Struggling to keep up with credit card debt? You’re not alone. The Federal Reserve Bank of New York put Americans’ total card balances at a record $1.17 trillion in Q3 2024. A credit card settlement letter template gives you a professional, structured way to propose a reduced payoff directly to your creditor and start moving toward real financial relief.

A settlement letter is a formal offer to pay less than what you owe. The creditor accepts this offer to close the account for good.

Get free templates you can download. Follow our easy guide to fill them out. Check out expert tips for timing your offer. Find answers to common questions about sending this letter.

Download Your Free Credit Card Settlement Letter Templates

Three ready-to-use templates are available to make the process easier. Each one contains all the sections you need, laid out in the right order.

Pick the format and paper size that works best for you:

Disclaimer: The Templates & Printables on this site are provided for informational and personal tracking purposes only. This is not financial, legal, tax, or credit advice. While reasonable efforts are made to ensure accuracy, Credit Card Wind makes no warranties as to the completeness, reliability, or accuracy of the calculations generated by these Templates & Printables. Users are responsible for independently verifying all data and calculations. Terms, conditions, rates, regulations, and legal requirements vary by institution, jurisdiction, and individual circumstances.

Always refer to your official statements, account agreements, and applicable laws, and consult a qualified professional before making any financial, legal, or other important decisions. By using these Templates & Printables, you acknowledge that Credit Card Wind and its owner shall not be liable for any damages, losses, or financial consequences arising from the use or misuse of these Templates & Printables.

This universal disclaimer applies to all templates and printables provided by Credit Card Wind (https://creditcardwind.com), created by Robert Williams (Owner at Credit Card Wind).

© Credit Card Wind. All rights reserved.

These templates and printables may be downloaded and used for personal, non-commercial purposes only. Redistribution, resale, or modification for commercial use without permission is strictly prohibited.

What Is a Credit Card Settlement Letter?

A credit card settlement letter is a formal written document sent from a debtor to a creditor or debt collection agency. It proposes paying a reduced amount, usually in one lump sum, as a complete and final resolution of the debt.

When the creditor accepts, the account is typically reported as “Settled” or “Settled in Full” on your credit report. That one document can take you from months of collection calls to a clear, documented resolution.

The Federal Reserve Bank of New York’s Q3 2024 Household Debt and Credit Report shows credit card balances hitting $1.17 trillion, a record. That number shows why debt settlement is a popular choice for Americans when their balances get too high.

Debt settlement is not the same as paying off a balance in full. It’s a negotiated agreement. And a well-written letter is what makes that negotiation official and documented in writing.

📌 Did You Know: Creditors often prefer receiving a partial payment over receiving nothing at all. This is especially true after an account has been in default for 90 days or more, because by that point, many creditors have already written the balance off internally as a loss.

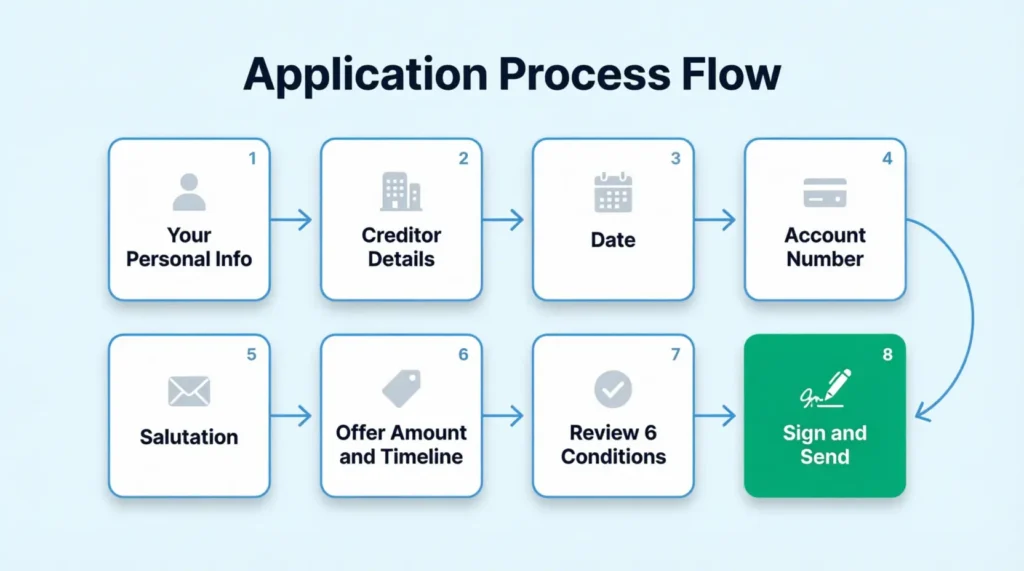

How to Fill In Your Settlement Letter Template (Step by Step)

