Running out of credit room mid-billing cycle can stall vendor payments and slow business growth, especially when revenue is rising but your limit isn’t keeping up.

About 40% of employer firms sought new financing in the prior year, with cash flow constraints listed among the most common challenges, according to the Federal Reserve’s 2024 Small Business Credit Survey.

A poorly written request for a company credit limit increase usually gets ignored. It often ends up at the bottom of the review pile before anyone even looks at it.

A formal, well-documented letter with a specific, justified request is the fastest path to getting your bank to say yes.

This guide offers free templates and a step-by-step walkthrough. You’ll learn what to include, how to write a strong reason, and what to do if your bank needs more convincing.

Download Your Free Company Credit Limit Increase Request Templates

Four ready-to-use templates are available here. Each one is professionally structured with every section your bank expects to see.

Pick the format that works best for you:

Disclaimer: The Templates & Printables on this site are provided for informational and personal tracking purposes only. This is not financial, legal, tax, or credit advice. While reasonable efforts are made to ensure accuracy, Credit Card Wind makes no warranties as to the completeness, reliability, or accuracy of the calculations generated by these Templates & Printables. Users are responsible for independently verifying all data and calculations. Terms, conditions, rates, regulations, and legal requirements vary by institution, jurisdiction, and individual circumstances.

Always refer to your official statements, account agreements, and applicable laws, and consult a qualified professional before making any financial, legal, or other important decisions. By using these Templates & Printables, you acknowledge that Credit Card Wind and its owner shall not be liable for any damages, losses, or financial consequences arising from the use or misuse of these Templates & Printables.

This universal disclaimer applies to all templates and printables provided by Credit Card Wind (https://creditcardwind.com), created by Robert Williams (Owner at Credit Card Wind).

© Credit Card Wind. All rights reserved.

These templates and printables may be downloaded and used for personal, non-commercial purposes only. Redistribution, resale, or modification for commercial use without permission is strictly prohibited.

What Is a Company Credit Limit Increase Request Letter?

A company credit limit increase request letter is a formal document a business submits to its bank or credit card issuer. It asks the financial institution to raise the borrowing limit on a current corporate credit account or facility.

Unlike personal credit requests, which can often be handled online in minutes, business credit limit requests typically require a written submission with proper documentation. Banks see these requests as a mini credit review. So, the format, content, and documents matter a lot.

A good request letter should include four key things:

- Your company and account details

- Your current limit and the amount you’re asking for

- A clear reason for the increase

- Financial documents that support your request

📌 Did You Know: The Federal Reserve’s 2024 Small Business Credit Survey found that nearly 4 in 10 employer firms applied for financing in the prior year, yet many reported receiving less than the full amount they requested. A well-structured credit increase letter with solid documentation can boost your chances of full approval.

