Mortgage Affordability Calculator With Credit Score

Estimate the home you can afford based on your income, debts, credit score, and down payment.

Your Financials

Your Results

You can afford a home up to

Estimated Monthly Payment

$2,050.28

Debt-to-Income (DTI)

30.8%

Estimated Interest Rate

6.25%

Monthly Cost Breakdown

Loan Amortization

How to Use

- Enter your gross annual income and monthly debts.

- Move the credit score slider or type your score to see estimated rates.

- Set down payment and loan terms. Optionally enter property tax & insurance.

- Press Calculate (or enable Auto-calc) to view your maximum affordable home price.

- Download a PDF summary or share results with a friend.

Disclaimer

This calculator is for informational purposes only. The results are estimates based on the information you provide and may not be accurate or applicable to your specific financial situation. The information provided does not constitute financial, legal or tax advice. We do not guarantee the accuracy of the calculations or the applicability of any information. Always consult a qualified financial professional for advice specific to your personal circumstances. Credit card terms, conditions, rates and offers are subject to change by the issuing bank at any time. We are not responsible for any actions or decisions taken based on the information provided by this tool.

Many Americans want to buy a home but aren’t sure what price they can truly afford. Your credit score quietly controls your interest rate and buying power. According to the Consumer Financial Protection Bureau, lower-score borrowers often pay far more in interest than excellent-credit borrowers on the same loan. A mortgage affordability calculator with a credit score helps you skip the guesswork and get a real number.

The answer is simple: add up your income, debts, and credit score. This will help you find a home price that fits your budget.

Keep reading. We’ll go through the formula, step-by-step instructions, expert tips, and a real-world example. This will help you shop with confidence.

What Is Mortgage Affordability with a Credit Score?

Mortgage affordability is the maximum home price you can buy without overextending your monthly budget. It’s not just about how much a bank will lend you. It’s about what you can comfortably pay every month without financial strain.

Here’s what makes this different from a basic mortgage calculator: your credit score is built directly into the equation. Your credit score doesn’t just affect whether you get approved. Your interest rate affects your monthly payment significantly. It also dramatically changes your maximum home price.

As the Consumer Financial Protection Bureau’s interest rate tool clearly shows, two borrowers with identical incomes and loan amounts can receive very different rates based solely on their credit scores. Over a 30-year term, that gap adds up to tens of thousands of dollars.

Three core concepts power every affordability calculation:

Debt-to-Income Ratio (DTI): This is the percentage of your gross monthly income going toward debt payments. Lenders use it to measure your capacity to take on more debt. A DTI at or below 36% is the standard benchmark most conventional lenders use to determine healthy borrowing limits.

Credit Score Tiers: Your FICO score runs from 300 to 850 and maps directly to the interest rate you’ll be offered. A higher score unlocks a lower rate, which means more buying power for the same monthly budget.

Maximum Affordable Price: This is the highest home price where your estimated monthly payment stays within your DTI cap. It’s the number this calculator finds for you.

How This Calculator Works

This calculator uses your financial details to find the highest home price you can afford. It ensures you stay within a 36% debt-to-income ratio. Here’s what it processes:

Your Income: Your annual gross income is divided by 12 to get your monthly gross income. All DTI math is based on this monthly figure.

Your Existing Debts: Car loans, student loans, and credit card minimums are added together here. These reduce the amount left available for your mortgage payment.

