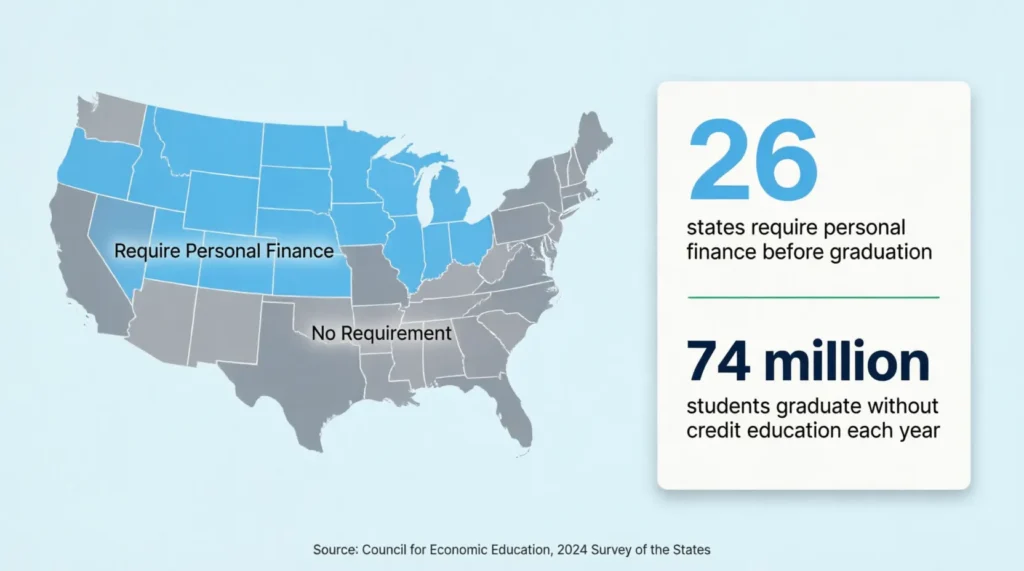

Managing a credit card in college can feel overwhelming. Most students receive their first card without any training on APR, minimum payments, or credit utilization, and the costs of that gap add up fast. According to the Council for Economic Education’s 2024 Survey of the States, only 26 states require a personal finance course before high school graduation.

A credit card worksheet for students is the simplest way to take control. Track your charges, calculate your utilization, and stay on top of every payment from day one.

Keep reading. This guide includes the basics, free downloadable worksheets, and practical tips to keep your credit score safe for years.

Download Your Free Credit Card Worksheets for Students

Two ready-to-use worksheet packs are available below. Each one is fully formatted and includes every section you need to start tracking right away. Pick the format and paper size that works best for you:

This pack includes:

- A glossary of key terms

- A monthly credit card budget worksheet

- A payment tracker with practice exercises

- A credit knowledge quiz

This version has:

- A detailed glossary.

- A monthly budget worksheet with a notes column and category ideas.

- A 3-month payment tracker with math practice problems.

- A credit quiz with reflection prompts.

- A fully completed sample worksheet with practice solutions.

Disclaimer: The Templates & Printables on this site are provided for informational and personal tracking purposes only. This is not financial, legal, tax, or credit advice. While reasonable efforts are made to ensure accuracy, Credit Card Wind makes no warranties as to the completeness, reliability, or accuracy of the calculations generated by these Templates & Printables. Users are responsible for independently verifying all data and calculations. Terms, conditions, rates, regulations, and legal requirements vary by institution, jurisdiction, and individual circumstances.

Always refer to your official statements, account agreements, and applicable laws, and consult a qualified professional before making any financial, legal, or other important decisions. By using these Templates & Printables, you acknowledge that Credit Card Wind and its owner shall not be liable for any damages, losses, or financial consequences arising from the use or misuse of these Templates & Printables.

This universal disclaimer applies to all templates and printables provided by Credit Card Wind (https://creditcardwind.com), created by Robert Williams (Owner at Credit Card Wind).

