Running a business means making fast financial decisions. Hitting a credit limit wall when you need flexibility is one of the most frustrating surprises an owner can face. The Federal Reserve’s 2026 Report on Employer Firms found that 60% of small employer firms applied for financing using credit cards — yet most applied without knowing what limit they’d qualify for before using a business credit card limit calculator.

A business card limit is set using your revenue, personal credit score, debt load, business age, and industry risk.

Here’s a simple guide on how the formula works. You’ll learn what each input means. Plus, you’ll find expert tips to help you present your best numbers before applying.

Business Credit Card Limit Calculator

Estimate your potential business credit card limit before you apply.

How to Use This Calculator

Enter monthly or annual revenue — you can type 240k or 240,000.

Fill in your business age and monthly debt — these help estimate risk.

Add your personal credit score — use the slider or type the number.

Results update live with a detailed explanation of your estimate.

Download a PDF snapshot or share your results with others.

What Is a Business Credit Card Limit?

A business credit card limit is the maximum dollar amount a card issuer allows a business to charge to its card at any given time. Think of it as the ceiling on your company’s spending power for that account.

Unlike personal credit cards, business card limits consider both the owner’s individual creditworthiness and the financial strength of the business itself. That’s why two businesses with the same credit score can end up with very different limits.

The Federal Reserve’s 2026 Report on Employer Firms (findings from the 2025 Small Business Credit Survey) reports that 60% of small employer firms applied for financing using credit cards, making credit cards among the most relied-upon financing tools for small businesses. Yet most owners still apply blindly, with no idea what limit they can expect.

That gap exists because issuers don’t publish their internal formulas. They evaluate several financial signals privately, and the decision can feel like a black box. Understanding what goes into that calculation changes everything.

📌 Did You Know: Business credit card limits are typically much higher than personal card limits. That’s because issuers consider business revenue and financial health. They do this with personal creditworthiness. This means qualifying businesses can access much more spending power than with just a personal card.

Key Factors That Determine Your Business Credit Limit

Issuers weigh a combination of financial signals when deciding how much credit to extend:

- Annual and monthly revenue: Your income signals how much debt you can realistically manage and repay.

- Personal credit score: Most small business issuers still rely heavily on the owner’s personal FICO score, especially for newer companies.

- Business age: Older businesses are seen as lower risk. Two years of operating history looks far more stable than six months.

- Monthly debt obligations: High debt payments reduce the credit a lender will safely extend to you.

- Existing credit lines: Responsible use of existing business credit is a positive signal — unless you’re already heavily leveraged.

- Industry risk: A SaaS company and a restaurant operate under different financial risk profiles. Lenders price this into your limit.

- Profit margin: Healthier margins can boost your score even when revenue is moderate.

How This Calculator Works

The business credit card limit calculator uses a weighted scoring model. This model mirrors the logic that card issuers actually apply when determining credit limits. No tool can give you an issuer’s internal number. What it does is produce a reliable estimate based on the same financial signals banks evaluate.

The calculator collects the following data points from you:

- Annual or monthly revenue: If you enter both, the monthly figure takes priority. You can use shorthand like ‘240k’ instead of ‘240,000.’

- Business age: Enter in years using the slider or by typing directly. Values above 10 years receive the maximum age score.

- Personal credit score: Enter a number between 300 and 850, drag the slider, or click a credit band button (Poor, Fair, Good, Very Good, Excellent).

- Monthly debt or debt service: All current monthly debt payments combined — loans, leases, and lines of credit.

- Existing business credit lines: The total dollar amount of any business lines of credit currently open.

- Industry risk level: Choose Low (SaaS, consulting), Medium (retail), or High (restaurants).

- Profit margin (optional): Enter as a percentage, e.g., ’15’ for 15%. The calculator uses industry defaults if you skip this.

- Requested limit (optional): Enter a target amount to compare it against your estimate and see if it’s realistic.

Every input updates the result in real time. There’s no ‘submit’ button — the estimate adjusts as you type. Once results appear, the panel also shows your top three score drivers and a personalized recommendation.

