Multiple Credit Card Payoff Calculator

Enter your credit card balances, APRs, and your monthly budget to see how quickly you can become debt-free. Compare different payoff strategies like Avalanche and Snowball.

Your Payoff Results

-

-

-

Personal Loan Comparison

Consolidation Simulation

Balance Paydown Over Time

Enter your card details to see the payoff chart.

A line chart showing the total credit card balance decreasing over time until it reaches zero.

Interest Paid Per Card

Your interest breakdown will appear here.

A bar chart showing the total interest paid for each individual credit card.

How to Use This Calculator

- 1 Add Your Cards: Enter the current balance, APR, and minimum payment for each credit card. Use the "Add Another Card" button for more.

- 2 Set Your Budget: Input the total amount you can afford to pay across all cards each month.

- 3 Choose a Strategy: Select either the Avalanche (highest interest first) or Snowball (lowest balance first) method.

- 4 Analyze Results: The calculator will instantly show your debt-free date, total interest paid, and a payoff chart. Use the toggles to compare with a personal loan.

Disclaimer: This calculator is for informational purposes only. The results are estimates based on the information you provide and may not be accurate or applicable to your specific financial situation. The information provided does not constitute financial, legal or tax advice. We do not guarantee the accuracy of the calculations or the applicability of any information. Always consult a qualified financial professional for advice specific to your personal circumstances. Credit card terms, conditions, rates and offers are subject to change by the issuing bank at any time. We are not responsible for any actions or decisions taken based on the information provided by this tool.

Have questions or need assistance? Contact Us

Carrying balances on two or more credit cards is genuinely stressful. Interest builds every month, and minimum payments barely make a dent. According to the Federal Reserve Bank of New York, credit card balances hit $1.17 trillion in Q3 2024. That’s why so many people are searching for a several credit card payoff calculator to build a real escape plan.

Pick a proven payoff strategy, set a monthly budget, and you’ll know exactly when you’ll be debt-free.

Keep reading for step-by-step instructions, the formulas behind the math, a real-world example, and expert tips. These will help you get out of debt faster and smarter.

What Is a Credit Card Payoff Plan?

A credit card payoff plan is a structured approach to eliminating your balances within a set timeline. It’s not about paying something each month and hoping for the best. It’s about knowing how much you owe, what each card is costing you in interest, and which one to focus on first.

Here’s why this matters so much right now. Data from the Federal Reserve Bank of New York shows that American credit card balances reached $1.17 trillion in Q3 2024, hitting record levels. On top of that, Federal Reserve G.19 consumer credit data puts the average interest rate on credit card accounts at around 21.5% going into 2025.

At that rate, a $6,000 balance paid with only minimum payments can take more than 15 years to cut. A solid payoff plan can cut that timeline to two or three years and save you thousands of dollars along the way.

📌 Did You Know: Making only minimum payments on a $6,000 balance at 21% APR can cost you more than $6,500 in total interest, nearly as much as the original debt itself.

How This Multiple Credit Card Payoff Calculator Works

This tool handles up to 12 credit cards at the same time, making it a practical fit for most households. Here’s what happens behind the scenes:

Card tracking. For each card, you enter the current balance, APR, and an optional minimum payment. Leave the minimum payment field blank. The calculator will automatically fill it in using the industry-standard formula.

Strategy selection. You choose between the Avalanche method or the Snowball method. Each month, the calculator sorts your cards and directs your extra budget accordingly.

Budget allocation. Every month, the tool pays the minimums on all cards first. Then it throws any leftover budget at your priority card based on the strategy you selected.

Visual charts. Two charts update automatically after every input. A one-line chart shows your total combined balance dropping over time. One bar chart breaks down interest paid per card, so you can immediately spot which card is costing you the most.

Bonus tools. A personal loan comparison lets you see whether refinancing beats your current plan. A consolidation simulation shows what happens if you roll all your balances into one lower-rate loan. Both features display the monthly payment, total interest, and potential savings side by side.