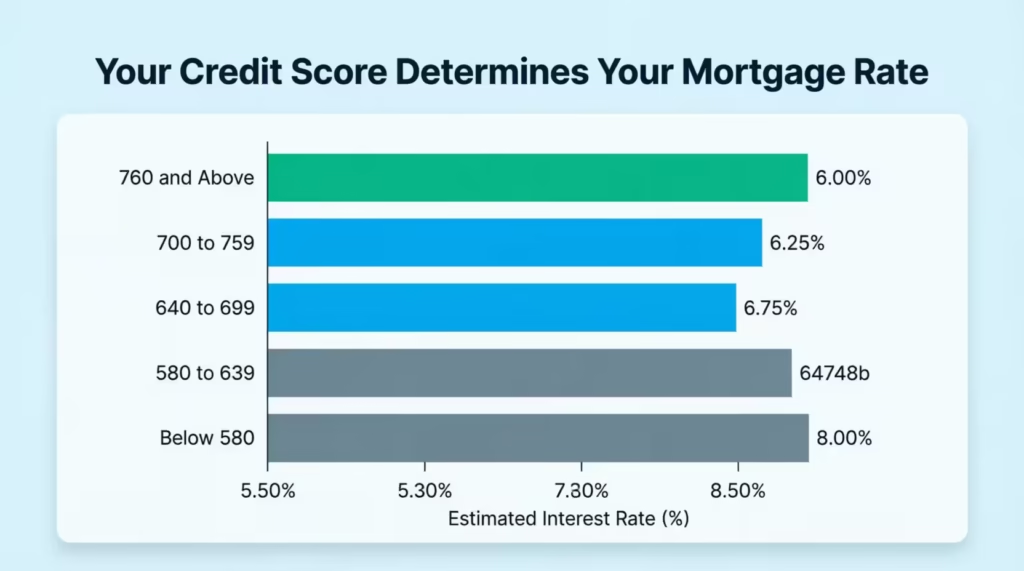

Your Credit Score: Based on your score, the calculator assigns an estimated interest rate automatically. You can override this manually if you’ve received a specific rate from a lender. The score-to-rate mapping the calculator uses reflects realistic conventional loan rate tiers:

| Credit Score Range | Estimated Rate |

|---|---|

| 760 and above | 6.00% |

| 700 to 759 | 6.25% |

| 640 to 699 | 6.75% |

| 580 to 639 | 7.25% |

| Below 580 | 8.00% |

Your Down Payment: The dollar amount you plan to pay upfront. It reduces the loan principal, which lowers your monthly payment. The down payment percentage is calculated and displayed automatically.

Additional Costs: Property taxes, home insurance, and HOA fees are factored into your total monthly payment. These costs are real and often missed by buyers who only focus on principal and interest.

The calculator features an auto-calculate mode that updates results in real time as you adjust any input. It also lets you export your full results as a PDF or share them directly on social media.

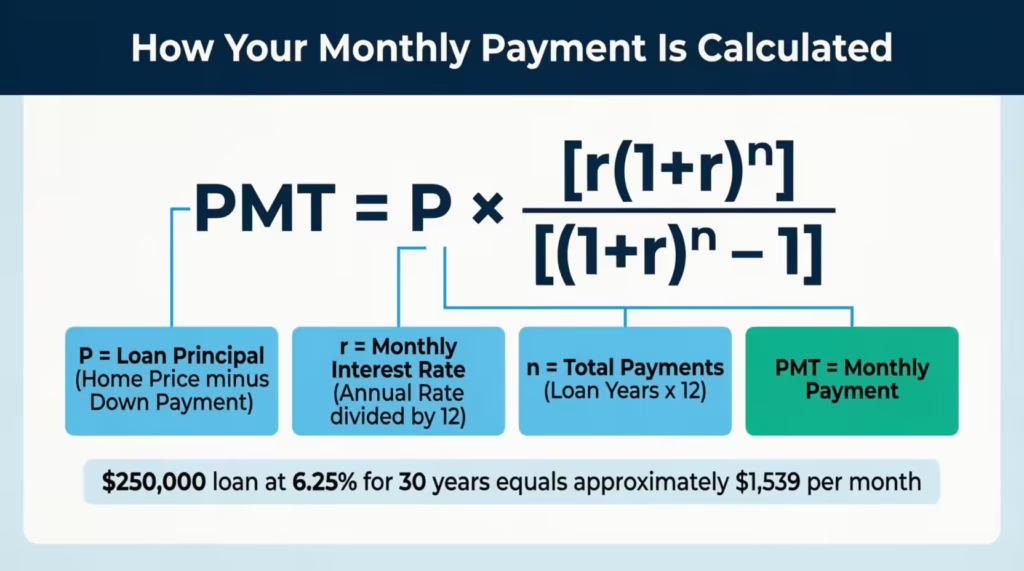

The Formula Explained

Two formulas drive every result this calculator produces.