The Formula Explained

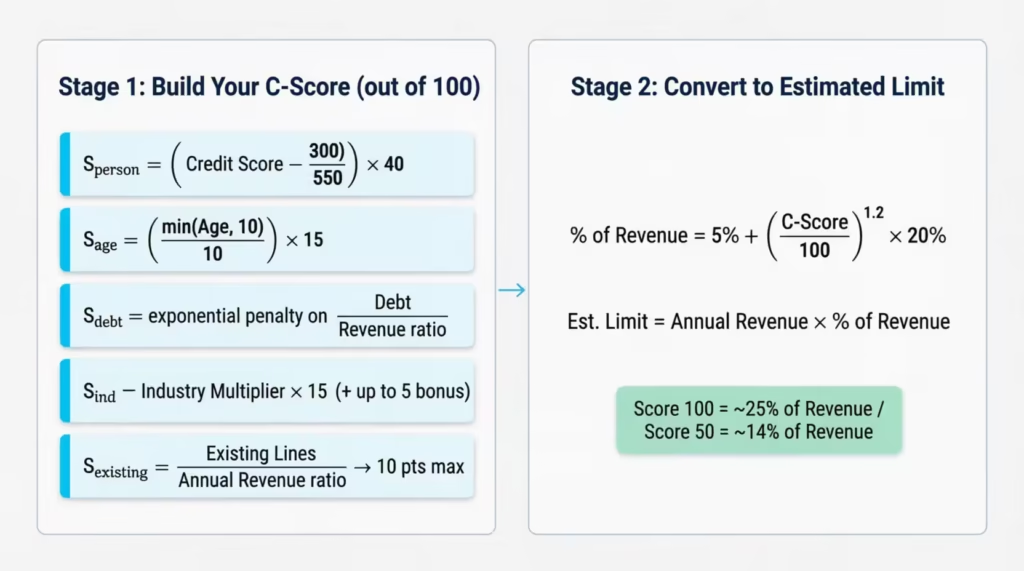

The calculation happens in two stages. First, it builds a composite creditworthiness score (C-score) out of 100 points. Then, it converts that score into a percentage of your annual revenue to produce the estimated credit limit.

Stage 1 — Composite Creditworthiness Score (C-Score)

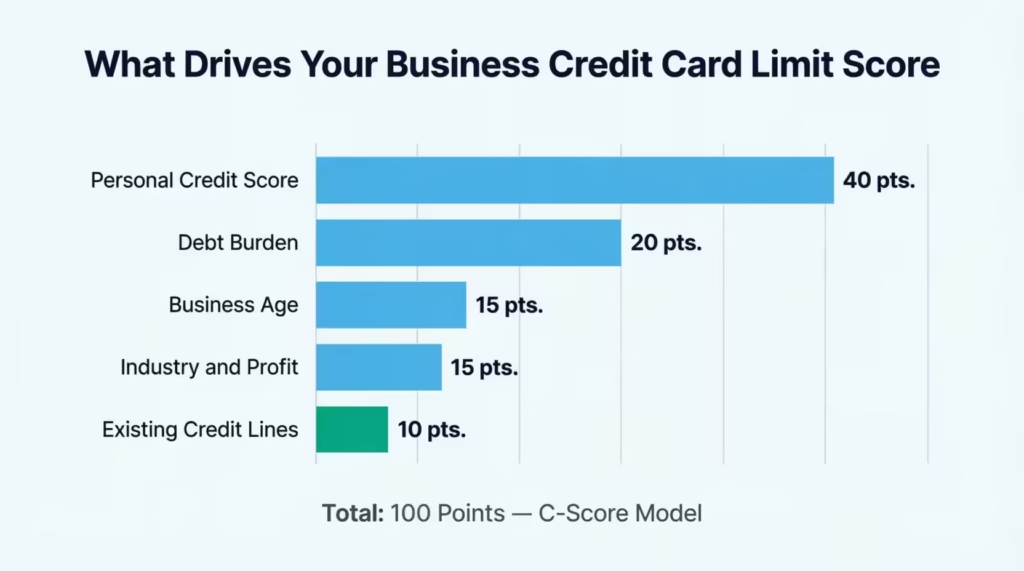

The C-score combines five weighted components:

| Factor | Max Points | What It Measures |

|---|---|---|

| Personal Credit Score | 40 | Owner’s FICO score, scaled from 300 to 850 |

| Business Age | 15 | Years in operation, capped at 10 years for full credit |

| Debt Burden | 20 | Monthly debt as a ratio of monthly revenue |

| Industry and Profit Lines | 15 | Industry risk level plus optional profit margin bonus |

| Existing Credit Lines | 10 | Current business credit relative to annual revenue |

Personal Score (S_person): Uses a linear scale from your credit score.

