Closing a credit card sounds easy. But if you rely on a phone call alone, you could end up with surprise annual fees, unresolved charges, or an account that was never officially closed.

According to Experian’s State of Credit report, the average American holds nearly 4 credit cards, which means most people will need to close at least one at some point. Sending a proper credit card cancellation request letter is the safest, most reliable way to protect yourself.

A written request gives the bank formal notice, creates a legal paper trail, and ensures you receive documented proof that the account is closed.

This guide has free templates you can download. It also offers step-by-step instructions and helpful tips to help you close your account smoothly, with no surprises.

Download Your Free Credit Card Cancellation Request Letter Templates

Three ready-to-use templates are waiting for you below. Each one is pre-written with all the key sections your bank needs to process the closure.

Pick the format and paper size that works best for you:

- Download US Letter PDF Template – Perfect for standard 8.5″ x 11″ printing in the United States

- Download A4 PDF Template – Ideal for A4-sized paper or international use

- Download A4 Word Template – Fully editable in Microsoft Word, so you can customize it to your situation

Disclaimer: The Templates & Printables on this site are provided for informational and personal tracking purposes only. This is not financial, legal, tax, or credit advice. While reasonable efforts are made to ensure accuracy, Credit Card Wind makes no warranties as to the completeness, reliability, or accuracy of the calculations generated by these Templates & Printables. Users are responsible for independently verifying all data and calculations. Terms, conditions, rates, regulations, and legal requirements vary by institution, jurisdiction, and individual circumstances.

Always refer to your official statements, account agreements, and applicable laws, and consult a qualified professional before making any financial, legal, or other important decisions. By using these Templates & Printables, you acknowledge that Credit Card Wind and its owner shall not be liable for any damages, losses, or financial consequences arising from the use or misuse of these Templates & Printables.

This universal disclaimer applies to all templates and printables provided by Credit Card Wind (https://creditcardwind.com), created by Robert Williams (Owner at Credit Card Wind).

© Credit Card Wind. All rights reserved.

These templates and printables may be downloaded and used for personal, non-commercial purposes only. Redistribution, resale, or modification for commercial use without permission is strictly prohibited.

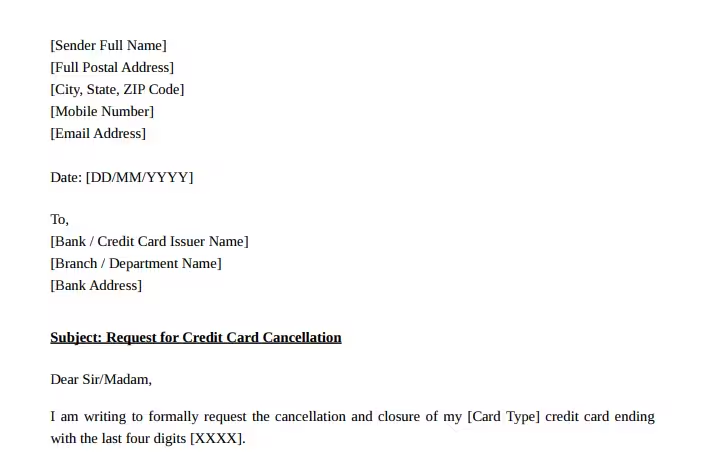

What Is a Credit Card Cancellation Letter?

A credit card cancellation letter is a formal written document sent to your bank or card issuer. It requests the immediate closure of your credit card account and asks for written confirmation once the process is complete.