© Credit Card Wind. All rights reserved.

These templates and printables may be downloaded and used for personal, non-commercial purposes only. Redistribution, resale, or modification for commercial use without permission is strictly prohibited.

Why Students Need Credit Card Worksheets

Getting your first credit card is exciting. But without a plan, it can quickly become a source of stress.

Most students step onto campus not knowing how credit utilization works. They’re often unaware of the consequences of only paying the minimum. A single missed payment can haunt them for years. That’s not a personal failure. It’s a system gap. And a structured monthly tracking tool bridges that gap directly.

A student spending tracker gives you a visual, hands-on way to connect your spending decisions to real financial outcomes. Instead of abstract concepts, you watch your balance climb and fall with every entry you log.

Budgeting apps show you what happened. A worksheet makes you think through what’s happening right now. That difference matters more than most students expect.

The Real Cost of Not Tracking

Credit card interest compounds quickly on a student budget. If your card carries a 22% APR and you hold a $600 balance while making only minimum payments, you’ll still be paying it off years later. A monthly tracking habit helps you spot that pattern before it becomes a long-term problem.

What’s Included in These Credit Card Worksheets

The worksheet packs in this guide were built to do more than log transactions. Each section teaches you how to think about credit at the same time you’re tracking it.

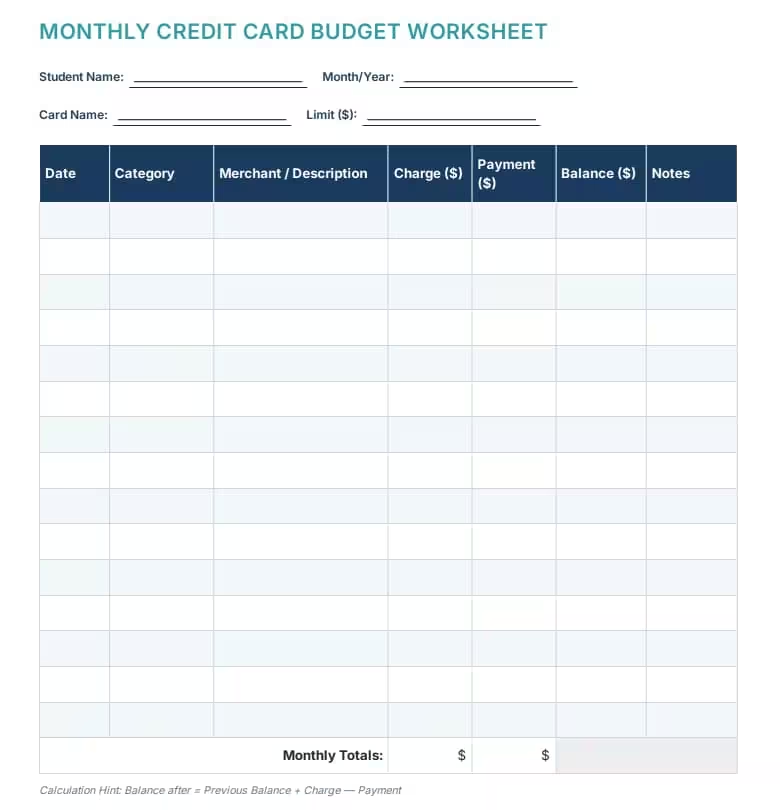

Monthly Credit Card Budget Worksheet

This is the core section of each pack. It’s a log-style table where you record:

- The date of each transaction

- The spending category (food, transport, subscriptions, books, etc.)

- The merchant or description

- The charge amount

- Any payments made

- Your running balance after each entry

At the bottom, a utilization calculator lets you check your credit utilization ratio at a glance. The formula is simple: divide your current balance by your credit limit, then multiply by 100. The A4 version also includes a notes column and a category suggestions list to help you get organized from the start.

Payment Tracker and Practice Exercises

This section keeps a running record of your payment history. You log your statement balance, minimum payment due, the date you paid, and the amount paid.

