Many people open their monthly credit card bills and feel instantly confused. The rows of numbers, unfamiliar labels, and multiple balance figures can feel more like a tax form than a simple bill.

Federal Reserve data shows Americans carry over $1.3 trillion in revolving credit card debt, yet many cardholders have never fully studied a sample credit card statement PDF from top to bottom.

A fictional practice statement lets you study every section without the pressure of real money on the line.

Keep reading to download two free templates. You’ll get a plain-English breakdown of every section. Plus, learn the exact habits that transform your real monthly bill into a useful financial tool.

Download Your Free Sample Credit Card Statement Templates

Two ready-to-use templates are available below. Both include every section found on a real bank statement, filled with fictional data so you can study the layout right away.

Pick the format and paper size that works best for you:

Disclaimer: The Templates & Printables on this site are provided for informational and personal tracking purposes only. This is not financial, legal, tax, or credit advice. While reasonable efforts are made to ensure accuracy, Credit Card Wind makes no warranties as to the completeness, reliability, or accuracy of the calculations generated by these Templates & Printables. Users are responsible for independently verifying all data and calculations. Terms, conditions, rates, regulations, and legal requirements vary by institution, jurisdiction, and individual circumstances.

Always refer to your official statements, account agreements, and applicable laws, and consult a qualified professional before making any financial, legal, or other important decisions. By using these Templates & Printables, you acknowledge that Credit Card Wind and its owner shall not be liable for any damages, losses, or financial consequences arising from the use or misuse of these Templates & Printables.

This universal disclaimer applies to all templates and printables provided by Credit Card Wind (https://creditcardwind.com), created by Robert Williams (Owner at Credit Card Wind).

© Credit Card Wind. All rights reserved.

These templates and printables may be downloaded and used for personal, non-commercial purposes only. Redistribution, resale, or modification for commercial use without permission is strictly prohibited.

What Is a Sample Credit Card Statement PDF?

A sample credit card statement PDF is a pre-filled, fictional billing document that mirrors the exact layout of a real credit card statement.

Card issuers are required by federal law to send customers a monthly statement for any billing cycle where a balance exists, a payment is due, or a charge appears. The Federal Reserve’s G.19 Consumer Credit release tracks total revolving credit outstanding in the United States, which surpassed $1.3 trillion in 2024. That figure reflects just how many Americans interact with these billing documents every single month.

The key difference between a sample and a real statement is simple. A sample version uses made-up names, fictional account numbers, and placeholder dollar amounts. This makes it a completely risk-free learning tool. You can trace how each number flows into the next. Get comfortable with the layout, so you’ll build confidence to catch errors on your own real account.

📌 Did You Know: Under the CARD Act of 2009, every credit card statement must include a minimum payment warning. It must show how long it takes to pay off your balance if you only make the minimum payment each month.

