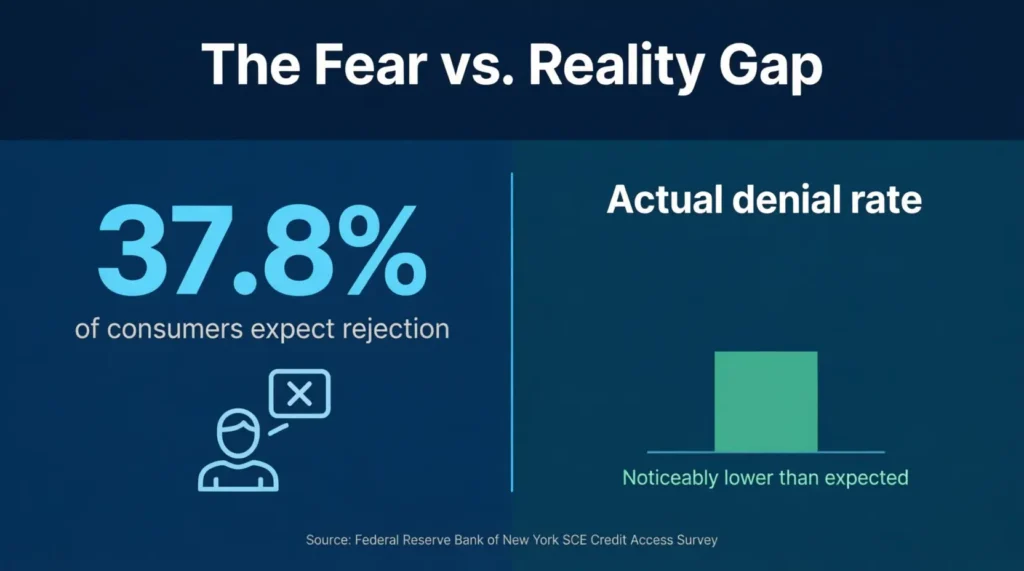

Need more spending room on your card, but don’t know how to ask your bank? A credit card limit increase request letter can feel tricky to write, especially if you’ve never done it before. The Federal Reserve Bank of New York found that 37.8% of people expect to be turned down for a higher limit, yet the real rejection rate sits much lower.

A well-written request letter can boost your approval odds and save you time.

Below, you’ll find free, ready-to-use templates, a step-by-step writing guide, and tips to help your request get approved on the first try.

Download Free Credit Card Limit Increase Request Letter Templates

5 ready-to-use templates are here to make the process simple. Each one covers every section you need, from your personal details to the actual request language.

Pick the format and paper size that works best for you:

Disclaimer: The Templates & Printables on this site are provided for informational and personal tracking purposes only. This is not financial, legal, tax, or credit advice. While reasonable efforts are made to ensure accuracy, Credit Card Wind makes no warranties as to the completeness, reliability, or accuracy of the calculations generated by these Templates & Printables. Users are responsible for independently verifying all data and calculations. Terms, conditions, rates, regulations, and legal requirements vary by institution, jurisdiction, and individual circumstances.

Always refer to your official statements, account agreements, and applicable laws, and consult a qualified professional before making any financial, legal, or other important decisions. By using these Templates & Printables, you acknowledge that Credit Card Wind and its owner shall not be liable for any damages, losses, or financial consequences arising from the use or misuse of these Templates & Printables.

This universal disclaimer applies to all templates and printables provided by Credit Card Wind (https://creditcardwind.com), created by Robert Williams (Owner at Credit Card Wind).

© Credit Card Wind. All rights reserved.

These templates and printables may be downloaded and used for personal, non-commercial purposes only. Redistribution, resale, or modification for commercial use without permission is strictly prohibited.

What Is a Credit Card Limit Increase Request Letter?

A credit limit increase request letter is a formal written document sent to a card issuer asking for a higher spending cap on an existing account. It puts your request in writing, which creates a clear paper trail and shows your bank that you’re serious.

Most people request a higher credit line by phone or through an online portal. But a written letter adds weight. It lets you explain your reasons, attach proof of income, and present your case in a clear, organized way.

The Federal Reserve Bank of New York’s SCE Credit Access Survey reports that many consumers avoid asking for more credit because they fear rejection. The actual denial rate, however, runs noticeably below what most people expect. A strong, formal letter can tip the odds even more in your favor.

