Mortgage Pre-Approval Calculator

Estimate your potential loan amount and monthly payments by factoring in your income, debts, and credit score.

Your Financial Details

Your Estimated Results

Pre-Approval Amount

$0

Total Monthly Payment (PITI)

$0.00

Estimated APR

0.00%

Debt-to-Income (DTI)

0%

Payment Breakdown

End of chart.

Save Your Results

Download a PDF summary of your pre-approval estimate for your records.

How to Use This Calculator

-

1

Enter your annual income and total monthly debt payments (e.g., car loans, student loans, credit cards).

-

2

Adjust the slider to your current credit score. Notice how the estimated interest rate changes automatically.

-

3

Fill in your desired loan term, down payment, and estimated annual property tax and insurance costs.

-

4

Review your estimated pre-approval amount, monthly payment, and DTI in the results section.

Trying to guess how much house you can afford can feel stressful, especially when your credit score, debts, and down payment all pull the number in different directions.

If you’re searching for a mortgage pre-approval calculator with credit score, you’re likely trying to set a real budget before you talk to a lender. Freddie Mac found that borrowers who gathered at least four rate quotes could save more than $1,200 a year.

A solid estimate starts with income, debt, rate, and down payment working together in one clear monthly payment test.

Keep reading, and you’ll see the math, the steps, the result guide, and smart ways to boost your buying power before you apply.

What Is Mortgage Pre-Approval?

Mortgage pre-approval is a lender’s estimate of how much money it may lend after checking income, debt, and credit. It helps set a price range for house hunting, but it is still not a final loan promise. The CFPB explains in its guide to prequalification and preapproval letters that lenders do not always use the same terms the same way, and both can still depend on assumptions.

In simple terms, this kind of estimate helps answer questions like these:

- How much home loan may fit the budget?

- How much do car loans, student loans, and credit cards cut into buying power?

- Could a stronger score lead to a better rate?

- Would a larger down payment lower the monthly cost?

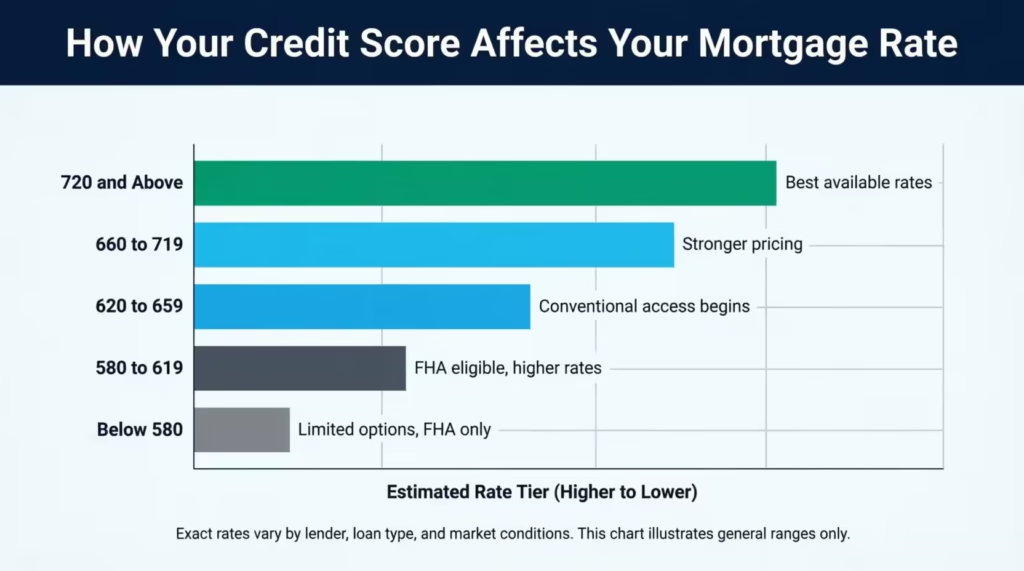

Credit score matters because it affects both approval odds and pricing. The CFPB notes in its explanation of how credit scores affect mortgage approval and rates that higher scores often help borrowers qualify for lower mortgage rates, and many lenders review scores from all three major credit bureaus and use the middle score.