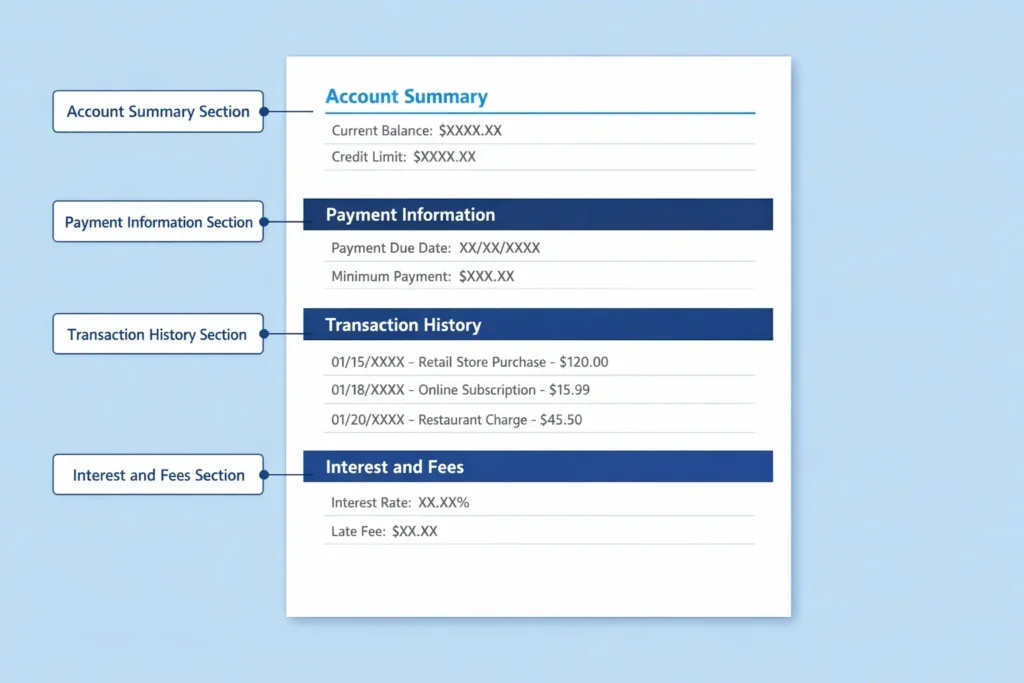

What’s Inside a Credit Card Statement?

A real billing statement fits a lot of information onto one page. Breaking it into four main areas makes the whole document much easier to follow.

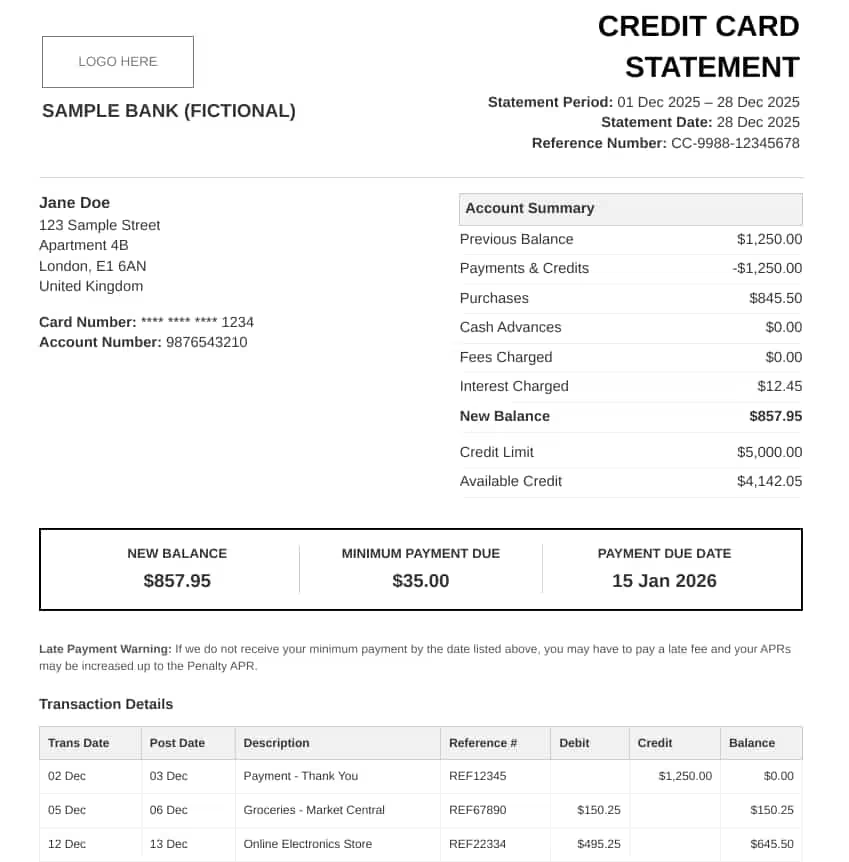

Account Summary

The account summary sits near the top of the page. It gives you a full snapshot of your account activity for the billing period.

