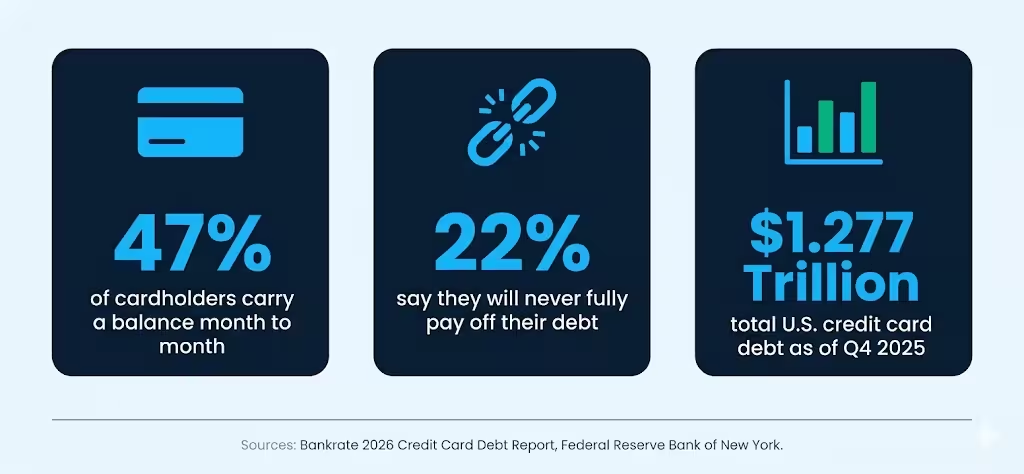

Drowning in credit card debt with no clear way out? That feeling is more common than you might think. Bankrate’s 2026 Credit Card Debt Report found that 47% of American cardholders carry a balance from month to month, and 22% say they don’t believe they’ll ever pay it off. Writing a credit card debt forgiveness letter is one of the most direct ways to ask your creditor for real relief.

A formal forgiveness request is a written letter you send to your creditor asking them to cancel or reduce what you owe. It puts your hardship on the record and opens the door to a settlement.

Below, you’ll find free, ready-to-use templates, a step-by-step guide for filling them out, and expert tips to help your request actually succeed.

Download Your Free Credit Card Debt Forgiveness Letter Templates

2 ready-to-use templates are available to make your life easier. Each one has every section you need to send a professional forgiveness request to your creditor.

Pick the format that works best for you:

Disclaimer: The Templates & Printables on this site are provided for informational and personal tracking purposes only. This is not financial, legal, tax, or credit advice. While reasonable efforts are made to ensure accuracy, Credit Card Wind makes no warranties as to the completeness, reliability, or accuracy of the calculations generated by these Templates & Printables. Users are responsible for independently verifying all data and calculations. Terms, conditions, rates, regulations, and legal requirements vary by institution, jurisdiction, and individual circumstances.

Always refer to your official statements, account agreements, and applicable laws, and consult a qualified professional before making any financial, legal, or other important decisions. By using these Templates & Printables, you acknowledge that Credit Card Wind and its owner shall not be liable for any damages, losses, or financial consequences arising from the use or misuse of these Templates & Printables.

This universal disclaimer applies to all templates and printables provided by Credit Card Wind (https://creditcardwind.com), created by Robert Williams (Owner at Credit Card Wind).

© Credit Card Wind. All rights reserved.

These templates and printables may be downloaded and used for personal, non-commercial purposes only. Redistribution, resale, or modification for commercial use without permission is strictly prohibited.