How This Calculator Works

This tool starts with your monthly income and debt load. Then it works backward to find a loan amount that keeps the full housing payment inside common debt limits.

Here is the basic flow:

- It turns annual gross income into monthly gross income.

- It checks a front-end housing ratio and a back-end total debt ratio.

- It uses the lower of those two limits as the largest safe monthly housing payment.

- It estimates an APR based on the score range unless you type in your own rate.

- It adds taxes, insurance, and PMI when needed.

- It solves for the loan amount that fits the full monthly payment.

- It shows the estimated loan amount, monthly payment, APR, and debt-to-income ratio.

The planning team designed the rate estimate, not as a live lender quote. Real mortgage pricing can shift from day to day, and lenders also look at savings, reserves, property type, and loan program.

The Formula Explained

You can follow the math more easily when you split it into small parts.

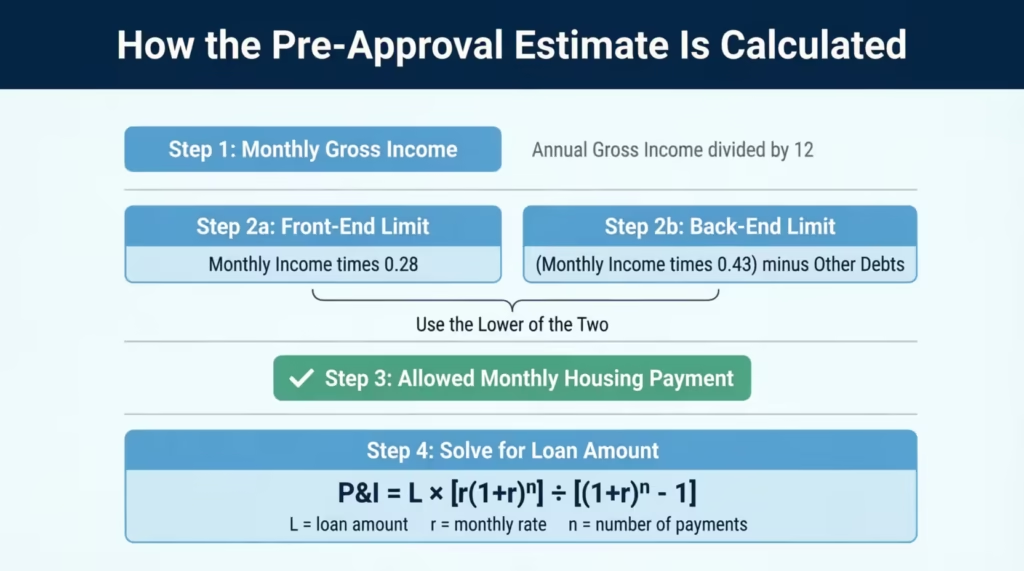

1) Monthly gross income

Monthly gross income = Annual gross income ÷ 12

2) Front-end housing limit

Front-end limit = Monthly gross income × 0.28

This caps the housing payment by itself.

3) Back-end debt limit

Back-end limit = (Monthly gross income × 0.43) − Other monthly debts

This caps housing plus other debts together.

4) Allowed monthly housing payment

Allowed housing payment = Lower of front-end limit or back-end limit

5) Principal and interest payment

P&I = L × [r(1 + r)^n] ÷ [(1 + r)^n − 1]

- L = loan amount

- r = monthly interest rate

- n = number of monthly payments

6) Other monthly housing costs

- Monthly property tax = Home price × annual tax rate ÷ 12

- Monthly insurance = Annual insurance ÷ 12

- Monthly PMI = Loan amount × annual PMI rate ÷ 12

7) Total monthly housing payment

Total payment = P&I + taxes + insurance + PMI

The calculator then works backward to find the largest loan amount that still keeps the full monthly payment inside the debt cap.

