Credit Card Rewards Calculator

Estimate your annual rewards based on your spending patterns

Enter Your Spending

Average US Consumer

$600 groceries, $300 dining, $200 gas, $150 travel, $250 other

Family Grocery-Focused

$900 groceries, $200 dining, $100 gas, $250 travel, $450 other

Frequent Traveler

$400 groceries, $400 dining, $800 gas, $150 travel, $300 other

Enter spending like "Groceries 600, Dining 300" to auto-fill categories

High spending detected

Is this annual amount correct? Values over $1,000,000 may be truncated for display.

Your Rewards Estimate

Total Annual Rewards

Enter your spending amounts to see reward estimates

Card Comparison

| Card | Annual Rewards | Net Value | Effective Rate |

|---|

Rewards Breakdown

| Category | Annual Rewards | Percentage |

|---|

Share & Save

How to Use

Enter your monthly or annual spending by category (or choose a preset).

Add up to 6 cards to compare or use recommended presets.

View results — total annual rewards, net value after fees, and visual breakdown. Download PDF, share, or copy a permalink.

Tips

Use the quick presets for common spending patterns

Compare multiple cards to find the best fit

Consider annual fees when evaluating net value

Points values are estimates and may vary

Disclaimer

This calculator is for informational purposes only. The results are estimates based on the information you provide and may not be accurate or applicable to your specific financial situation. The information provided does not constitute financial, legal or tax advice. We do not guarantee the accuracy of the calculations or the applicability of any information. Always consult a qualified financial professional for advice specific to your personal circumstances. Credit card terms, conditions, rates and offers are subject to change by the issuing bank at any time. We are not responsible for any actions or decisions taken based on the information provided by this tool.

You’ve been swiping your card at grocery stores, gas stations, and restaurants all year. But do you actually know what you’re earning back? Most cardholders don’t.

The Consumer Financial Protection Bureau’s 2025 market report found that rewards cards now account for 92% of all general-purpose card purchase volume in the U.S. Yet billions in earned rewards go untracked every year. Using a credit card rewards calculator puts those numbers right in front of you.

The answer is simpler than you think: enter your spending by category and get your full annual rewards estimate in seconds.

Get the full formula, a real-world example, expert tips, and step-by-step guidance. This will help you get more value from every dollar you spend.

What Is a Credit Card Rewards Calculator?

A credit card rewards calculator is a free tool that estimates how much cash back, points, or miles you can earn based on your actual spending habits. You enter how much you spend across different categories, like groceries, dining, travel, and gas.

The tool then applies each card’s reward rate to those amounts and shows you your projected annual earnings.

This is especially useful when you’re comparing cards before applying. Instead of guessing which one wins, you get a side-by-side view of real numbers.

The CFPB’s 2025 Consumer Credit Card Market Report confirms that rewards cards now account for 92% of all general-purpose card purchase volume in the U.S. Rewards programs have become the dominant force in the card market. But most people still don’t know exactly what they’re earning. This tool closes that gap.

📌 Did You Know: CFPB research found that cardholders who carry a balance from month to month earn just 27% of total rewards while paying 94% of all interest and fees charged. Paying off your balance in full each month makes your rewards worth far more.

How This Calculator Works

This calculator takes your spending and runs it through each card’s reward structure. It breaks spending into six categories:

- Groceries

- Dining

- Travel

- Gas

- Online Shopping

- Other

You choose whether to enter monthly or annual amounts. The tool then applies each card’s category-specific reward rate to your numbers. It calculates total annual rewards, subtracts any annual fee, and outputs your net annual value and effective reward rate.

Two cards are compared side by side by default:

- Chase Sapphire Preferred: $95 annual fee. Earns 2% on dining and travel, 1% on all other categories. Includes a sign-up bonus of $600 if you meet the $4,000 spending threshold in the first year.

- Citi Double Cash: No annual fee. Earns a flat 2% on every purchase, every category. No sign-up bonus.

The calculator ranks both cards from highest to lowest net annual value based on your specific spending. You also get a doughnut chart that shows which category earns you the most in rewards. Results update in real time as you type.

💡 Pro Tip: Try the quick presets before manually entering your numbers. The “Average US Consumer,” “Family Grocery-Focused,” and “Frequent Traveler” presets fill in realistic spending amounts instantly. They give you a solid benchmark before you fine-tune with your actual figures.