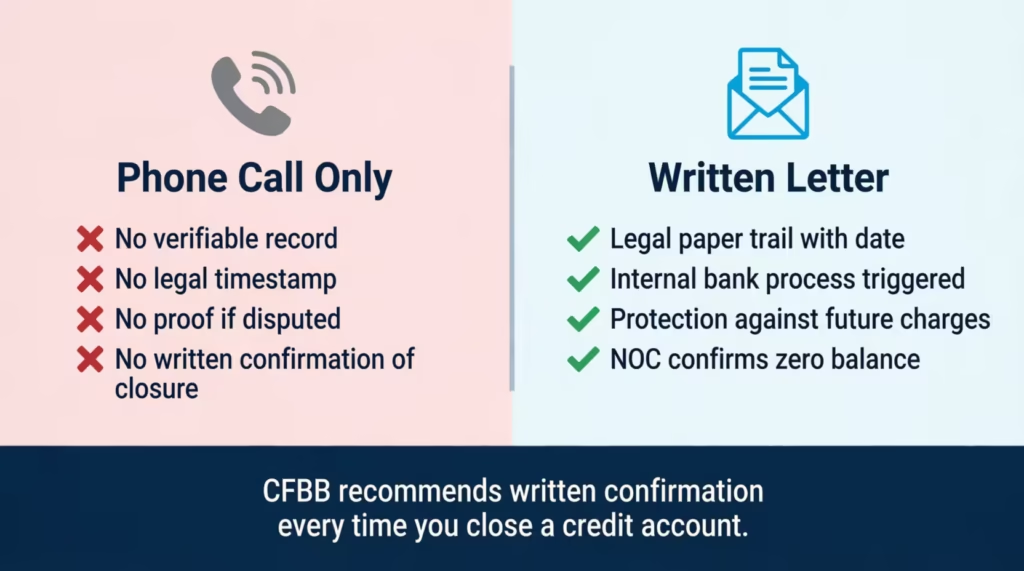

This type of letter serves as official documentation. It’s different from calling customer service or chatting with an agent online. A phone conversation leaves no verifiable record. A written letter does.

Most U.S. banks and credit unions accept these letters by mail, fax, in-person delivery at a branch, or secure upload through an online banking portal.

Data from Experian’s State of Credit report shows that the average American has close to 4 credit card accounts. Given that number, knowing how to close an account properly is a financial skill worth developing.

Your card closure letter should cover these key sections:

- Your full name, address, and contact details

- Your credit card type and the last four digits of the card number

- A clear statement confirming that all outstanding dues are paid

- A formal request for cancellation and account closure

- A request for a written confirmation or NOC (No Objection Certificate)

- Your signature, printed name, and the date

Why a Written Letter Is Better Than a Phone Call

Most people call their bank to close a card. It’s quick, it’s convenient, and it feels like enough. But a phone call has one significant problem: there is no paper trail.

What happens if the bank doesn’t process the request? Or if you get charged an annual fee two months later? Without a written record, you have no proof that the cancellation was ever requested.

Here’s what a formal written closure request gives you that a phone call never can:

1. Legal proof of the request. A signed, dated letter is timestamped evidence. If a dispute ever comes up, you can point to the exact date you made the request.

2. A formal internal process trigger. Banks are more likely to process a written request promptly. A physical or uploaded letter creates an internal ticket that gets tracked through their system.

3. Protection Against Future Charges. A written request on file makes it harder for the bank to say they never got the cancellation.

4. An NOC (No Objection Certificate). This is the gold standard of account closure proof. The NOC states the card is cancelled, the account is fully closed, and the balance is zero.

The Consumer Financial Protection Bureau recommends getting written confirmation any time you close a credit account. It’s a straightforward step that protects your financial record long after the closure.

⚠️ Mistake to Avoid: Never send a closure request while you still have a balance on the card. Banks will reject the closure until all dues are fully paid, including pending EMIs and recurring charges. Clear the balance first, then write the letter.

