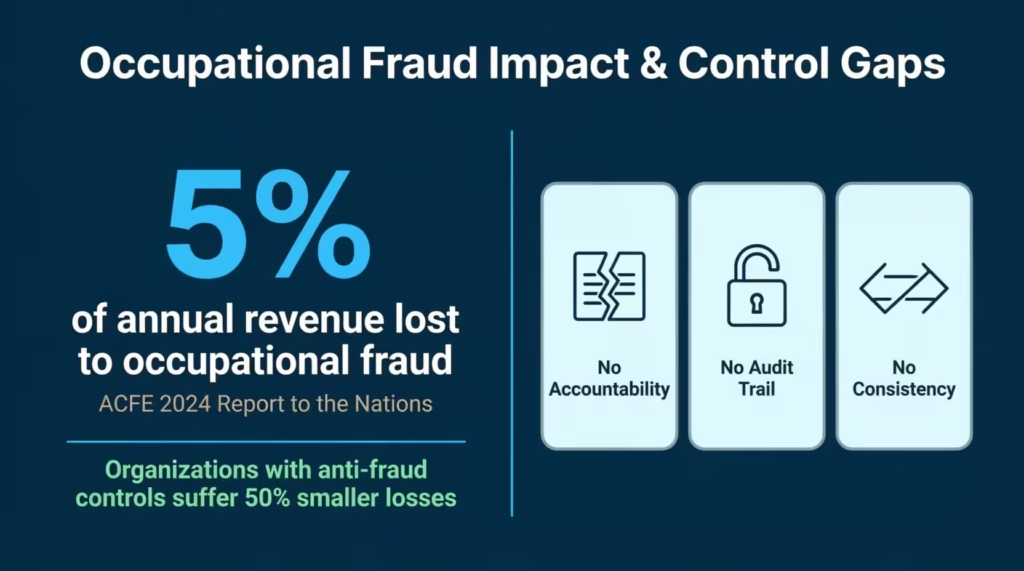

Managing employee spending without a written policy is a costly oversight no business can afford. The ACFE’s 2024 Report to the Nations found that organizations lose an estimated 5% of annual revenue to occupational fraud every year, and misuse of company-issued cards is one of the most common entry points.

Without a company credit card policy template, employees lack clear rules. This leaves your finance team with no basis to enforce any guidelines.

The fix is simpler than it sounds: put the rules in writing before handing out a single card.

Here are free templates in Word and PDF formats. You’ll also find a simple guide to help you fill them out and share your policy with your team.

Download Your Free Company Credit Card Policy Templates

Three ready-to-use templates are available to make your life easier. Each one has all the sections your policy needs. This includes card issuance rules, eligibility criteria, spending limits, and employee sign-off.

Pick the format and paper size that works best for you:

Disclaimer: The Templates & Printables on this site are provided for informational and personal tracking purposes only. This is not financial, legal, tax, or credit advice. While reasonable efforts are made to ensure accuracy, Credit Card Wind makes no warranties as to the completeness, reliability, or accuracy of the calculations generated by these Templates & Printables. Users are responsible for independently verifying all data and calculations. Terms, conditions, rates, regulations, and legal requirements vary by institution, jurisdiction, and individual circumstances.

Always refer to your official statements, account agreements, and applicable laws, and consult a qualified professional before making any financial, legal, or other important decisions. By using these Templates & Printables, you acknowledge that Credit Card Wind and its owner shall not be liable for any damages, losses, or financial consequences arising from the use or misuse of these Templates & Printables.

This universal disclaimer applies to all templates and printables provided by Credit Card Wind (https://creditcardwind.com), created by Robert Williams (Owner at Credit Card Wind).

© Credit Card Wind. All rights reserved.

These templates and printables may be downloaded and used for personal, non-commercial purposes only. Redistribution, resale, or modification for commercial use without permission is strictly prohibited.

What Is a Company Credit Card Policy?