The template is straightforward, but every field matters. Leaving sections blank or using vague language can weaken your offer. This can happen even before the creditor reads the first paragraph. Follow these steps carefully.

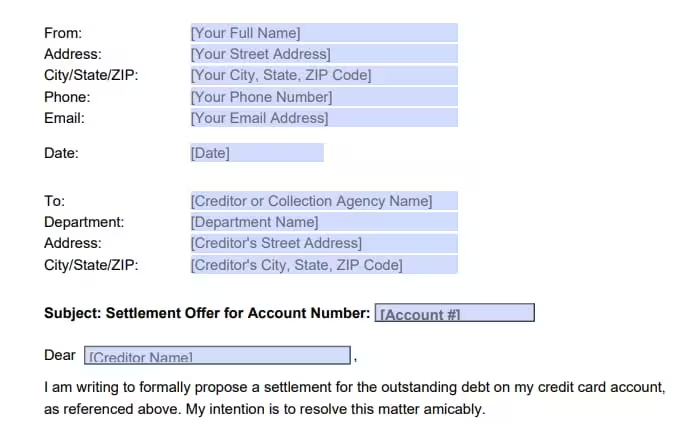

Step 1: Fill In Your Personal Information

At the top of the letter, fill in your full name, mailing address, city, state, ZIP code, phone number, and email address. This is your “From” section.

Use the address where you currently live and receive mail. Creditors may send written responses to this address, so accuracy matters.

Step 2: Add the Creditor’s Information

In the “To” section, list the creditor’s full legal name. Include the specific department for your account, like “Collections” or “Debt Recovery.” Don’t forget their complete mailing address.

If you’re in doubt, call the creditor. Ask them for the specific department and mailing address to use for written settlement correspondence.

Step 3: Enter the Date

Write the full date in standard format: Month Day, Year. For example: June 15, 2025.

The date marks a clear timeline. This is crucial if there’s a dispute about when the offer was made.

Step 4: Add Your Account Number

In the subject line, fill in the account number exactly as it appears on your statement. This helps the creditor locate your account without delays.

💡 Pro Tip: If your account has been sold to a collection agency, include both the original creditor’s account number and the collection agency’s internal reference number. This prevents processing delays and shows the creditor you’ve done your homework.

Step 5: Address the Letter Correctly

After “Dear,” add the full name of the person or department you are writing to. “Dear Collections Department” works well if you don’t have a specific contact name.

A clear, specific greeting reads more professionally and shows you know who you’re dealing with.

Step 6: Fill in Your Settlement Offer Amount and Timeline

This is the most critical part of the letter. Two blanks need your attention:

- Lump-sum payment amount: Enter the dollar figure you are offering to pay. Be specific. Write a number you can realistically deliver within the timeframe you propose

- Payment timeline: Enter the number of days within which you will make the payment after receiving written acceptance. Thirty days is a common and credible timeline. Keep it realistic.

Step 7: Review the Six Settlement Conditions

The template includes six pre-written conditions that protect you throughout the process. Read each one carefully before sending:

- The proposed payment is considered the full and final payment of the debt

- The creditor will stop all collection activity immediately upon acceptance.

- The creditor will report the account as “Paid in Full” or “Settled in Full” to all three major credit bureaus: TransUnion, Experian, and Equifax.

- The creditor will provide written confirmation that the debt is resolved and the account closed.

- The terms of this settlement offer remain confidential between both parties.

- This offer is not an admission of liability in any future legal proceedings

If the creditor wants to change these conditions, talk to a credit counselor or attorney. Don’t agree to new terms without their advice.

Step 8: Sign and Send the Letter

Sign with your full legal name. If you’re using the editable Word template, you can type your name or insert a scanned signature.

Keep a signed copy of the letter for your own records before sending. Send the original by certified mail. Get a return receipt for proof of delivery.