💡 Pro Tip: Run the personal loan comparison before calling your bank. If a consolidation loan at a lower APR saves you $1,000 or more in total interest, it’s worth a serious look.

The Formula Explained

There are three core formulas powering this calculator. Understanding them helps you trust the results you see.

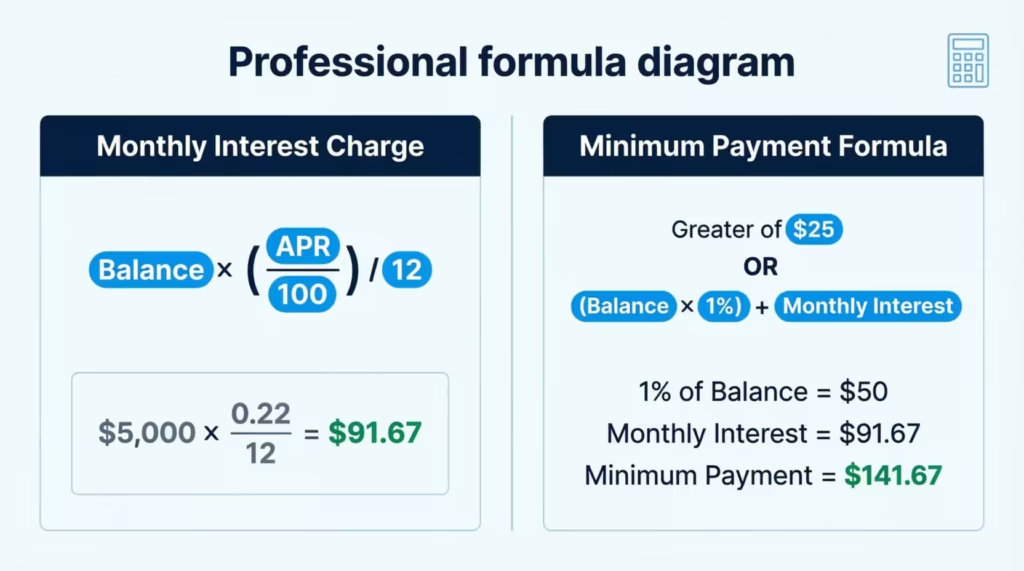

1. Monthly Interest Charge

This is how the calculator figures out how much interest your card adds each month:

Monthly Interest = Balance x (APR / 100) / 12

Here’s what that looks like in practice. Say your card carries a $5,000 balance at 22% APR:

Monthly Interest = $5,000 x 0.22 / 12 = $91.67

That’s $91.67 going straight to the credit card company every single month, before a single dollar reduces your actual balance. That’s why high-APR cards are so dangerous to ignore.

2. Minimum Payment Calculation

The calculator uses the standard formula that most major card issuers actually follow:

Minimum Payment = Greater of $25 OR (Balance x 1%) + Monthly Interest

So on that same $5,000 balance at 22% APR:

- 1% of balance = $50

- Monthly interest = $91.67

- Minimum = $50 + $91.67 = $141.67

This formula reflects industry practice, as described by the Consumer Financial Protection Bureau.

3. Loan Comparison Formula

When you enable the personal loan comparison, the calculator uses the standard amortization formula:

Monthly Payment = P x [r(1+r)^n] / [(1+r)^n – 1]

Here, P is the loan amount, r is the monthly interest rate (APR / 12 / 100), and n is the total number of monthly payments. This lets you compare a fixed personal loan directly against your current card payoff plan.