A company credit card policy is a formal, written document that sets the rules for how employees can use a business-issued credit card. It explains who can get a card, what purchases are allowed, how much employees can spend, how to document expenses, and what happens if they break the rules.

Think of it as your organization’s rulebook for corporate spending. Without it, you’re relying on each employee to know the difference between a business dinner and a personal one. That’s not a safe assumption.

ACFE’s 2024 Report to the Nations data shows that organizations worldwide lose an estimated 5% of annual revenue to occupational fraud each year, with expense reimbursement schemes ranking among the most frequently reported fraud types. A well-written corporate card policy is one of the best ways for finance teams to prevent issues.

Why Every Business Needs One in Writing

Some small businesses skip the formal policy and rely on verbal guidelines or “common sense.” That approach creates three real problems.

No accountability. If the rules aren’t written down, employees can always claim they didn’t know what was allowed. You have no recourse.

No audit trail. Without a policy, auditors, courts, and regulators lack a guide when issues arise.

No consistency. One manager might approve a $200 team dinner without receipts. Another might flag a $12 parking charge. Written rules remove that inconsistency entirely.

Even a simple one-page document is better than nothing. A comprehensive, well-structured policy protects your business from every angle.

📌 Did You Know: The ACFE reports that organizations with strong anti-fraud controls suffer losses roughly 50% smaller than those without them. A written corporate card policy is one of the most consistently cited preventive controls in fraud risk management.

What Should a Company Credit Card Policy Include?

A strong corporate expense policy addresses all the key situations your finance team will face. Here’s a breakdown of every major section and why each one matters.

1. Purpose and Scope

This opening section explains why the policy exists and who it applies to. It should list all groups eligible for a company card. This includes full-time employees, contractors, and authorized representatives. Being explicit here prevents disputes later. Contractors especially may assume the rules don’t apply to them unless the policy says otherwise.

2. Card Issuance and Ownership

This section makes one thing crystal clear: the card belongs to the company, not the employee. It should also state that cards are non-transferable. Letting a colleague borrow your company card, even briefly, is a direct violation. All cards must be returned immediately upon request or upon leaving the organization.

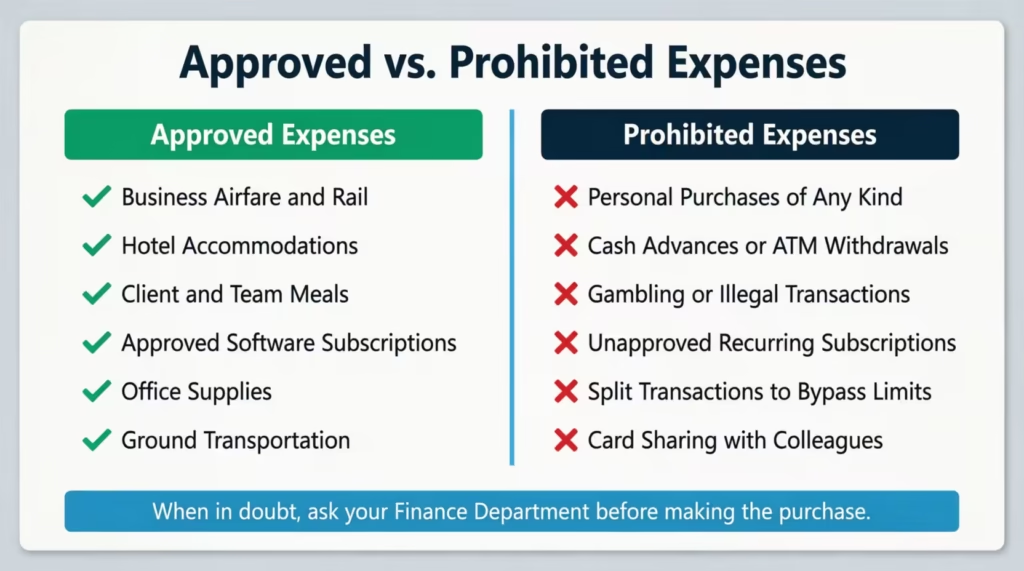

3. Authorized vs. Prohibited Expenses

This is the heart of your employee card usage policy. Be specific. Vague terms like “reasonable business expenses” invite interpretation and, eventually, abuse.