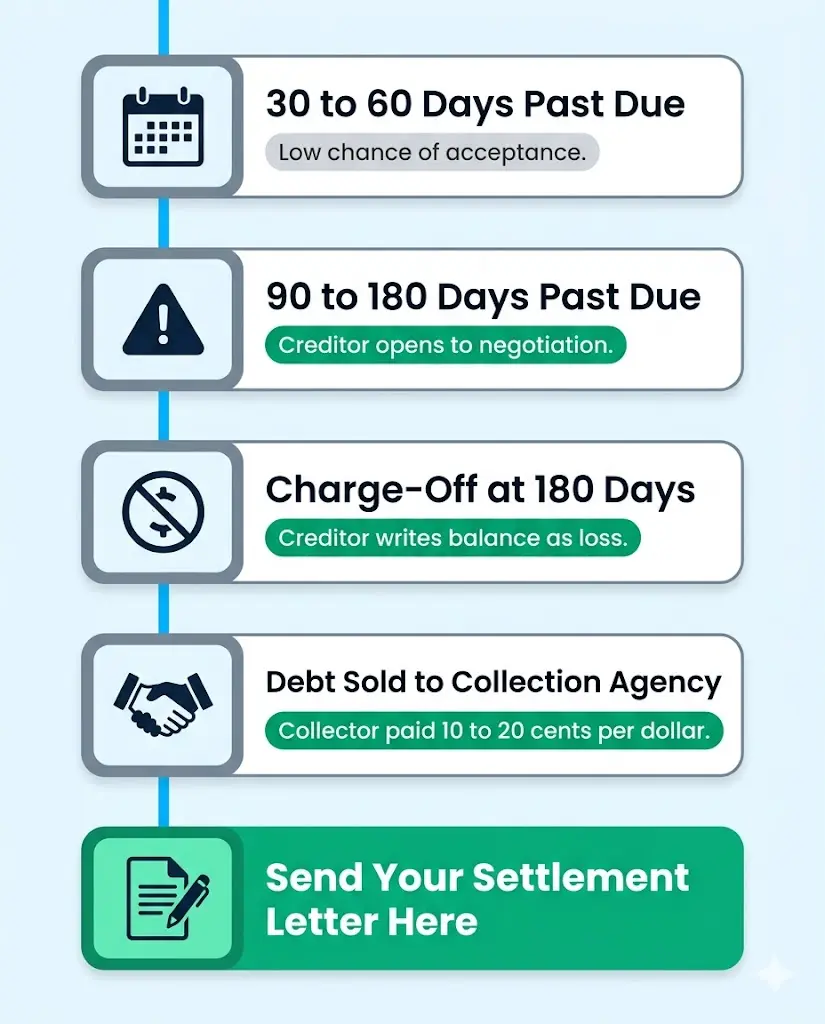

When Should You Send a Debt Settlement Offer?

Timing matters more than most people realize. Timing your settlement offer boosts the chances of acceptance a lot.

The best windows to send a settlement offer:

- After 90 to 180 days past due. At this stage, creditors are much more open to negotiation. The risk of a total loss grows each month.

- After a charge-off. When a creditor charges off an account, it means they have written off the balance as a loss. This usually happens after 180 days of no payment. Recovering even a portion becomes more attractive to them at that point.

- After the debt is sold to a collection agency. Third-party collectors often purchase debt portfolios for 10 to 20 cents on the dollar. That low acquisition cost gives them real flexibility to accept reduced settlement offers.

- During a documented financial hardship. Evidence of job loss, medical bills, or a major life event often makes creditors more willing to consider a lower figure.

⚠️ Mistake to Avoid: Don’t send a settlement offer until you have the lump sum ready and available. If the creditor accepts and you can’t pay within the agreed window, the offer becomes void. Only negotiate when you can follow through immediately.

How to Negotiate a Credit Card Settlement Before You Write

The letter formalizes an agreement, but the real groundwork often happens before anything goes on paper. Knowing how to approach this step can improve your final settlement percentage and save you thousands.

Start by confirming who holds the debt.

Find out whether your account is still with the original creditor or has been sold to a third-party collection agency. The current debt holder is the party you negotiate with, and knowing who that is prevents wasted effort.

Know a realistic starting offer.