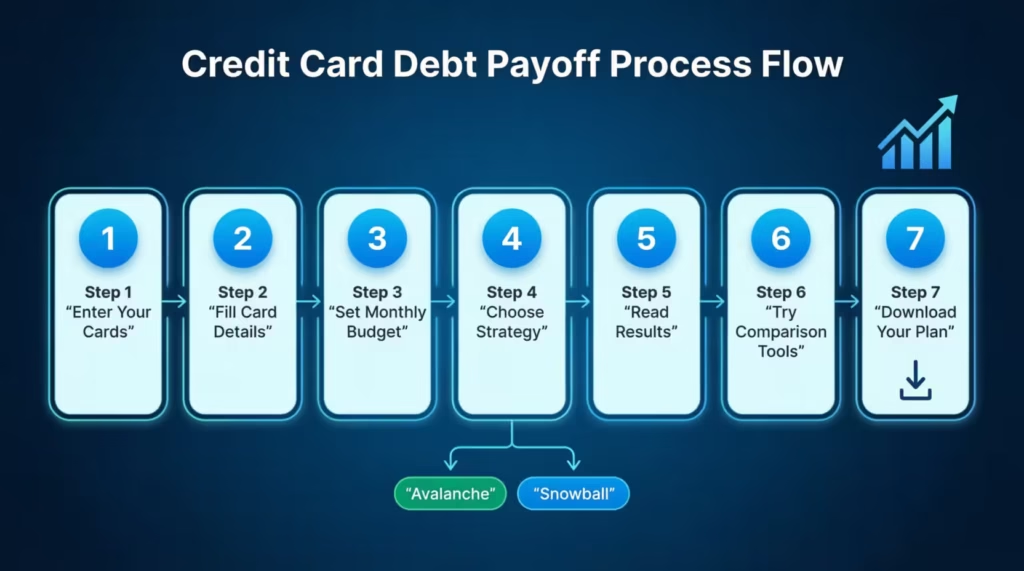

How to Use This Calculator (Step by Step)

Follow these steps to get accurate, useful results:

Step 1: Enter your cards.

The calculator starts with a few pre-loaded card rows. Click “Add Another Card” to add more (up to 12 total). Give each card a name, like the card issuer or nickname, so it’s easy to identify in the charts.

Step 2: Fill in the card details.

For each card, enter:

- Current balance (what you owe today, not the credit limit)

- APR (check your latest statement or your card’s mobile app)

- Minimum payment (or leave it blank to use the auto-calculated amount)

Step 3: Set your total monthly budget.

Enter the total dollar amount you can realistically commit to credit card payments each month. This must be at least equal to the sum of all your card minimums. The calculator will tell you the exact least required if you’re unsure.

Step 4: Choose your strategy.

Select Avalanche to target the highest-APR card first. Select Snowball to knock out the smallest balance first. Once you pick either choice, the system handles it automatically.

Step 5: Read your results.

Three summary boxes appear at the top of the results panel: Debt-Free In, Debt-Free Date, and Total Interest Paid. These give you the clearest possible picture of your payoff plan.

Step 6: Try the optional comparison tools.

Toggle on “Compare With a Personal Loan” to check a potential refinancing option. Toggle on “Simulate Loan Consolidation” to see what combining all your balances into one loan would look like.

Step 7: Download your plan.

Click “Download PDF” to save a copy of your results. It’s useful to review monthly, share with a financial advisor, or simply keep as a motivational reminder.

How to Read Your Results

The results panel gives you three immediate takeaways at the very top.

Debt-Free In. This is the number of months until your final card is paid off. If it shows 30 months, you have a clear, data-backed timeline to work toward. Try increasing your monthly budget by $50 and watch this number shrink in real time.

Debt-Free Date. This converts your payoff timeline into an actual month and year. Seeing a real finish line on the calendar makes this feel far more achievable than a vague number of months.

Total Interest Paid. This is the total amount you’ll pay in interest over your entire payoff period. If it shocks you, that reaction is exactly the motivation you need to bump up your budget.

Reading the charts:

The line chart tracks your total combined balance decreasing month by month. A steep early drop means your extra payments are hitting hard. A flat early section followed by a steep drop is normal with the Snowball method, where you’re building momentum.

The bar chart shows interest paid per individual card. The tallest bar is your most expensive card. If it’s not already your primary target, that’s worth reconsidering.