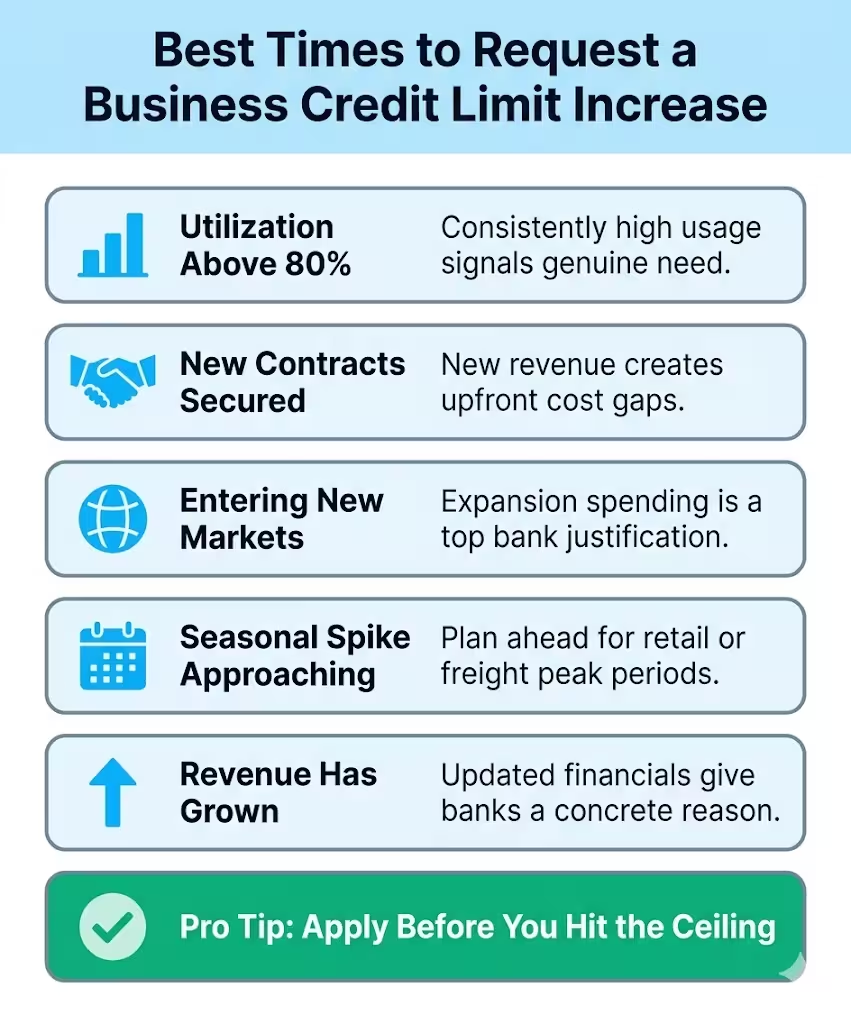

When Is the Right Time to Request a Higher Business Credit Limit?

Timing your request well can make a significant difference. Banks are more likely to act quickly when your business is in a strong financial position, and the reason for the request is well-documented. Here are the most common situations where a formal request makes sense.

Your utilization is consistently high. If your business often uses 80% or more of its credit limit, it shows the limit isn’t enough for your needs. The sample letter in the formal template shows a logistics company with 88% monthly utilization. This high rate was causing delays in mid-cycle payments.

You’ve secured new contracts. Winning new business often creates a gap between upfront costs and incoming revenue. A higher credit limit helps you manage early expenses. This way, you can keep daily operations running smoothly.

You’re expanding into new markets or services. Whether it’s new equipment, additional hires, or entering a new region, documented expansion spending is one of the most accepted justifications that banks look for.

You’re heading into a seasonal spike. Retail businesses, contractors, and freight companies often need extra headroom during specific months. A temporary credit limit increase, found in the email templates pack, is a great option for seasonal needs.

Your revenue has grown considerably. If your annual revenue is up since your last credit limit review, your bank might not know. Updated financial figures give the reviewer a concrete reason to revisit the limit.

💡 Pro Tip: Don’t wait until you’re nearly maxed out before sending your request. Apply when your account is in good standing and utilization is high, but not at the ceiling. Banks prefer proactive, well-timed requests over urgent ones made under pressure.

What Your Bank Actually Looks for in a Credit Limit Increase Request

Before you write, it’s good to know how lenders evaluate these requests. Banks consider various factors, and the best applications cover them all.

Payment history. This is the single most important signal. A consistent record of on-time payments tells the bank you manage credit responsibly. Template 3 in the email pack highlights payment history as a main reason, and that’s on purpose.

Credit utilization. High utilization demonstrates genuine need. Using over 80 to 85% consistently boosts your case. This is true if you also have a clean payment record and strong financials.

Business financial health. This is where supporting documents come in.

The bank can check your ability to repay by looking at:

- Audited financial statements

- Bank statements

- Accounts receivable aging reports

- Cash flow forecasts

The more thorough your documentation, the faster the review.

Years in operation. Established businesses with longer account histories get faster decisions. The corporate credit limit request letter template has a “Years in Operation” field. Lenders pay close attention to this detail.

The specificity of your stated reason. A vague reason stalls a request. A clear reason related to growth, signed contracts, or a clear need pushes it ahead.

