Running company credit cards without written rules puts every business at risk. Charges slip through. Receipts go missing. Finance teams waste hours chasing approvals that should be automatic.

According to the ACFE’s 2024 Report to the Nations, expense reimbursement fraud is one of the most frequently reported forms of occupational fraud across all industries. A clear credit card usage policy template stops those problems before they start.

A corporate card policy puts the rules in writing, so cardholders know exactly what’s permitted before any spending happens.

This guide covers it all: what to include in the policy, how to complete each section, and how to create a system your team will actually use.

Download Your Free Credit Card Usage Policy Templates

Two ready-to-use templates are available to make your setup easier. Each one includes all the core sections your business needs.

Pick the format and paper size that works best for you:

Disclaimer: The Templates & Printables on this site are provided for informational and personal tracking purposes only. This is not financial, legal, tax, or credit advice. While reasonable efforts are made to ensure accuracy, Credit Card Wind makes no warranties as to the completeness, reliability, or accuracy of the calculations generated by these Templates & Printables. Users are responsible for independently verifying all data and calculations. Terms, conditions, rates, regulations, and legal requirements vary by institution, jurisdiction, and individual circumstances.

Always refer to your official statements, account agreements, and applicable laws, and consult a qualified professional before making any financial, legal, or other important decisions. By using these Templates & Printables, you acknowledge that Credit Card Wind and its owner shall not be liable for any damages, losses, or financial consequences arising from the use or misuse of these Templates & Printables.

This universal disclaimer applies to all templates and printables provided by Credit Card Wind (https://creditcardwind.com), created by Robert Williams (Owner at Credit Card Wind).

© Credit Card Wind. All rights reserved.

These templates and printables may be downloaded and used for personal, non-commercial purposes only. Redistribution, resale, or modification for commercial use without permission is strictly prohibited.

What Is a Credit Card Usage Policy?

A credit card usage policy is a formal written document that defines how company-issued credit cards can be used. It outlines which employees are eligible to carry a card, what types of purchases are permitted, how spending limits work, and what happens when someone breaks the rules.

Think of it as the rulebook every cardholder must agree to before they ever swipe a company card.

The policy also protects the business legally. It keeps a record of what was shared with cardholders. This is important if a dispute or disciplinary issue arises.

The ACFE’s 2024 Report to the Nations found that organizations lose a median of 5% of annual revenues to fraud, with asset misappropriation schemes, including expense fraud, among the most frequently occurring types. A documented policy is one of the simplest preventive controls a business can put in place.

📌 Did You Know: A written credit card policy is considered a foundational internal control. Businesses without one are statistically more exposed to expense abuse and unauthorized purchases.

Why Every Business Needs a Corporate Card Policy

A lot of small businesses hand out company cards with nothing more than a verbal understanding. That approach works fine until it doesn’t.

It prevents unauthorized spending. Without a policy, employees might not realize that a personal online order or team lunch is a violation. Written rules remove that ambiguity completely.

It speeds up the approval process. When spending limits and approval rules are clear, finance managers save time. They don’t need to make new decisions for each purchase.

It protects the company in disputes. A signed policy is the best proof if an employee makes an unauthorized charge and the company takes action. Without it, the situation becomes a “he said, she said” problem.

It reduces audit risk. Auditors look for documented controls. A clean, well-maintained expense policy document signals that the finance function is under proper oversight.

It keeps cardholders accountable. When employees sign the acknowledgment section, they accept personal responsibility for every transaction made on their card. That signature carries real weight.

Consider what happened at a mid-sized marketing agency after they required all 14 cardholders to sign a formal corporate spending policy. Within the first quarter, receipt submission rates jumped from roughly 60% to 94%. The finance team went from processing reconciliation exceptions every week to handling them once a month.

What a Strong Credit Card Usage Policy Should Cover

The templates available on this page include all the sections a complete company card policy needs. Here’s what each one does and why it matters.