Common approved expense categories:

- Business travel (airfare, rail, ground transportation)

- Hotel accommodations for authorized business trips

- Client and team business meals

- Approved professional software subscriptions

- Office supplies when standard procurement isn’t available

Common prohibited uses:

- Personal purchases of any kind, regardless of intent to repay

- Cash advances or ATM withdrawals

- Gambling or illegal transactions

- Recurring subscriptions without prior written approval

- Splitting transactions to stay under single-transaction limits

That last point deserves attention. Splitting a $600 purchase into three $200 transactions to bypass an approval limit is policy abuse. It raises red flags for auditors.

⚠️ Mistake to Avoid: Don’t leave gray areas in your expense categories. If alcohol is permitted at client dinners but restricted at team lunches, state that explicitly. Vague language leads to misuse and disputes that are nearly impossible to resolve fairly.

4. Spending Limits and Controls

Each cardholder should have two limits assigned: a monthly spending limit and a per-transaction limit. The Finance Department sets these based on the employee’s role and actual business needs.

Some companies also implement Merchant Category Code (MCC) blocks. Card issuers set restrictions on where you can use the card. This means you can’t use it at certain places, like casinos, grocery stores, or electronics retailers.

All requests for a limit increase must be in writing. They need approval from the Finance Director before any purchase is made, not afterward.

5. Receipt and Documentation Requirements

No receipt. No reimbursement. That’s the standard rule, and it exists for good reason.

Cardholders must send original itemized receipts for any transaction over a set minimum, usually $25 or $50. Each receipt must clearly show:

- The vendor name

- The date of the transaction

- Items or services purchased

- The total amount charged

Digital scans and clear photos of receipts are generally acceptable. File all documentation through the company’s expense management platform, like Expensify, SAP Concur, or Ramp. Do this within the required number of business days.

💡 Pro Tip: Set a hard submission deadline, such as the 5th business day of the following month. Open-ended deadlines create last-minute rushes and incomplete records. Michael, a finance director at a mid-sized consulting firm, cut late expense submissions by 70%. He did this by adding an automated reminder in Expensify. This reminder is linked to the policy’s monthly cutoff.

6. Expense Review and Reconciliation

Monthly reconciliation is non-negotiable in any solid corporate card program. Each cardholder checks their statement. They match each charge to a receipt and flag any transactions they don’t recognize or dispute.

The Finance Department then conducts a second-level review to catch anything that was missed. Disputed charges should be reported to both the Finance team and the card issuer at the same time. Delays in reporting can affect the company’s chargeback rights.

7. Lost, Stolen, or Misused Cards

This section gives employees a clear, step-by-step action plan for an urgent situation. If a card is lost or stolen, the cardholder must:

- Contact the card issuer immediately to report and cancel the card.

- Notify the Finance Department and their direct manager within a set window, commonly within 4 hours.

- Cooperate fully with any follow-up investigation.

The company is not responsible for charges made after the card is officially reported. But if an employee delays reporting and fraud occurs during that gap, they may be held personally liable.