The A4 version tracks three months at a time and includes three math practice problems. One example: if your balance is $1,200 at a 19% APR and you pay only the minimum, how does your interest charge compare to paying the balance in full? Working through these problems by hand makes the numbers stick in a way a calculator app never quite does.

Credit Knowledge Quiz

This short quiz covers the three to five concepts students most commonly get wrong. What actually lowers your utilization? What does APR stand for? What is a healthy credit score? The reflection box at the end asks you to write two things you’ll do differently next month. That small step turns a worksheet into a lasting habit.

Sample Filled Worksheet (A4 Version Only)

The A4 pack includes a fully completed example. You can see exactly how a student named Alex Rogers filled in their October 2025 transactions across categories like Transport, Dining, Books, and Subscriptions. This removes the guesswork from getting started and gives you a clear model to follow.

Understanding Credit Card Basics for Students

Before you fill in a single row of your worksheet, it helps to understand what you’re tracking and why it matters. According to the Council for Economic Education’s 2024 Survey of the States, only 26 states require students to complete a personal finance course before graduating high school. That means millions of students arrive at college without a working understanding of how credit actually works.

APR (Annual Percentage Rate)

APR is the yearly cost of borrowing money on your card. If your APR is 22% and you carry a $1,000 balance for a full year, you’ll pay roughly $220 in interest alone. Most student credit cards carry APRs between 19% and 27%, depending on your credit profile and card issuer.

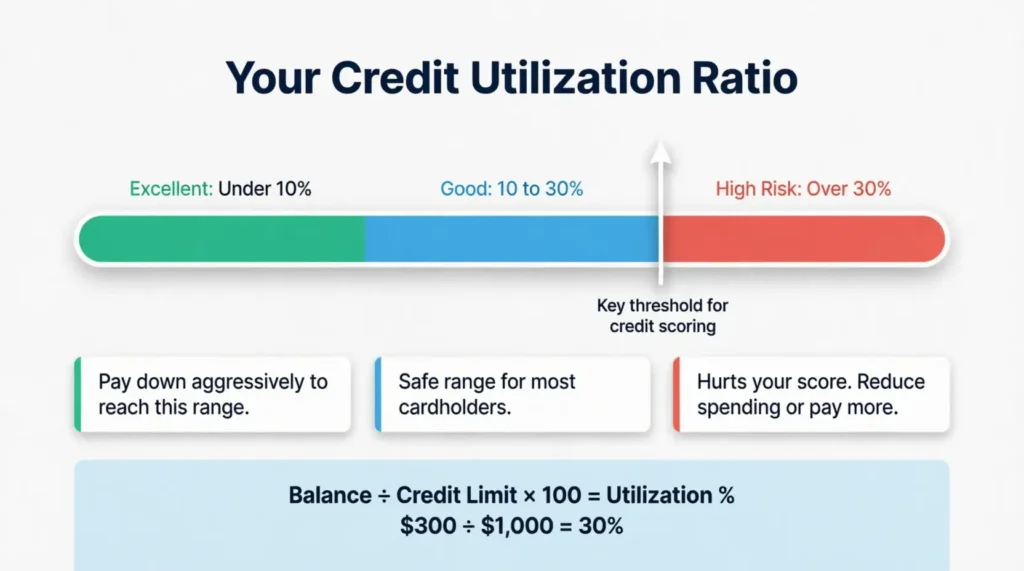

Credit Utilization

Credit utilization is the percentage of your total credit limit that you’re currently using. A $300 balance on a $1,000 limit equals 30% utilization. Keeping this figure below 30% is a widely cited benchmark for maintaining a healthy credit score. Dropping it below 10% tends to produce the strongest results for active credit builders.

Minimum Payment

The minimum payment is the smallest amount you must pay by your due date to avoid a late fee. Paying only the minimum keeps the account in good standing on paper — but the remaining balance keeps accruing interest every day. It’s a legal option, but it can turn a manageable debt into a much larger one over time.