Think of it this way. A phone call lasts a few minutes, and the agent moves on. A letter stays in your file. It gives the reviewer all the facts at a glance: your income, your payment track record, and the exact limit you want.

💡 Pro Tip: Some issuers, like Capital One and Discover, use only a soft inquiry for limit increase requests. Ask your issuer before you submit so you know whether it will affect your credit report.

Why Would Someone Need to Request a Higher Credit Limit?

People ask for a bigger credit line for many different reasons. Not all of them involve spending more money. Some of the most common situations include:

Lowering Credit Utilization

Credit utilization is the share of available credit being used at any given time. For example, carrying a $3,000 balance on a card with a $5,000 limit means 60% utilization. That ratio weighs heavily on credit scores. MyFICO notes that amounts owed make up roughly 30% of a FICO Score. A higher limit with the same spending pattern can drop that ratio fast.

Preparing for a Large Purchase

Sometimes a planned expense, like a home repair, a vacation, or a medical bill, exceeds the current limit. Requesting an increase ahead of time avoids a declined transaction at the worst possible moment.

Building a Stronger Credit Profile

A higher overall credit line can help long-term credit health. It signals to future lenders that existing creditors trust the borrower with more money. That trust can make it easier to qualify for a mortgage, auto loan, or better card down the road.

Gaining Financial Flexibility

Life doesn’t always follow a budget. Emergency car repairs, unexpected travel, or sudden family needs can pop up. A larger credit cushion provides a safety net without the need to open a brand-new account.

⚠️ Mistake to Avoid: Don’t request a higher limit just to spend more when the budget can’t support it. A bigger limit only helps if spending habits stay the same or improve. Maxing out a higher limit will spike utilization and hurt the very score it was meant to protect.

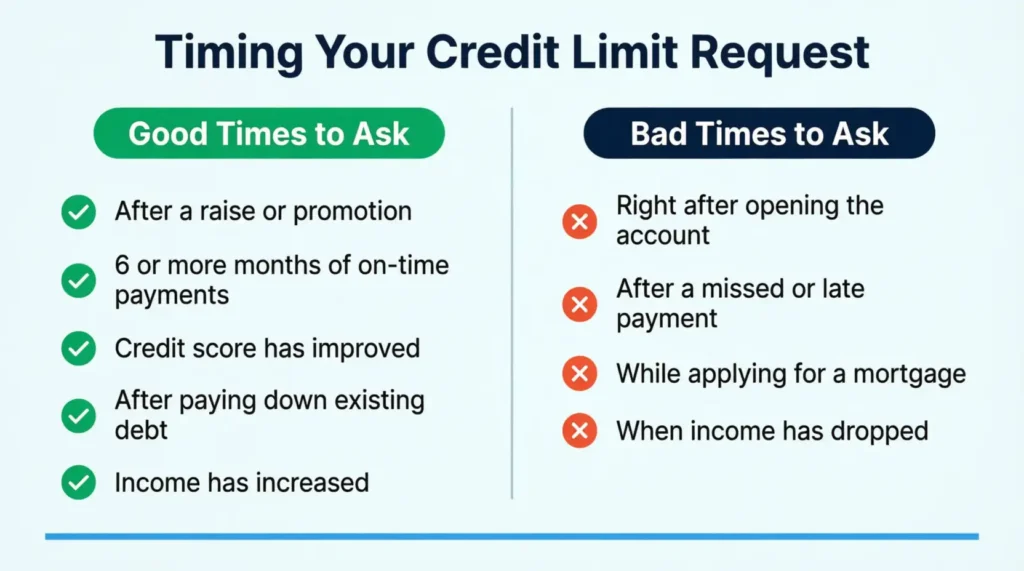

When Is the Best Time to Request a Credit Limit Increase?

Timing matters. Sending a request at the right moment can raise the chance of approval. Sending it at the wrong time can lead to a denial and a wasted hard inquiry.

Good Times to Ask

- After a raise or a new job. A higher income is one of the strongest signals an issuer looks for. It shows the ability to handle more credit.

- After six months of on-time payments. Most banks require an account to be open at least three to six months before they’ll consider an increase. A clean payment record during that window helps.

- When the credit score has improved. A noticeable jump in score, say from fair to good or good to excellent, tells the issuer the borrower is managing debt well.