Formula 1: Monthly Principal and Interest Payment (PMT)

This is the standard mortgage payment formula used by every lender:

PMT = P x [r(1+r)^n] / [(1+r)^n – 1]

Where:

- P = Loan principal (home price minus your down payment)

- r = Monthly interest rate (annual rate divided by 12)

- n = Total number of payments (loan years multiplied by 12)

For example, on a $250,000 loan at 6.25% for 30 years, the monthly rate is 0.0625 / 12 = 0.005208. The total payments are 360. PMT works out to approximately $1,539 per month.

Formula 2: Maximum Affordable Home Price

The calculator works backward from your DTI limit. It first calculates the maximum monthly housing payment you can afford:

Max Monthly Payment = (Monthly Gross Income x 36%) – Existing Monthly Debts

Then it uses a binary search method. It checks prices from a low estimate to a high limit. It narrows this range step by step. This continues until it finds the highest home price where your total monthly cost stays within that limit.

Total Monthly Cost = P&I Payment + Monthly Property Tax + Monthly Insurance + HOA

The result is rounded down to the nearest $1,000 for a conservative, realistic estimate.

💡 Pro Tip: You can manually override the interest rate field at any time. If you’ve already been pre-approved or received a quote from a lender, enter that rate for the most accurate result the calculator can give you.

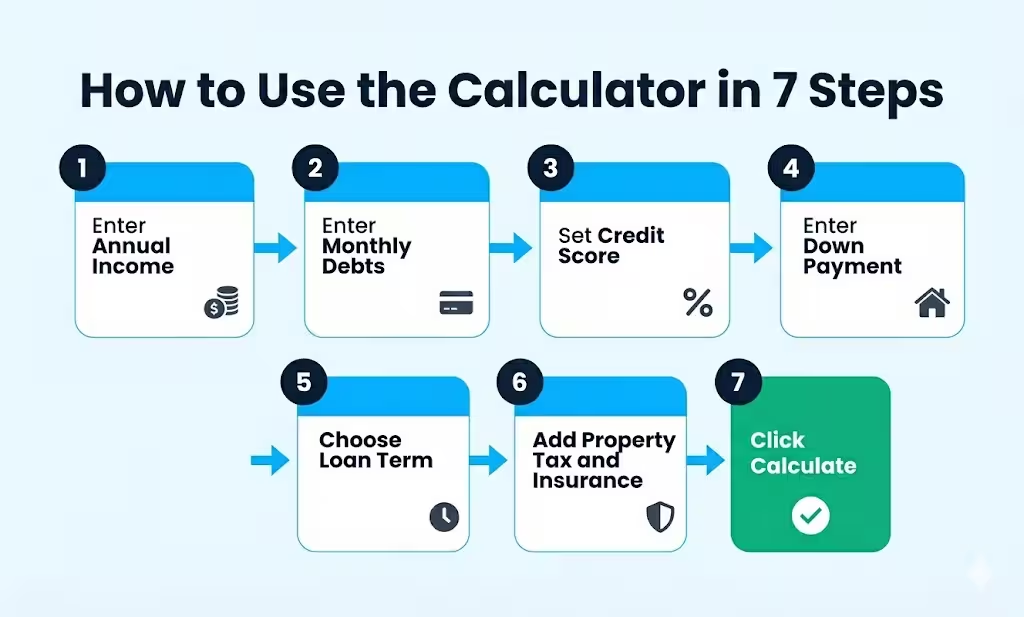

How to Use This Calculator (Step by Step)

Follow these steps, and you’ll have a solid estimate in under two minutes.

Step 1: Enter Your Annual Gross Income.

Type your total pre-tax income. If you’re buying with a partner, combine both incomes. The calculator automatically shows your monthly payment below the input field.

Step 2: Enter Your Total Monthly Debts.