Real-World Example

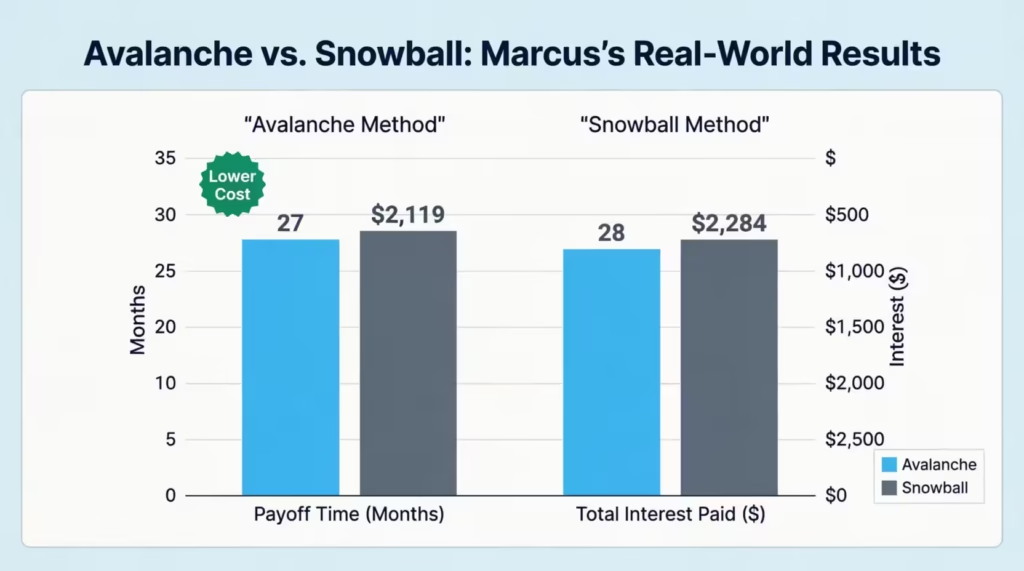

Let’s say Marcus, a 35-year-old marketing coordinator in Chicago, has three credit cards:

| Card | Balance | APR | Min Payment (Auto) |

|---|---|---|---|

| Visa Platinum | $4,500 | 24.99% | $128.75 |

| Mastercard Cash+ | $2,100 | 19.99% | $56.00 |

| Discover It | $3,200 | 21.99% | $90.67 |

Total balance: $9,800Marcus’s monthly budget: $500

Using the Avalanche method (highest APR first, targeting the Visa Platinum):

- Payoff time: 27 months

- Total interest paid: $2,119

Switching to the Snowball method (lowest balance first, targeting the Mastercard Cash+):

- Payoff time: 28 months

- Total interest paid: $2,284

The Avalanche method saves Marcus roughly $165 in interest. However, the Snowball method fully pays off the Mastercard in about five months, giving him a genuine early win that keeps him on track.

Marcus ran both scenarios in under two minutes. He started with Snowball for the motivation, then switched to Avalanche after knocking out his first card. The calculator made it easy to see exactly what each choice would cost him.

⚠️ Mistake to Avoid: Never use your minimum payment as your payoff strategy. On a $9,800 balance at 22% APR, paying only minimums could stretch your payoff timeline past 25 years and cost more in interest than the original balance.

Expert Tips and Insights

1. Pick the strategy that fits your personality, not just the math.

The Avalanche method has a mathematical advantage. The Snowball method wins motivationally. Early wins boost long-term financial success. Studies in behavioral economics show this clearly. People who have small successes are more likely to stick to their goals. If you’ve started and stopped a payoff plan before, Snowball might be worth the small extra cost in interest.

2. Always round up your monthly budget.

If your total minimums come to $225, don’t budget exactly $225. Round up to $275 or $300. Even $50 extra each month can shave several months off your timeline and cut out hundreds of dollars in interest. It’s one of the easiest ways to speed up your plan.