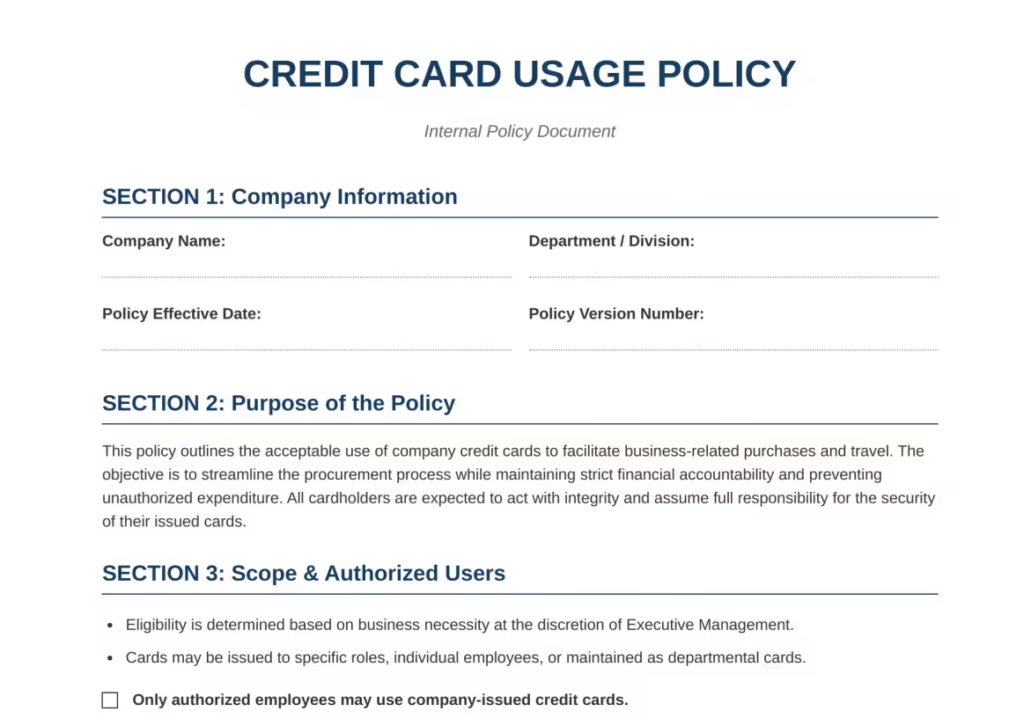

Company or Organization Information

This section identifies the business, the relevant department, the effective date, and the version number. Versioning matters because policies change over time. Keeping a version number lets you track which employees signed which version of the document.

Policy Objective

A brief statement of why the policy exists. This section isn’t just filler. It helps cardholders understand the intent behind the rules, not just the rules themselves. That context makes employees more likely to follow the policy in spirit, not just on paper.

Eligible Users and Cardholder Responsibilities

Not every employee needs a company card. This section explains who qualifies. This includes permanent employees, certain job roles, or departmental cards that a team shares. The cardholder is personally responsible for every transaction. This responsibility includes the duty to report a lost or stolen card immediately to the Finance Department.

Permitted and Prohibited Use

This is the most practical section of any business credit card guidelines document. It lists approved expense categories alongside a clear list of prohibited uses.

Standard permitted categories include:

- Business travel (airfare, lodging, approved ground transportation)

- Vendor payments for authorized hardware, software, or professional services

- Office supplies and emergency operational expenses

Common prohibited uses include:

- Personal purchases of any nature, even if intended to be reimbursed

- Cash advances or ATM withdrawals

- Gambling, alcohol, or entertainment without prior written approval

- Unauthorized online subscriptions or recurring transactions

The clearer this section is, the fewer disputes your finance team will deal with.

Spending Limits and Approval Requirements

Both templates include a table for this section.

The table shows each expense category, including:

- Single transaction limit

- Monthly limit

- Manager approval needed before or after acquisition

This section is what transforms a policy from a vague set of guidelines into an operational tool. A table with actual dollar amounts is far more enforceable than a paragraph that says “reasonable business expenses.”

Receipt Submission and Documentation

This section tells cardholders how to document their purchases and how quickly receipts must be submitted. The US Letter template allows for a 5-business-day period. After that, the charge can be taken from the employee’s paycheck. That single rule eliminates most receipt-chasing situations.

A standard documentation checklist in these templates includes:

- Receipt submitted

- Business purpose is clearly stated

- Transaction date and vendor verified

Monitoring, Review, and Audit Process

Finance teams need the authority to review card statements without giving prior notice. This section gives them that authority in writing. It also tells cardholders that their transactions will be checked often. This usually helps lower policy violations.