- After paying down existing debt. A lower debt-to-income ratio makes the request look less risky.

Bad Times to Ask

- Right after opening the account. The issuer just set the limit based on the most recent review. Asking again too soon rarely works.

- After a missed or late payment. This sends a completely incorrect signal. Wait until the account is back on track for at least six months.

- While applying for a mortgage. A hard inquiry from the limit request can ding the score at the worst time. Hold off until the mortgage closes.

- When income has dropped. If earnings have gone down, the issuer may actually lower the limit instead of raising it.

Experian recommends timing the request to moments of clear financial strength: a better score, higher income, or lower debt.

What Information Do You Need to Include in Your Request Letter?

A complete letter gives the issuer everything needed to make a fast decision. Missing details can slow the process or lead to a flat-out denial. Below are the key pieces every request should contain.

Personal Identification

- Full legal name

- Credit card account number (last four digits only for security)

- Phone number and email address

Financial Details

- Current credit limit

- Requested new credit limit

- Current annual income

- Employer name and job title

- Monthly housing payment (rent or mortgage)

Reason for the Request

Clearly state why the increase is needed. Strong reasons include a recent promotion, increased income, improved credit score, or a planned large purchase. Be specific. “More flexibility” is vague. “My annual income increased from $55,000 to $72,000 after a promotion in March” is concrete.

Supporting Documents (Optional but Helpful)

- Recent pay stubs (last two)

- Most recent tax return or W-2

- Bank statements showing consistent savings

- Proof of address

Authorization Statement

Some issuers require a line permitting them to check the credit report. Include a sentence such as: “I authorize [Bank Name] to perform a credit review as needed to process this request.”

📌 Did You Know: The Word templates provided above include a built-in supporting documents checklist so nothing gets forgotten. Just check the boxes next to each item before you send.

How to Write a Credit Card Limit Increase Request Letter (Step-by-Step)

Don’t stare at a blank page. Follow these steps to put together a clear, professional letter that covers all the bases.

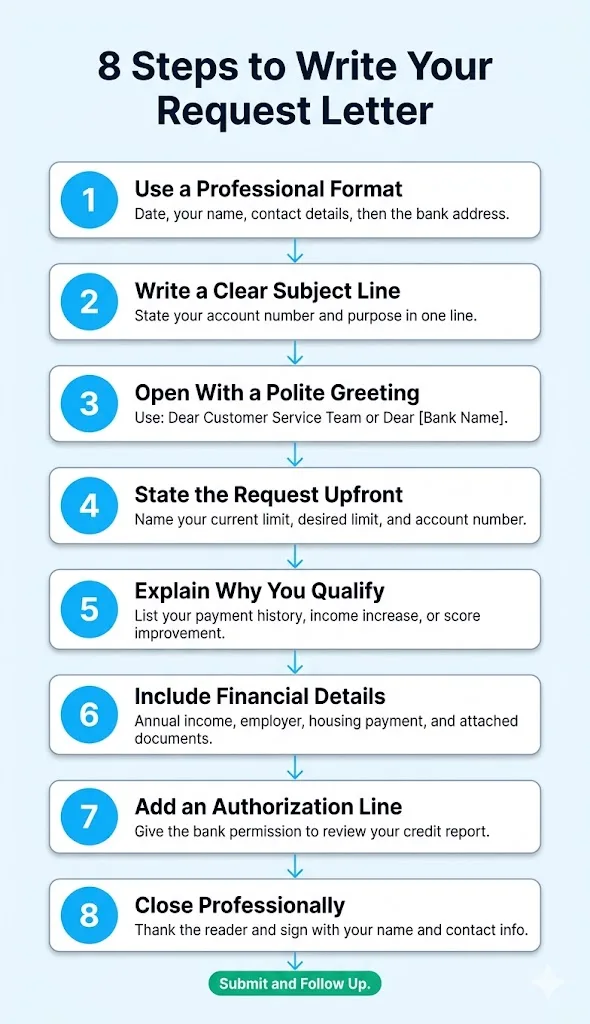

Step 1: Use a Professional Format

Start with the date, your full name, and your contact details at the top. Then add the bank’s name, credit card department, and mailing address. This mirrors standard business letter format and signals that the request is serious.

Step 2: Write a Clear Subject Line

State the purpose right away. Something like:

Subject: Credit Limit Increase Request for Account Ending in 4532

This helps the bank route the letter to the right department without confusion.