- Previous Balance — What you owed at the close of last month’s cycle

- Payments and Credits — Payments you made, plus any merchant refunds

- Purchases — Total new charges added during the billing cycle

- Cash Advances — Any cash you withdrew using your card

- Fees Charged — Annual fees, late fees, or any other account charges

- Interest Charged — Interest applied to your carried balance

- New Balance — Your total amount owed as of the statement date

- Credit Limit — The maximum your issuer allows you to spend

- Available Credit — The remaining spending room on your account

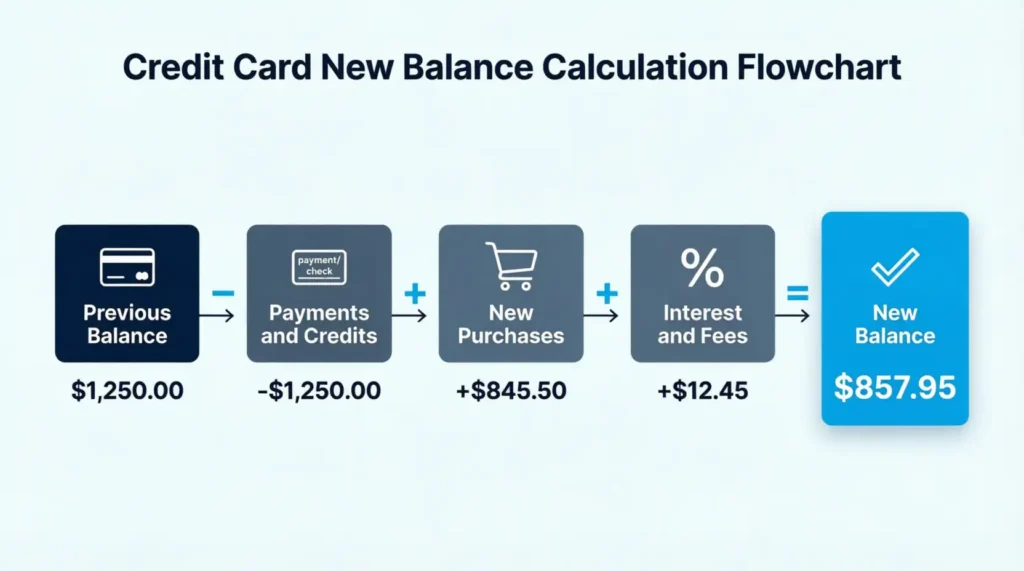

In the A4 template, for example, Jane Doe’s previous balance of $1,250.00 was fully paid. New December purchases of $845.50 and $12.45 in interest brought the new balance to $857.95. That simple chain of arithmetic is how every statement balance is calculated.

Payment Information Box

This section is often the most important part of the entire page. It highlights three figures every cardholder must know:

- Statement Balance (or New Balance)