Violations and Disciplinary Actions

Both templates use a tiered escalation approach:

- Written warning and policy retraining

- Temporary suspension of card privileges

- Financial recovery from the employee’s payroll

- Disciplinary action up to and including termination of employment

Publishing these consequences ahead of time makes enforcement easier if something goes wrong.

Employee Acknowledgment

The final section is a signature block. The employee confirms they have read and understood the policy and agree to comply. This section also records the last 4 digits of the assigned card. This links the employee to a specific card number for audits.

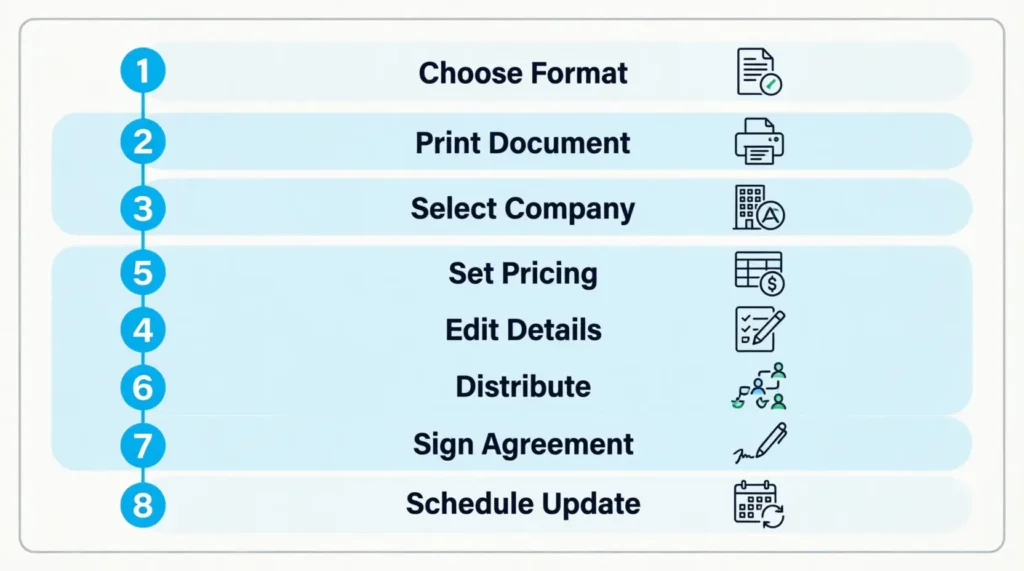

How to Use These Templates

Both downloadable templates are print-ready PDF files. Follow these steps to put them to work for your business.

Step 1: Choose your format.

Download the A4 version if your team uses international paper sizes. Download the US Letter version if you’re printing on standard American paper.

Step 2: Print the template.

Both PDFs are formatted for clean single-page printing. Print one copy per cardholder, plus one master copy for your records.

Step 3: Fill in the company information.

Complete the header area before distributing. Add the company name, department, effective date, and version number.

Step 4: Set your spending limits.

The spending limits table is intentionally left blank. Fill in the dollar amounts and approval requirements that match your actual business rules, by category.

Step 5: Customize the permitted and prohibited use sections.

The templates include standard categories. Add or remove items to match your specific business operations.

Step 6: Distribute to cardholders.

Give every cardholder a printed copy. Walk them through the key sections, especially the permitted use list and the receipt submission deadline.

Step 7: Collect signed acknowledgment pages.

Keep the signed acknowledgment on file for each cardholder. File it with their HR records or in a dedicated compliance folder.

Step 8: Review and update annually.

A policy that’s never updated becomes outdated quickly. Set a calendar reminder to review the document once a year, or whenever a significant change occurs in your expense processes.

💡 Pro Tip: Assign a version number (for example: v1.0, v1.1) every time you make changes. This makes it easy to track which version each employee has signed and whether anyone needs to re-acknowledge an updated policy.

How to Fill Out the Policy Step by Step

Filling out the templates is straightforward. This walkthrough covers the sections that most businesses find confusing on the first pass.

Header fields: Start with the organization name and the name of the policy owner, which is usually the Finance Department or the CFO. The effective date is the date the policy goes live. The review date should be 12 months from the effective date.