What to Include in Your Credit Limit Increase Request Letter

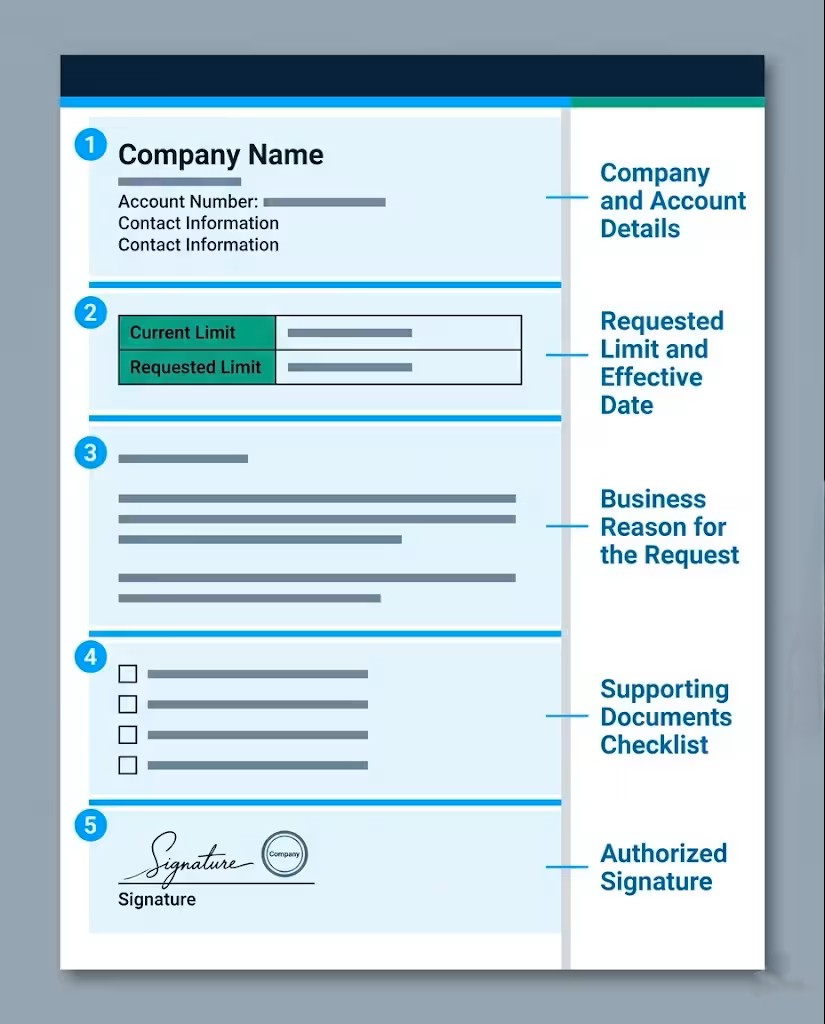

The formal letter template includes five structured sections. Here’s what belongs in each one and why it matters.

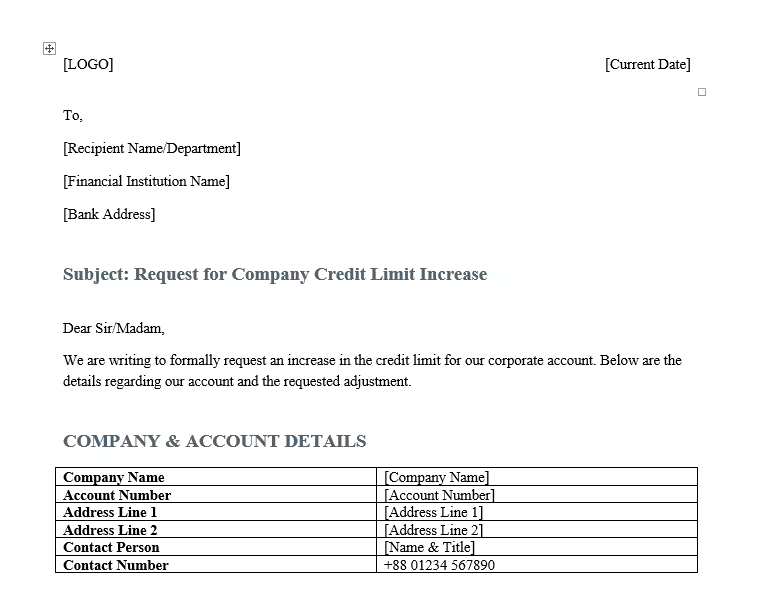

Company and Account Information

Open with a clear header that identifies your business and the account you’re referencing. This section should include:

- Company legal name and registered address

- Business registration number and EIN (US) or VAT/Tax ID (UK/international)

- Contact person name, phone number, and email

- Credit account number (last 4 digits are standard)

- Credit product type, such as Corporate Visa Signature or Commercial Mastercard Corporate

- Current credit limit and average monthly utilization percentage

This section clears up any confusion about which account and company the request is for.