The Formula Explained

Here’s the exact math the calculator uses. It runs calculations in cents to avoid decimal rounding errors. All results display in dollars.

Step 1: Convert to annual spending

If you enter monthly figures, the calculator multiplies each category by 12.

Annual Spend = Monthly Spend × 12

Step 2: Calculate rewards per spending category

For each category, the tool multiplies your annual spend by the card’s reward rate for that category.

Rewards per Category = Annual Spend × (Reward Rate ÷ 100)

Step 3: Add up total annual rewards

All category rewards are summed together.

Total Annual Rewards = Groceries Rewards + Dining Rewards + Travel Rewards + Gas Rewards + Online Rewards + Other Rewards

Step 4: Apply the sign-up bonus (if eligible)

The bonus is added only if your total annual spending meets or exceeds the card’s required minimum spend threshold. It’s kept separate from the ongoing net value.

Step 5: Calculate net annual value

This is your real bottom-line number.

Net Annual Value = Total Annual Rewards – Annual Fee

Step 6: Calculate the effective reward rate

This tells you exactly what percentage of every dollar spent you get back.

Effective Rate = (Net Annual Value ÷ Total Annual Spending) × 100

Quick illustration:

Say you spend $700 per month on groceries with a card that pays 3% on that category.

- Annual grocery spend: $700 × 12 = $8,400

- Category rewards: $8,400 × (3 ÷ 100) = $252

- If the card charges a $95 annual fee: net value from this category alone = $157

The effective rate across all categories tells you the complete picture.

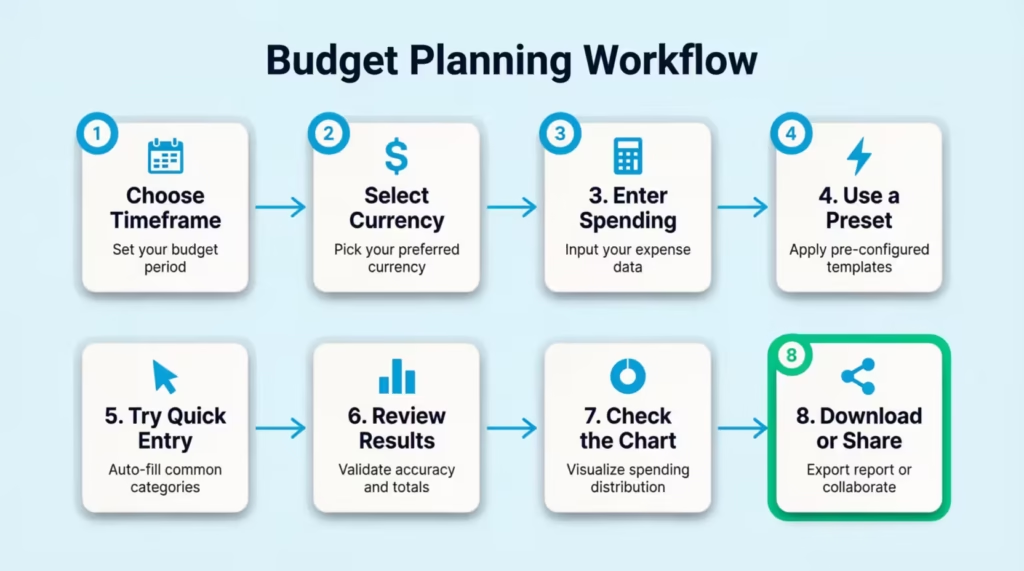

How to Use This Calculator (Step by Step)

Step 1: Choose your timeframe

At the top of the input panel, toggle between “Monthly” and “Annual.” Monthly is the easier starting point for most people since it matches your billing cycle.

Step 2: Select your currency

The default is USD. You can switch to EUR, GBP, or CAD using the dropdown.

Step 3: Enter your spending amounts

Fill in the six spending fields: groceries, dining, travel, gas, online shopping, and other. Each field shows your category’s percentage share of total spending as you type.

Step 4: Or use a quick preset

Don’t have your numbers handy? Click one of the three preset profiles:

- Average US Consumer: $600 groceries, $300 dining, $200 gas, $150 travel, $250 online, $400 other

- Family Grocery-Focused: $900 groceries, $200 dining, $250 gas, $100 travel, $200 online, $450 other

- Frequent Traveler: $400 groceries, $400 dining, $150 gas, $800 travel, $300 online, $250 other

Step 5: Try the Quick Entry field

You can also type something like “Groceries 700, Dining 300, Travel 200” directly into the Quick Entry box. The calculator parses your text and auto-fills the matching fields.