Step 3: Open With a Polite Greeting

Use “Dear Customer Service Team” or “Dear [Bank Name] Credit Card Department.” Keep it simple and professional.

Step 4: State the Request in the First Paragraph

Get to the point without delay. Mention the current limit, the desired new limit, and the account’s last four digits. One or two sentences is enough.

Example: “I am writing to request an increase in my credit limit from $5,000 to $8,000 for my account ending in 4532.”

Step 5: Explain Why You Deserve the Increase

This is where the case gets built. Mention one or more of these:

- Length of time as a customer

- On-time payment track record

- Recent income increase

- Low utilization history

- Improved credit score

Be factual. Numbers and dates work better than general claims.

Step 6: Include Supporting Financial Details

List annual income, employer, and any relevant financial strengths. If attaching documents, mention them here: “I have included my two most recent pay stubs for your review.”

Step 7: Add an Authorization Line

Write: “I authorize [Bank Name] to conduct a credit review if needed to process this request.”

Step 8: Close Professionally

Thank the reader for their time. Sign with your full name, date, and preferred contact method.

How to Use the Free Templates Provided

Each template is designed to save time and remove the guesswork. Here’s how to get the most out of them.

Using the Fillable PDF Templates (US Letter or A4)

- Download the PDF that matches your paper size (US Letter for the US, A4 for most other countries).

- Open the file in a PDF reader like Adobe Acrobat Reader (free) or your browser’s built-in viewer.

- Click on each blank field and type your information: name, account number, current limit, requested limit, income, and reason.

- Review every field before saving.

- Print and mail the letter, or save it as a completed PDF to attach to a secure message through the bank’s online portal.

Using the Word Templates (US Letter or A4)

- Download the Word file for your preferred paper size.

- Open it in Microsoft Word, Google Docs, or any compatible word processor.

- Replace all bracketed text (like [Full Name], [Bank Name], [Current Limit]) with your real details.

- Choose one of the three letter styles included:

- Option 1: Short / Direct – Best when the request is simple and the account history is strong. Under 150 words.

- Option 2: Standard / Professional – Best for most situations. Covers the basics with a bit more detail and context.

- Option 3: Detailed / Evidence-Based – Best when income has changed, a promotion happened, or supporting documents are being attached.

- Delete the two options you don’t need.

- Use the built-in follow-up template at the bottom if no response comes within 7 to 14 days.

- Check the supporting documents checklist, print or save it, and send.

Using the Email Templates

- Download the Email Templates PDF.

- Pick one of the five suggested subject lines at the top. For example: “Request to Increase Credit Limit — Account [last 4 digits].”

- Choose from three email body styles:

- Short Template (under 150 words) – Quick and clean. Works well for issuers with a general email inbox.

- Standard Template (200 to 350 words) – More detailed. Good for explaining income changes or long customer history.

- Follow-up Template (one paragraph) – Use this if you haven’t heard back within two weeks.

- Each email comes in plain text and HTML-ready format. Use plain text for most email clients. Use HTML if the bank’s portal supports rich text formatting.

- Replace all placeholder text with real details, paste into the email body, and send.

💡 Pro Tip: Always keep a copy of the sent letter or email. If the bank asks a follow-up question, having the original on hand makes it easy to respond quickly and stay consistent.

Common Mistakes to Avoid When Requesting a Credit Limit Increase

A solid request can fall apart because of small, avoidable errors. Steer clear of these pitfalls.

Asking for Too Much

Requesting double or triple the current limit without a matching jump in income looks unrealistic. A good rule of thumb: ask for a 10% to 25% increase, or match the request to a documented income change. Jennifer, a marketing manager at a mid-size agency, asked for a $15,000 jump on a $6,000 limit with no income proof. She was denied and had a hard inquiry on her report with nothing to show for it.

Not Updating Income First

Many issuers let cardholders update their income through the app or website. If income rose but the bank’s records still show the old number, the request may be judged on outdated data. Always update income before sending the letter.

Submitting Incomplete Information

Leaving out the account number, skipping the reason for the request, or forgetting to include a signature can delay or derail the process. Use the checklist in the Word templates to avoid this.

Requesting Too Often

Banks flag frequent requests. Most issuers allow one request every six months. Sending many letters in a short span can signal financial distress to the issuer.