S_person = ((Credit Score – 300) / 550) x 40

Example: A score of 720 earns ((720 – 300) / 550) x 40 = 30.5 out of 40 points.

Business Age Score (S_age): Caps at 10 years for the full score.

S_age = (min(Business Age, 10) / 10) x 15

Example: A 5-year-old business earns (5 / 10) x 15 = 7.5 out of 15 points.

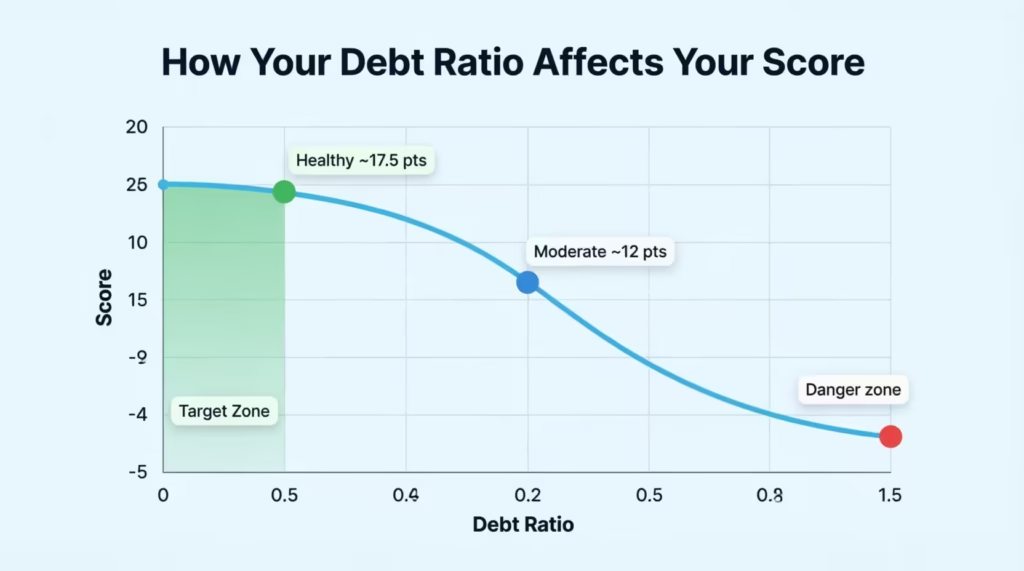

Debt Burden Score (S_debt): Applies an exponential penalty as monthly debt rises relative to revenue.

Debt ratio = Monthly Debt divided by Monthly Revenue.

A ratio below 0.25 earns near-full points. Above 1.5, the component goes negative and pulls the total score down.

Industry Score (S_ind): Combines industry risk with a profit margin bonus.

- Low-risk industries (SaaS, consulting): multiplier of 1.0 — full 15 points possible

- Medium-risk industries (retail): multiplier of 0.7 — up to 10.5 points

- High-risk industries (restaurants): multiplier of 0.4 — up to 6 points

A profit margin bonus of up to 5 additional points can be added on top of the industry base score.

Existing Credit Score (S_existing): Rewards responsible credit use.

- Existing lines below 50% of annual revenue: full 10 points

- Between 50% and 200% of annual revenue: partial credit with a moderate penalty

- Above 200% of annual revenue: zero points (over-leveraged signal)

Stage 2 – Converting Score to Estimated Limit

Once the C-score is calculated, the calculator applies this conversion:

Percentage of Annual Revenue = 5% + (C-score / 100)^1.2 x (25% – 5%)

Estimated Limit = Annual Revenue x Percentage (capped at $2,000,000)

In plain terms: a perfect score of 100 yields roughly 25% of annual revenue. A score of 50 yields about 14%. The floor is 5% regardless of score. The calculator then applies a range band: the low estimate is 60% of typical, and the high estimate is 160% of typical.