Statement Cycle and Grace Period

A statement cycle is typically 30 days. At the end of each cycle, your card issuer calculates your balance and sends a statement. Your payment due date is usually 21 to 25 days after the statement closes. Pay your full balance before that due date and you owe zero interest for the entire cycle.

📌 Did You Know: You can carry a high-APR card and never pay a single dollar in interest. Interest only applies when you carry a balance past the due date. Pay in full every month, and your APR becomes irrelevant.

How to Use Your Credit Card Worksheet Effectively

The worksheets in this guide are straightforward to fill out. Follow these steps to get the most from each month’s sheet.

Step 1: Set Up Your Header Information

At the top of the monthly budget worksheet, fill in your name, the month, your card name, your cardholder name, and your credit limit. This takes less than a minute and keeps every month’s sheet clearly labeled and easy to reference later.

Step 2: Log Every Transaction the Day It Happens

Don’t let charges pile up at the end of the week. Logging each transaction the same day helps keep your balance accurate. It also makes it easy to spot any unfamiliar entries quickly. Record the date, spending category, merchant name, charge amount, and updated balance.

💡 Pro Tip: Set a 60-second phone reminder each evening to update your worksheet. Students who log daily report far fewer billing surprises than those who batch-update at the end of the month.

Step 3: Calculate Your Monthly Totals

At the end of the month, add up your total charges and total payments. The A4 version includes a dedicated Monthly Totals row for this purpose. Then run your utilization check: divide your ending balance by your credit limit and multiply by 100.

Step 4: Complete the Payment Tracker

Move to the Payment Tracker section and fill in your statement balance, minimum payment due, the date you paid, and how much you actually paid. Record this on the day you make the payment for the most accurate monthly history.

Step 5: Work Through the Credit Knowledge Quiz

Use the quiz section once a month, not just when you first download the worksheets. Each time you work through it, you reinforce the core concepts. The reflection prompts at the end are worth taking seriously. Writing down two specific actions to take next month builds habits more effectively than simply reading through the answers.

Budgeting With Your Credit Card Worksheet

A college budget worksheet does something a spending app can’t fully replicate: it slows you down.

When you log a transaction by hand, you’re forced to think about it. You see the running balance change. You feel the category total grow. That friction is intentional, and it works.

Category Tracking Keeps You Honest

The Monthly Budget Worksheet includes a Category column. Group your spending into buckets like Food, Transport, Books, Subscriptions, and Entertainment. At the end of the month, look at which category carried the highest total.

Take Maya, a sophomore studying communications, who used the worksheet for the first time last semester. She discovered she had spent $215 that month on food delivery — nearly 40% of her part-time income. Seeing that total in one column, written in her own handwriting, made the pattern impossible to ignore. She brought it down to $75 the following month.

Set a Spending Target Before the Month Starts

Before a new month begins, write a planned spending limit for each category at the top of your worksheet. Keep your total planned spending well below your credit limit. This gives you a benchmark to compare against your actual charges at the end of the month and turns tracking into a proactive habit, not just a record.

⚠️ Mistake to Avoid: Never treat your credit limit as your budget. A $2,000 limit is not an invitation to spend $2,000. High utilization hurts your credit score, and it puts you one late paycheck away from carrying an expensive balance.

Common Credit Card Mistakes Students Make

Even careful, motivated students fall into the same traps. Knowing what they are makes them much easier to avoid.