Spending limits table: This is the section that requires the most thought. Go through each expense category and set two numbers: the maximum amount per single transaction and the largest monthly total. Then decide whether manager approval is required before the purchase, after the purchase, or not at all.

For example:

- Travel and entertainment: $500 single transaction limit, $2,000 monthly limit, manager approval required

- Office supplies: $150 single transaction limit, $500 monthly limit, no pre-approval required

- Software or IT services: $300 single transaction limit, $1,000 monthly limit, manager approval required

Receipt submission window: Fill in the number of business days your team will use as the receipt deadline. Five business days is the most common standard among small and mid-sized businesses.

Disciplinary escalation steps: The templates provide a standard four-step escalation. Review these steps with your HR team before finalizing. Some states limit payroll deductions for unauthorized expenses. So, check local laws before adding that clause.

Acknowledgment section: Leave this blank until it’s time for each employee to sign. Don’t pre-fill names. The employee should fill in their own full name, job title, card digits, and the date they are signing.

⚠️ Mistake to Avoid: Don’t send the policy as a PDF attachment and assume that downloading it counts as acknowledgment. A printed, signed signature page is the only document that carries real weight in a disciplinary process.

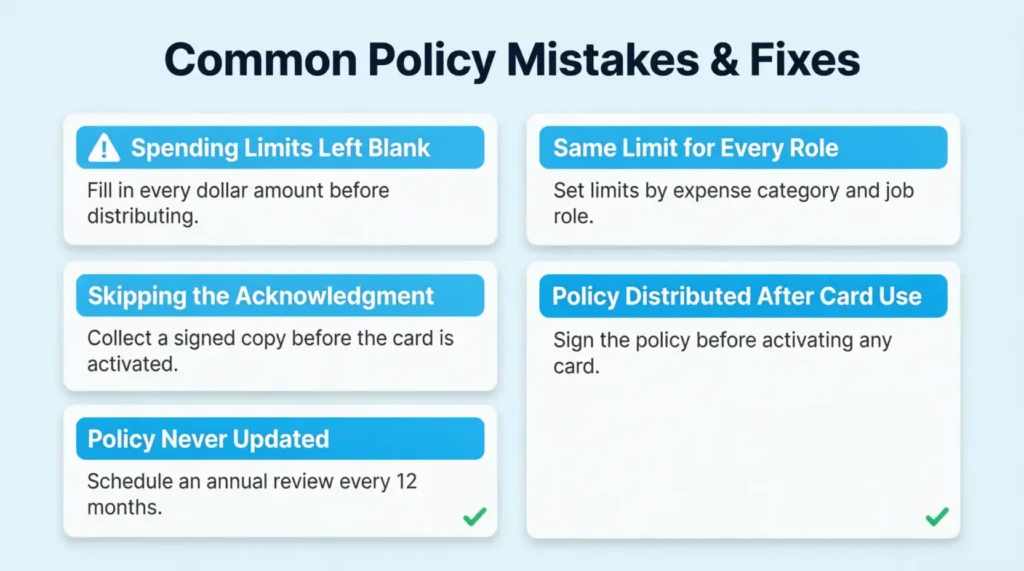

Common Corporate Card Policy Mistakes and How to Avoid Them

Even businesses that already have a policy in place often make these errors.

Leaving the spending limits table blank.

A policy without actual dollar amounts in the limits table doesn’t enforce anything. Cardholders have no way to know when they need approval before spending.

Skipping the acknowledgment step.

Some finance teams distribute the policy by email and assume receipt counts as acknowledgment. It doesn’t. A signed acknowledgment is the only document that holds up in a formal dispute.

Writing the policy once and never revisiting it.

Business expenses evolve. If your company has added new expense categories since the policy was last written, those categories are now unregulated. That’s a gap in coverage.

Setting the same spending limit for every cardholder.

An executive’s travel budget and an operations assistant’s supply budget aren’t the same. The spending limits table in these templates is designed to be filled in by category and role, not set as a single blanket number.

Distributing the policy after the card is already in use.

The policy should be signed before a card is activated. Jennifer, the finance director at a logistics company, found out that three cardholders on her team never saw the policy. It was given out after the cards had been in use for months. When she ran her first formal audit, reconciliation took three times longer than it should have.