💡 Pro Tip: Your debt burden is the fastest score you can move before applying. Cutting your monthly debt payments by 20% before applying can raise your estimate significantly. This often has a bigger impact than any other action.

How to Use This Calculator (Step by Step)

Follow these steps to get the most accurate estimate:

- Enter your revenue. Type your annual or monthly revenue in the corresponding field. You can use shorthand – ‘240k’ instead of ‘240,000.’ If you fill in both fields, the monthly figure takes priority, and a blue note will appear to confirm this.

- Set your business age. Use the slider or type the number directly. Businesses under two years will get a more cautious estimate. This better matches what most issuers actually do.

- Adjust your personal credit score. Drag the slider, type the number, or click one of the five credit band buttons (Poor, Fair, Good, Very Good, Excellent). This single input carries 40% of the total weight, so accuracy here matters most.

- Add your financial details. Fill in your total monthly debt service and any existing business credit lines. These fields are optional but strongly recommended. Skipping them keeps your estimate at Medium confidence.

- Select your industry risk. Choose Low, Medium, or High from the dropdown. Think about how stable your cash flow is. Predictable recurring revenue (like SaaS or consulting) is low-risk. High overhead and volatile revenue (like restaurants) are high-risk.

- Add your profit margin if you know it. Enter it as a whole number, such as ’15’ for 15$. If you skip this step, the calculator will use industry defaults. It assigns 20% for low-risk businesses, 10% for medium-risk, and 8% for high-risk ones.

- Enter a requested limit (optional). If you have a target limit in mind, type it in. The calculator will compare your goal against your estimated range and warn you if it looks unrealistic.

- Review your results instantly. The right panel shows real-time updates. You’ll see your typical, low, and high estimates. It also displays your confidence rating and your top three score drivers. Plus, there’s a personalized recommendation just for you.

How to Read Your Results

The results panel gives you several distinct outputs. Here’s what each one means.

Typical Estimated Limit

This is your central estimate, which is the most likely limit based on the information you provide. You can use it as a baseline to compare different card options or determine how much credit to request.

Low and High Estimates

The range exists because real-world offers vary. Different issuers apply different criteria, so actual limits can fall anywhere in this band. The low estimate is 60% of typical; the high estimate is 160% of typical.

Confidence Level

The confidence rating (Low, Medium, or High) tells you how reliable your estimate is. It rises when you complete more optional fields and when your C-score is above 70. It drops when your debt ratio is high, your credit score falls below 600, or warning flags appear in the results.

Top 3 Score Drivers

These are the three factors contributing the most to your composite score. They also pinpoint where a small improvement would have the biggest impact on your estimated limit.

Actionable Recommendations

The calculator provides a specific, data-driven suggestion based on your numbers. If your monthly debt is above $1,000, it calculates exactly how much your limit could improve if you reduced that debt by 20% before applying.

Requested Limit Comparison

If you entered a target limit, the calculator flags it against your range. If your goal exceeds the high estimate, it suggests applying for a lower amount. If it falls below the low estimate, it signals that you may qualify for more than you’re requesting.

💡 Pro Tip: Click ‘Download PDF’ before you leave the page. It saves all your results, including your score breakdown and recommendations. This is helpful when you compare cards or discuss options with a financial advisor.