The Requested Limit and Effective Date

Be specific. State your current limit clearly, then state the exact figure you’re requesting. Include the date you want the increase to take effect. Also specify whether this is a permanent or temporary increase.

A request that says “we’d like more credit” rarely moves quickly. A request that says “we are requesting an increase from $150,000 to $500,000, effective March 1, 2026, on a permanent basis” gives the reviewer a clear decision to make.

A Clear, Well-Justified Reason for the Request

This is the section where most letters succeed or fail. The dedicated section below covers exactly how to write this well.

Supporting Documents Checklist

The template includes a checkbox list covering the most common supporting documents:

- Audited financial statements (last 2 years)

- Recent bank statements

- Accounts receivable aging report

- Tax returns

- Cash flow forecast

Include whichever ones apply to your situation. More documentation generally results in faster, more confident approvals.

Authorized Signature and Company Seal

The letter must be signed by an authorized signatory, such as a Chief Financial Officer, Finance Director, or Managing Director. Add a company seal or stamp if your organization uses one. This step confirms the request is official and matches the formal document standard that banks expect.

How to Use These Templates (Step-by-Step)

Each format serves a specific purpose. Here’s how to get the most out of each one.

Using the PDF Template (US Letter or A4)

The PDF format is ideal for businesses seeking a print-ready and professional submission.

- Download the version that matches your paper size. Use US Letter for American businesses and A4 for UK or international submissions.

- Open the file in Adobe Acrobat or any PDF viewer that supports form filling.

- Fill in all fields marked in brackets, including company name, address, account number, and requested limit.

- In Section 4, write your specific reason for the increase. Keep it clear and factual.

- Check the boxes next to the supporting documents you’ll be attaching.

- Sign the document, using a digital signature if preferred, and add your company seal if applicable.

- Save the completed file and attach it to your submission email, or print it for postal delivery.

Both PDF templates have a complete sample. You can use it as a guide while you fill in your own details.

Using the Editable Word Template (A4)

The Word version allows unrestricted editing. It’s a great choice if you want to change the layout or add more context.

- Download and open the file in Microsoft Word.

- Replace all placeholder text in brackets with your actual company and account details.

- Update the table in Section 2 with your current figures, including revenue, utilization, and employee count.

- Write your reason for the request in Section 4, using plain, direct language.

- To save as a PDF, go to File, then Save As, and select PDF.

⚠️ Mistake to Avoid: Don’t send the letter with placeholder text still in it. A field like “[Company Name]” left blank signals to the bank that the letter was put together carelessly. It undermines your credibility before anyone reads the actual request. Proofread the completed letter twice before sending.

Using the Email Templates

The email templates pack covers every stage of the request process. The 10 templates are divided into three groups:

Initial Request Templates (5 Options):

- Formal Request: A detailed and polite request for services.

- Short Professional Version: A concise and direct request suitable for busy professionals.

- Payment History-Focused Version: A request emphasizing past payments and transactions.

- Expansion or New Contract Version: A request for extending services or starting a new contract.

- Temporary Increase Request: A request for a short-term increase in services or support.

Choose the one that best matches your situation.

Follow-up emails (3 options):

- First follow-up: Send after 5 to 7 business days.

- Second follow-up: Send after 10 to 14 days.

- Escalation email: Use politely if you still haven’t heard back.

Response templates (2 options):

- An approval confirmation response to send when your request is approved.

- A decline response with a reconsideration request for when you want to challenge a rejection.

To use the email templates, copy the message. Replace the bracketed placeholders with your details. Then, send it to your bank’s corporate credit team or your relationship manager.

How to Write a Persuasive Reason for Your Credit Limit Request

The reason section is where most corporate credit limit increase applications are won or lost. A weak reason slows the review. A strong, specific reason moves the application forward.

Lead with what changed. Don’t write “we need more credit.” Instead, write something like: “Our company secured three new government contracts in Q4 2025, requiring upfront procurement of server hardware and software licenses totaling approximately $320,000, before the first contract payments arrive.”

Tie your reason to documented evidence. Reference a specific contract, purchase order, or expansion plan that you’re attaching as a supporting document. The bank should be able to open your attachments and quickly verify what you’ve stated in your letter.