- Minimum Payment Due

- Payment Due Date

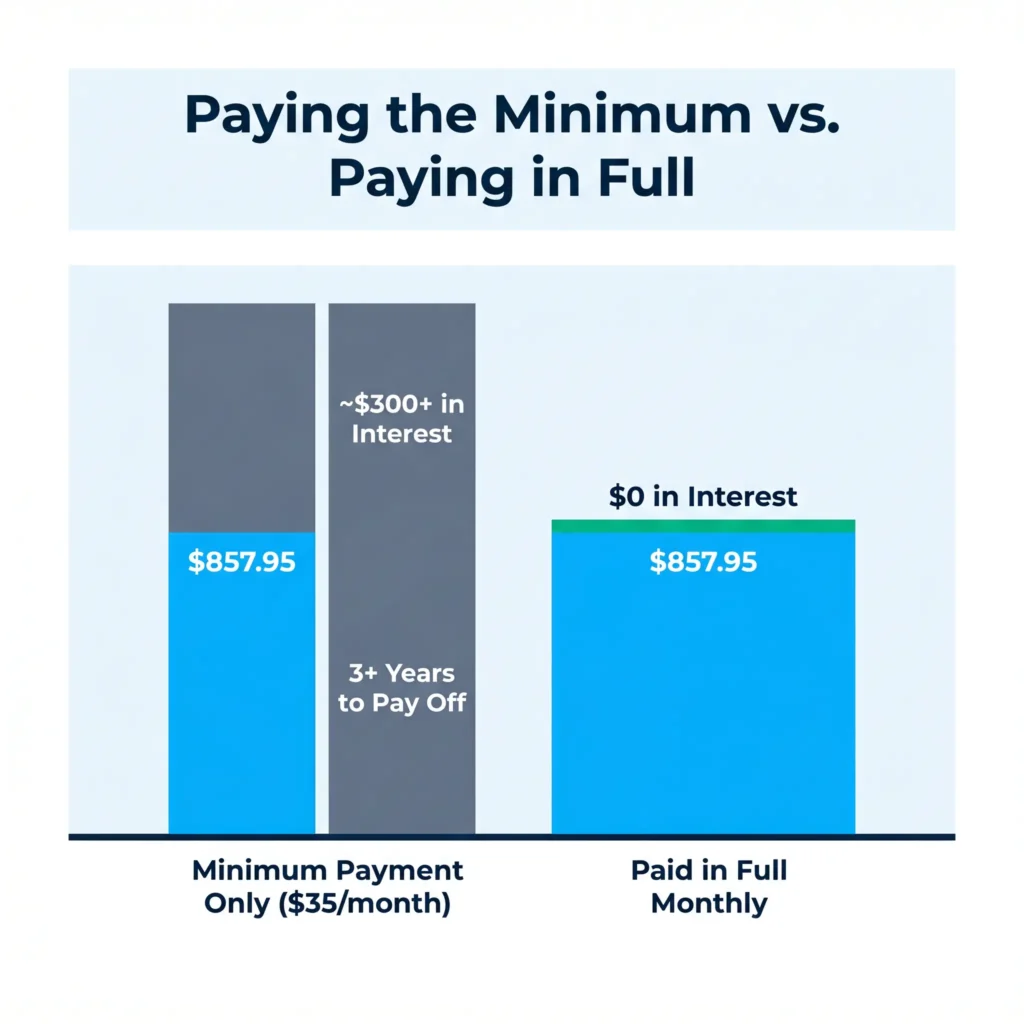

Missing the due date by even one day can trigger a late fee. Both templates show a minimum payment of $35.00 on a balance just under $910.00, which is realistic for most standard consumer credit accounts.

⚠️ Mistake to Avoid: Paying only the minimum keeps your account current, but it doesn’t stop interest from building. A balance of $857.95 at 18.99% APR, paid at $35.00 per month, can take over three years to clear and cost hundreds of dollars in interest alone.

Transaction History

The transaction log lists every charge and payment made during the billing cycle. Each row includes:

- Transaction date and post date

- Merchant description

- Reference or Transaction ID number

- Debit (charge) or Credit (payment) amount

- Running balance after each entry

The US Letter template lists five December entries:

- A grocery store visit

- An online payment

- A tech gadget purchase

- A gas station stop

- A dining charge

Scanning this section each month is the fastest and most reliable way to catch unauthorized activity before it becomes a bigger problem.

Interest and Fees Summary

This section explains exactly how interest was calculated for the period. It shows:

- The APR for each balance type (purchases vs. cash advances)

- The total interest charged in dollars this period

- Any fees applied, including annual fees or late fees

Both templates carry an 18.99% purchase APR. The US Letter version shows a separate cash advance APR of 24.99%. This is common but often overlooked. Cash advances almost always carry a higher rate and rarely come with a grace period.

💡 Pro Tip: If your statement shows $0.00 in interest charged, your issuer granted you a grace period because you paid your full balance last month. Keep that habit and you’ll never pay a cent in interest.