How to Use This Calculator

Follow these steps:

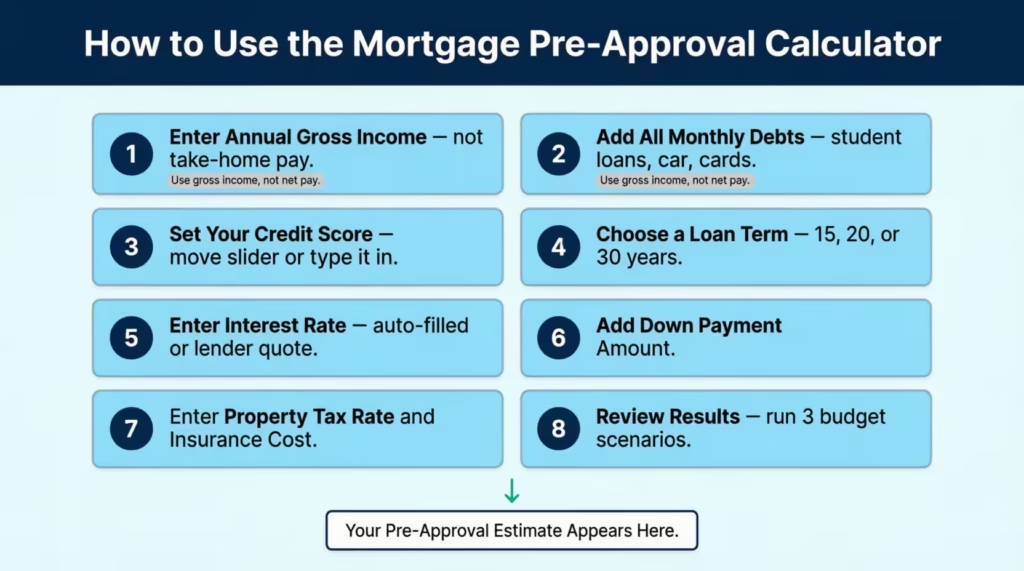

- Enter annual gross income, not take-home pay.

- Add all monthly debt payments. This should include student loans, car loans, personal loans, minimum credit card payments, and other recurring debts.

- Move the credit score slider or type the score directly.

- Pick a loan term of 15, 20, or 30 years.

- Use the auto-filled rate or enter a lender quote in the interest rate box.

- Add the down payment amount.

- Enter the property tax rate and annual home insurance estimate.

- Turn on PMI only if you expect less than 20% down and want that cost included.

- Review the results, then test a few new scenarios.

⚠️ Mistake to Avoid: Do not enter net pay from your paycheck. Mortgage math uses gross income before taxes and deductions.

A smart way to use the tool is to run three versions:

- a safe budget

- a target budget

- a stretch budget

That makes it easier to see what changes the number the most.

How to Read Your Results

The result box gives you four main numbers.

Pre-Approval Amount

This is the estimated loan principal, not the full home price. To estimate the purchase price, add the down payment to the loan amount.

Total Monthly Payment (PITI)

This is the full monthly housing cost. It includes principal, interest, property taxes, homeowners’ insurance, and PMI when used.

Estimated APR

This is the planning rate used in the estimate. It may come from the score range in the tool or from the rate you typed in. Real lender pricing can differ because lenders also review assets, loan type, reserves, and property details.

Debt-to-Income Ratio

This is your full monthly housing payment plus other monthly debts, divided by gross monthly income. It is one of the biggest numbers lenders watch. The Fannie Mae Selling Guide on debt-to-income ratios says manually underwritten loans are generally capped at 36%, may go up to 45% with stronger files, and loan casefiles run through Desktop Underwriter can allow up to 50%.

If your estimated number looks tight, that does not always mean homeownership is out of reach. It usually means one or more of the major inputs, such as debt, rate, down payment, or score, needs a closer look.

💡 Pro Tip: Change one input at a time. If the number jumps after you lower debt by $200 or raise the down payment by $10,000, you will know exactly which move helped most.