Describe the operational impact of your current limit. If the current limit is being reached before the billing cycle ends, say so directly. Explaining that “our current limit is being reached within the first two weeks of each billing cycle, causing delays in vendor payments and mid-month operational disruptions” is concrete and credible.

Signal repayment capacity. The reason section isn’t only about need. It’s also about showing you can handle a higher limit responsibly. Recent revenue growth, a big contract win, or better cash flow shows the bank that the larger facility is manageable.

A well-written reason might look like this: “Global Tech Solutions Inc. is expanding into the European market and has signed three new government contracts in Q4 2025. These contracts require increased procurement of server infrastructure and software licenses.

Our current $150,000 limit is being reached within the first two billing cycle weeks, creating vendor payment delays. Annual revenue of $12.5M and a spotless payment history confirm our capacity to manage an increased credit facility.”

That’s specific, documented, and addresses both need and repayment ability. That’s what gets approved.

Real-World Example: How a Business Secured a Corporate Credit Line Increase

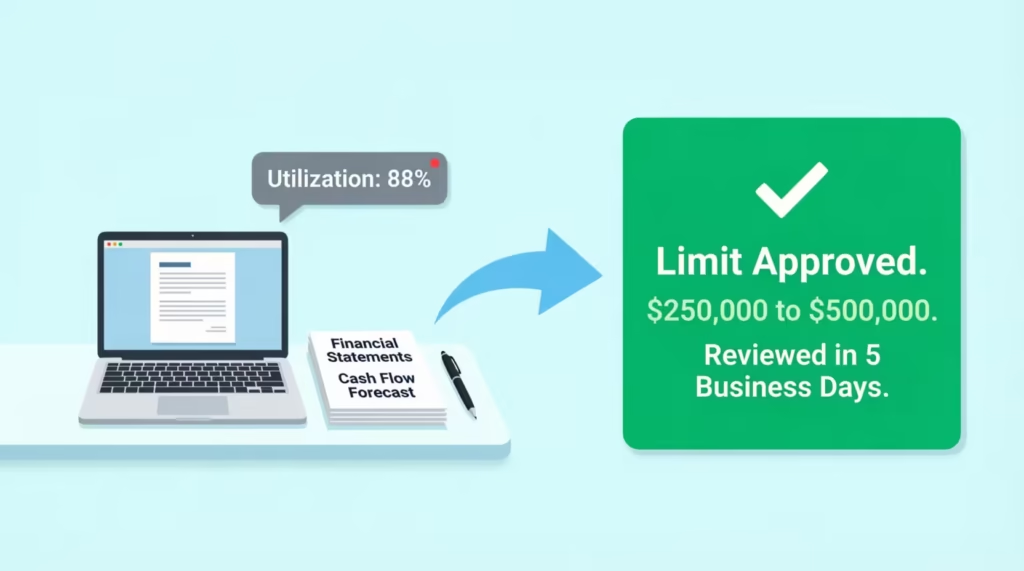

Marcus Webb, the Finance Director at a mid-sized freight logistics firm with 145 employees, faced a constant issue. The company’s monthly corporate card utilization was sitting at around 88% of a $250,000 limit. Three new shipping contracts needed upfront payments for carriers, port fees, and customs deposits. However, the billing cycle ran dry by mid-month.

Marcus assembled a formal credit limit increase application using the structured letter template. The submission included:

- A specific request to raise the limit from $250,000 to $500,000, with an effective date set for the following billing period

- A section that is named the new North American Shipping Contract and explains its mid-cycle impact on daily operations.

- Audited financial statements showing consistent annual revenue exceeding $14 million

- Six months of bank statements and a forward-looking cash flow forecast

The bank’s commercial credit team reviewed the submission within five business days. The increase was approved in full. The relationship manager’s feedback: the quality of the documentation and the specificity of the stated reason were the deciding factors.

The takeaway is straightforward. Banks don’t approve these requests based on goodwill. They approve them based on clear, organized evidence.

Common Mistakes That Get Business Credit Increase Requests Rejected

Even well-intentioned applications regularly contain avoidable errors. These are the most common ones that cause delays or rejections.