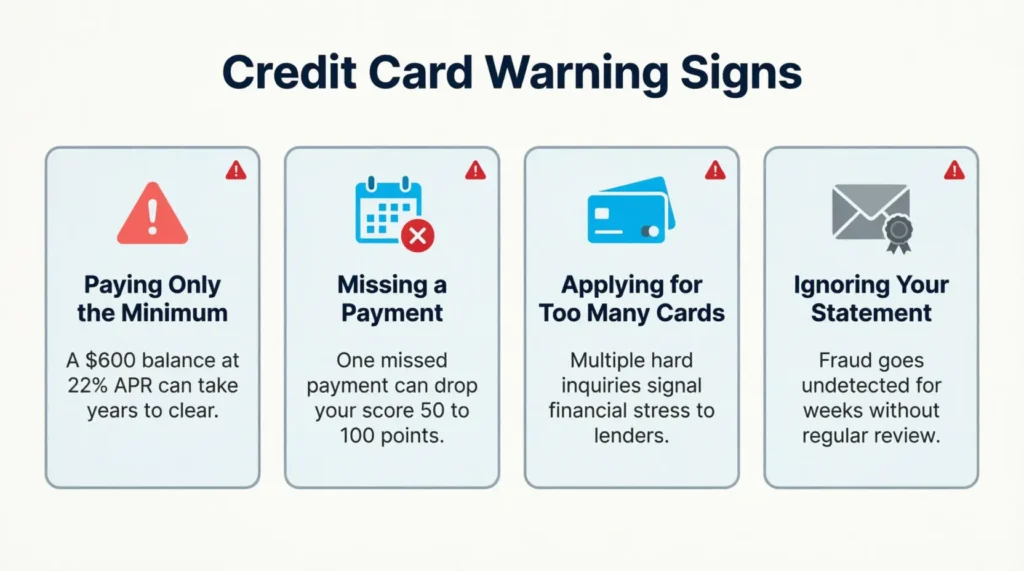

Paying Only the Minimum

This is the single most expensive habit on the list. A $600 balance at 22% APR, paid with minimum-only payments, can take years to fully clear and cost nearly double the original balance in total interest. The payment tracker exercises in your worksheet help make math clear and personal.

Missing a Payment Entirely

A single missed payment can drop a credit score by 50 to 100 points, depending on where it starts. It also triggers a late fee and may activate a penalty APR on some cards. Setting up autopay for at least the minimum payment makes this mistake nearly impossible.

Applying for Several Cards at Once

Each credit card application generates a hard inquiry on your credit file. Multiple inquiries in a short window signal financial pressure to lenders and temporarily lower your score. Start with one card, build a track record over 12 or more months, and only then consider adding a second.

Ignoring Your Monthly Statement

Your statement contains every charge, your minimum payment, your due date, and your APR. Not reading it is how fraudulent charges go unnoticed for weeks. Make it a habit to review your statement the same day it arrives or within 24 hours.

Smart Credit Card Strategies for Students

Responsible card management is not only about avoiding mistakes. It’s also about using credit deliberately to build something valuable over time.

Pay Your Full Statement Balance Every Month

Paying the full statement balance each month eliminates interest charges entirely. On a student card with a 24% APR, this single habit can save hundreds of dollars per year compared to carrying even a small recurring balance.

Keep Your Utilization Consistently Low

Use your card regularly, but keep the balance small relative to your limit. Aim for no more than 30% utilization at any given time. If you’re actively trying to build credit, staying under 10% tends to produce the fastest score improvement.

Assign Your Card to One Spending Category

Pick one category for credit card use — groceries, gas, or monthly subscriptions — and use cash or debit for everything else. This limits your exposure while keeping the card active and reporting to the credit bureaus each month.

Set Up Automatic Payments

Most card issuers let you schedule automatic payments for your full statement balance each month. If your income is unpredictable, set autopay for the minimum payment and pay the rest manually before the due date. Either way, never miss the payment window entirely.

Building Credit as a Student

One of the most valuable steps you can take in college is building a strong credit history. Credit scores impact apartment applications, auto loans, and some finance job offers. Starting early gives you years of positive history before those moments arrive.