Most settlements fall between 40% and 60% of the total balance. However, results can differ. Factors include the age of the debt, the creditor’s policies, and how long the account has been overdue. Starting your written offer at 25% to 30% leaves room for counter-offers without giving away negotiating space.

Make your case before writing.

Call the creditor’s settlement or hardship department. Explain your financial situation briefly before sending the letter. Mention a job loss, unexpected medical expenses, or other documented hardship. This context primes the creditor to take the written offer more seriously.

Never pay before getting written confirmation.

As the FTC advises on settling credit card debt, you should always get the full agreement in writing before transferring any money. A verbal agreement offers no legal protection.

Know your state’s statute of limitations.

Each state sets a time limit on how long a creditor can legally sue you for unpaid debt. This information affects your negotiating position, particularly on older debts. Knowing it before you start discussions puts you in a stronger spot.

Important Tips for a Successful Settlement

Knowing what to write in the letter is one thing. Knowing how to play the negotiation well is another. These strategies improve your chances of landing a better outcome.

Start lower than you can actually afford.

If paying 50% of the balance is realistic, open the offer at 30%. Creditors almost always counter. Leave space between your first offer and your highest limit. This way, you can negotiate and meet in the middle without paying too much.

Have the funds available before you send anything.

Never make an offer you can’t back up immediately. If a creditor accepts a $2,000 settlement, that $2,000 needs to be ready to send within the agreed window. Offers that fall through damage your credibility in future negotiations.

Don’t reveal your maximum in the letter or on follow-up calls.

Let the creditor work to negotiate. Once they know your ceiling, there’s no reason for them to accept anything below it.

Use a cashier’s check or money order for payment.

Avoid giving any creditor or collection agency direct access to your bank account. Once they have your account number, they could potentially withdraw more than what was agreed. A cashier’s check or money order keeps the transaction clean and fully traceable.

Keep every document related to the process.

Keep the original letter and your certified mail receipt. Save the creditor’s written acceptance, your payment receipt, and any follow-up messages. Also, keep a copy of your credit report when it shows the settled status. These records protect you if the account is ever disputed or resold to another collector.

What Happens After You Send the Letter?

Sending the letter is one step. The process doesn’t end there, and knowing what comes next keeps you in control.

A response typically arrives within 5 to 30 business days.

Timelines vary depending on the creditor’s workload and internal review process.

Expect one of three outcomes.

The creditor may accept your terms, reject the offer, or counter with a higher amount. A counteroffer is common and doesn’t mean the negotiation has failed. It simply means both sides haven’t landed on a number yet.

Get written confirmation before making any payment.

Once the creditor accepts your terms, request a formal written settlement agreement. The document must clearly list the agreed amount and payment deadline. It should also confirm that the account will close and be marked as settled.

Use a traceable payment method.

Certified check, money order, or bank wire transfer are the safest options. Avoid cash or informal digital transfers that are difficult to document if a dispute arises later.

Keep every document in a safe place.

Save the original letter you sent, the creditor’s written acceptance, and your payment confirmation. These records protect you if the creditor or a future collector tries to pursue the debt again.

What If the Creditor Doesn’t Respond?

Not every creditor replies quickly. Some don’t reply at all. Knowing what to do when silence follows your letter keeps the process moving.

Follow up with a phone call after 30 days. Call the creditor or collection agency and reference your letter directly. Mention the date it was sent and your certified mail tracking number if you have one. Ask whether they received it and when you can expect a response. Stay calm and professional.

Send a second letter if the call doesn’t move things forward. Reference the first letter by date in the opening line. Restate your offer clearly. Send the second letter by certified mail as well, so you have a new tracking record. Keep your tone neutral and factual.

Consider a different approach if two letters and calls produce nothing. A few options are worth exploring at this stage:

- Offer a slightly higher amount. The initial figure may have been too low for the creditor to take seriously.

- Work with a debt settlement company. These firms have strong ties with major creditors and collection agencies. This helps speed up the process.

- Consult a nonprofit credit counselor. Nonprofit credit counseling agencies can negotiate directly on behalf of debtors. Their involvement typically carries more weight than a solo letter from the debtor.

Be patient but persistent. Collection agencies manage thousands of accounts. Yours can get overlooked in the shuffle. Polite, consistent follow-up every two to three weeks is often what moves a stalled negotiation forward.