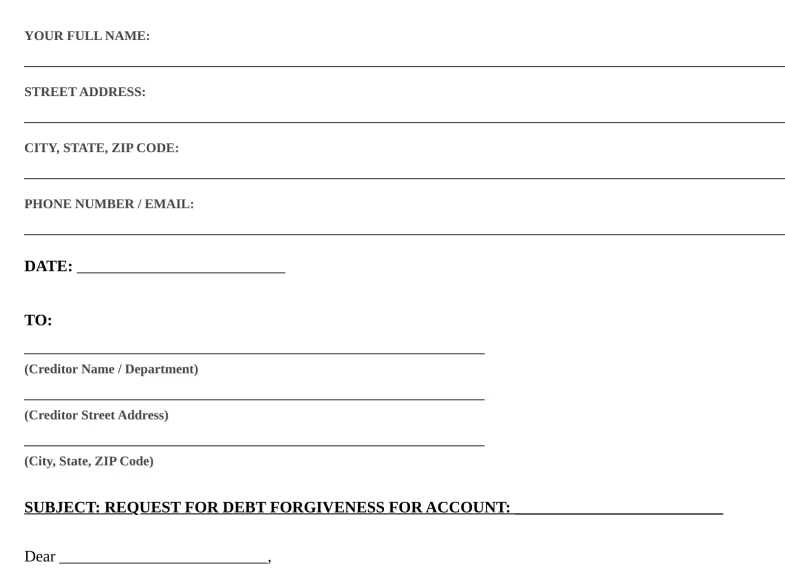

What Is a Credit Card Debt Forgiveness Letter?

A debt forgiveness letter is a formal written request you send to a creditor. In this letter, you ask them to forgive, cancel, or reduce your outstanding credit card balance. It’s different from a phone call because it creates a paper trail. That paper trail protects you later.

This type of letter is sometimes called a hardship letter, a debt settlement letter, or a debt relief request. The names change, but the goal stays the same. You explain why you can’t pay what you owe. Then you propose a fair solution.

There are actually two sides to this term:

- The letter you send – This is your request to the creditor. You explain your hardship and propose a settlement. The templates on this page are designed for this purpose.

- The letter you receive – After a creditor agrees to forgive part of your debt, they send you a confirmation letter. This letter states the forgiven amount and confirms the account is resolved.

Both matter. But the starting point is always the letter you write and send.

Bankrate’s 2026 Credit Card Debt Report found that 47% of American cardholders carry a balance. Among those with debt, 22% say they don’t believe they’ll ever pay it off. A well-written forgiveness request can be the first step toward breaking that cycle.

The scope of the problem is massive. Federal Reserve Bank of New York data shows total U.S. credit card debt hit $1.277 trillion by the end of Q4 2025. That’s the highest number since tracking began in 1999. With average APRs above 20%, even small balances grow fast.

💡 Pro Tip: A forgiveness request works best when it’s sent in writing, not just discussed over the phone. Written letters create a documented record that protects both sides if the creditor later claims they never agreed to anything.