Add up all recurring monthly debt payments: car loans, student loan minimums, and credit card minimums. Do not include utilities, groceries, or streaming subscriptions. These are not counted by lenders in DTI calculations.

Step 3: Set Your Credit Score.

Drag the slider or type your score directly into the number box. The interest rate field updates automatically based on your score range. If you have a lender’s specific rate, type it into the interest rate field to override the estimate.

Step 4: Enter Your Down Payment Amount.

Type the dollar amount you plan to put down. The percentage is calculated for you automatically. A 20% down payment means you won’t need private mortgage insurance (PMI). This can save you $100 to $200 each month, besides to your regular payment.

Step 5: Choose Your Loan Term.

Select 15, 20, or 30 years. A 30-year term gives you the lowest monthly payment but costs the most in total interest. A 15-year term builds equity faster and saves tens of thousands in interest over the life of the loan.

Step 6: Fill In Additional Costs.

Enter your estimated property tax rate (the default is 1.2%), home insurance rate (default 0.35%), and any monthly HOA or maintenance fees. Even small adjustments to these fields change your monthly payment meaningfully.

Step 7: Click Calculate.

Your results appear instantly. Review the greatest affordable home price, your estimated monthly payment, your DTI, and the two visual charts. You can also download a full PDF summary or share your results.

How to Read Your Results

After calculating, four outputs and two charts appear.

Maximum Affordable Home Price: This is the top-end price the calculator recommends based on your inputs and the 36% DTI threshold. Treat it as a ceiling, not a spending target.

Estimated Monthly Payment: This is your full projected housing cost: principal, interest, taxes, insurance, and HOA combined into one number. This is the amount that will leave your bank account every single month.

Debt-to-Income (DTI): This shows what percentage of your gross monthly income goes toward all debts combined. Below 36% is considered a healthy range. Between 36% and 43%, most lenders will still approve a loan, but with stricter conditions. Fannie Mae’s Selling Guide sets a maximum DTI of 45% for many conventional loans, though a lower ratio gives you better rate options and stronger approval odds.

Estimated Interest Rate: This confirms which rate tier your credit score falls into, or shows the rate you entered manually.

Monthly Cost Breakdown Chart: This doughnut chart splits your total payment into principal and interest, property taxes, insurance, and HOA fees. It helps you see clearly where your housing budget actually goes.

Amortization Chart: This line chart shows how your loan balance decreases over time alongside cumulative interest paid. In the early years, most of your payment goes to interest. Over time, more flows to the principal as the balance drops.

Real-World Example

Here’s a concrete scenario to bring the numbers to life.