How to Use the Sample Credit Card Statement Templates

These templates work as learning tools, teaching aids, and practice documents. Follow these steps to get the full value from them.

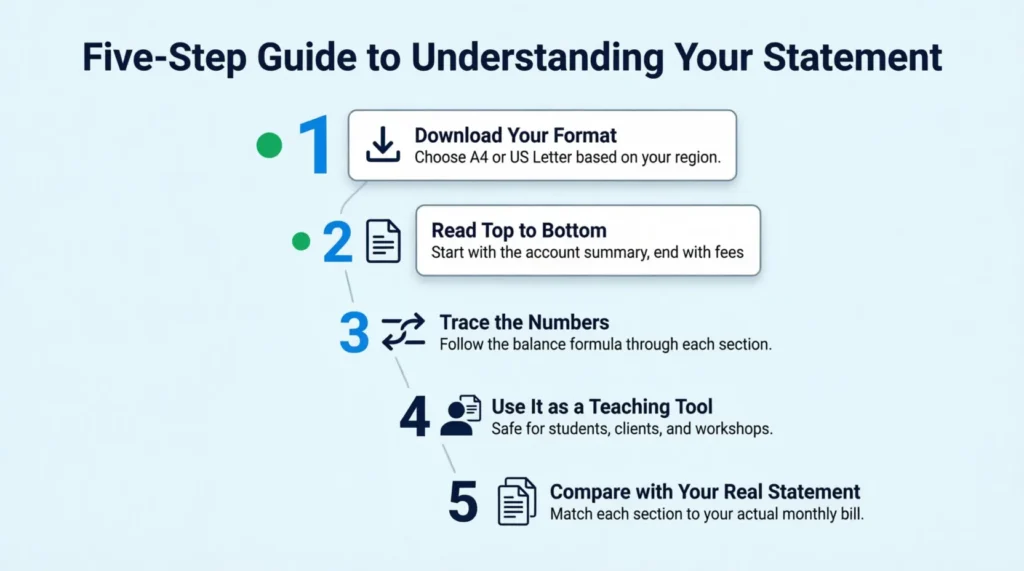

Step 1: Download the format that fits your needs

Choose the A4 version if you’re in the UK, Australia, or most of Europe. Choose the US Letter version if you’re in the United States. Both contain the same core sections.

Step 2: Read from top to bottom

Start with the account summary. Then move to the payment information box. Then review the transaction history line by line. Finish with the interest and fees section. Each part connects to the next, so reading in order builds a clearer picture of how the whole document works.

Step 3: Trace how the numbers connect

The new balance is not a random number. It follows a clear formula: previous balance, minus payments, plus purchases, plus interest and fees, equals the new balance. Tracing this on a fictional document makes it easy to verify the same logic on your real statement later.

Step 4: Use it as a teaching tool

Parents can print the US Letter version and walk through it with teenagers before they apply for their first card. Financial coaches can use either version during group workshops. Because all data is fictional, there’s zero privacy concern.

Step 5: Compare it side by side with your real statement

Once you’re comfortable with the practice layout, pull out your real credit card bill and match each section. Your issuer’s branding and design will look different, but every required section will be present. Federal law under the Truth in Lending Act (TILA) requires all card issuers to disclose the same core information.

Key Differences Between the A4 and US Letter Templates

Both templates teach the same core content, but a few design and data details differ between them.

| Feature | A4 Template | US Letter Template |

|---|---|---|

| Paper Size | A4 (210 x 297 mm) | US Letter (8.5 x 11 in) |

| Cardholder Name | Jane Doe | Jane Q. Sample |

| Address | London, United Kingdom | Chicago, Illinois |

| Statement Period | Dec 1–28, 2025 | Dec 1–31, 2025 |

| Ending Balance | $857.95 | $907.95 |

| Payment Due Date | Jan 15, 2026 | Jan 25, 2026 |

| Cash Advance APR | Not listed separately | 24.99% |

| Fees Section Style | Single combined table | Separated by balance type |

| Layout Style | Bold centered header | Two-column header block |

The US Letter template gives a detailed interest breakdown. It separates purchase balances from cash advance balances. This makes it a slightly more advanced study document. The A4 version is cleaner and works well as a first introduction to statement reading.