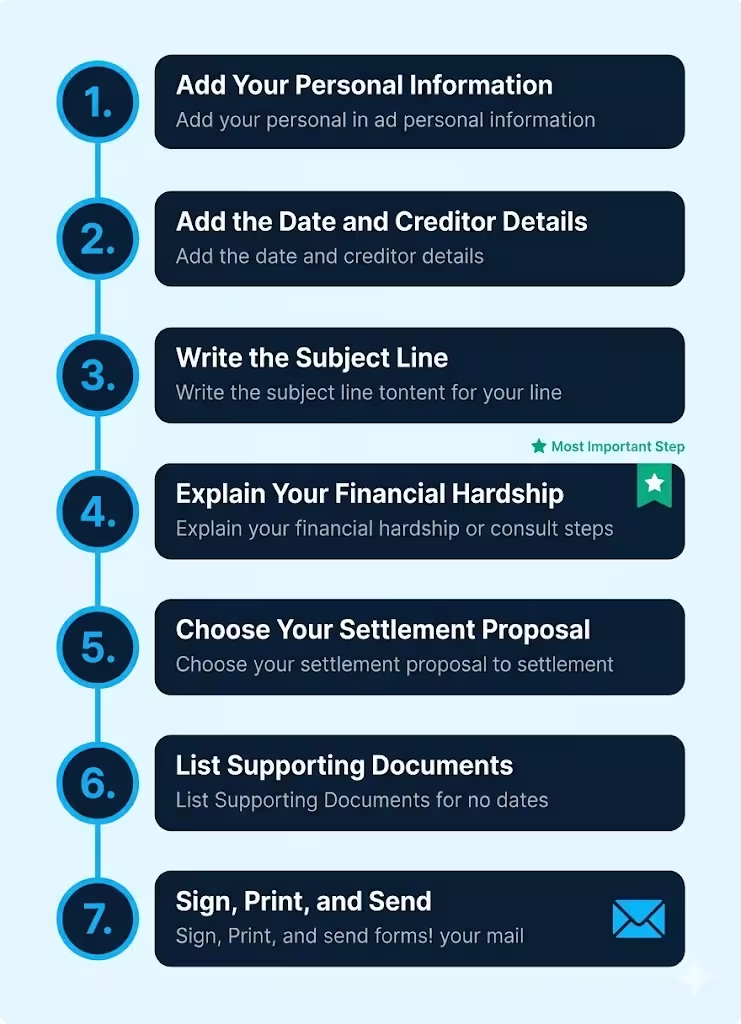

How to Use the Debt Forgiveness Letter Template (Step by Step)

The template has every section you need. Here’s exactly how to fill it out.

Step 1: Add Your Personal Information

At the top of the letter, fill in:

- Your full legal name

- Your street address, city, state, and ZIP code

- Your phone number

- Your email address

Use the same name and address that appear on your credit card statements. This helps the creditor match your letter to your account in a timely manner.

Step 2: Add the Date and Creditor’s Details

Write today’s date below your contact info. Then add the creditor’s details:

- The creditor’s name (the company, not a person)

- The correct department (Collections Department or Hardship Department)

- The creditor’s mailing address

You can find the creditor’s mailing address on your monthly statement or on the back of your credit card.

Step 3: Write the Subject Line

The template includes a subject line that reads: “Request for Debt Forgiveness for Account Number: [Your Credit Card Account Number].”

Fill in your actual account number here. This ensures your letter goes to the right file. Double-check the number before you send it.

Step 4: Explain Your Financial Hardship

This is the most important section. The template has a placeholder where you describe what happened. Be honest and specific. Here are some examples:

- “I was laid off from my position at [Company Name] on [Date] and have been looking for new work since then.”

- “A serious medical emergency in [Month/Year] left me with $15,000 in hospital bills and no income for three months.”

- “My household income dropped by 40% after my spouse passed away in [Month/Year].”

Don’t be vague. Numbers, dates, and real details make your case stronger. Creditors receive hundreds of these letters. Specific details stand out.

Step 5: Choose Your Settlement Proposal

The template gives you two options:

- Option A (Lump-Sum Settlement): Offer a single payment to close the debt. Example: “I can offer a one-time payment of $2,500 to settle my $6,000 balance in full.”

- Option B (Structured Forgiveness): Ask the creditor to forgive a part and let you pay the rest over time. Example: “I request that you forgive $3,000 of my $6,000 balance. I’ll pay the remaining $3,000 in monthly payments of $250.”

Pick the option that fits your budget. Delete the option you don’t use before sending.

Step 6: List Your Supporting Documents (Optional)

The template has a section to list any documents you attach. Strong supporting evidence includes:

- A layoff or termination letter from your employer

- Medical bills or a doctor’s statement

- Proof of reduced income (pay stubs or bank statements)

- A death certificate (if applicable)

Remove any sensitive info like Social Security numbers before attaching these documents.

Step 7: Sign, Print, and Send

Type your full name at the bottom. Print the letter. Sign it by hand above your typed name. Send it by certified mail with return receipt requested. This gives you proof that the creditor received your letter.

Keep a copy of everything: the letter, the attachments, and the certified mail receipt.

⚠️ Mistake to Avoid: Never send your forgiveness request by regular mail without tracking. If the creditor claims they never got it, you’ll have no proof. Always use certified mail with a return receipt so you have a documented delivery record.

When Should You Send a Debt Forgiveness Request?

Timing matters. Not every situation calls for a forgiveness letter. Here are the best times to send one:

You’ve experienced a major financial hardship. This includes job loss, a medical emergency, divorce, disability, or the death of a spouse. Creditors are more likely to negotiate when there’s a clear reason you can’t pay.