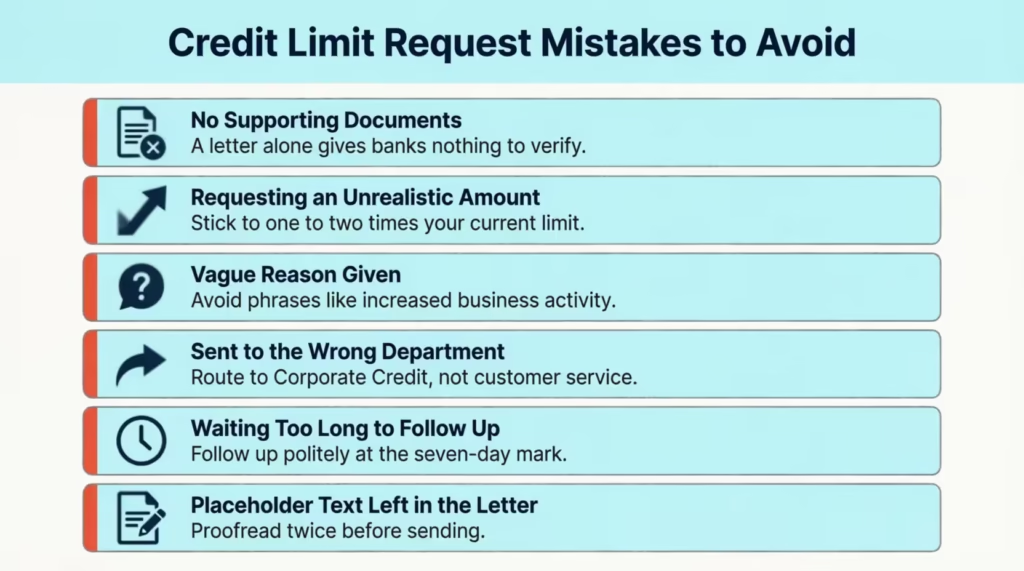

Submitting without supporting documents. A letter alone gives the bank nothing to verify. The checklist in the formal template is there because banks need financial proof before taking action. Missing attachments are the single most common reason for delayed reviews.

Requesting an unrealistic amount. Asking to jump from $50,000 to $2,000,000 with no supporting documentation signals poor planning. A request for one to two times the current limit, backed by solid financial proof, is often the most believable range.

Writing a vague reason. “Increased business activity” is the most common weak reason in these letters. Named contract wins or specific expansion projects, hold much more importance.

Sending to the wrong department. Many requests are delayed. This happens when they go to general customer service instead of corporate credit or relationship management. The subject lines in the email templates are specifically worded to help route your message correctly.

Waiting too long to follow up. After submitting, most businesses either follow up too soon (within two days) or not at all. Following up at the 7-day mark with a polite, professional message is the appropriate approach.

Not proofreading before sending. Unfilled placeholders, formatting errors, or inconsistent figures between the letter and attached documents can all make a reviewer pause or ask for clarification.

What to Do After Sending Your Request

Submitting the letter is just the first step. Here’s what to expect and how to handle each stage.

Following Up on Your Request

Most banks take 5 to 14 business days to review corporate credit limit applications. A polite follow-up after 7 business days is appropriate and expected.

The email templates include three follow-up options, each designed for a different stage:

- The first follow-up is 5 to 7 days later. It asks for a status update and checks if you can provide more documents.

- The second follow-up comes 10 to 14 days later. It restates the request and checks if anything else is needed.

- The polite escalation email is for when you get no response. It helps make sure your request reaches the right person.

All three are professional in tone. The goal is to prompt a status update, not to pressure the reviewer.

Alternatives If Your Request Is Refused

Rejection isn’t the end. Other options exist.

Ask for a Smaller Enhancement

If they denied your request for $50,000, try asking for $30,000 instead.

Sometimes banks are willing to approve less than originally asked for.

Apply with an Alternative Lender

Your current bank said no? Try another one.

Different lenders have different criteria. You might qualify elsewhere.

Consider a Business Line of Credit

This is different from a credit card. It works like this:

Approval for a maximum amount

Borrow only what you need

Pay interest only on what you use

Borrow, repay, and borrow again

Lines of credit often have higher limits than credit cards.

Look Into Business Term Loans

For a one-time need, a term loan might work better:

Borrow a fixed amount

Repay it over a set period

Interest rates may be lower than those on credit cards

Good for specific purchases or projects

Try Invoice Financing

If you have outstanding invoices, you can get cash for them:

A company buys your unpaid invoices

You get money immediately (usually 70-90% of the invoice value)

When your customer pays, the company takes its fee

You get the rest

This provides quick cash without borrowing.