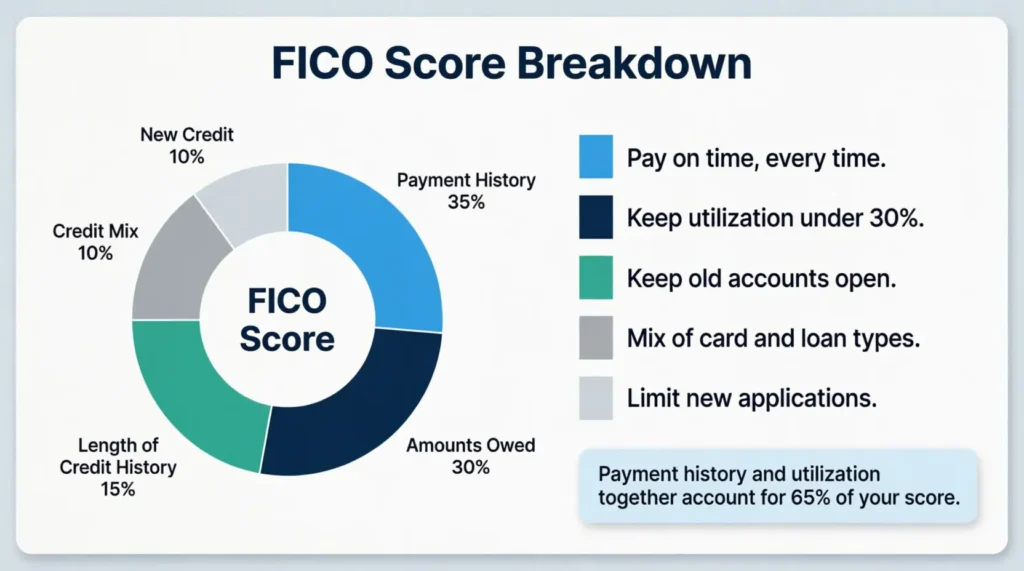

How Your FICO Score Is Calculated

FICO scores, the top model used in lending, fall into five categories:

| Factor | Weight |

|---|---|

| Payment history | 35% |

| Amounts owed (utilization) | 30% |

| Length of credit history | 15% |

| Credit mix | 10% |

| New credit inquiries | 10% |

Payment history and utilization together account for 65% of your score. Those are precisely the two things your monthly worksheet tracks most directly.

Getting Started With No Credit History

Two great options for students with no credit history are:

- A secured credit card, where you deposit cash equal to your limit as collateral.

- A student credit card made for those with limited credit profiles.

Use it for one or two regular monthly purchases and pay the full balance each month.

Checking Your Credit Report for Free

Every consumer in the United States is entitled to a free credit report from each of the three major bureaus every 12 months through AnnualCreditReport.com. Review yours at least once per year for errors. A single incorrect late payment or unfamiliar account could be pulling your score down without your knowledge.

What to Do If You’re Struggling With Credit Card Debt

Carrying credit card debt on a student budget is stressful. But there are concrete steps to work through it.

Stop Adding to the Balance

The first step is straightforward: stop using the card for new purchases while you pay down the existing balance. Switch to cash or a debit card for daily spending and direct all available money toward what’s already owed.

Pay More Than the Minimum Each Month

The minimum payment keeps your account current but barely touches the principal. Pay as much above the minimum as your budget allows. Even an extra $20 to $30 per month accelerates your payoff timeline noticeably and cuts your total interest cost over time.

Call Your Card Issuer

Many students don’t realize that card issuers often run hardship programs. A short phone call can sometimes result in a temporary rate reduction, a waived late fee, or a modified payment arrangement. Issuers generally prefer to work with a struggling cardholder rather than absorb the cost of a default.

Use Free Financial Counseling Through Your Campus

Many colleges and universities provide free one-on-one financial counseling. You can find this service at the student affairs or financial aid office. A counselor can help you build a payoff plan and review your options. They will keep you accountable, all without any sales pressure and at no cost to you.

Credit Card Safety and Security Tips

Using a credit card safely is just as important as using it wisely. Fraud and identity theft hit younger cardholders more often. This is partly because new users check their accounts less often.