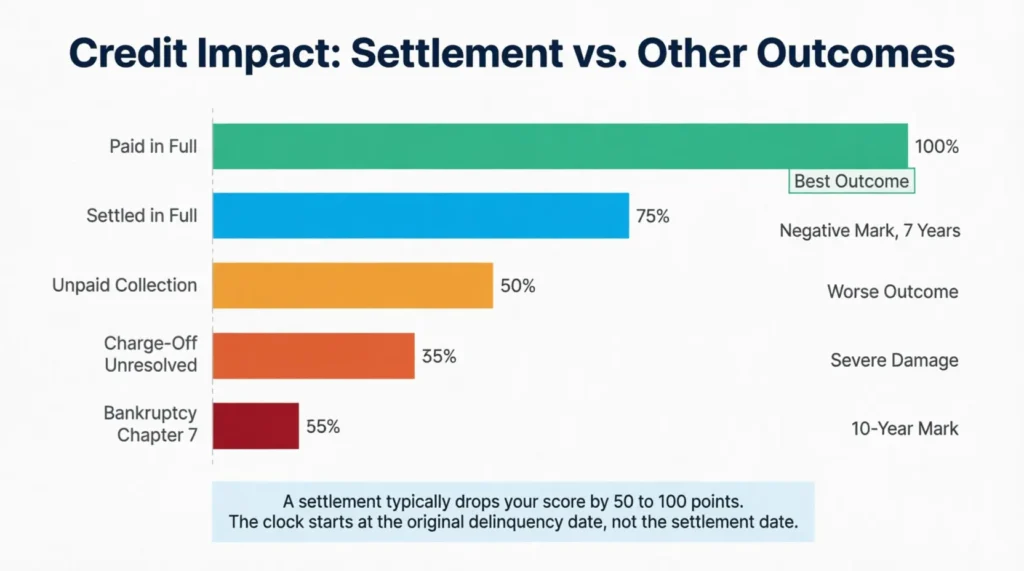

How Debt Settlement Affects Your Credit Score

Knowing the credit impact before you send a letter helps you make better. It keeps you from reacting impulsively.

The short-term impact is negative. A settled account is reported as “Settled” or “Settled for Less Than the Full Amount” on your credit file. This notation is better than an unresolved charge-off or an open collection, but it carries more weight than “Paid in Full.”

To put it in context, a settled account is still a better outcome than:

- Unpaid collections

- Unresolved charge-offs

- Bankruptcy

- Continued missed payments with no resolution

Expect a credit score drop of 50 to 100 points. The exact impact depends on your current score and overall credit history. That said, if the account was already in collections or had been charged off, most of the damage was already done before the settlement letter ever went out. Resolving the account at least stops additional negative reporting.

The negative mark lasts seven years. A settlement entry stays on your credit report for seven years from the original delinquency date, not from the date of settlement. That’s an important distinction many people miss. The clock starts when the account first went delinquent, not when you settled.

Watch out for the tax bill. When a creditor forgives $600 or more in debt, federal rules require them to report it as income using Form 1099-C. IRS Tax Topic 431 covers when cancelled debt is taxable and what exceptions may apply, including insolvency exceptions that some borrowers qualify for. This is a step many people overlook until tax season arrives.

📌 Did You Know: If a creditor forgives $3,000 of a $5,000 balance and you settle for $2,000, the IRS may treat that $3,000 difference as ordinary income for that tax year. Budget for the potential tax bill before finalizing any agreement.

Rebuilding Your Credit After Settlement

Settlement is not the end of the story. Credit recovery is possible, and it starts the same day you commit to a few consistent habits.

- Pay every remaining bill on time going forward. Payment history is the single biggest factor in your credit score.

- Keep balances on active credit cards well below their limits.

- Avoid applying for multiple new credit accounts at once.

- Consider a secured credit card if your score is too low to qualify for a standard card. These report to all three bureaus and build a positive history quickly.

- Becoming an authorized user on a family member’s account can boost your score. This works well if they have a strong payment history. Plus, you won’t need to open a new account.

- Check your credit reports regularly for errors, especially after settlement. Errors are more common than most people expect, and disputing them is free.

Legal Protections You Should Know About

Dealing with debt collectors can be scary. However, federal law provides debtors with real rights that they can enforce. Knowing these protections before you start negotiating puts you in a much stronger position.