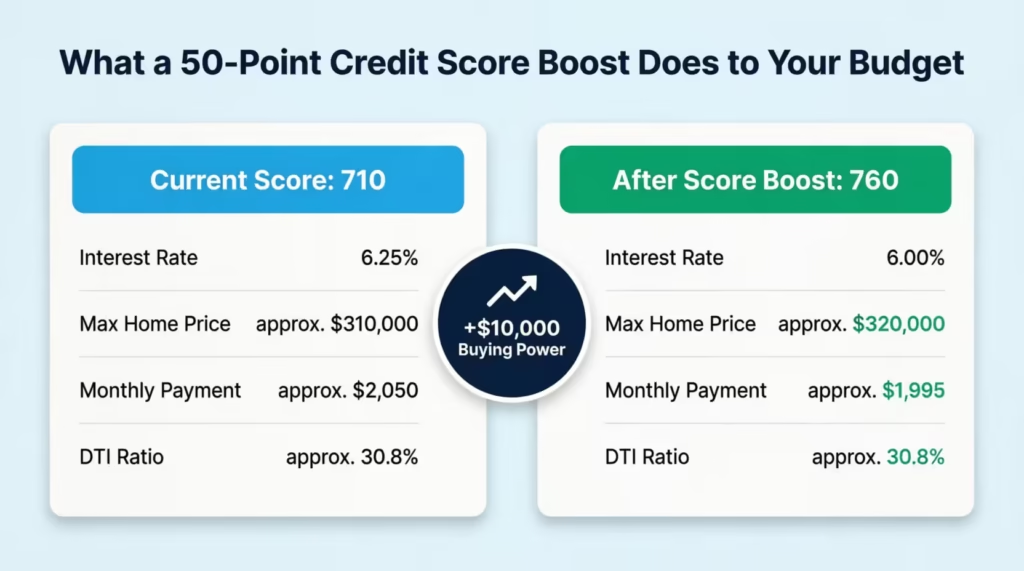

Meet James, a 34-year-old project manager in Columbus, Ohio. He earns $90,000 per year. He has a $400 car payment and $200 in student loan minimums each month, totaling $600 in existing debts. His credit score is 710. He has saved $60,000 for a down payment and plans to use a 30-year loan.

Here’s what the calculator returns:

- Assigned Interest Rate: 6.25% (700 to 759 score tier)

- Monthly Gross Income: $7,500

- Max Monthly Housing Budget: ($7,500 x 36%) – $600 = $2,100

- Maximum Affordable Home Price: approximately $310,000

- Estimated Monthly Payment: approximately $2,050 (principal, interest, taxes, and insurance combined)

- DTI: approximately 30.8%, well within the healthy range

Now James asks a smart question: what if he raised his credit score from 710 to 760 before applying?

At 6.00% instead of 6.25%, the same inputs push his maximum affordable price up to approximately $320,000. That’s about $10,000 more in buying power. This comes from a 50-point credit score boost and a few months of paying down debt.

That’s the real, measurable value of knowing how your credit score connects to your home-buying budget.

Expert Tips and Insights

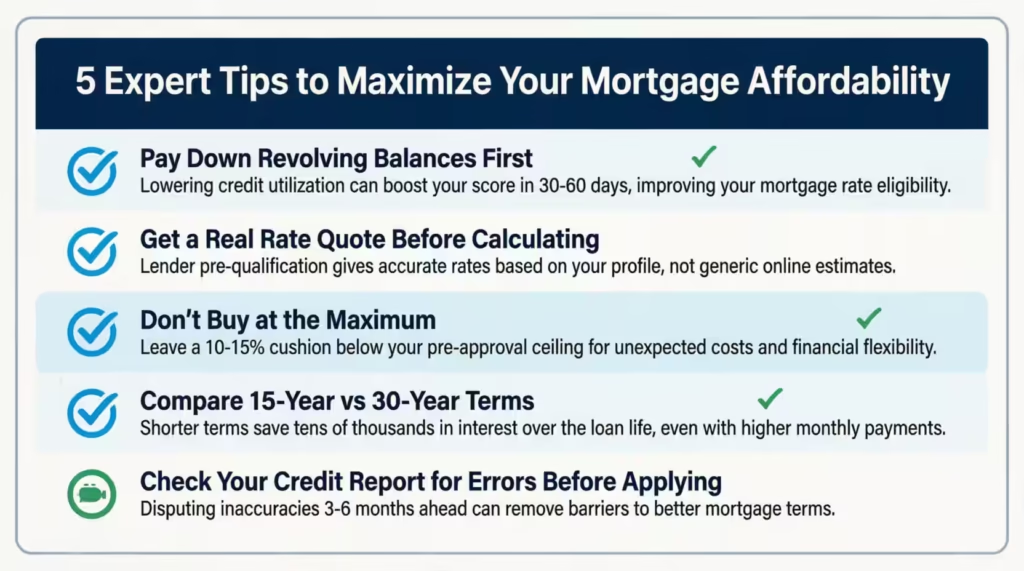

- Pay Down Revolving Balances First. Credit utilization accounts for 30% of a FICO score. Paying credit card balances below 30% of their limits can push your score up noticeably within one to two billing cycles. Even a modest 20-point score improvement can shift you into a better rate tier and increase your buying power.

- Get a Real Rate Quote Before Calculating. The built-in rate estimates are good starting points. However, lenders price risk in different ways. Getting pre-qualified from two or three lenders gives you a real rate to use. This makes your results much more accurate than any estimate.