Check Your Account at Least Once a Week

Log in to your card account weekly to scan recent transactions. Fraudulent charges are far easier to dispute when caught early. The Consumer Financial Protection Bureau outlines your full rights as a cardholder, including the process for reporting and disputing unauthorized activity.

Never Share Your Card Details

Your card number, expiration date, and CVV should never be shared via text, email, or phone unless you initiated the contact. No legitimate card issuer will ever ask for your full card number through an email message.

Use Virtual Card Numbers for Online Shopping

Many issuers now offer virtual card numbers for online purchases. A virtual number links to your real account but is unique to a single merchant. If a retailer suffers a data breach, your actual card number stays protected.

Consider a Credit Freeze When You’re Not Applying for Credit

If you’re not actively seeking new accounts, placing a security freeze on your credit file with all three bureaus is a free and simple step. A freeze blocks anyone from opening new credit in your name. It takes just a few minutes to set up and can be lifted instantly whenever you need to apply for something.

Maximizing Credit Card Rewards as a Student

Not every student card offers rewards — but many do. A small amount of strategy makes a meaningful difference over time.

Know Exactly How Your Card Earns

Some student cards offer a flat cash-back rate on all purchases. Others pay higher rates in specific categories like dining, streaming services, or gas. Before deciding which purchases to route through your card, read the rewards schedule in your card’s terms or mobile app.

Redeem on a Regular Schedule

Unredeemed points and cash back sit idle and earn nothing while they wait. Set a quarterly calendar reminder to redeem your rewards. Most cards let you apply cash back directly as a statement credit, which reduces your balance and effectively lowers your cost of living.

Rewards Are a Bonus, Not a Reason to Spend More

This is a trap that catches even experienced cardholders. Buying things you wouldn’t otherwise purchase just to earn points always costs more than the reward is worth. Earn on spending you’d make anyway and let the cash back be a bonus, never a motivation.

When to Consider Getting a Second Credit Card

A second credit card increases your total available credit. It can lower your overall utilization ratio, but only if you’re genuinely ready for the added responsibility.

Consider a second card only if all four of these conditions apply:

- Your first card has been open for at least 12 months

- Every payment has been on time without exception

- Your utilization is consistently below 30%

- You have a specific, practical reason for adding it (such as better rewards in a category you use regularly)

If any of those conditions aren’t yet in place, wait. A second card adds complexity. And complexity creates the conditions for missed payments if your tracking system isn’t fully locked in.

💡 Pro Tip: When you do add a second card, choose one that fills a gap your first card doesn’t cover. If your first card earns dining rewards, your second might focus on travel, groceries, or gas.

Tracking Credit Card Use: Digital vs. Paper Worksheets

Both methods work. The best choice is whichever one you’ll actually use consistently every month.

Why Paper Worksheets Work Well for Students

Writing by hand activates memory differently from typing. Research in educational psychology consistently shows that handwritten note-taking improves retention and comprehension. For students still building financial habits, the physical act of writing a charge creates a brief pause that digital entry skips. That pause is where awareness develops.

Paper worksheets can be used offline. They never crash and need no subscription. Plus, they don’t compete with push notifications for your attention. The packs in this guide are designed for exactly this kind of intentional, low-friction monthly review.

Why Digital Tools Have Their Place

Apps and bank dashboards offer real-time account sync, automatic categorization, and instant spending alerts. If you make many small transactions every week across different accounts, a digital tool might be better for tracking them.

The Hybrid Approach

Many students find the best results using both together. The banking app catches every transaction automatically. The monthly worksheet forces a structured, intentional review of the totals. Together, they build both awareness and habit without relying entirely on either one.

Resources for Student Credit Card Management

A range of free, trustworthy resources can help you go further with credit management:

- Consumer Financial Protection Bureau (CFPB): Free tools, guides, and complaint resources for credit card users. Their student-focused content is especially practical for first-time cardholders.

- AnnualCreditReport.com: The official government-authorized source for free annual credit reports from all three major bureaus.