Real-World Example

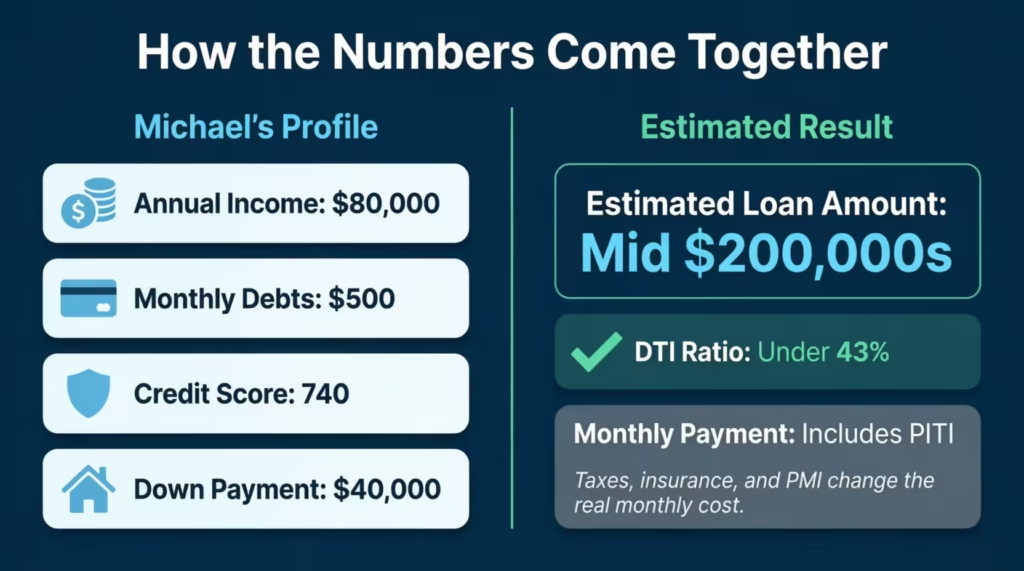

Michael is a project manager in Dallas. He earns $80,000 a year and pays $500 a month toward other debts. His score is 740. He wants a 30-year loan, plans to put down $40,000, expects a 1.25% property tax rate, and estimates $1,200 a year for homeowners’ insurance.

With those numbers, the estimate would likely land around a mid-$200,000 loan amount, with a monthly payment that includes principal, interest, taxes, and insurance. His debt-to-income ratio would stay under the common 43% back-end benchmark, which is why the scenario looks workable.

This example shows why the full payment matters. A buyer may focus on principal and interest alone, but taxes and insurance can take a big bite out of what first seems affordable.

Expert Tips and Insights

A stronger score usually helps in two ways. It can improve approval odds, and it can lower the rate. The CFPB explains in its consumer guide on credit score effects on mortgage rates that higher scores generally make borrowers eligible for lower interest rates, so even a modest score gain before applying can help.

Lowering monthly debt often works faster than trying to grow income. Paying off a $325 car payment or a $95 credit card minimum can improve the back-end ratio right away. Since mortgage approval often hinges on monthly obligations, cutting required payments can meaningfully raise borrowing power.

If a conventional loan looks tight, other loan paths may still exist. HUD states in its FHA credit score eligibility rules that FHA-insured financing is not allowed below a 500 score, allows up to 90% loan-to-value from 500 to 579, and allows maximum financing at 580 and above. The VA Home Loan Guaranty Buyer’s Guide also says the VA does not set a minimum credit score, though lenders often apply their own standards.

📌 Did You Know: Freddie Mac found in its research on how shopping mortgage lenders can save money that borrowers who got at least four mortgage quotes could save more than $1,200 a year in higher-rate periods.

Before applying, pull your credit reports, fix errors, and avoid opening new credit if you can. The CFPB warns in its guidance on credit score impact before a mortgage application that report errors can raise borrowing costs and that too many new credit accounts in a short time can hurt scores.