Consider Equipment Financing

Need credit to buy equipment? Get financing specifically for that:

The equipment itself serves as collateral

Easier to qualify for than unsecured credit

Spread the cost over time

Establish Credit and Apply Again in the Future

Sometimes you need more time. Focus on:

Building payment history

Growing your revenue

Improving your credit score

Reducing existing debt

Reapply in 6-12 months with an application that presents stronger qualifications.

Work with a Credit Counselor

A business credit counselor can:

Review your financial situation

Identify problems

Create an improvement plan

Guide you through the reapplication process

Professional help is worth the investment.

💡 Pro Tip: After a decline, ask your relationship manager directly: “What specific steps would put our account in a stronger position for this request?” Most banks are willing to give guidance. Responding to that feedback in 60 to 90 days shows you care. This can often help you out.

Tips to Strengthen Your Corporate Credit Application Before You Send It

A few targeted steps before you submit can noticeably improve the outcome.

Clean up your payment history first. If there have been any late payments in the past 6 to 12 months, address them before sending your request. A spotless recent payment record matters more to reviewers than a perfect history from three years ago.

Reduce your balance slightly before applying. If your utilization is at 95%, try to lower it to 75% or 80% before submitting. This shows financial control while still highlighting your real needs.

Prepare your documents before you start writing the letter. Banks move faster when attachments are complete, clearly labeled, and easy to navigate. Label each file descriptively, such as “Audited Financial Statements 2024” or “Q4 2025 Cash Flow Forecast.”

Keep your requested amount proportionate to the evidence. If your supporting documents show revenue growth of $2 million over the past year, a request to increase the limit by $200,000 to $400,000 is proportionate. Requests that are too large for the documented growth often raise questions instead of solving them.

Address the letter to the right person. If you have an assigned relationship manager, address the letter directly to them by name. If not, use the Corporate Credit Department or Commercial Banking Department as the recipient.

Frequently Asked Questions

How do I formally ask my bank to increase my company’s credit limit?

Send a written request to your bank’s Corporate Credit Department or your relationship manager. Provide your account details, the desired limit, a clear business reason, and supporting documents such as bank and financial statements.

What documents does a bank usually require for a business credit limit increase?

Most banks ask for audited financial statements from the last two years, recent bank statements, an accounts receivable aging report, tax returns, and a cash flow forecast. The exact list varies by institution, so confirm with your bank before submitting.

How long does a corporate credit limit increase review usually take?

Most banks take between 5 and 14 business days to review a corporate credit limit request. Larger increases or incomplete submissions might take longer. This is because the bank may need to ask for more documents.

What counts as a strong reason for a business credit limit increase?

Specific, documented reasons work best, such as newly signed contracts, business expansion requiring upfront capital, or consistent high utilization due to measurable revenue growth. Vague language like “increased business activity” is less likely to prompt a fast approval.

Can my company request a temporary credit limit increase instead of a permanent one?

Yes, most banks let businesses boost spending temporarily. This helps with seasonal needs or short-term cash flow. Your request should specify a clear start date, end date, and the specific reason for the temporary increase.

How much of a credit limit increase should a company request?

Requesting between one and two times your current limit is generally reasonable and easier to justify with standard documentation. Requests above that range can happen. However, they need stronger financial proof and a clear business case.

Does requesting a credit limit increase affect a business’s credit score?

Most corporate credit limit reviews check your business credit profile with a soft pull. This way, your score won’t change. However, this varies by issuer, so confirm with your bank directly before submitting your request.

Who should sign a company credit limit increase request letter?

The letter must be signed by someone with financial authority over the account. This is usually the Chief Financial Officer, Finance Director, Managing Director, or another officer recognized by the bank for credit matters.

Conclusion

Getting your corporate credit limit raised doesn’t have to be a slow or uncertain process. The key is preparation. You need a clear, structured letter. Include a specific reason and real documentation. Also, attach all supporting financial documents.

This guide has templates for all your needs. Whether you face cash flow issues, new contracts, or plans to expand, you’ll find the right format here.

Based on how banks evaluate these submissions, the most effective approach is to use the formal PDF or Word letter as your primary submission and the email templates for follow-up at every stage. If this guide helped your team, share it with your accountant, CFO, or any business owner managing corporate credit facilities.