You’ve already fallen behind on payments. If you’re 90 or more days past due, the creditor knows collecting the full amount is getting harder. At this point, they may prefer a partial payment over nothing at all.

Your account has been sent to collections. Once a debt goes to a collection agency, the original creditor has already written off the balance. Collectors often buy debt for pennies on the dollar. That means they may accept a much smaller settlement.

You’re considering bankruptcy. If bankruptcy is on the table, creditors take notice. In a Chapter 7 case, they might receive nothing at all. A settlement looks much more attractive compared to zero recovery.

Situations Where a Different Approach May Work Better

- If you’re only slightly behind, call your card issuer first and ask about their hardship program.

- If your debt is small (under $500), a phone call might resolve things faster than a letter.

- If you earn well but have high balances, consider a balance transfer card or a debt management plan. It might be a smarter first move.

What to Say (and What to Avoid) in Your Letter

The words you choose can make or break your request. Here’s a quick guide.

Phrases That Help Your Case

- “I want to take responsibility for this debt and find a realistic solution.”

- “Due to [specific hardship], my income has dropped significantly.”

- “I am prepared to offer $[amount] as a lump-sum settlement within [timeframe].”

- “I value our long-standing relationship as a customer of [number] years.”

- “Please contact me at your earliest convenience to discuss options.”

Phrases That Hurt Your Case

- “I’ll pay whatever I have to.” – This signals you can afford more than you’re offering. It kills your leverage.

- “I don’t think I owe this debt.” – Unless the debt is fraudulent, disputing it during settlement talks stalls the process.

- “I can start paying you something each month.” – Vague offers of small monthly payments don’t motivate creditors. They want specific proposals.

- “My lawyer told me to write this.” – Mentioning legal action too early can make the creditor defensive and less willing to negotiate.

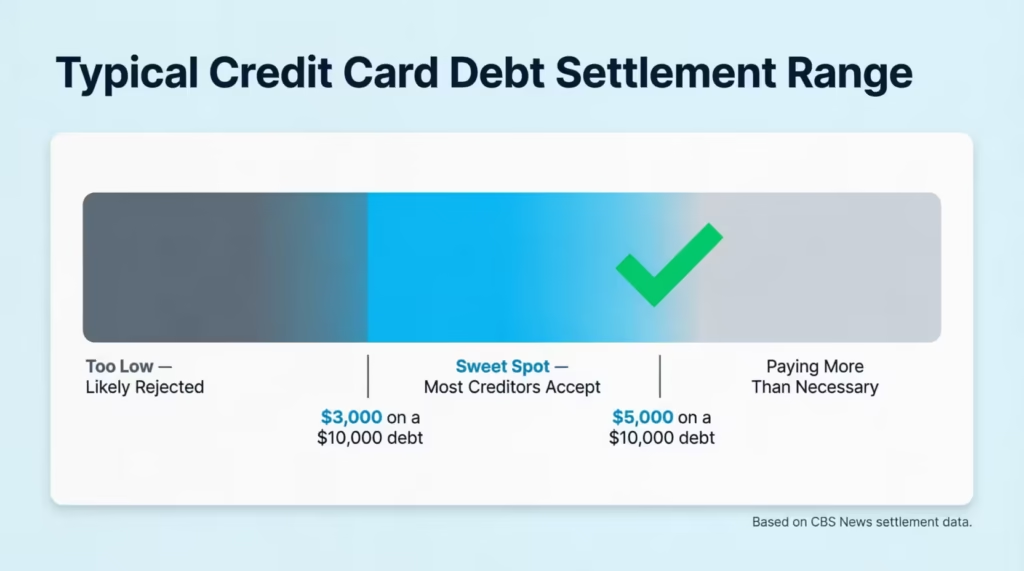

📌 Did You Know: Most successful debt settlements fall between 30% and 50% of the original balance, according to CBS News. So if you owe $10,000, an offer between $3,000 and $5,000 is a reasonable starting point for most creditors.

How Creditors Decide Whether to Forgive Your Debt

Creditors don’t forgive debt out of kindness. It’s a business decision. Here’s what they weigh:

Your payment history. Were you a reliable customer before the hardship started? A long track record of on-time payments works in your favor.