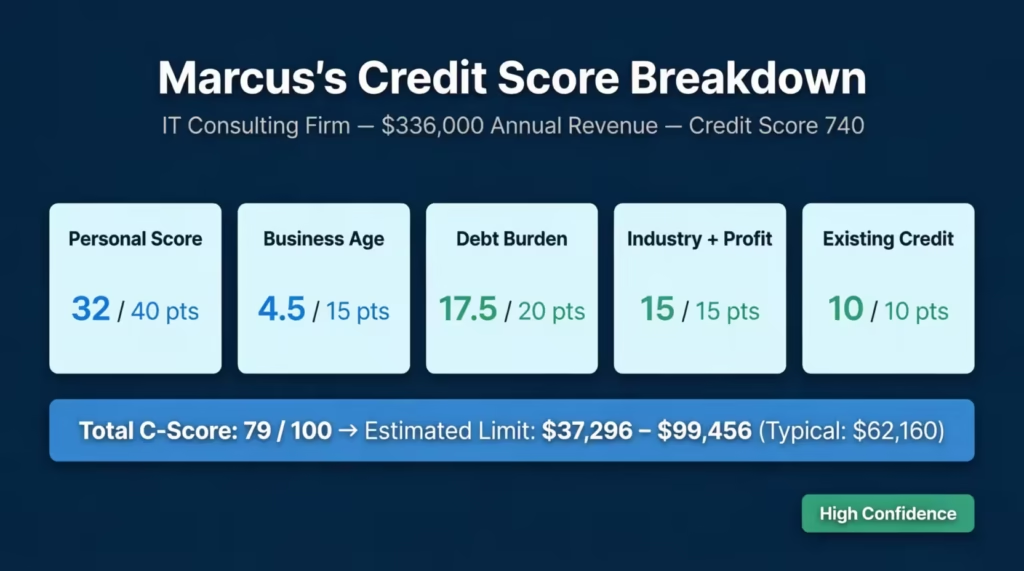

Real-World Example

Meet Marcus, the owner of a three-year-old IT consulting firm in Austin, Texas. He brings in $28,000 per month in revenue, carries $4,200 in monthly debt payments, has no existing business credit lines open, and holds a personal credit score of 740. He selects Low Industry Risk.

Here’s how his score breaks down:

- Personal Score: ((740 – 300) / 550) x 40 = 32 points

- Business Age: (3 / 10) x 15 = 4.5 points

- Debt Burden: Debt ratio = $4,200 / $28,000 = 0.15 (healthy) = approximately 17.5 points

- Industry and Profit: Low-risk multiplier 1.0 x 15 = 15 points (plus a small default margin bonus)

- Existing Credit: No open lines, ratio is 0% of annual revenue = 10 points (full credit)

Total C-Score: approximately 79 out of 100

Annual Revenue: $28,000 x 12 = $336,000

Percentage of Revenue: 5% + (0.79)^1.2 x 20% = approximately 18.5%

Typical Estimated Limit: $336,000 x 18.5% = approximately $62,160

- Low estimate: approximately $37,296

- High estimate: approximately $99,456

Marcus’s result carries a High confidence rating because he completed all optional fields and his C-score is above 70. His calculator recommendation is to maintain his low debt ratio and consider opening a small business credit line now to build his existing-credit score before his next application.

Expert Tips and Insights

1. Focus on Personal Credit Score First

It carries 40% of the total weight. A move from 680 to 740 can shift your estimated limit by thousands of dollars. Pull your credit report before applying and dispute any errors you find. Paying down high-utilization accounts is one of the fastest ways to push your score up.

2. Reduce Monthly Debt Before You Apply

The debt burden component uses an exponential penalty curve. That means small reductions in monthly debt create disproportionately large gains in your score. Aim to bring your debt ratio below 0.25 — that keeps monthly debt under 25% of monthly revenue.

3. Match Your Industry Risk Selection Honestly

Don’t round down to look better on paper. If your business is in a volatile industry, choose Medium, not High. This will help keep your estimate realistic. Issuers are familiar with your industry, so your application won’t fool them.

4. Enter Your Profit Margin for a More Precise Estimate

The profit margin field is optional, but it adds a real bonus to your industry score. A margin of 12 to 15% can push your estimated limit meaningfully higher compared to the industry default. Take five minutes to look it up in your financial statements.

5. Build Business Credit Before You Need a High Limit

Opening a small business line of credit early can help your credit score. Even if you don’t use it much, making timely payments builds your credit history. Starting this process months before a big application gives your profile a real head start.

⚠️ Mistake to Avoid: Applying for a business credit card using personal income instead of business revenue is one of the most common errors. Issuers want to see what the business earns, not the owner’s take-home pay. Combining these two figures can lead to a limit that is much lower than what your business is actually eligible for, or even a denial.