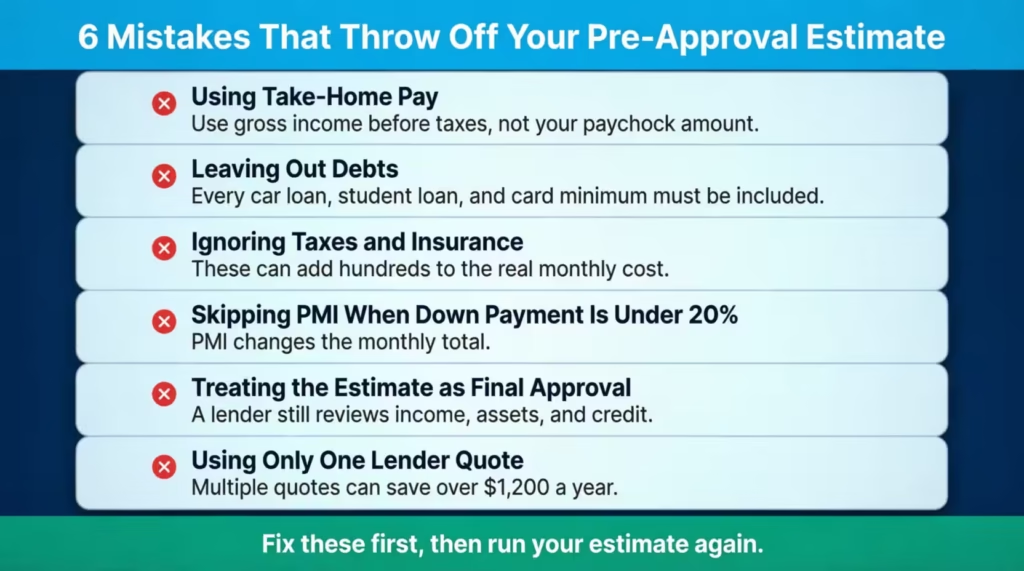

Common Mistakes to Avoid

Common mistakes can make the estimate look better than real life.

- Using take-home pay instead of gross income. Jennifer, a nurse in Phoenix, first used her after-tax pay and got a much lower number than she really qualified for. Gross income is the standard starting point.

- Leaving out debts. David, a sales manager in Tampa, forgot his $410 car payment. When he added it back, his estimate dropped fast because the debt ratio changed.

- Ignoring taxes and insurance. These costs can push a payment hundreds of dollars higher each month.

- Turning off PMI when the down payment is small. If the loan-to-value ratio stays above 80%, PMI can change the monthly cost.

- Treating an estimate like a final approval. A lender may still verify job history, assets, reserves, property details, and credit changes before issuing a firm loan decision.

- Using only one lender quote. Better pricing can appear when you compare multiple offers.

Frequently Asked Questions (FAQs)

What credit score do I need for mortgage preapproval?

Many conventional lenders look for at least a 620 score, but loan type matters. FHA rules let you finance fully with a score of 580 or higher. If your score is between 500 and 579, you typically need to put down 10%. VA doesn’t set a minimum score, but lenders often do.

Does mortgage preapproval affect credit score?

Yes. A true preapproval usually involves a hard credit inquiry, so the score may dip a few points for a short time. The effect is often small. Mortgage rate shopping completed on time is often viewed as preferable to submitting several separate loan applications.

How long does a mortgage preapproval last?

Most preapproval letters last about 30 to 90 days, with 60 to 90 days being common. Lenders use short time frames because income, debt, rates, and credit can change, so an expired letter often needs fresh documents and a new review.

What documents are needed for mortgage preapproval?

Most lenders ask for proof of income, recent pay stubs, W-2s or 1099s, tax returns, bank statements, ID, and details on debts and assets. Self-employed borrowers often need more paperwork. Lenders need to analyze income trends in detail.

Can I get preapproved with student loan debt?

Yes. Student loans do not block preapproval by themselves. The main issue is the monthly payment. This payment affects your debt-to-income ratio. A higher ratio can lower how much a lender will approve.

Do all lenders use the same credit score for mortgages?

No. Mortgage lenders usually check scores from the three big credit bureaus. They often use the middle score to decide on pricing and approvals. The exact model and lender overlay can still vary, so two lenders may not view the same file the same way.

Can I get preapproved before finding a house?

Yes, and many buyers do. Getting preapproved early can help set a realistic budget, spot credit issues before making offers, and show sellers that financing is already being reviewed by a lender.

Does a higher down payment increase mortgage preapproval?

In many cases, yes. A larger down payment lowers the loan amount. This can reduce your monthly payment. It may also remove PMI on a conventional loan when the loan-to-value ratio drops to 80% or less. That can improve both affordability and approval odds.

Bottom Line

We covered what this estimate means, how the math works, what each result shows, and how credit score, debt, rate, and down payment shape buying power.

Begin by using the mortgage pre-approval calculator with your credit score, then verify the results with a lender quote to ensure accuracy before you start house hunting.

The combination of planning and real-world lender feedback provides the clearest path forward. If this guide helped, please share it on social media with friends or family who may need it too.