How far behind are you? Accounts that are 120 or more days past due are more likely to be settled. At that point, the creditor has two choices. They can deal with rising collection costs or sell the debt for less than it’s worth.

Your documented hardship. A letter backed by medical bills, a layoff notice, or proof of income loss carries far more weight than a vague claim of “hard times.”

The amount you’re offering. Offering too little (say, 10% of the balance) won’t get a response. Offering too much leaves money on the table. The sweet spot is typically 30% to 50% for most credit card debts.

Whether you mention bankruptcy. This isn’t a threat. It’s a fact. If you file Chapter 7, the creditor might get nothing. Many creditors would rather settle for 40 cents on the dollar than risk zero recovery.

The age of the debt. Older debts, especially those close to the statute of limitations in your state, are more likely to be settled. The creditor knows time is running out on their ability to collect.

What Happens After You Send the Letter?

Once your letter reaches the creditor, here’s the typical process:

- The creditor reviews your request. This can take 2 to 4 weeks. Larger banks may take longer.

- They may counter your offer. Don’t be surprised if the first response asks for more than you proposed. This is a normal negotiation.

- You negotiate back and forth. Expect one to three rounds before reaching a final number.

- You reach an agreement. Once both sides agree, the creditor sends a written settlement letter confirming the terms.

- You make the payment. Pay only after you have the agreement in writing. Never pay based on a verbal promise alone.

- The creditor updates your account. Your credit report will show the debt as “settled” or “settled for less than the full amount.”

Get Everything in Writing

This point deserves repeating. Do not send any money until you have a written agreement that states:

- The exact settlement amount

- The payment deadline

- That the creditor considers the debt resolved after payment

- How the account will be reported to the credit bureaus

A written agreement protects you from future collection attempts on the same debt. Without it, you have no leverage.

How Debt Forgiveness Affects Your Credit Score

Let’s be honest. Debt forgiveness does hurt your credit. But it may still be the smartest move.

The “settled” notation. When a debt is settled for less than the full amount, the credit bureaus mark it as “settled.” This notation stays on your report for up to seven years from the date of settlement. Experian notes that this status signals to future lenders that the original balance wasn’t fully repaid.

The score dropped. The exact drop depends on your starting score and overall credit profile. Someone with a 750 score will lose more points than someone already at 550. In general, a settlement can lower a score by 50 to 150 points.

The recovery. Credit scores can recover over time. After settling, the path forward includes:

- Paying all other bills on time every month

- Keeping credit card balances low on remaining accounts

- Avoiding new hard inquiries for 6 to 12 months

- Checking your credit report for errors regularly

The trade-off. If you’re already 90 or more days late or in collections, your credit has already taken a hit. Settling the debt stops the damage and gives you a clear starting point for rebuilding.

💡 Pro Tip: After any settlement, request your credit report from all three major bureaus. Make sure the settled account is reported correctly. Errors happen more than you’d expect, and disputing them early prevents long-term damage to your score.

Tax Rules for Forgiven Credit Card Debt

Here’s something many people don’t expect. Forgiven debt can be taxable income.

The IRS rule. When a creditor forgives $600 or more of your debt, they report it to the IRS using Form 1099-C. The forgiven amount is treated as income on your tax return. The IRS explains on Topic No. 431 that canceled debt is generally taxable unless a specific exception applies.

How much could you owe? That depends on your tax bracket. If your creditor forgives $5,000 and your effective tax rate is 22%, you could owe roughly $1,100 in extra taxes that year.

The insolvency exception. There’s good news for people who are truly struggling. If your total debts exceed your total assets at the time of forgiveness, the IRS considers you “insolvent.” In that case, you can exclude some or all of the forgiven amount from your taxable income. You’ll need to file Form 982 with your tax return to claim this exclusion.

Other exceptions include:

- Debt discharged in a Title 11 bankruptcy case

- Cancellation of qualified principal residence debt (before January 1, 2026)

- Certain student loan discharges are approved by the IRS

The bottom line on taxes: factor this into your settlement math. If a creditor agrees to forgive $8,000, set aside money for the potential tax bill. Talk to a tax professional before filing.