Step 6: Review your results

The results panel updates in real time on the right side. You’ll see total annual rewards, net annual value, and effective rate for each card. The best card gets a green “Best” badge.

Step 7: Check the rewards breakdown chart

A doughnut chart shows which categories contribute most to your rewards total. Use this to spot your biggest earning opportunities.

Step 8: Download or share your results

Click “Download PDF” to save a formatted report. You can also share results directly to Facebook, X, WhatsApp, or Reddit, or copy a link to the page.

How to Read Your Results

The results panel gives you three key numbers for each card. Here’s exactly what each one means.

Annual Rewards

This is your gross rewards total before subtracting any fees. It includes the sign-up bonus if your projected annual spending hits the required threshold.

Net Annual Value

This is the number that tells you whether a card is truly worth it. It’s your gross rewards minus the annual fee. A card earning $500 in rewards with a $250 annual fee delivers a net value of $250. Use this to compare cards directly.

Effective Rate

This shows what percentage of your total spending you’re actually getting back. A 1.8% effective rate means you earn $1.80 for every $100 spent. This is the most apples-to-apples comparison you can make across cards with different structures.

The card with the highest net annual value appears at the top of the comparison table with a green “Best” label. That’s the calculator’s recommendation based solely on your spending profile.

Check the doughnut chart to see which category earns the most. If dining earns you the most rewards but you rarely eat out, consider switching your card. Look for one with better rates for groceries or online shopping.

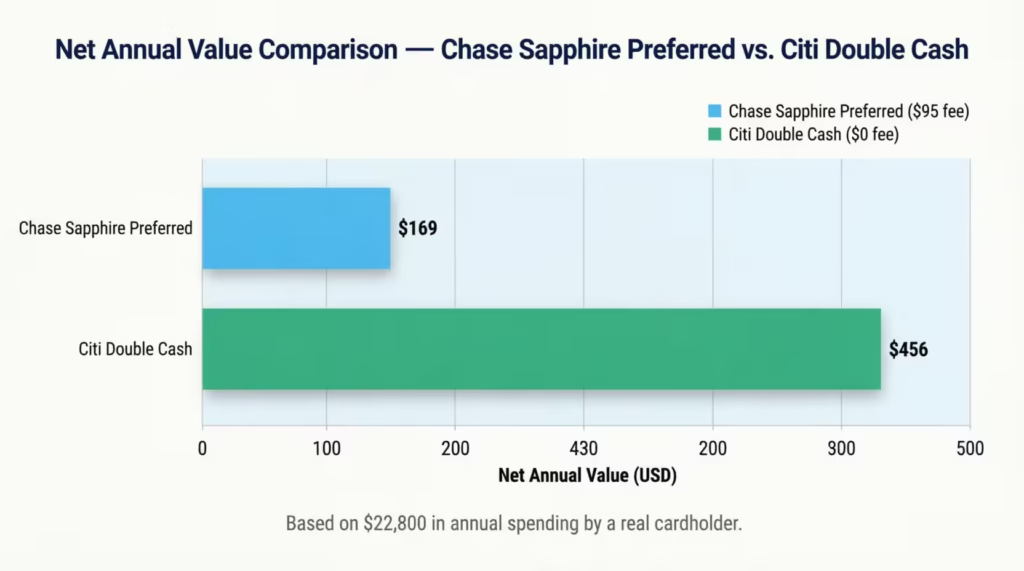

Real-World Example

Here’s how the numbers play out in a real scenario.

Marcus, a 34-year-old high school teacher from Columbus, Ohio, tracked his spending for a month. Here are his averages:

- $750 on groceries

- $200 on dining

- $300 on gas

- $100 on travel

- $350 on online shopping

- $200 on other expenses

That’s $1,900 per month, or $22,800 per year.