3. Use the payment rollover technique.

When a card is fully paid off, don’t spend its minimum payment. Roll it directly into your next target card. The calculator does this for you, but understanding the idea helps explain why your payoff speed increases once you clear a card.

4. Re-run your plan after any income change.

Got a tax refund, a bonus, or a small raise? Open the calculator and update your monthly budget. Even a one-time extra payment of $400 can push your debt-free date months closer. The calculator recalculates everything in seconds.

5. Keep paid-off cards open.

Closing a card reduces your total available credit. That raises your credit utilization ratio, which is one of the biggest factors in your credit score. Leave paid-off cards open, even if you don’t use them. Just hide them if you’re tempted to spend.

Common Mistakes to Avoid

- Entering the wrong APR. Many people confuse a promotional rate with their actual rate. A 0% promo APR that expires in three months is not your real rate. Always use the standard APR shown on your most recent statement or in your card’s app.

- Setting an unrealistic monthly budget. Entering an optimistic number gives you a shorter payoff date on screen, but a plan you can’t actually follow through on. Start with a budget you’re genuinely comfortable committing to, then increase it when life allows.

- Continuing to charge on cards you’re paying off. This calculator assumes that you have frozen your balances. Every new transaction changes the math. Many financial advisors suggest physically separating yourself from the card. You can put it in a drawer or remove it from your digital wallet. Do this until your balance hits zero. This helps you avoid unnecessary spending.

- Skipping the consolidation simulation. A lot of users ignore this feature without even trying it. If you can qualify for a personal loan at 11% to 13% APR, consolidating $9,000 in credit card debt into it could realistically save you over $1,200. The simulation takes about 30 seconds and shows you the exact comparison.

FAQs

What’s the difference between the Avalanche and Snowball methods?

The Avalanche method targets the highest-APR card first and saves the most money in total interest. The Snowball method targets the smallest balance first, creating early wins that help with motivation. The Avalanche is the better financial choice; Snowball often works better for people who need momentum to stay on track.

What happens if my monthly budget is lower than my total minimum payments?

The calculator displays an error message explaining the exact least you need. If your income can’t cover the minimums, contact your card issuers. Ask about hardship or reduced-payment programs. You can also reach out to a nonprofit credit counselor through the National Foundation for Credit Counseling.

How is the auto-calculated minimum payment determined?

The formula is the greater of $25 or 1% of your balance plus your monthly interest charge. This closely mirrors the standard formula used by most major U.S. credit card issuers.

Can I enter a card with a 0% promotional APR?

Yes. Enter 0 in the APR field. The calculator manages zero-interest cards well. It also allocates your extra budget smartly to your other cards.

How accurate is the debt-free date?

It’s precise based on the numbers you enter. In real life, balances can shift if you make new purchases or if your APR changes. Re-run the calculator every one to two months with updated balances to keep your plan accurate.

Does using this calculator affect my credit score?

No. This is a planning tool only. It does not connect to your credit file, access any personal financial data, or perform any kind of credit inquiry.

Should I consolidate my credit card debt into a personal loan?

Consolidation makes sense when the personal loan APR is lower than your weighted average card APR. Use the consolidation simulation in the calculator. Compare the total interest paid for both options before making your decision.

How many credit cards can I add?

The calculator supports up to 12 credit cards at once, which covers the large majority of users managing many card balances.

Conclusion

Taking control of credit card debt starts with a clear picture of where you stand. We covered how the payoff tool works and the formulas behind it. We also explored two proven strategies and provided a real-world walkthrough. Finally, we discussed the most common mistakes people make along the way.

Start with the Avalanche method for the best results, as long as you can maintain a consistent monthly pace. If motivation has held you back in the past, begin with the Snowball method to build momentum. The truth is, the best plan is the one you’ll actually follow through on, and this various credit card payoff calculator gives you every tool you need to do exactly that.

If this guide helped, please share it on social media. Someone in your circle might be carrying this same weight right now and just needs a place to start.