Ignoring the Issuer’s Preferred Channel

Some banks specifically ask for requests through their app or phone line. Sending a letter when the bank only processes online requests can mean it never reaches the right team. Check the issuer’s website for the recommended method before mailing anything.

Using Vague Language

“I need more credit” doesn’t help. “My annual income increased to $68,000, and I’d like to raise my limit from $4,000 to $6,000 to better manage monthly travel expenses” gives the reviewer something concrete to work with.

What Happens After You Submit Your Request?

The letter is sent. Now what? The timeline and process vary by issuer, but the general flow looks like this.

The Review Process

The bank’s credit department reviews the request. It checks factors like:

- Payment history on the account

- Current credit utilization

- Overall credit report and score

- Income versus existing debt

- Length of relationship with the issuer

Some issuers use automated systems that return an answer in minutes. Others route the request to an underwriter, which can take 7 to 30 days.

Possible Outcomes

Approved: The new limit appears on the account, often within one to two business days. It may take several weeks to show up on credit bureau reports.

Denied: The issuer is required to send an adverse action letter explaining the reasons. Common denial reasons include:

- Account is too new (under six months)

- Recent late payments

- Income is too low relative to the requested amount

- Too many recent credit inquiries

- High existing utilization across all accounts

Counter-offer: Some issuers approve a smaller increase than requested. This is still a win. Accept it, wait six months, and try again.

If There’s No Response

Use the follow-up template included in the Word and email files. Wait 7 to 14 days before reaching out. Reference the original submission date and account number. A polite follow-up shows persistence without being pushy.

Michael, a software developer in Austin, submitted a limit increase request online and heard nothing for three weeks. He sent the follow-up email template, and the bank responded within 48 hours with an approval.

Alternatives to Requesting a Credit Limit Increase

A formal letter isn’t the only path to more available credit. If the timing isn’t right or the request was denied, consider these alternatives.

Request Through the Issuer’s App or Website

Most major banks, including Chase, Capital One, Bank of America, and Discover, let cardholders request increases right from the mobile app or account dashboard. The process often takes less than two minutes and may only trigger a soft inquiry.

Call the Issuer’s Customer Service Line

A phone call allows for a real-time conversation. The agent can ask clarifying questions, and in some cases, approve the increase on the spot. Be ready to share income, employment details, and the desired new limit.

Wait for an Automatic Increase

A January 2026 Federal Reserve study found that roughly 80% of all credit limit increases in the U.S. are bank-initiated, not requested by consumers. About 12% of credit cards receive an automatic increase each year, adding up to approximately $160 billion in new available credit annually. Maintaining on-time payments and low utilization makes an account more likely to be flagged for one of these automatic bumps.

Apply for a New Credit Card

A brand-new card with its own limit adds to the total available credit. This can also lower overall utilization. The trade-off: it adds a hard inquiry and shortens average account age.

Transfer Available Credit Between Cards

Some issuers allow shifting unused credit from one card to another within the same account. This raises the limit on one card without any credit check. Ask the issuer if this option exists.

How a Credit Limit Increase Affects Your Credit Score

A higher limit can help, hurt, or have no effect on a credit score. The outcome depends on how the increase happens and what comes after.

The Positive Side: Lower Utilization

This is the biggest benefit. If spending stays the same but the limit goes up, the utilization ratio drops. Since utilization carries heavy weight in scoring models, even a small drop in the ratio can push a score upward.

