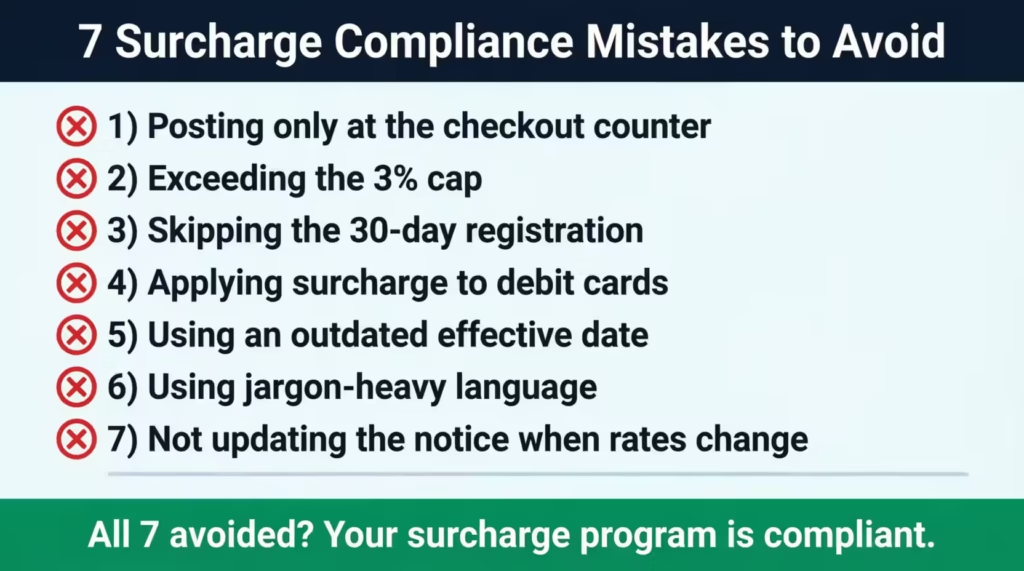

Common Mistakes to Avoid When Using a Credit Card Surcharge Notice

Even merchants who know they need a surcharge posting sometimes get the details wrong. These are the most costly errors to watch for.

Posting Only at the Checkout Counter

Card networks require surcharge disclosure at the point of entry and at the point of sale. Many merchants post only at the register and assume that’s sufficient. It isn’t, and a customer complaint can expose that gap quickly.

Exceeding the 3% Cap

Mastercard’s merchant support guidelines confirm that surcharges above 3% of the transaction amount violate the card network agreement, even when a merchant’s actual processing costs are higher than that limit.

Skipping the 30-Day Registration Requirement

Merchants must notify both Visa and Mastercard at least 30 days before charging any surcharge. Many businesses start collecting the fee first and register later. That makes the program non-compliant from day one, even if every notice is perfectly posted.

Applying the Surcharge to Debit Cards

Surcharges apply only to credit card transactions. You can’t charge fees on debit card payments, including prepaid cards. This rule comes from card networks and may also clash with federal payment laws.

Using an Outdated or Blank Effective Date

The effective date on your notice must match the actual start date of your surcharge program. A missing or old date brings up compliance issues and weakens the credibility of the whole disclosure.

Using Confusing or Jargon-Heavy Language

Customers should be able to read the notice and immediately understand what the charge is, why it applies, and what their payment alternatives are. Overly technical phrasing defeats the purpose of having a notice at all.

Not Updating the Notice When the Rate Changes

If the surcharge percentage goes up or down, the posted notice must be updated right away. An outdated rate creates customer confusion and opens a compliance gap that a single complaint can turn into a formal dispute.