Your Rights Under the FDCPA

The Fair Debt Collection Practices Act (FDCPA) is the primary federal law governing what third-party debt collectors can and cannot do. Under this law, a debt collector cannot:

- Call before 8 AM or after 9 PM in your local time zone

- Contact you at work if you’ve told them not to

- Harass, threaten, or use abusive language

- Lie about the amount you owe

- Threatening legal action they don’t intend to take or legally can’t take

- Continue contacting you after receiving a written request to stop, with limited exceptions

These protections apply to third-party collection agencies. They do not apply to original creditors collecting their own debts, though some state laws cover those situations too.

Your Right to Dispute the Debt

Within 30 days of receiving a collection notice, you have the right to dispute the debt in writing. After the collector gets the written dispute, they must pause collection efforts. They need to send written proof of the debt before continuing. Don’t let that 30-day window pass without acting if anything about the debt seems inaccurate.

Your Right to Request Debt Validation

At any point during the collection process, you can request written proof that the debt is actually owed.

The validation must include:

- The name of the original creditor

- The total amount owed

- An explanation of how that amount was calculated

This step is especially important if the debt has been bought and sold multiple times.

State-Level Protections

Many states have consumer protection laws that go beyond federal FDCPA requirements. Some states cap interest on old debt, extend dispute windows, or restrict how collectors can contact debtors. Research your state’s specific rules or consult a local consumer attorney. They can explain any extra protections that may apply to you.

When to Seek Legal Help

Consider speaking with a consumer rights attorney if any of the following apply:

- A collector is violating your FDCPA rights

- You are being sued for the debt

- The balance is large enough that the outcome significantly affects your finances

- You’re not sure whether the debt is actually yours

- You’ve been threatened with wage garnishment

Many consumer attorneys provide free initial consultations. Some also work on contingency. This means they only get paid if they win your case.

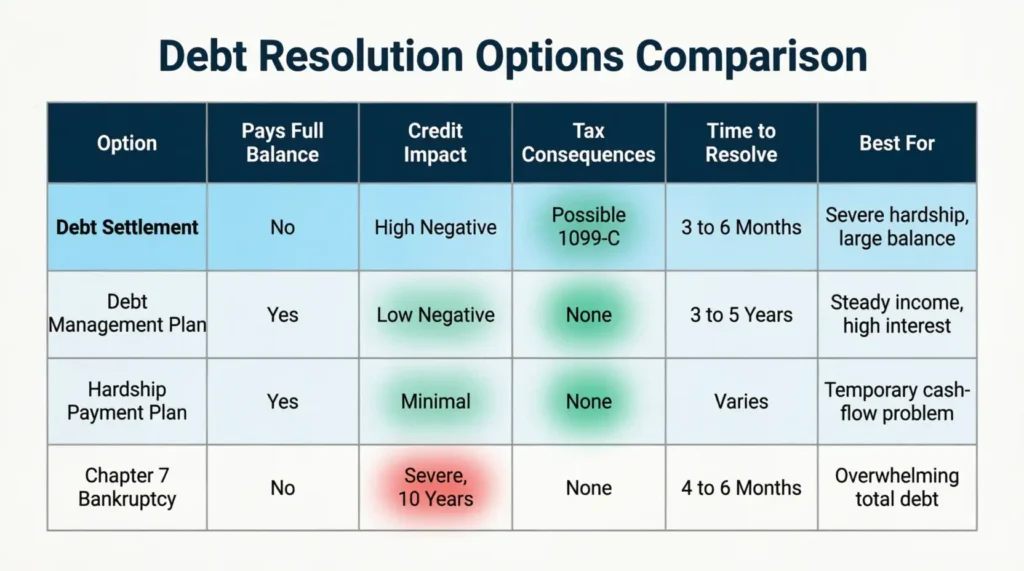

Debt Settlement vs. Other Debt Relief Options

Settlement isn’t the right fit for everyone. Comparing it against other options helps you make a smarter decision for your specific situation.

Debt Management Plans (DMPs) come from nonprofit credit counseling agencies. They help you pay off your full balance at lower interest rates over time. This option protects your credit score far better than a settlement.