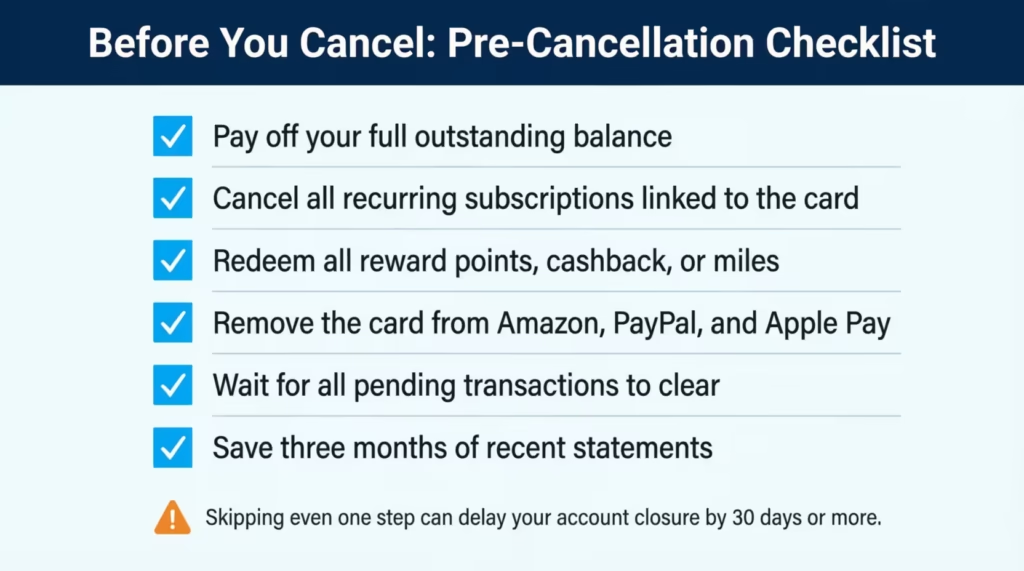

Before You Write: A Quick Pre-Cancellation Checklist

A well-written letter won’t do much if your account isn’t ready to close. Run through this checklist before you sit down to fill out the template.

- [ ] Pay off your full outstanding balance

- [ ] Cancel all recurring subscriptions and auto-payments linked to the card

- [ ] Redeem any unused reward points, cashback, or travel miles

- [ ] Remove the card from online accounts like Amazon, PayPal, and Apple Pay

- [ ] Wait for all pending transactions to post and fully clear

- [ ] Download or save at least three months of recent statements for your records

Skipping even one of these steps can stall the entire process. Take Michael, a project coordinator from Denver, for example. He submitted his closure request before noticing that a $14.99 streaming subscription was still billed to his card. The charge created a new balance, and his bank put the closure on hold for an additional 30 days.

A five-minute review before you write can save you weeks of delay.

What to Include in Your Credit Card Cancellation Letter

Getting the content right matters. Here is a breakdown of every section the letter should include.

1. Your Full Name and Contact Information

Start with your full legal name, home address, city, state, and ZIP code. Include your phone number and email address so the bank can reach you if they need to verify anything.

2. The Date

Write the date clearly at the top of the letter. Use MM/DD/YYYY format for the U.S. Letter version. This date is your official timestamp for when the request was made.

3. Bank and Branch Information

Add the bank’s full name, the specific branch or department name, and the bank’s complete mailing address. You’ll find this on the back of your card, in your monthly statement, or on the bank’s official website.

4. Your Card Identification Details

Include the type of card (Gold, Platinum, Rewards, Cashback, etc.) and the last four digits of the card number. Never write the full 16-digit card number in any written letter. The last four digits are enough to identify the account securely.

5. Confirmation of Zero Balance

This section is one of the most critical parts of the letter. State clearly that all outstanding dues have been paid in full. Confirm that there are no pending EMIs (Equated Monthly Installments), recurring charges, or unauthorized transactions on the account as of the date of the letter.

This statement protects you. If the bank ever claims a balance was present, your written confirmation creates a counter-record.

6. Your Formal Closure Request

State clearly and directly that you are requesting the immediate cancellation and closure of the credit card account. Use professional, firm language. Both templates above include this section already written in clear, formal language.

7. Request for an NOC or Written Confirmation

Ask the bank to send you a written confirmation letter or a No Objection Certificate (NOC) once the closure is complete. This document should confirm three specific things:

- The card has been cancelled

- The account is fully closed

- The balance on the account is zero

💡 Pro Tip: Keep your NOC in a safe place, whether physical or digital. If you apply for a mortgage, auto loan, or new credit card later, lenders may ask for proof that your old accounts were closed correctly. An NOC saves you time and paperwork later.

8. Physical Card Disposal Statement

Let the bank know what you did with the physical card. The two most common options are:

- You’ve already destroyed it by cutting through the magnetic stripe and chip

- You will return it to the branch as per the bank’s policy

Check your bank’s specific guidelines before destroying the card. Some institutions prefer you return it in person.

9. Your Signature, Printed Name, and Card Reference

Sign the letter by hand if submitting a physical copy. Print your full name clearly below the signature. Include your credit card number with only the last four digits visible, formatted as XXXX-XXXX-XXXX-1234. Add an account number if the bank requires one.

How to Fill Out the Template (Step-by-Step)

Got your template downloaded? Here’s how to complete it from start to finish.