He plugged those numbers into the calculator and got these results:

Chase Sapphire Preferred ($95 annual fee, 2% dining/travel, 1% all else):

| Category | Monthly | Annual | Rate | Rewards |

|---|---|---|---|---|

| Groceries | $750 | $9,000 | 1% | $90 |

| Dining | $200 | $2,400 | 2% | $48 |

| Gas | $300 | $3,600 | 1% | $36 |

| Travel | $100 | $1,200 | 2% | $24 |

| Online | $350 | $4,200 | 1% | $42 |

| Other | $200 | $2,400 | 1% | $24 |

| Total | $22,800 | $264 |

- Net Annual Value: $264 – $95 = $169

- Effective Rate: 0.74%

Citi Double Cash ($0 annual fee, 2% on everything):

- Total rewards: $22,800 × 2% = $456

- Net Annual Value: $456 – $0 = $456

- Effective Rate: 2.00%

The calculator immediately flags Citi Double Cash as the better card for Marcus. His spending is heavy on groceries, gas, and online shopping. The Sapphire Preferred’s bonus categories (dining and travel) represent less than 16% of his total spending. A flat 2% card earns him $287 more per year.

⚠️ Mistake to Avoid: Never assume a premium travel card beats a flat-rate card without running the actual numbers. If your main spending categories are groceries and gas, the travel card may not benefit you. It only offers bonus rewards for flights and hotels. Because of this, you could be leaving hundreds of dollars on the table each year.

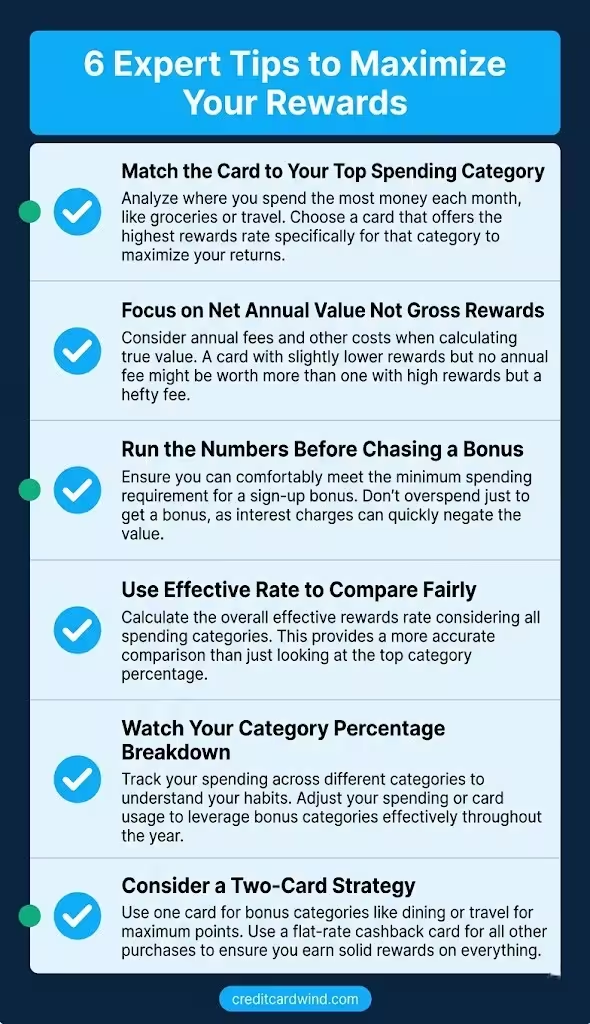

Expert Tips and Insights

Match the card to your top spending category

Your highest-spend category should earn your best reward rate. If you spend $1,000 per month on groceries, look for a card that earns 3% to 6% on grocery purchases. Even a 2-percentage-point difference in rate on that one category can add $240 or more per year.

Focus on net annual value, not gross rewards

A card with a $550 annual fee can still be worth it if the perks match your lifestyle. But the net annual value column shows you whether it actually works in pure dollar terms. Always subtract the fee before comparing.

Run the numbers before chasing a sign-up bonus

Sign-up bonuses look great on paper. But you need to hit a spending threshold in a short window, usually 3 months. The calculator only applies the bonus if your projected annual spending meets that threshold naturally. Don’t overspend just to earn a bonus.

Use the effective rate to compare across different spending levels

When comparing a card with $1,200 in annual spending to one with $24,000, raw rewards totals don’t give a fair picture. The effective rate makes things fair. It reveals the real return for every dollar spent, no matter how much you spend.

Watch your category percentage breakdown

As you fill in your numbers, the calculator shows what percentage of total spending each category represents. This quick snapshot shows where most of your money goes. It might not match your assumptions about where your rewards come from.