- Don’t Buy at the Maximum. Lenders approve loans based on income ratios. But life brings unexpected costs: home repairs, job changes, medical expenses. Buy 10% to 15% less than your maximum. This gives you a financial cushion that’s easy to overlook when you’re excited about a home.

📌 Did You Know: Using the calculator for a 15-year and a 30-year loan takes about 30 seconds. However, comparing interest savings can show a cost difference of tens of thousands of dollars over the loan’s life. - Check Your Report Before Applying. Errors on credit reports are more common than most people realize. Disputing a wrong late payment or a mistaken collection account can boost your score. You can do this before you apply, and it doesn’t need any changes to your financial habits.

Common Mistakes to Avoid

- Using Net Income Instead of Gross Income: Always enter pre-tax income. The calculator uses gross income to stay consistent with how lenders calculate DTI. Using take-home pay gives you a lower, inaccurate estimate of what you can afford.

- Skipping Property Tax and Insurance: Many buyers just look at principal and interest. Then they are surprised by the total monthly payment after closing. This calculator factors in taxes, insurance, and HOA fees. That’s why its estimates are more realistic than those from basic payment calculators.

- Ignoring the Interest Rate Override: If you have a pre-approval letter or a specific lender rate, enter it. The auto-populated rate gives a good estimate. However, a real rate from a lender is more accurate and can change your results significantly.

- Treating DTI as the Only Budget Metric: A DTI below 36% is a lender guideline. It doesn’t factor in childcare costs, retirement contributions, tuition, or your emergency fund. Qualifying for a loan and comfortably affording one are two different things.

- Not Updating Your Credit Score Input: If your score changed recently, update it before running the calculator. A 20-point drop can change your rate tier. This may lower your maximum affordable price by thousands of dollars overnight.

Frequently Asked Questions (FAQs)

What credit score do I need to qualify for a conventional mortgage?

Most conventional lenders need a minimum credit score of 620. FHA loans allow scores as low as 500 with a 10% down payment, or 580 with 3.5% down, based on HUD’s FHA program requirements.

What is a good DTI ratio for a mortgage?

A DTI at or below 36% is generally considered strong for conventional mortgage approval. Most lenders allow up to 43% to 45% DTI with strong credit, but a lower ratio gives you better rates and fewer restrictions.

Does the calculator include private mortgage insurance (PMI)?

No, PMI is not included directly. If your down payment is under 20%, expect to add about $50 to $200 each month for PMI costs. This will continue until you reach 20% equity.

How accurate is the interest rate assigned by my credit score?

It’s a realistic estimate based on common score tiers. For the best result, use a real quote from a lender or mortgage broker in the rate field before finishing your final calculation.

Can I use this calculator if I am self-employed?

Yes. Enter your annual net income as your gross income figure. Lenders usually look at two years of self-employment income. So, your qualifying income might not match your latest tax return.

What happens if my DTI result is above 36%?

The calculator will still show a result, but you may see a warning. A DTI above 36% means your budget is stretched. Some lenders approve loans up to 43% to 45% DTI, but your interest rate and loan conditions may be less favorable.

Does a larger down payment always raise my maximum affordable home price?

Yes. A larger down payment reduces your loan principal, which lowers your monthly P&I payment. That frees up more of your monthly budget, allowing you to qualify for a higher home price.

How does the loan term choice affect my results?

A 15-year term increases your monthly payment but saves you significantly in total interest. A 30-year term lowers your monthly payment. This can increase how much home you can afford. However, it ends up costing more over the loan’s lifetime.

Conclusion

Understanding what you can afford doesn’t have to be a mystery. It comes down to knowing your income, your debts, your credit score, and how they all work together to produce a reliable home price.

We’ve covered how the calculator works, what each result means, a real-world example, and common mistakes that can affect your numbers.

Run the test twice: first with your current credit score, and then with a score increased by 30 to 40 points. That comparison might make you think about paying down debt first. Spending a few months on this could save you thousands when you start touring homes.

If this guide helped you, share it with a friend or family member who’s thinking about buying a home.