Best Practices for Keeping Your Card Policy Effective

Having a policy is the first step. Enforcing it consistently is what makes it work.

Run a monthly statement review.

Both templates include a monitoring and review section for a reason. Finance teams should check submitted receipts against card statements at the end of each billing cycle. They shouldn’t wait until something seems suspicious.

Separate the approval and spending functions.

The employee who approves purchases shouldn’t be the same person submitting them. This basic separation of duties is a standard internal control that Federal Reserve Small Business Credit Survey data consistently flags as a gap in small business financial management.

Train cardholders at onboarding, then again annually.

A one-time briefing isn’t enough. Build a short annual refresher into your finance calendar so cardholders stay current on any policy updates.

Automate receipt collection where possible.

Digital tools that capture receipts at the point of purchase greatly lessen the documentation burden. The policy sets the rules. The tools make those rules easy to follow.

Act on violations consistently.

The disciplinary escalation in the violations section only works if it’s applied every time. If minor violations go unaddressed, cardholders learn the policy isn’t serious. One inconsistency in enforcement can undermine the entire document.

Issue a policy update notice whenever you make changes.

Don’t just update the document quietly. Send a short notice to all cardholders, explain what changed, and collect fresh signatures on the updated version.

Frequently Asked Questions

Does a small business need a credit card usage policy?

Yes. Any business that issues credit cards to employees should have a written policy, regardless of company size. Small businesses face a higher risk of expense fraud. This is mainly because they usually have fewer financial controls than larger companies.

What is the difference between a corporate card policy and a cardholder agreement?

A corporate card policy is an internal company document that sets spending rules and expectations. A cardholder agreement is a contract between the cardholder and the card issuer (the bank). Both are separate documents, and signing a cardholder agreement does not replace an internal company policy.

Can an employer recover unauthorized charges from an employee’s paycheck?

In many U.S. states, yes, if the employee has signed a written policy that includes that consequence. Rules differ by state, so businesses should check local wage and payroll laws. They can do this with their HR or legal team before adding this clause.

How often should a credit card usage policy be updated?

The policy should be reviewed at a minimum once per year. It should also be updated any time spending limits change, new expense categories are added, or the company’s approval structure is reorganized.

What should happen when an employee loses a company credit card?

The employee must report the loss immediately to both the Finance Department and the card issuer. The policy should specify the exact internal contact and the timeline for reporting. Delays in reporting can result in the employee being held personally liable for unauthorized charges made during that window.

Is the acknowledgment signature legally binding?

A signed acknowledgment isn’t a full legal contract. It’s proof that the employee got, read, and agreed to the policy. In HR or legal proceedings, it carries significant weight as evidence that the employee was informed of the rules.

Can one policy cover all departments?

Yes, but the spending limits and approval requirements in the table should be customized by department or job role. A single blanket dollar limit for every cardholder rarely reflects actual business operations.

What is the standard receipt submission window for corporate cards?

Most corporate card policies require receipts within 3 to 5 business days of the transaction. The US Letter template here follows a 5-business-day standard. After that, the charge may be seen as a personal expense. The employee can recover it from their payroll.

Who should review the policy before it goes live?

At minimum, the Finance Department and an HR representative should review the document. If the policy has payroll deductions for unauthorized spending, it’s smart to get a legal or employment attorney to confirm the language. This extra step can be helpful.

What happens if a cardholder violates the policy?

The templates include a four-step escalation process: a written warning, temporary card suspension, financial recovery, and potential termination. The specific outcome depends on the severity of the violation and how many times it has occurred.

Bottom Line

A company credit card policy isn’t a bureaucratic formality. It’s a practical financial control that protects the business. It also sets clear expectations for cardholders and gives the finance team the authority to act when something goes wrong.

The templates here include all key sections:

- Eligibility

- Permitted and prohibited use

- Spending limits

- Receipt requirements

- Monitoring

- Disciplinary escalation

Based on the structure of these documents, the most effective approach is to fill in the spending limits table completely, collect signed acknowledgments before activating any card, and schedule an annual review to keep the document current.

Download the format that fits your paper size, fill in the blanks, and get it signed. It’s one of the simplest steps a business can take to prevent expense issues before they start.

If this helped your finance team or a colleague who manages company cards, share it with them. A solid corporate card policy benefits the whole organization, not just the people who carry the cards.