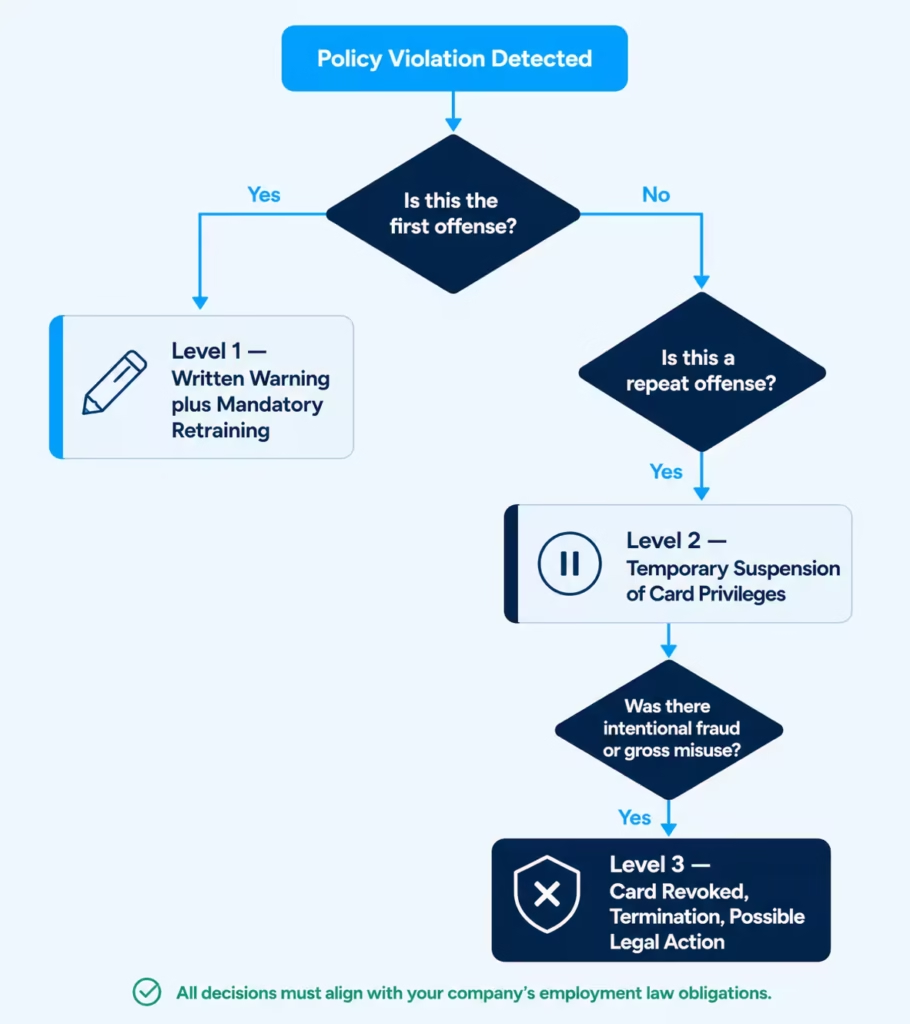

8. Policy Violations and Disciplinary Action

This section must be clear, firm, and fair. A tiered escalation structure works best.

- Level 1: Written warning and mandatory retraining

- Level 2: Temporary suspension of card privileges

- Level 3: Permanent revocation and possible termination

Intentional fraud, meaning using the card for personal gain with the intent to deceive, is a termination-level offense. The company may also pursue legal action in serious cases.

9. Audit and Compliance

The Finance Department should reserve the right to audit any card transaction at any time, without prior notice. Transaction records and receipts must be retained for a defined number of years. In most U.S. contexts, this ranges from three to seven years, depending on the applicable regulatory requirements.

All employees must cooperate fully with both internal audits and any external regulatory reviews.

10. Employee Acknowledgment

This final section is often the most overlooked, and yet it’s one of the most legally important parts of the entire document. Each cardholder must sign to confirm they received, read, and understood the policy. This protects the company if an employee later claims they were never informed of the rules.

Keep a signed copy on file for every cardholder. Digital signatures are valid in most U.S. jurisdictions.

How to Fill Out Your Company Credit Card Policy Template (Step by Step)

The template you downloaded covers all the sections above. Here’s exactly how to complete it without missing anything critical.

Step 1: Add Your Company Information

Start at the top. Replace every bracketed placeholder with your actual details:

- Your company’s full legal name

- A policy reference number (create a simple internal numbering format if you don’t have one)

- The effective date

- The version number (start at 1.0 for a new policy)

- The name and title of the approving authority

Replace the logo placeholder with your official company logo file.

Step 2: Define Who Is Eligible for a Card

In the Scope section, be precise about which roles qualify. For example: “All full-time employees at the Senior Manager level or above who regularly incur approved business travel expenses.”