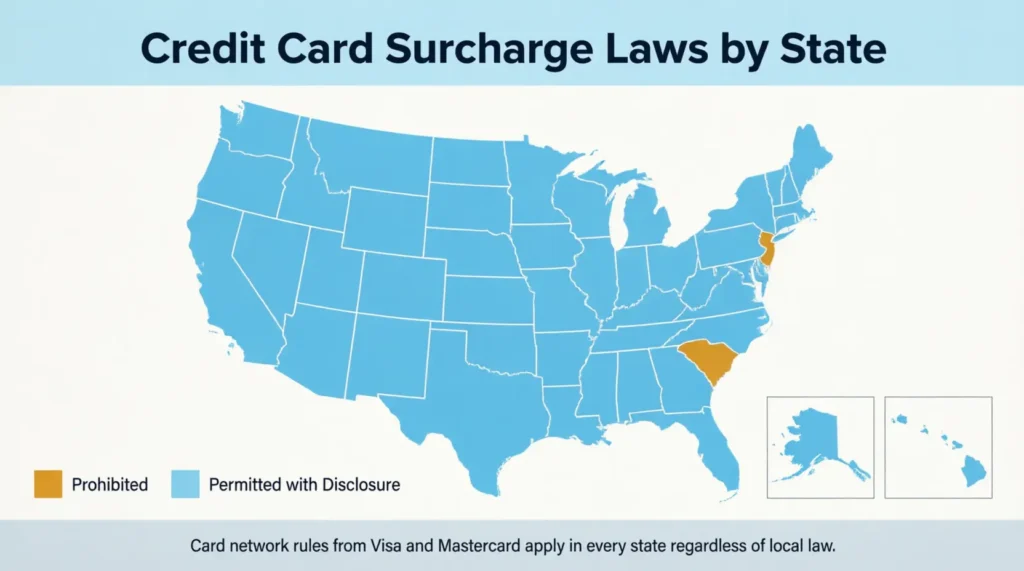

State-by-State Rules: What You Need to Know

Credit card surcharge laws vary significantly across the country. Before posting any notice or charging any fee, knowing the rules in your specific state is essential.

States That Currently Prohibit Credit Card Surcharges

Two states currently maintain enforceable bans on credit card surcharges:

- Connecticut: State law prohibits merchants from charging more than the listed price for credit card transactions.

- Massachusetts: Surcharges on credit card payments are explicitly banned under state law.

Businesses in these states can’t add a credit card surcharge. This rule applies no matter the notice given or the card network used.

States That Allow Surcharges with Proper Disclosure

Most US states let merchants add a credit card surcharge. They must give proper notice before the transaction. This shows a trend of court rulings recently. These rulings said that many state surcharge bans are unfair limits on commercial speech. States like California and New York, which once had active bans, now permit surcharging with proper disclosure.

Card Network Rules Apply in Every State

Even in states that permit surcharging freely, Visa and Mastercard rules still apply nationwide. The 3% cap, the 30-day advance registration, and the dual-location disclosure requirement all remain in effect everywhere in the US.

⚠️ Mistake to Avoid: State surcharge laws change. A state that allowed surcharging last year may have updated its rules. Always verify your current state rules through your state Attorney General’s website or a local business attorney before implementing any surcharge program.

A Note on Puerto Rico

Merchants in Puerto Rico should talk to local legal experts. There may be extra rules beyond the usual card network requirements.

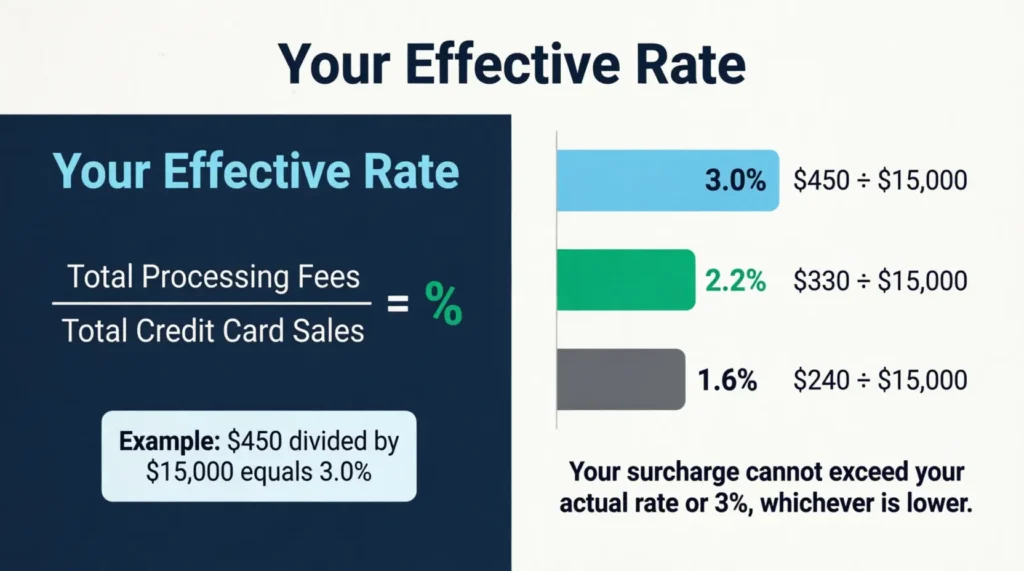

How to Calculate Your Surcharge Percentage

Your surcharge rate has two rules: it can’t exceed your real credit card costs. Also, it can’t go over 3%, the limit set by Visa and Mastercard. Both rules apply at the same time.