Alternatives to a Debt Forgiveness Request

A forgiveness letter isn’t the only path forward. Depending on your situation, one of these options might fit better.

Credit Card Hardship Programs

Many big issuers, like Chase, Citi, Bank of America, and American Express, provide hardship programs. These programs can lower your interest rate. They might also waive late fees or cut your smallest payment for a certain time. You usually need to call and request enrollment. The benefit: these programs typically don’t damage your credit the way a settlement does.

Balance Transfer Cards

If your credit score is still in decent shape, a 0% APR balance transfer card can give you 12 to 21 months of interest-free payments. This won’t reduce what you owe, but it stops interest from piling up while you pay down the principal.

Nonprofit Credit Counseling

A nonprofit credit counseling agency can negotiate a debt management plan (DMP) with your creditors. DMPs often lower your interest rates and combine multiple payments into one monthly amount. The National Foundation for Credit Counseling can help you find a reputable, accredited agency in your area.

Debt Consolidation Loans

A personal loan at a lower interest rate can roll many credit card balances into one fixed monthly payment. This simplifies your finances and can save real money on interest charges over time.

Bankruptcy (Last Resort)

Chapter 7 bankruptcy can eliminate most unsecured debts, including credit card balances. Chapter 13 creates a court-supervised repayment plan instead. Both options carry serious long-term credit consequences (7 to 10 years on your report). But they offer legal protection and a true fresh start when all other options have failed.

Frequently Asked Questions

Can you write a debt forgiveness letter yourself without hiring a lawyer?

Yes. A forgiveness request is a straightforward letter that anyone can write. The free templates on this page include every section you need. No lawyer is required, though consulting one is always an option for complex situations.

How long does it take for a creditor to respond to a forgiveness request?

Most creditors respond within 2 to 4 weeks. Some larger banks may take up to 6 weeks. If you don’t hear back, follow up with a phone call to the hardship or collections department.

Will my creditor always agree to forgive part of my debt?

No. Creditors are not required to accept any settlement offer. Success depends on your hardship documentation, how far behind you are, and the amount you propose. Accounts that are 90 or more days past due tend to have the highest settlement rates.

Does settling a debt for less remove it from my credit report?

No. A settled debt stays on your credit report for up to 7 years. It will show as “settled” or “settled for less than the full balance,” which is better than an unpaid collection but not as strong as “paid in full.”

Do I have to pay taxes on forgiven credit card debt?

If a creditor forgives $600 or more, they report it to the IRS on Form 1099-C. The forgiven amount is treated as taxable income unless you qualify for an exception, like insolvency or bankruptcy discharge.

Should I stop making payments before sending a forgiveness letter?

Stopping payments can increase your leverage in negotiations, but it also damages your credit score and may trigger late fees and collections. Weigh the trade-offs carefully. Some advisors recommend continuing minimum payments until a settlement is finalized.

What documents should I include with my forgiveness request?

Strong supporting documents include a layoff or termination letter, medical bills, proof of income reduction (pay stubs or bank statements), and any other evidence that confirms your financial hardship.

Can I send a debt forgiveness letter for a debt that’s already in collections?

Yes. You can send a settlement offer directly to the collection agency that now owns the debt. Collectors often buy debt at a steep discount, so they may accept a lower settlement amount than the original creditor would.

Bottom Line

Dealing with credit card debt that’s spiraling out of control is stressful. But a well-crafted forgiveness request can open a real path to relief. The key steps are straightforward: download the free template, fill it out with honest details about your hardship, choose a settlement option that fits your budget, and send it by certified mail.

Based on current settlement data, most creditors accept offers between 30% and 50% of the outstanding balance when a genuine hardship exists. The process takes patience, but saving thousands of dollars is worth the effort.

The most effective approach is to combine a strong written request with solid supporting documents and a clear dollar amount. That combination shows creditors you’re serious and prepared, not just hoping for a favor.

If you know someone who’s struggling with credit card payments right now, share this guide with them. A single well-written letter could save them thousands and give them a real chance to start fresh.