If contractors are also eligible, state that explicitly and include any additional conditions that apply to them specifically.

Step 3: Set Spending Limits

Fill in the monthly and per-transaction limit fields in the Spending Limits section. Work with your Finance Director to determine appropriate amounts by role and business need.

Start conservative. Cardholders can ask for temporary increases by using the written exception process. This is for times when they truly need more flexibility.

Step 4: Clarify Approved and Prohibited Expenses

Review the expense categories table and customize it to match your organization. Add any industry-specific categories that are relevant to your business. Remove anything that doesn’t apply.

Be precise with restricted items. If alcohol is permitted at client dinners up to $50 per person, write that exact threshold in. Don’t leave it open to interpretation.

Step 5: Set Your Documentation Rules

Fill in your minimum receipt threshold and your firm submission deadline. For example: “All documentation must be submitted within 5 business days of the following month’s close.”

Name the expense management system your team uses. If you use Ramp, Expensify, or SAP Concur, add it by name. Remove any ambiguity about where expenses are filed.

Step 6: Define the Consequences

In the violations section, fill in the suspension duration for Level 2 offenses. Note whether the company pursues payroll deductions for unauthorized charges (where legally permitted in your state).

Have your legal team check this section before finalizing the policy. This is especially important if your company operates in different states or countries.

Step 7: Collect Employee Signatures

Once the policy is approved, distribute it to every current and future cardholder. Each person must sign the acknowledgment section before their card is activated.

Store signed copies in your HR or finance management system. Set a recurring calendar reminder to collect fresh signatures whenever the policy is updated.

💡Tip: Not sure what spending limit to set for company cards? Try the business credit card limit calculator before finalizing your policy.

Common Mistakes Companies Make With Corporate Card Policies

Even well-intentioned businesses stumble in a few predictable ways. Here are the most common ones.

Writing the policy once and forgetting it.

Business expenses change. Software subscriptions, remote work tools, and new expense categories are now big expenses. They didn’t even exist three years ago. A policy that isn’t reviewed regularly becomes outdated, and outdated rules are difficult to enforce.

Being too vague.

Language like “reasonable business expenses” is an open invitation for interpretation. One person’s reasonable team dinner is another’s $400 expense report.

Skipping the acknowledgment section.

Jennifer, a finance manager at a manufacturing company, dealt with a formal dispute. An employee claimed they weren’t told about the receipt documentation rules. She had no signed acknowledgment on file. The case dragged on for weeks before it was resolved in the employee’s favor.

Setting unrealistic spending limits.

When limits are too low, employees find ways to get around them. They might split transactions, use personal cards, and ask for reimbursement. Others may make unauthorized purchases and hope for forgiveness later. Each of these workarounds costs the business.

No exception-handling process.

Without a clear path for requesting limit increases, employees either overspend without approval or skip necessary purchases altogether. A documented exception request process solves both problems.

How to Enforce Your Corporate Card Policy Effectively

A policy that lives in a shared drive and never gets mentioned isn’t being enforced. Here’s how to make the rules genuinely stick.

Train every employee at onboarding.

Don’t just hand someone a card and a PDF. Walk through the key rules in a live or recorded onboarding session. Make sure new cardholders understand the consequences of violations before they ever use the card.

Use your expense platform to automate compliance.

Tools like Ramp and Expensify flag out-of-policy transactions automatically, send reminders for missing receipts, and can restrict specific merchant categories. Let the software do the heavy lifting where you can.

Review transactions monthly, every single month.

Even random spot-checks act as a strong deterrent. Employees who know their expenses may be reviewed tend to submit more accurate, complete reports.

Apply consequences consistently.

The biggest enforcement failure is uneven application of the rules. If a senior manager submits expenses without receipts and faces zero consequences, junior employees will notice. The policy loses its credibility fast.

💡 Pro Tip: Schedule a brief annual “policy refresh” meeting with all active cardholders. A 20-minute walk-through of any updates keeps the rules top-of-mind and signals clearly that the company takes expense compliance seriously.