Common Mistakes to Avoid

Even experienced cardholders make these errors. Knowing what to watch for saves time, money, and frustration.

Confusing the statement balance with the current balance

The statement balance is what you owed when your billing cycle closed. The current balance includes every new charge made since then. Always pay the statement balance in full by the due date to avoid interest. Your current balance may already be higher.

Ignoring the payment due date

The due date is a hard deadline. Card issuers report late payments to the credit bureaus after 30 days past due. A single missed payment can stay on your credit report for up to seven years.

Misreading credits as charges

Credits reduce your balance. Payments you make, merchant refunds, and cashback rewards all appear in the credit column. Beginners often mix up credit entries with new charges. This confusion can cause them to have the wrong balance in mind.

Overlooking small or unfamiliar transactions

Fraudulent charges often start at just one or two dollars to test whether a card number is active. Reviewing every line, including the small ones, is the most practical fraud detection habit a cardholder can build.

Treating the minimum payment as the finish line

The minimum payment keeps your account in good standing. It doesn’t stop interest from compounding. On an $857.95 balance at 18.99% APR, paying only $35.00 per month means the total cost of those December purchases balloons far beyond the original charges.

Benefits of Using a Practice Statement

A fictional billing document has more real-world value than most people expect.

Financial literacy for first-time cardholders

Students and adults who have never held a credit card can study the document structure without opening a real account. Understanding billing cycles, APR, and minimum payments is key for managing money. Sadly, schools often don’t teach this directly.

Preparation before applying for a card

If you’re comparing credit card offers, a practice statement gives you a concrete preview of the monthly information you’ll be managing. You’ll know exactly what to look for before the first real statement arrives.

Budgeting and expense tracking

Some people use a printed billing template to log their monthly spending. They do this manually before connecting to a digital budget app. Writing numbers by hand builds financial awareness in a way that automated tools often can’t match.

Debt payoff planning

Seeing $12.45 in interest charged on an $857.95 balance makes the cost of carrying a balance concrete and real. That visual connection helps people understand debt payoff math far better than an abstract formula ever could.

Teaching and coaching applications

Financial coaches, school counselors, and personal finance educators can print either template. They can then work through it with clients or students, ensuring privacy is protected. The fictional data makes the document safe to share, project, or distribute in any setting.

How Sample Statements Help Credit Scores

Your credit card statement and credit score are linked, even if they come from different sources. The statement comes from your card issuer. Your credit score is built on data that the same issuer reports to the three major credit bureaus: Equifax, Experian, and TransUnion.

Two figures on your statement carry the most weight on your score.

Credit Utilization Ratio

Credit utilization is the percentage of your available credit that you’re currently using. It’s calculated by dividing your balance by your credit limit.

In the A4 template, Jane Doe’s balance of $857.95 sits against a $5,000.00 credit limit. That’s a utilization rate of roughly 17%. The CFPB advises keeping credit utilization below 30% to protect your credit score. Many credit experts recommend maintaining a utilization rate below 10% when working to improve your score.

Payment History

Payment history is the single largest factor in most credit scoring models.FICO research shows that a single missed payment, reported after 30 days, can drop a good score by 60 to 110 points, depending on your starting score and how recent the missed payment was.

The payment due dates on both templates—January 15 and January 25—are the hard deadlines. These dates show what your issuer would report to the bureaus if these were real accounts. Paying on time, every time, is the highest-impact single habit for building a strong credit profile over the long term.

📌 Did You Know: Your card issuer typically reports your balance to the bureaus on your statement closing date, not your payment due date. Paying your balance down before the closing date lowers the utilization figure that gets reported, which can improve your score faster.