Step 1: Find Your Effective Processing Rate

Pull up your payment processor’s monthly statement. Find the total processing fees charged and the total credit card sales volume for that same period. Then divide the total fees by the total sales.

Total Processing FeesTotal Credit Card SalesYour Effective Rate $450$15,0003.0% ($450 ÷ $15,000) $330$15,0002.2% ($330 ÷ $15,000) $240$15,0001.6% ($240 ÷ $15,000)

Step 2: Choose a Rate at or Below Your Effective Rate

In the first example, the merchant’s actual cost is 3%, so 3% is the maximum compliant surcharge. Many merchants pick a lower round number, like 2.5%. This keeps them safely within the cap and helps them avoid compliance risks.

Step 3: Update Your Notice

After you choose a percentage, add it to your surcharge notice template. Then, update the example calculation table with the new figures.

💡 Pro Tip: Don’t automatically set your surcharge at the 3% maximum. If your actual processing rate is 2.2%, your surcharge must reflect that number. Charging more than your actual cost violates Visa and Mastercard merchant agreements, not just local law.

Alternatives to Charging a Credit Card Surcharge

A surcharge isn’t the only way to manage credit card processing costs. Depending on your business model, one of these alternatives may be a better fit.

Cash Discount Program

Instead of adding a fee for credit cards, offer a discount for cash payments. The listed price becomes the credit card price, and cash customers pay less. This sidesteps many surcharge regulations entirely because you’re lowering a price instead of adding a fee. Many modern payment processors can set up dual pricing at the terminal. This helps handle transactions automatically.

Convenience Fee

A convenience fee applies when a customer uses a specific payment channel that isn’t the standard option for that business. For example, A property management company might charge a convenience fee for tenants who pay rent online using a credit card. In contrast, tenants who pay in person at the office do not incur any fees. Convenience fees follow specific card network rules. It’s important to understand these rules before you implement one.

Minimum Purchase Requirement

Visa and Mastercard both allow merchants to set a minimum credit card purchase amount of up to $10.00. This lowers the effect of processing fees on small transactions. It does this without changing prices or adding new fees.

Dual Pricing

Some point-of-sale systems now support dual pricing, displaying both a cash price and a credit price on the same screen. Customers see both options and choose accordingly. This method is clear and simple to manage. It’s gaining popularity with small business owners who want to recover processing costs. They prefer this over a traditional surcharge program.

Each option has trade-offs. The best choice depends on your customers, how many transactions you have, and how your payment processor manages each program.

Tips for Explaining the Surcharge to Customers

Posting the notice handles the compliance side. Handling the conversation at checkout is a different skill. These tips make it easier for you and your team.

Train Your Staff Before Launch Day

Before posting any notice, ensure every employee knows the surcharge details. They should understand why it exists and how to respond if a customer questions it. A staff member who can’t explain the fee clearly makes the situation worse, not better.

Keep the Explanation Short and Direct

One phrase works well in almost every situation: “We charge a small processing fee for credit card payments. You can avoid it by paying with cash or a debit card.” That sentence covers the fact, the reason, and the alternative. It’s all the customer needs.

Point to the Posted Notice

If a customer seems surprised, gesture toward the notice and say: “It’s also posted at our entrance.” That reference shows your disclosure is in place and proper, which usually ends the conversation quickly.

Stay Matter-of-Fact

Processing fees are a real business cost. Framing the surcharge clearly, instead of apologetically, shows confidence. This approach helps maintain a professional tone in the interaction. Treating it as something to apologize for signals to the customer that it’s unusual, when in fact it’s an increasingly common and fully legal practice.

Acknowledge Customers Who Pay with Cash

A simple “Thanks for using cash” signals appreciation without making credit card users feel penalized. Small acknowledgments like this build goodwill over time.

How Our Templates Help You Save Time and Stay Compliant

Building a surcharge notice from scratch takes time, and getting the details wrong carries real consequences. These templates remove both problems at once.

Every template includes the sections that card networks expect:

- Surcharge disclosure statement

- Example calculation table

- Compliance language placeholder

- Merchant contact area

The formatting is clean, professional, and ready to print. All you need to add is your specific business details.