- Your campus financial aid office: Many colleges offer free one-on-one counseling, sometimes with no appointment required.

- Your card issuer’s education center: Discover, Capital One, Chase, and most major issuers publish free financial literacy resources designed specifically for new cardholders.

- National Endowment for Financial Education (NEFE): Publishes free research and practical tools focused on young adult financial skills.

Long-Term Financial Habits Beyond Worksheets

A monthly tracking tool is a starting point, not the finish line. The habits you build now become the financial foundation you carry through every decade ahead.

Expand to a Full Monthly Budget

Once you track card spending well, add all income sources and expense categories to your system. The 50/30/20 framework is a useful guide for young adults with variable incomes. It suggests spending 50% on needs, 30% on wants, and 20% on savings and debt payoff.

Build a Small Emergency Fund First

Before focusing on rewards optimization or credit score tactics, build a basic emergency fund. Even a $500 to $1,000 set aside can prevent a car repair or medical bill from becoming new credit card debt. This single step reduces your dependence on credit during high-stress moments.

Think of Your Credit Score as a Long-Term Asset

A credit score isn’t just a three-digit number. It’s a financial credential that follows you for life. Students who score above 700 get better loan rates, rental terms, and insurance premiums. Those who score lower miss out on these benefits. Every month of responsible card use contributes to that outcome.

Revisit Your Worksheet Setup Each Semester

Financial needs change. At the start of each new semester, review your spending categories, monthly limits, and payment setup. What worked with a lighter course load might need changes during finals or an unpaid internship when money is tight.

Frequently Asked Questions

What does a student credit card worksheet include?

A student credit card worksheet usually has a monthly transaction log, a payment tracker, and a credit utilization calculator. It also includes a quiz or reflection section. This helps reinforce key ideas like APR, minimum payments, and credit limits.

How often should I fill out my credit card worksheet?

Log transactions daily or every few days to keep your running balance accurate. Finish the monthly summary each time the statement cycle ends. This includes the payment tracker and the utilization calculation.

What is a good credit utilization ratio for students?

Staying below 30% is the standard recommendation for a healthy credit score. Keeping utilization below 10% tends to produce the best results for students actively building credit.

Does tracking my spending actually improve my credit score?

A worksheet itself does not change your score, but the habits it reinforces do. On-time payments and low utilization together account for 65% of your FICO score.

What is the difference between the minimum payment and the statement balance?

The minimum payment is the smallest amount required by your due date to avoid a late fee. The statement balance is the full amount owed. Paying only the minimum leaves the rest subject to daily interest charges.

How many credit cards should a college student have?

Starting with one card is the standard recommendation. A second card can be considered after at least 12 months of on-time payments and consistently low utilization.

What happens if I miss a credit card payment?

A missed payment typically triggers a late fee and may raise your interest rate. If the payment is more than 30 days late, it gets reported to the credit bureaus and can lower your score by 50 to 100 points.

Is it safe to use a credit card for online shopping?

Yes, with precautions in place. Use virtual card numbers when your issuer offers them. Shop only on secure websites to ensure safety. Review your account weekly for any charges you do not recognize. This helps protect against fraud.

What is the grace period on a credit card?

The grace period is the window between your statement closing date and your payment due date, typically 21 to 25 days. Paying your full balance within this window means you owe no interest for that billing cycle.

Do student credit cards report to the credit bureaus?

Yes. Student credit cards report account activity to all three major bureaus. Every on-time payment builds positive credit history, and every missed payment or high balance affects your score.

Bottom Line

Managing a credit card in college relies on three key points:

- Understand how credit works.

- Track your spending each month.

- Pay your full balance whenever you can.

This guide covers key concepts like APR, utilization, payment history, and statement cycles. These are the basics for a strong financial life.

For many students, a structured monthly tracking system works best. It shows the numbers clearly before they turn into problems. The free worksheets in this guide are designed to make that easy. If you know a college student who needs help with credit card spending, share this page. It might save them years of interest and stress.