Step 1: Enter your personal information.

Fill in your full name, mailing address, phone number, and email at the top of the letter. Double-check the spelling of your name to match your bank’s records exactly.

Step 2: Write the date.

Use the date you plan to submit the letter, not the date you started filling it out. Use MM/DD/YYYY for the U.S. Letter PDF or DD/MM/YYYY for the A4 version.

Step 3: Add the bank’s details.

Enter the bank’s full name, the branch or department name, and the bank’s complete mailing address. If submitting in person, this section still serves as part of your documented record.

Step 4: Identify your card.

Write the card type (such as Gold, Platinum, or Cashback) and the last four digits of your card number in the fields provided.

Step 5: Review the balance confirmation statement.

Both templates contain a pre-written statement confirming your balance is cleared. Read it carefully before signing. If you still have a balance on the account, do not submit the letter yet.

Step 6: Choose the physical card disposal option.

In the Word template, you can edit this line directly. In the PDF version, cross out whichever option doesn’t apply. The two choices are “destroyed” or “will be returned to the branch.”

Step 7: Sign and fill in your details.

Hand-sign the letter. Print your full name clearly below the signature. Write your credit card number in the XXXX-XXXX-XXXX-1234 format and include your account number if the bank requires it.

Step 8: Make a copy and save it.

Before sending anything, make a physical photocopy or save a scanned digital copy. This copy is your primary proof of request if any dispute comes up later. Store it somewhere easy to access.

How to Submit Your Letter to the Bank

Once the letter is complete, you have four solid options for delivery.

Option 1: In Person at the Branch (Most Recommended)

Walk into your local bank branch and hand the letter directly to a customer service representative. Ask for a stamped acknowledgment receipt on the spot. This is the most reliable method because you have immediate proof of delivery.

Option 2: USPS Certified Mail.

Send the letter by USPS Certified Mail. You’ll get a tracking number and a signed delivery receipt. This receipt is legal proof of submission. This is the best remote option if you can’t visit the branch.

Option 3: Secure Online Portal

Many banks now have a secure messaging system inside their online banking app or web portal. You can upload a signed PDF directly through the portal. Always screenshot or save the confirmation message you receive after uploading.

Option 4: Email to the Bank’s Official Address.

Some banks accept email submissions, but only to their verified, official email addresses. Scan your signed letter as a PDF and attach it. Never send sensitive documents to unverified contacts.

📌 Did You Know: USPS Certified Mail (Form 3800) provides a signed delivery receipt that can serve as legal evidence of submission. If your bank ever disputes receiving your request, a signed receipt is very difficult to argue against.

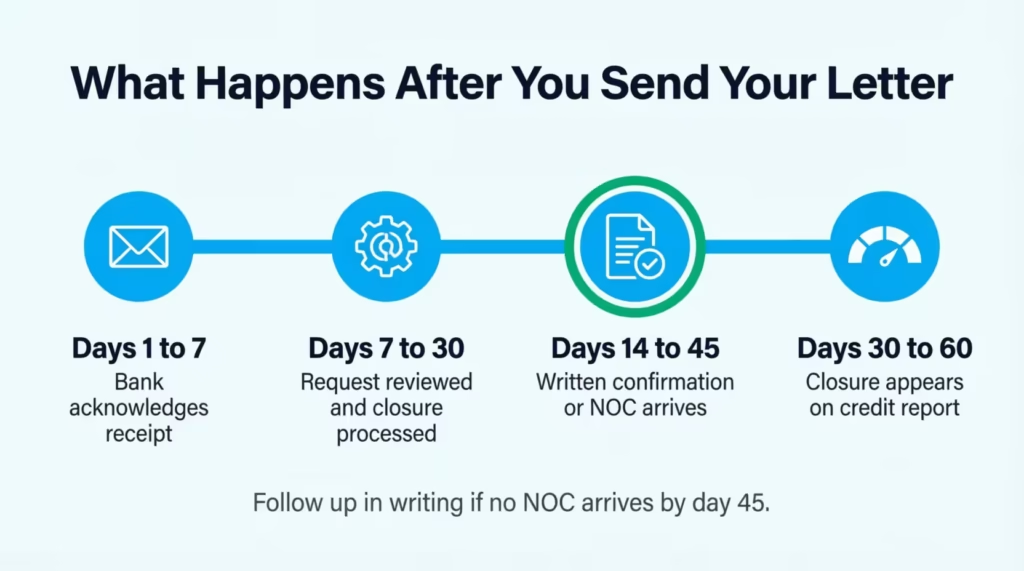

What to Expect After You Send the Letter

Here is a realistic timeline of what happens after your written request goes in.