The Word versions give full editing flexibility. Change the font, adjust the layout, add your brand colors, or reword sections to match your business voice. PDF versions are perfect for businesses that need to print right away. They don’t require opening a word processor.

Both format types include a QR code placeholder. Linking that code to your full surcharge policy page gives customers a way to review the complete details before paying. That extra step builds trust and reduces in-person questions at the counter.

Four formats mean no compromise on size or paper type. US Letter for standard US printing. A4 for international businesses or those who prefer A4-size paper. Each format is sized and spaced to print cleanly on a single sheet.

Real-Life Example: How One Coffee Shop Used Our Template

Maria Chen, owner of Sunrise Brew in Portland, Oregon, absorbed credit card processing fees for three years. Then, she decided it was time to act. Her monthly processing costs were about $680, based on around $22,000 in credit card revenue. This means the effective rate was roughly 3.1%.

She downloaded the US Letter PDF template. Then, she filled in her business name. She set the surcharge to 3% and completed the example calculation table. She registered with both Visa and Mastercard 35 days before her launch. This kept her safely ahead of the 30-day requirement. On launch day, she laminated the completed notice and posted one copy at the front door and a second at the counter.

In the first week, three customers asked about the fee. Her barista, James, handled each one the same way: “It’s a small processing fee for credit cards. You’re welcome to use cash or a debit card to avoid it.” All three customers stayed and paid without further pushback.

By the end of her first full month with the surcharge, Maria recovered $620 of her $680 processing costs. That’s about 91% of a cost she had quietly managed for years. It was tackled with just one printed sheet and 35 days of planning.

Frequently Asked Questions (FAQ)

Is it legal to charge a credit card surcharge in the United States?

Credit card surcharges are legal in most US states, but Connecticut and Massachusetts currently prohibit them. Regardless of state law, Visa and Mastercard merchant rules must also be followed for any compliant surcharge program.

How much can a merchant charge as a credit card surcharge?

Visa and Mastercard both cap surcharges at 3% of the transaction amount. The surcharge can’t be more than your actual cost for accepting credit cards. So, the lower of the two amounts is the most you can legally charge.

Can a business apply a surcharge to debit card payments?

No. Credit card surcharges apply only to credit card transactions. You can’t apply the fee to debit cards, including prepaid ones. This rule is set by card networks and may also go against federal payment laws.

Do I need to notify Visa or Mastercard before adding a surcharge?

Yes. Visa and Mastercard require merchants to register their intent to surcharge. This must happen at least 30 days before the fee starts. Surcharging without prior registration is a rule violation. This holds true, even if your posted notice is well formatted.

Does the surcharge need to appear on the customer’s receipt?

Yes. The surcharge must be listed as a separate line on the receipt. This helps customers see exactly what they were charged.

What is the difference between a credit card surcharge and a convenience fee?

A surcharge applies to all credit card transactions at a business. A convenience fee is charged when a customer pays using a method that’s not the standard. For example, paying a bill by phone instead of in person will incur this fee.

Can I apply a surcharge to all credit card types, including business and rewards cards?

Yes. Surcharges can apply to all credit card types. The same 3% cap and disclosure requirements apply regardless of whether the card is personal, business, or a rewards credit card.

What happens if my surcharge exceeds the 3% cap?

Surcharges above 3% violate Visa and Mastercard merchant agreements. This can lead to formal warnings, financial penalties, or the termination of your ability to accept those card brands entirely.

Do I need a lawyer to write compliance language for my surcharge notice?

Not necessarily, but it’s smart to check your state Attorney General’s website for needed disclosure language. A local business attorney can check if your state has special wording rules before you post anything.

Can a customer refuse to pay the credit card surcharge?

Yes. Customers who don’t want to pay the surcharge can choose to pay with cash or a debit card instead. The purpose of a surcharge notice is to give customers an informed choice before the transaction is complete.

Bottom Line

Bottom Line

Managing credit card processing costs is a real challenge for small business owners. A clearly posted surcharge notice is one of the simplest ways to recover those costs while keeping customers fully informed.

Do it right:

- Know your state’s rules.

- Register with card networks 30 days ahead.

- Post the notice at both the entry and checkout.

- Stay at or below the 3% cap.

Using a credit card surcharge notice template is the best way for merchants to start their surcharge program. This guide covers the necessary compliance steps.

Share this guide. If you know a business owner paying processing fees each month, share this page with them.

Four free templates and a step-by-step guide can help them save hundreds of dollars each month while staying compliant.