Chapter 7 bankruptcy wipes out most unsecured debt but leaves a mark on your credit report for ten years. It’s typically a last resort when all other options have been exhausted.

Many credit card issuers offer hardship payment plans. These plans let you pay at a lower rate without formally settling your account. These plans usually don’t carry the same negative credit reporting or tax consequences.

Each option carries different trade-offs. If you’re unsure which path fits your situation, a nonprofit credit counselor can help you map out a plan before you commit to any one route.

Common Mistakes That Can Derail Your Settlement Offer

A poorly timed or poorly written letter can weaken your negotiating position before a creditor even picks up the phone. Watch out for these errors.

Sending the letter too early.

Creditors have little incentive to settle when your account is only 30 to 60 days past due. Waiting until delinquency is more advanced gives you stronger negotiating leverage.

Offering more than you can pay.

Only offer an amount you can deliver within the agreed window. Breaking the agreement voids it entirely and signals unreliability for any future negotiation.

Paying without written confirmation first.

Paying based on a verbal agreement alone means the creditor could still report the full original balance as unpaid. Never transfer money without a signed written acceptance in hand.

Accepting terms that remove the credit bureau condition.

Condition three in the template requires the creditor to update all three major credit bureaus. If that condition is stripped from the counteroffer, push back. Without it, your credit file may never reflect the resolution.

Forgetting about the Form 1099-C.

Many people are caught off guard by the tax bill that follows debt forgiveness. Account for the potential tax liability before signing any final agreement.

Using emotional language in the letter.

The letter should be factual, professional, and focused entirely on numbers and conditions. Emotional appeals can make the offer feel less credible and harder to take seriously in a business context.

Frequently Asked Questions

What percentage of the debt do creditors usually accept in a settlement?

Most creditors take 40% to 60% of the original balance. However, this can change. It depends on how old the debt is and if it’s with the original creditor or a collection agency.

Is a credit card settlement letter legally binding?

The letter itself is a formal written offer, but it becomes legally binding only when both parties sign a written settlement agreement. Never make any payment until you have that signed document in hand.

How long does it take for a creditor to respond to a settlement offer?

Most creditors respond within 5 to 30 business days. If you haven’t received a response after 30 days, follow up in writing and keep a record of every communication.

Does settling a credit card debt hurt your credit score?

Yes, in the short term. A “Settled” status is better than an unresolved charge-off. However, it still counts as a negative mark. It remains on your credit report for seven years from the original delinquency date.

Do you have to pay taxes on forgiven credit card debt?

Possibly. If the creditor forgives $600 or more, you may receive a Form 1099-C and owe income tax on the forgiven amount. Certain exceptions apply, such as insolvency, so consult a tax professional to see what applies to your situation.

Can I send a settlement offer letter to a debt collection agency?

Yes. If your debt has been sold to a third-party collector, that agency is now the party you negotiate with. Address the letter to the collection agency and include both the original account number and their reference number.

Should I send the settlement letter by certified mail?

Yes. Certified mail with a return receipt gives you documented proof that the creditor received your letter. Keep the tracking number and the signed return receipt with your records.

What happens if the creditor rejects my settlement offer?

You can revise and resubmit with a different amount, or explore alternatives such as a debt management plan or a hardship program. A rejection is not the end of the negotiation process.

Can I negotiate a settlement if my account is still current?

It’s uncommon. Creditors have little reason to settle accounts in good standing. Settlement discussions typically become more productive once an account is significantly past due.

Is it better to settle a credit card debt or pay it in full?

Paying in full is always better for your credit score and avoids any tax complications from forgiven debt. If full payment isn’t realistic, a formal settlement is far better than leaving the account unresolved.

Bottom Line

Carrying unmanageable credit card debt is stressful. However, taking clear and structured action can quickly change your financial trajectory. A well-crafted debt settlement offer provides you with a documented and professional way to engage your creditor. This approach helps you move toward a genuine resolution.

Key takeaways:

- Time your offer well.

- Fill in every field correctly.

- Confirm all terms in writing before you pay.

- Prepare for any credit and tax impacts that may arise.

A complete, condition-specific letter, like the credit card settlement template above, boosts your offer’s chances. It makes your offer more serious and likely to be accepted.

If someone you know is buried in credit card debt with no clear plan, share this guide with them. A structured approach like this could save them months of stress and thousands of dollars.