Days 1 to 7: Acknowledgment.

Most banks confirm they received your closure request within 5 to 7 business days. If you submitted in person and got a stamped receipt, you already have this confirmation.

Days 7 to 30: Processing.

The bank reviews the request, verifies your balance status, and begins the formal closure process. This process requires a duration of 7 to 30 days, based on the bank’s internal procedures.

Days 14 to 45: Written Confirmation or NOC.

You should receive a written confirmation letter or NOC within 30 to 45 days. If nothing arrives by day 45, send a follow-up letter referencing your original request date.

Days 30 to 60: Credit Report Update.

Once the account is officially closed, the update typically appears on your credit report within 30 to 60 days. You can check your report for free at AnnualCreditReport.com, which is federally authorized to provide one free report per bureau per year.

⚠️ Mistake to Avoid: Don’t assume the card is cancelled just because you sent the letter. Follow up if you haven’t received written confirmation within 45 days. Some closure requests fall through administrative gaps, allowing the account to remain open.

Will Closing a Credit Card Affect Your Credit Score?

Yes, it can. But for most people, the impact is manageable when you understand what’s actually happening.

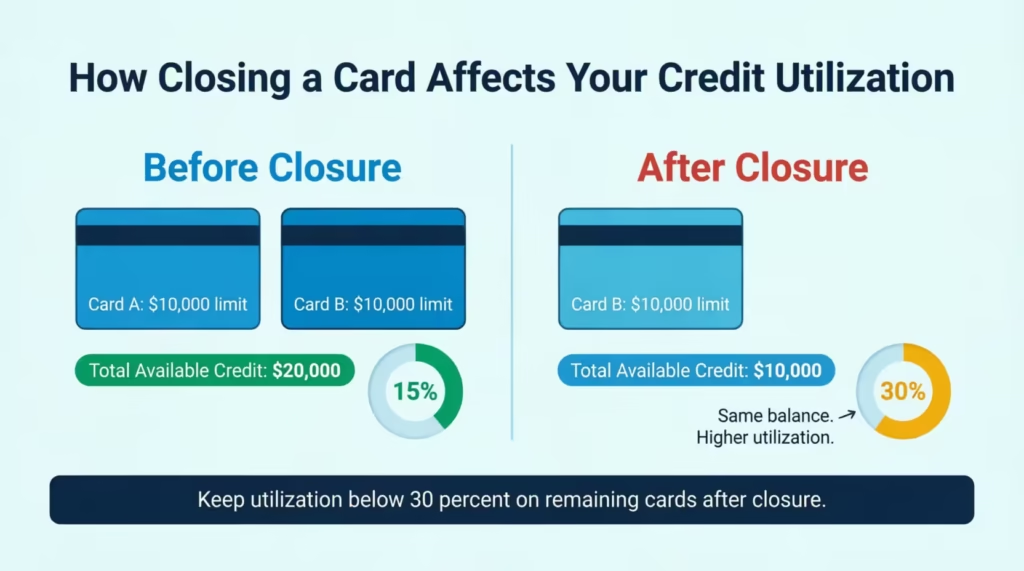

Credit Utilization Ratio: This is the biggest factor to watch. When you close a card, you lose that card’s available credit limit. Your total available credit drops. If you carry balances on other cards, your utilization percentage goes up, and that can lower your score.

Here’s a simple example. Say you have $20,000 in total available credit across two cards. You close one card with a $10,000 limit. Your available credit drops to $10,000. Any balances you still carry now represent a higher percentage of that limit.

CFPB data on credit score factors shows that keeping credit utilization below 30% is one of the most important habits for maintaining a strong score.

Account Age: Closed accounts don’t vanish from your credit history right away. They typically stay on your report for up to 10 years. So closing an older card won’t immediately erase its positive history.

Mix of Credit: Having a variety of open credit accounts is a small factor in your score calculation. Closing one card slightly reduces that mix, but it’s rarely a major issue on its own.