Common Mistakes to Avoid

Mistake 1: Overestimating Revenue

Some owners enter their best month’s revenue rather than a consistent average. If an issuer asks for bank statements, a difference between your application and your actual numbers can raise a red flag. This might lead to a lower limit than you expected.

Mistake 2: Entering Conflicting Revenue Figures

If you input $240,000 for annual revenue and $30,000 for monthly revenue, the calculator finds a problem. It sees a difference of more than 15% between the two amounts. So, it uses the monthly figure instead. Always make sure your two revenue fields are mathematically consistent, or leave one blank.

Mistake 3: Skipping the Debt and Credit Line Fields

Leaving monthly debt and existing credit lines blank keeps the confidence level at Medium. This can lead to an overestimate. Include all regular debt payments. This means loans, equipment leases, and existing lines of credit. Doing this gives you the clearest view of your finances.

Mistake 4: Choosing the Wrong Industry Risk Level

The industry risk multipliers in this calculator are 1.0, 0.7, and 0.4. The difference between Low and High can reduce your score by up to 9 points. Choosing the wrong category skews your result in ways that can lead to a disappointing real-world offer.

Mistake 5: Treating the Estimate as a Guaranteed Offer

This calculator is an educational estimating tool, not a pre-qualification. Card limits can differ by 50% or more from estimates. This depends on the issuer’s models, how you present your application, and current market conditions. Use the result as a guide, not a contract.

Frequently Asked Questions (FAQs)

What is a typical credit limit for a small business credit card?

Small business cards usually have limits from $5,000 to $50,000. But businesses with strong revenue and credit profiles can get higher limits. Some premium cards have no preset spending limit.

Does my personal credit score affect my business credit card limit?

Yes. Most issuers depend on the owner’s credit score. This is especially true if the business doesn’t have a credit history. In this calculator, personal credit score carries 40 out of 100 possible points.

Can a startup get a high business credit card limit?

It’s possible but unlikely. Businesses with less than two years of history tend to receive lower limits. Strong personal credit can partially offset limited business history, but age is still a meaningful factor.

How does my debt-to-revenue ratio affect my limit?

The higher your monthly debt payments are relative to your revenue, the lower your estimated limit becomes. The calculator applies an exponential penalty, so a debt ratio above 1.5 can produce a negative score contribution.

Do existing business credit lines hurt my application?

Not necessarily. Existing lines below 50% of annual revenue score full points and are seen as responsible credit use. The concern starts when credit goes over 200% of annual revenue. This shows that a company is over-leveraged.

What does the confidence rating mean in this calculator?

The confidence rating (Low, Medium, or High) tells you how reliable your estimate is. High confidence means you completed all optional fields and your composite score is above 70. Low confidence usually signals limited data or a credit score below 600.

How do I increase my business credit card limit after approval?

The best way to build credit is to make on-time payments. Also, keep credit use below 30%. Show steady revenue growth, too. Many issuers review accounts periodically and increase limits automatically. You can also request a manual review with updated financials.

Is industry risk a major factor in credit limit decisions?

Yes. Industries with volatile revenue and high overhead are treated as higher risk. In this calculator, the industry multiplier goes from 1.0 (low risk) to 0.4 (high risk). This can change your composite score by as much as 9 points.

What happens if my requested limit is higher than my estimate?

The calculator shows a warning if your target exceeds the high estimate. Applying for an amount outside your estimated range can reduce approval odds. It’s generally better to apply for an amount within your estimated range.

Can I enter annual revenue instead of monthly revenue?

Yes. The calculator accepts either or both. If you enter only annual revenue, it is divided by 12 to derive the monthly figure. If you enter both, the monthly revenue takes priority, and a note appears on the screen to confirm which value is being used.

Bottom Line

We’ve covered what goes into a business credit card limit, how the scoring model works, how to use the calculator step by step, and how to interpret every piece of your results. The key takeaway is simple: your limit isn’t random, it’s driven by five measurable factors, and understanding them gives you control.

I prioritize personal credit scores because they have the greatest impact on the model. They offer the best opportunity for improvement. You can dispute errors on your credit report before applying to ensure accuracy.

If this guide helped you, please share it with a fellow business owner who’s prepping an application. It could save them a lot of guesswork and help them walk in with confidence.