When Should You Review and Update Your Policy?

A corporate expense policy isn’t a set-it-and-forget-it document. It needs to grow with your organization.

Review it at least once a year. A recurring annual calendar reminder works well here. Yearly reviews keep the policy current without creating a significant administrative burden.

Update it when your business changes. New offices in other states or countries, new expense software, or a new card issuer each trigger a policy review. What works for a 10-person team may not work for a 100-person organization.

Update it after a violation. If an incident exposed a gap in the policy rules, close that gap right away. David, a compliance officer at a regional logistics company, updated the corporate card guidelines. An employee had argued that food delivery app charges weren’t clearly covered by the old policy. That gap was closed the next business day.

Update it when laws change. Tax rules, labor laws, and financial regulations affecting expense management shift regularly. Consulting your legal and tax advisors during every annual review keeps the policy compliant and defensible.

Legal Considerations for Corporate Credit Card Policies

Every policy has legal implications. Keep these in mind.

Payroll Deduction Laws

Some states allow companies to deduct unauthorized charges from paychecks. Others don’t. Check your local laws before including this in your policy.

Employee Privacy

You have the right to watch the card use. But be transparent about it. Tell employees that transactions will be reviewed.

Tax Compliance

Proper documentation helps with taxes. Receipts prove that expenses were for business. This protects your company during an IRS audit.

Liability for Fraud

If an employee commits fraud, the company may be liable until the card is reported lost or stolen. Your policy should make reporting mandatory within a specific timeframe.

Employment Law Compliance

Terminating someone for policy violations must follow employment law. Consult with HR or legal counsel before taking action.

Frequently Asked Questions (FAQs)

What should a company credit card policy include?

A complete policy covers card eligibility, approved and prohibited expense categories, spending limits, receipt and documentation requirements, the reconciliation process, disciplinary consequences for violations, and an employee acknowledgment section with a signature line.

Can employees use a company credit card for personal expenses?

No. Personal purchases on a company card are prohibited under virtually all corporate card policies, even if the employee plans to repay the company. This applies regardless of the dollar amount involved.

What happens if an employee misuses a company credit card?

Consequences typically follow a tiered structure: a written warning and mandatory retraining for minor violations, suspension of card privileges for repeat offenses, and termination or potential legal action for intentional fraud or gross misuse of company funds.

Do employees need receipts for all company card transactions?

Most corporate policies need itemized receipts for purchases over a set limit, usually $25 to $50. Some organizations require receipts for every transaction, regardless of the amount.

How often should a company’s credit card policy be reviewed?

At a minimum, once per year. The policy needs updating after major business changes, any rule violations, or updates to laws and regulations.

Who is responsible for approving company credit card expenses?

The Finance Department typically handles final review and reconciliation. Department heads can approve expenses in their budget. The Finance Director approves requests for spending limit increases or policy exceptions.

Can a company deduct unauthorized card charges from an employee’s paycheck?

In many U.S. states, payroll deductions for unauthorized card use are allowed. This happens if the policy clearly states this consequence and the employee has signed an acknowledgment. Laws vary significantly by state, so legal review is always recommended before pursuing this route.

What is a Merchant Category Code (MCC) block?

An MCC block is a restriction set by the card issuer. It prevents a company card from being used at certain merchants. This includes casinos, grocery stores, and entertainment venues. This rule relies on standard codes for each type of business.

Conclusion

A strong corporate card policy is one of the most practical financial controls a business can have. It protects against fraud, removes uncertainty for employees, and gives your Finance team a clear framework to enforce.

The best approach is to begin with a well-structured company credit card policy template. Then, customize your spending limits and approved expense categories to fit your organization. Finally, collect a signed acknowledgment from every cardholder before activating their card. That single step prevents the majority of disputes before they ever start.

If this guide helped you get your corporate spending policy in order, share it with a business owner or finance manager on your team. Clear, written expense rules can save a small business thousands of dollars every year.