The Bottom Line: For most cardholders, closing a single card that carries no balance has a modest, short-term effect. It’s usually worth doing if the card charges a high annual fee with no real benefits, or if you’re simplifying your finances.

Mistakes That Can Delay or Derail Your Card Closure

Even with a letter in hand, these common errors can slow things down or cause real problems.

1. Sending the letter with an active balance, banks will not close an account if a balance remains. This is the most common reason closures get rejected. Always pay off the full amount first.

2. Forgetting to cancel auto-payments. A gym membership, streaming service, or insurance premium linked to the card can trigger a new charge after you send the letter. That new charge creates a fresh balance and stalls the entire closure.

3. Not asking for written confirmation. Some banks won’t automatically send a confirmation letter unless you request one. Always ask in writing and specify that you want an NOC.

4. Closing your oldest card. Your oldest active credit card helps your score through account age. When choosing which card to close, try to cancel newer accounts before older ones if you can.

5. Not keeping a copy of the letter. Without a copy, you have no record of what you requested or when. This makes any future dispute very difficult to resolve. Keep both a physical copy and a digital scan.

6. Using vague or casual language, a card closure letter is a formal business document. Phrases like “please close my account if possible” weaken your request. Use direct, professional language. Both templates above handle the wording for you.

Tips for a Smooth Credit Card Cancellation

Follow these tips to make the process easier.

- Send the letter via certified mail – This provides proof of delivery. If the bank claims it never received the letter, you have evidence.

- Keep copies of everything – Save a copy of the letter, the tracking number, and any confirmation emails or letters from the bank.

- Follow up – If you do not hear back within two weeks, call the bank. Ask for the status of the card cancellation request.

- Check your credit report – A few months after canceling, review your credit report. Ensure that the system shows the account as closed and updates the account status correctly.

- Be polite – Even if you are frustrated with the bank, maintain a professional tone in your letter. This makes the process smoother.

Frequently Asked Questions

How long does it take for a credit card to be officially closed after sending a letter?

Most banks process credit card closures within 7 to 30 business days. Written confirmation or an NOC typically arrives within 30 to 45 days. If you haven’t heard back by then, send a follow-up letter referencing your original submission date.

Can I submit a cancellation letter if I still have an outstanding balance?

No. Banks will not close a credit card account while a balance remains. Pay off all dues, including any pending EMIs and recurring charges, before submitting your closure request.

What is an NOC, and why should I ask for one?

An NOC (No Objection Certificate) is a bank document. It confirms that your account is closed and your balance is zero. It protects you from future billing disputes and may be required when applying for loans or other credit products.

Does cancelling a credit card lower my credit score?

Closing an account can lower your score temporarily. This happens because it decreases your total available credit and increases your credit utilization ratio. The impact is usually small if your other active accounts are in good standing.

What if I already called to cancel but never sent a written letter?

A phone cancellation may not be fully documented on the bank’s end. Send a written follow-up letter confirming your request. This creates a paper trail and ensures you receive official written confirmation of the closure.

What should I do with my physical credit card after sending the letter?

Cut the card through the chip and magnetic stripe to prevent any further use. Some banks may ask you to return the physical card to a branch. Check your bank’s specific policy before destroying it.

What happens to my reward points when I cancel my credit card?

Most banks forfeit unused reward points once an account is closed. Redeem all points, cashback, or miles before you send your cancellation letter. This way, you won’t lose them for good.

Can I cancel a credit card by email?

Some banks accept email submissions, but only to their official, verified email addresses. Attach a signed PDF of your letter and send it to the bank’s confirmed contact address. Always follow up to confirm they received it.

Conclusion

Sending a credit card cancellation request letter is the best way to close your account. It helps avoid unexpected charges and gives you proof that the account is closed.

The process is straightforward: clear your balance, cancel recurring payments, redeem your rewards, fill out a free template, and submit it with a delivery confirmation. Once the NOC arrives, store it somewhere safe.

Based on everything covered in this guide, submitting in person or via USPS Certified Mail is the most reliable approach for most cardholders, since both methods give you immediate, verifiable proof of delivery.

If you know someone who’s planning to cancel a credit card soon, share this guide with them. A few minutes of proper paperwork can save them weeks of follow-up headaches and billing surprises.