Tips for Managing Real Credit Card Statements

Once you’re comfortable reading a billing statement, these habits keep your accounts clean and your credit health on track.

Set up automatic payments

Even if you plan to pay in full each month, set up auto-pay for at least the minimum. This protects your account if you ever forget. A single late fee and the potential APR increase that follows will cost far more than the five minutes it takes to configure auto-pay once.

Review your statement on the same day each month

Pick a consistent date, such as the first weekend after your statement closes, and treat it like a brief monthly financial check-in. Compare the transaction list against your own spending records. Flag anything unfamiliar and contact your issuer right away.

Watch your utilization rate monthly

Your available credit figure appears on every statement. Tracking it monthly helps you see when your spending nears the 30% utilization limit. This way, you can act before it impacts your score.

Save a PDF copy of every statement

Most card issuers keep digital statements available for only 12 to 24 months. Downloading your copy each month creates a personal archive. This archive helps with tax prep, rental applications, mortgage documents, and fraud disputes.

Read every notice on your statement

Issuers sometimes adjust your APR, change reward program terms, or introduce new fees. These updates are disclosed on or alongside your statement. Reading the full document each month helps you avoid unexpected charges.

Frequently Asked Questions

What is a credit card statement used for?

A credit card statement summarizes all account activity for the billing period. It shows your balance, transactions, fees, interest charges, and the minimum amount due. Cardholders use it to verify charges, track spending, and make on-time payments.

What is the difference between a statement balance and a current balance?

The statement balance is what you owed when your billing cycle closed. The current balance includes new charges made after that date. Paying the statement balance in full by the due date avoids interest charges on those purchases.

How often is a credit card statement generated?

Most card issuers produce a new statement once every 28 to 31 days. The exact dates depend on your account’s billing cycle, which is set when you first open the account.

What happens if I only pay the minimum payment each month?

Interest continues to accrue on the remaining balance. Over time, you can end up paying significantly more than the original charges. Your statement is legally required to show the total cost of paying only the minimum each month.

Can I use a sample credit card statement template as proof of address or income?

No. A fictional template uses made-up names and placeholder data, so it carries no legal or financial validity. Only statements issued by a real financial institution on a real account can be used for verification purposes.

Is a credit card statement the same as a bank statement?

No. A credit card statement covers charges, payments, and interest on a revolving credit account. A bank statement shows deposits and withdrawals from a checking or savings account. Both may come from the same institution but cover entirely different account types.

How long should I keep my credit card statements?

Keep statements for at least one year for general spending records. Hold on to them for up to seven years if they include tax-relevant purchases or business expenses that may be needed during an audit.

What does “available credit” mean on my statement?

Available credit is the difference between your credit limit and your current balance. It shows how much more you can charge before reaching your limit. Keeping this figure high relative to your credit limit helps your credit utilization rate stay healthy.

What is a billing cycle on a credit card?

A billing cycle is the time period covered by one statement, typically 28 to 31 days. All transactions made during that window appear on the resulting statement. New charges made after the cycle closes appear on the next statement.

Why does my statement balance differ from the balance shown in my bank’s app?

Your statement balance reflects the closing date of your billing cycle. The figure in your app is a real-time current balance that includes charges and payments made after the cycle ended. The two numbers update on different schedules and will rarely match exactly.

Bottom Line

A credit card bill is one of the most information-packed financial documents people get monthly. But it rarely includes an explanation. The two free templates on this page cover each section. They include the account summary and details on interest and fees. This way, you’ll know the layout before using real money.

The most effective monthly habit is reading your entire billing document. Don’t just glance at the minimum payment and due date. This way, you’ll understand all the details and avoid surprises. That single routine catches errors and prevents late fees. It also protects your utilization rate and keeps your credit picture accurate.

If you know someone who dreads opening their monthly credit card bill because it feels overwhelming, share this page with them. A few minutes with a fictional statement can spare them from very real financial mistakes.