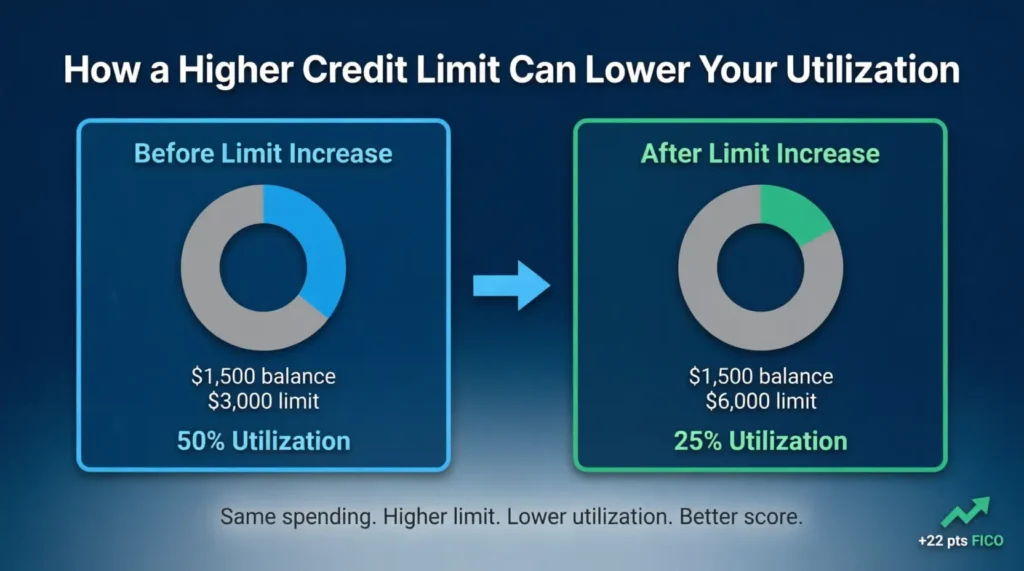

David, a teacher in Ohio, had a $3,000 limit and carried about $1,500 in monthly charges. That’s 50% utilization. After his limit jumped to $6,000, the same spending pattern dropped utilization to 25%. His FICO Score rose by 22 points within two months.

The Negative Side: Hard Inquiries

Some issuers pull a full credit report when processing a limit increase request. Experian reports that a single hard inquiry can lower a FICO Score by up to five points. That dip is temporary, usually fading within 12 months. But many hard inquiries in a short window can stack up.

The Neutral Side: No Change in Behavior

If spending rises to match the new limit, utilization stays the same, and the score won’t budge. Worse, if the higher limit leads to overspending, the score could actually drop.

How Scoring Models Weigh It

Credit utilization falls under the “Amounts Owed” category. That category accounts for about 30% of a FICO Score. The other four factors, payment history (35%), length of credit history (15%), credit mix (10%), and new credit (10%), also play a role. A limit increase touches two of those categories: amounts owed (through utilization) and new credit (through any hard inquiry).

⚠️ Mistake to Avoid: Don’t assume a higher limit will automatically fix a low score. If late payments or collections are dragging the score down, those issues must be addressed first. Utilization improvements only matter when the rest of the credit profile is in decent shape.

Frequently Asked Questions (FAQs)

Can a credit limit increase be denied even with good credit?

Yes. Issuers look at more than just the credit score. High existing debt, a recent increase, or a short account history can all lead to denial, even with a good FICO Score.

Does every credit limit increase request trigger a hard inquiry?

No. Some issuers, like Capital One and Discover, use a soft inquiry that doesn’t affect the credit score. Always ask the issuer which type of pull they use before submitting.

How long does it take to get a response after submitting a request?

It depends on the issuer. Some make an instant decision online. Others take 7 to 30 days, especially if documents need manual review. Check the issuer’s FAQ page for estimated timelines.

How much of an increase should I request?

A 10% to 25% bump over the current limit is a safe starting point. Match the request to any income change. Asking for double the limit without proof of higher earnings often leads to denial.

Will a higher credit limit help with a mortgage application?

It can. A higher limit lowers credit utilization, which can raise the credit score. But request the increase well before applying for the mortgage. A hard inquiry too close to the application date could hurt more than it helps.

Can I request a credit limit increase by email instead of a letter?

Some issuers accept requests through secure email or their online message center. The email templates above have ready-to-use formats. They also include suggested subject lines for this purpose.

How often can I ask for a credit limit increase?

Most banks allow one request every six months. Asking more often than that can signal financial stress and may result in automatic denials.

Does a denied request hurt the credit score?

The denial itself doesn’t affect the score. But if the issuer ran a hard inquiry during the review, it can lower the score by a few points, regardless of what happens next.

Bottom Line

Getting a higher credit line starts with a clear, well-organized request. The right letter covers personal details, income proof, and a strong reason for the increase. Timing the request after a raise, a score improvement, or six months of clean payment history gives it the best shot at approval.

Based on the research above, the most effective approach is to use one of the provided templates, customize it with real financial details, and submit it through the issuer’s preferred channel. A credit card limit increase request letter doesn’t need to be complicated. It just needs to be complete.

If you know someone who’s been wanting a higher credit line but doesn’t know where to start, share this guide. These free templates could save them hours of guesswork.