Consider a two-card strategy

Many experienced cardholders pair a category bonus card with a flat-rate card. For example, a 6% grocery card for supermarket runs and a 2% flat card for everything else. Run both in the calculator to see if the added complexity is worth the extra rewards.

Common Mistakes to Avoid

Ignoring the annual fee

Always calculate net value, not just gross rewards. A card earning $400 in rewards with a $450 annual fee actually costs you $50 per year to hold. This is one of the most common and costly oversights.

Using rough spending guesses instead of real numbers

The calculator is only as accurate as your inputs. Pull up your last two or three credit card or bank statements and use actual monthly averages. Even a $200 difference per category can shift the result by $50 or more annually.

Picking a card purely for the sign-up bonus

Offers like “Earn $600 after spending $4,000 in 3 months” are appealing, but they’re one-time events. The calculator models your ongoing annual value. Long-term reward rate and annual fee matter far more than any intro bonus for total lifetime card value.

Assuming all reward points have the same value

Cash back has a fixed value of 1 cent per cent earned. Points can be worth more, sometimes 1.5 to 2 cents or even higher when using travel transfer partners. But if you redeem them for gift cards or merchandise, their value may drop. This calculator uses standardized point values, so the actual value may differ based on how you redeem.

Letting a high gross rewards number distract you from the net picture

Jennifer, a freelance graphic designer in Austin, Texas, was thrilled to see $790 in gross annual rewards on her premium travel card. Then she subtracted the $550 annual fee. Her net value dropped to $240. Her effective rate on $26,000 in annual spending came out to just 0.92%. She ran the Citi Double Cash scenario and found she’d earn $520 net instead. The switch was a straightforward $280-per-year improvement.

Forgetting that bonus category caps change the math

Some cards pay elevated rates only up to a spending cap. A card might earn 6% on groceries, but only on the first $6,000 in annual grocery spending. After that, the rate drops to 1%. If your grocery budget exceeds that cap, your real average rate on groceries is much lower than advertised. Adjust your inputs in the “Other” category to simulate the overflow spending at the base rate.

Frequently Asked Questions (FAQs)

How accurate is a credit card rewards calculator?

Results are highly accurate based on the spending data you enter. Rewards can change a bit based on card-specific categories, bonus limits, or updates in reward rates that the tool doesn’t show.

Can I compare more than two credit cards at once?

This calculator compares two default cards side by side. To assess more cards, check each card’s reward rates and annual fee. Then, use your spending details in separate sessions.

Does the calculator include the sign-up bonus in my results?

Yes, but only if your projected annual spending meets or exceeds the card’s required minimum spend threshold. The sign-up bonus is shown separately from your ongoing annual net value.

What is the difference between gross rewards and net annual value?

Gross rewards are the total earned before fees. Net annual value subtracts the card’s annual fee from gross rewards. Net annual value is the number that reflects your actual financial benefit each year.

What does the effective reward rate mean?

It’s the percentage of your total annual spending you receive back as rewards after accounting for the annual fee. A 1.8% effective rate means you earn $1.80 back for every $100 spent, net of fees.

Should I always choose the card with the highest net annual value?

Net annual value is the best single starting point. Consider card perks like travel insurance, purchase protection, and airport lounge access. These add value beyond just the rewards you see in calculations.

What should I do if I don’t know my exact monthly spending?

Review your last two to three credit card or bank statements and calculate a category average. Small variations of $50 to $100 per category won’t dramatically shift the final result for most spending profiles.

Is cash back always better than points or miles?

Cash back offers fixed, predictable value. Points and miles can be worth more, often 1.5 to 2 cents or even more per point. This higher value comes when you redeem them through travel transfer partners. But they require more effort to optimize. Cash back is better for simplicity; points are better for those willing to manage redemptions strategically.

Conclusion

We’ve covered how a credit card rewards calculator works. We discussed the formula, how to read the results, and common mistakes people make. From annual fees to effective rates to sign-up bonus thresholds, there are real details that change which card wins for your wallet.

Begin with the Average US Consumer preset to set a baseline. Then, swap in your actual spending numbers for a clearer picture.

In my experience, most people are surprised by how much the net annual value shifts once they account for their real category mix. Share this guide with a friend who’s choosing their next card. It could save them real money.